Why Nvidia Stock Is Plummeting Today

Nvidia (NASDAQ: NVDA) stock is getting hit hard in Tuesday’s trading. The semiconductor company’s share price was down 8.7% as of 2:15 p.m. ET, according to data from S&P Global Market Intelligence.

The artificial intelligence (AI) leader’s share price is falling in response to rising concerns about the health of the U.S. economy. News out of China and other geopolitical dynamics are also prompting sell-offs for Nvidia and other chip stocks today.

Investors are feeling jittery ahead of this week’s jobs report

The U.S. Department of Labor is expected to release its latest employment data on Friday, and Wall Street is seeing an uptick in bearish sentiment ahead of the report. Investors have been looking forward to interest-rate cuts that are expected to be delivered by the Federal Reserve this month, and the rate reduction could be larger than many analysts initially expected. But there’s a catch.

Some analysts now expect that the Fed will cut interest rates by a full point this year. If so, that could be a sign that the central banking authority believes the economy is on track for a recession. Investors are bracing for a worrying jobs report at the end of this week, and Nvidia and other high-profile growth stocks are seeing big valuation pullbacks.

Concerns that China will invade Taiwan hit chip stocks, again

In an interview on Sunday, Taiwanese President Lai Ching-te said that China should also move to reclaim land from Russia if it wants to officially make Taiwan its territory. Rather than suggesting that China should take back Russian land that used to be within its own borders, Lai was making a statement about whether the Chinese government was being logically consistent in some of its stated reasons for plans to exert greater control over Taiwan. Nevertheless, it looks like the comments from Taiwan’s president are highlighting the risk that China could invade Taiwan at some point in the not-too-distant future.

While the Chinese government has long made claims that Taiwan is already part of its territory, the contention has taken on added importance in light of the crucial role that Taiwan plays in semiconductor manufacturing and artificial intelligence trends. The island nation is home to Taiwan Semiconductor Manufacturing — the leading contract manufacturer of semiconductors that’s responsible for the fabrication of advanced chips for AI applications. Nvidia relies on TSMC for the fabrication of its chips, and any disruptions to the fab leader’s output could have major implications for the company’s performance.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $731,449!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 3, 2024

Keith Noonan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

Why Nvidia Stock Is Plummeting Today was originally published by The Motley Fool

Nvidia Receives DOJ Subpoena In Antitrust Investigation: What To Know

NVIDIA Corp NVDA shares are trading lower after hours Tuesday after the company received a subpoena from the U.S. Department of Justice (DOJ).

According to a Bloomberg report, the DOJ sent subpoenas to Nvidia and other companies in an escalation of its investigation into possible antitrust law violations by the AI computing giant.

Read Next: What’s Going On With Lululemon Stock After Earnings?

The DOJ is concerned with whether Nvidia penalizes buyers that don’t exclusively use Nvidia chips and if the company is making it difficult for customers to switch to other chip suppliers. According to the report, the investigation is being led by the DOJ’s San Francisco office.

When trying to assess whether or not Nvidia will trade higher from current levels, it’s a good idea to take a look at analyst forecasts.

Wall Street analysts have an average 12-month price target of $152.71 on Nvidia. The Street high target is currently at $200 and the Street low target is $90. Of all the analysts covering Nvidia, 47 have positive ratings, two have neutral ratings and none have negative ratings.

In the past month, 28 analysts have adjusted price targets. Here’s a look at recent price target changes [Analyst Ratings]. Benzinga also tracks Wall Street’s most accurate analysts. Check out how analysts covering Nvidia have performed in recent history.

Stocks don’t move in a straight line. The average stock market return is approximately 10% per year. Nvidia is 124.22% up year-to-date. The average analyst price target suggests the stock could have further upside ahead.

For a broad overview of everything you need to know about Nvidia visit here. If you want to go above and beyond, there’s no better tool to help you do just that than Benzinga Pro. Start your free trial today.

NVDA Price Action: According to Benzinga Pro, Nvidia shares are down 2.13% after-hours at $105.70 after falling 9.53% during regular trading Tuesday.

Read Also:

Image: Shutterstock

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

3 High-Yield Dividend Stocks That Are Screaming Buys in September

High-yielding dividend stocks have underperformed in recent years. Higher interest rates have weighed down many.

However, that could be about to change, given the expectations that the Federal Reserve will start cutting interest rates soon. That’s left several high-quality, high-yield dividend stocks looking like screaming buys this September for those seeking income and upside potential. Three top ones to buy this month are Kinder Morgan (NYSE: KMI), Brookfield Renewable (NYSE: BEPC)(NYSE: BEP), and Enbridge (NYSE: ENB).

Plenty of gas to continue growing

Kinder Morgan currently yields over 5%. That’s several times higher than the S&P 500‘s dividend yield of less than 1.5%. The primary reason is Kinder Morgan’s dirt cheap valuation.

The natural gas pipeline giant expects to produce around $2.26 per share of distributable free cash flow this year. With its share price recently around $21.50 apiece, it trades at less than 10 times earnings. That’s significantly cheaper than the S&P 500’s 24.

Kinder Morgan might not stay that cheap for long if the Fed starts raising rates. However, that’s not Kinder Morgan’s only upside catalyst. The pipeline company retains about half its cash flow after paying dividends, which it uses to grow shareholder value by investing in high-return capital projects, repurchasing shares, and enhancing its financial flexibility. The company currently has about $5.2 billion of high-return capital projects under construction, half of which will come online by the end of next year. The growing cash flow from those capital projects will give it more fuel to increase its dividend, which it has done for seven straight years.

Powerful potential

Brookfield Renewable currently yields around 5%. The leading global renewable energy producer generates lots of stable cash flow to pay dividends. It produced $0.96 per share of funds from operations (FFO) during the first half of this year, about 75% of which it paid out in dividends. Annualize its FFO and Brookfield trades at 15 times earnings, given its recent share price at around $28.50.

The company is dirt cheap compared with the broader market and its growth potential. Brookfield Renewable expects several catalysts to grow its FFO per share by more than 10% annually through 2028. That should give it the power to increase its dividend by 5% to 9% annually. The company has grown its payout at a 6% compound annual rate over the past two decades.

Brookfield Renewable has significant long-term upside potential, given the accelerating demand for power, especially renewable energy. The world needs to deploy an unprecedented amount of electricity-generating capacity over the next 20 years to power electric vehicles, homes, businesses, and new technologies like AI. The market is severely underestimating this opportunity, which could power robust growth for Brookfield Renewable for decades to come.

The fuel to keep its streak alive

Enbridge currently yields more than 6.5%. The Canadian pipeline and utility company generates lots of stable cash flow to pay dividends. It expects to produce about $5.60 Canadian, or $4.15, of distributable cash flow per share this year at the mid-point of its outlook. With its share price right around $40, it trades at less than 10 times free cash flow.

The company pays out 60% to 70% of its stable cash flow in dividends. It retains the rest to fund expansion projects and maintain its financial flexibility. The company has a massive CA$24 billion ($17.8 billion) of capital projects currently under construction that should come online through 2028. Those projects include additional oil storage and export capacity, natural gas pipelines, gas utility expansions, and renewable-energy projects.

Enbridge expects a combination of expansion projects, cost savings and optimizations, and acquisitions to fuel 3% annual cash flow per share growth through 2026 and 5% per year after that. That should give the company the fuel to continue increasing its dividend by as much as 5% annually. It’s managed to raise its payout for 29 straight years.

Bargain buys this September

Because Kinder Morgan, Brookfield Renewable, and Enbridge trade at dirt cheap valuations, they offer high dividend yields and upside potential. They could easily generate double-digit total annual returns from here. That compelling combination makes them look like screaming buys this September.

Should you invest $1,000 in Kinder Morgan right now?

Before you buy stock in Kinder Morgan, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Kinder Morgan wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $731,449!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 26, 2024

Matt DiLallo has positions in Brookfield Renewable, Brookfield Renewable Partners, Enbridge, and Kinder Morgan. The Motley Fool has positions in and recommends Brookfield Renewable, Enbridge, and Kinder Morgan. The Motley Fool recommends Brookfield Renewable Partners. The Motley Fool has a disclosure policy.

3 High-Yield Dividend Stocks That Are Screaming Buys in September was originally published by The Motley Fool

Why stocks could drop 10% over the next 8 weeks, according to a bullish forecaster who's nailed his calls this year

-

Stocks could pull back as much as 10% in the next eight weeks, Fundstrat’s Tom Lee said.

-

He told CNBC that investors should be cautious ahead of Fed interest-rate cuts and the election.

-

Lee says the sell-off will be an ideal time to buy the dip.

Stocks are facing a possible double-digit drawback in the next eight weeks as a slew of market-moving events temporarily challenge this year’s gains, Fundstrat’s Tom Lee told CNBC.

Lee suggested that the market could fall between 7% to 10%, and recommended that investors gear up for elevated turbulence.

“I think investors should be cautious for the next eight weeks,” the typically bullish investor said. “Market’s been up seven of the eight months this year. So we know it’s an incredibly strong market. But we also have the September cuts, and we have the election: things that’ll get people nervous.”

That’s partly a reference to the Federal Reserve’s upcoming policy meeting in mid-September, during which the central bank is expected to slash interest rates by at least 25 basis points.

Analysts have separately indicated that the market might not welcome deeper cuts. Bank of America wrote on Tuesday that if the Fed had to cut by 50 basis points instead, this would likely be in response to elevated recession risk.

Friday’s jobs report will determine the Fed’s decision later this month, with some on Wall Street fearing it may come in weaker than expected. But Lee cited that a pullback could ensue even if it beats forecasts, as investors readjust interest rate outlooks.

“If it’s too strong and investors worry and so the stock market’s down Friday, I’d be buying that dip,” he told the outlet.

Lee has been largely on the mark with his stock market calls in 2024, heading into the year as one of Wall Street’s bullish forecasters. His optimism has been met in the form of an 18% year-to-date gain for the S&P 500 through Friday.

Meanwhile, election uncertainty may put off investors until the results are known, experts told Business Insider.

Even outside an election year, September is a challenging month for stocks in a non-election year. But when voters head to the polls, seasonal volatility can extend as far as mid-October. SoFi’s Liz Young Thomas told the outlet.

There’s a silver lining: investors can expect a relief rally once a president is chosen, she said.

Lee similarly cited that the “tough” weeks ahead should be viewed as a buying opportunity.

“I think in the next eight weeks, people get a chance to buy,” he told CNBC. “I think it’s good to be cautious, but just ready to buy that dip.”

The strategist has been one of the market’s staunchest bulls. In June, he argued that the S&P 500 could triple this decade, reaching 15,000 by 2030.

Read the original article on Business Insider

Stock market today: Dow slides 600 points, Nasdaq sinks 3% as Nvidia leads chip sell-off

Investors began September trading with a thud as stocks tumbled on Tuesday to start a historically tough month for markets, with AI darling Nvidia (NVDA) and chip names leading tech stocks down. The turn into the red comes amid a crucial week of data on the economy and labor market highlighted by an influential monthly jobs report.

The Dow Jones Industrial Average (^DJI) slid 1.5%, or over 600 points. The S&P 500 (^GSPC) dropped 2.1%, while the tech-heavy Nasdaq Composite (^IXIC) pulled back 3.3%.

Stocks are retreating from near highs as Wall Street hunkers down after a rollercoaster August, with the prospect of a potentially stormy September ahead. Investors are assessing the risk of data shocks or presidential race surprises in a month that’s typically terrible for traders.

Nvidia (NVDA) fell almost 10% Tuesday, as investors continue to withdraw following a lackluster earnings report and lingering questions about the future of the AI trade. Other chip stocks fell in tandem, with Broadcom (AVGO), Qualcomm (QCOM), and Taiwan Semiconductor Manufacturing Company (TSM) all down more than 6%.

Also top of mind is the August jobs report, due out on Friday, which could influence how deeply the Federal Reserve cuts interest rates at its meeting this month. With inflation now cooling, policymakers are on alert for the labor market to fall into place.

For investors, the focus is on whether the signs of slowing in the July jobs report were overstated — or an early warning of a broader slowdown. Any hints of stress should put pressure on the Fed to make a bigger reduction in rates. As of Tuesday, traders were pricing in 39% odds of a 50 basis point cut instead of 25 basis points, per the CME FedWatch Tool.

A measure of US manufacturing ticked up last month, according to fresh figures from the Institute for Supply Management (ISM). But the metric reflected slowed factory activity, with a reading below a threshold that suggests a contraction in the manufacturing sector.

LIVE COVERAGE IS OVER10 updates

3 Fantastic Stocks That Could Join The S&P 500 by 2025

Ever wondered why some stocks are in the S&P 500 and others aren’t? Well, it turns out there’s a very specific set of criteria that must be met for a stock to gain entry into the index, which will be revealed below.

But now, three Fool.com contributors will name their top stocks that could be added to the index by 2025. Let’s dive right in.

Palantir meets all the criteria for inclusion in the S&P 500

Jake Lerch (Palantir Technologies): My choice as a stock that could join the S&P 500 by next year is Palantir Technologies (NYSE: PLTR). Palantir is the maker of an AI-powered platform that helps organizations understand complex datasets, and the company’s stock is red-hot.

So far this year, Palantir stock is up a remarkable 80%. Its market cap is now $68 billion, making the AI stock America’s 279th-largest public company by market cap. Yet, as of this writing, Palantir is still not a member of the S&P 500.

So what gives?

It’s a good question because Palantir checks all of the boxes needed for inclusion in the S&P 500:

-

A U.S. Company

-

Market cap of at least $18 billion

-

Stock is highly liquid

-

Public float is at least 50% of total shares outstanding

-

Positive earnings in its most recent quarter and total positive earnings in the four most recent quarters

First off, Palantir is based in the U.S. and has a market cap of nearly $70 billion — check.

Second, Palantir’s stock is highly liquid; its public float is well over 50% of its outstanding shares available.

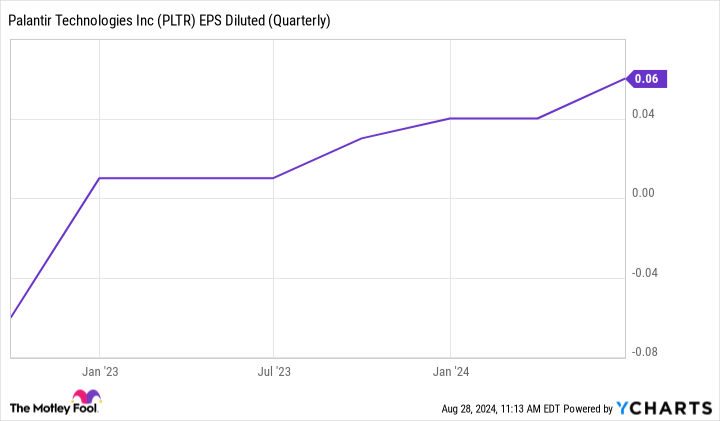

Finally, we come to profitability. Profitability, in all likelihood, is why Palantir is not in the S&P 500. While the company has reported positive earnings in each of the last six quarters, they have been tiny profits.

As you can see above, Palantir had quarterly losses as recently as late 2022. Because of that, the committee has likely delayed putting Palantir into the S&P 500 — waiting to see more quarters of positive earnings before giving Palantir the nod.

However, one more quarter of positive earnings might be enough to lead to the committee adding Palantir to the index by 2025. And that’s exactly what I think will happen.

S&P 500 inclusion might help make this company the next great advertising stock

Will Healy (The Trade Desk): Mega-cap tech stocks like Alphabet (NASDAQ: GOOGL) (NASDAQ: GOOG) and Meta Platforms (NASDAQ: META) have built their fortunes on digital advertising. These companies generate tens of billions in revenue every quarter by helping businesses of all sizes reach desired audiences, and that market power makes them mainstays of the S&P 500.

Amid the influence of this industry, the next advertising stock to enter the S&P 500 might just be The Trade Desk (NASDAQ: TTD). Its demand-side platform allows agencies and companies to manage digital ad campaigns, running ads in the times and places where they believe they can generate the highest returns. Additionally, with the help of AI tool Kokai, users can further refine the timing and placement of ads to derive more value.

Thanks to its capabilities, it has become a stock with a $50 billion market cap, far above the minimum market cap required to enter the S&P 500. From that point, its financials will likely help boost this stock further.

Revenue for the first half of 2024 was just under $1.1 billion, a 27% increase compared with the same period last year. The company has also recovered from an earnings slump it faced in 2022. With that, its net income was $117 million in the first six months of 2024, rising 176% compared with year-ago levels.

Amid these fast-rising profits, its 205 price-to-earnings (P/E) ratio is likely not representative of its valuation, but its price-to-sales (P/S) ratio of 24 admittedly makes it expensive. Still, analysts forecast 26% revenue growth this year and 20% in 2025, meaning revenues will continue to place downward pressure on its sales multiple.

Finally, investors should remember what inclusion in the index means — a place in the portfolio of every investor who invests in the S&P 500 through index funds. That rising influence should further bolster the stock as more advertisers turn to its platform.

Coinbase would give the S&P 500 exposure to cryptocurrency’s potential upside.

Justin Pope (Coinbase): If the S&P 500 is going to look to innovation and add AI tech companies such as CrowdStrike and Super Micro Computer into the index, it makes perfect sense to add Coinbase (NASDAQ: COIN), too. Cryptocurrencies are still hotly debated among investors, but the asset class is forcing its way into the conversation. According to research by The Motley Fool, approximately one-quarter of investors are “very likely” to buy at least some form of cryptocurrency.

The case for Coinbase is simple. It’s a publicly traded U.S. company, making it arguably the safest exchange and crypto-finance company after fraud and controversy have tainted or destroyed private and foreign competitors like Binance and FTX.

Next, it easily meets the criteria for inclusion in the S&P 500; its current $42 billion market cap meets the minimum threshold. Plus, it is comfortably GAAP profitable, with almost $1.4 billion in net income over the past four quarters.

Most importantly, it’s a fantastic business. Coinbase’s exchange is its core business, but its ambitions span the crypto economy, including financial products such as banking and payment cards that allow users to spend their crypto as dollars. Cryptocurrency can be cyclical, but Coinbase has proven it can endure the downturns. The company is also in a great financial position, with over $8 billion in cash on its balance sheet, nearly a fifth of the stock’s value.

Cryptocurrencies must continue to gain adoption among society and investors for Coinbase’s business to grow over the long term. However, there isn’t a better stock for exposure to crypto’s potential upside. Adding Coinbase to the S&P 500 would reflect a forward-thinking investment strategy and help lift the index higher over the coming years if cryptocurrency continues gaining steam.

Should you invest $1,000 in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $731,449!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 3, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Jake Lerch has positions in Alphabet and CrowdStrike. Justin Pope has no position in any of the stocks mentioned. Will Healy has positions in CrowdStrike, Palantir Technologies, Super Micro Computer, and The Trade Desk. The Motley Fool has positions in and recommends Alphabet, Coinbase Global, CrowdStrike, Meta Platforms, Palantir Technologies, and The Trade Desk. The Motley Fool has a disclosure policy.

3 Fantastic Stocks That Could Join The S&P 500 by 2025 was originally published by The Motley Fool

Madison Covered Call and Equity Strategy Fund (MCN) Declares Quarterly Dividend

MADISON, Wis., Sept. 03, 2024 (GLOBE NEWSWIRE) — The Madison Covered Call and Equity Strategy Fund MCN (the “Fund”) declares its quarterly dividend of $0.18/share. The dividends will be payable September 30, 2024, to shareholders of record on September 17, 2024. The ex-dividend date will be September 17, 2024. If it is determined that a notification is required pursuant to Section 19(a) of the Investment Company Act of 1940, as amended, such notice will be posted to the Fund’s website after the close of business three business days before the payable date. If a distribution rate is largely comprised of sources other than income, it may not reflect Fund performance.

The Fund’s objective is to achieve a high level of current income and current capital gains, with long-term capital appreciation as a secondary objective. The Fund intends to pursue its objective by investing in a portfolio of common stocks and utilizing an option strategy, primarily by writing (selling) covered call options on a substantial portion of the common stocks in the portfolio in order to generate current income and gains from option writing premiums and, to a lesser extent, from dividends. Market action can impact dividend issuance as the Fund’s total assets affect the Fund’s future dividend prospects. The Fund provides additional information on its website at www.madisonfunds.com.

Certain statements in this release are forward-looking. The Fund’s actual results may differ from current expectations or projections due to numerous factors, including but not limited to changes in the equity markets, changes in the portfolio’s value and other risks generally discussed in the Fund’s filings with the SEC. Neither the Fund nor Madison undertakes any obligation to publicly update or revise any forward-looking statements.

“Madison” and/or “Madison Investments” is the unifying tradename of Madison Investment Holdings, Inc., Madison Asset Management, LLC (“MAM”), and Madison Investment Advisors, LLC (“MIA”). MAM and MIA are registered as investment advisers with the U.S. Securities and Exchange Commission. Madison Funds are distributed by MFD Distributor, LLC. MFD Distributor, LLC is registered with the U.S. Securities and Exchange Commission as a broker-dealer and is a member firm of the Financial Industry Regulatory Authority. The home office for each firm listed above is 550 Science Drive, Madison, WI 53711. Madison’s toll-free number is 800-767-0300.

CONTACT:

Madison

Greg Hoppe: gregh@madisonadv.com

800-767-0300

![]()

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Asana Partners Promotes Clare Walsh to Managing Director

CHARLOTTE, N.C., Sept. 3, 2024 /PRNewswire/ — Asana Partners, a retail-focused real estate private equity firm, today announced that Clare Walsh has been promoted to Managing Director.

![]()

In her role as Managing Director, Walsh will oversee retail leasing strategy and execution in addition to her continued role on the firm’s Investment Committee.

Walsh joined Asana Partners in 2018 as Director — Leasing Strategy and has more than 14 years of experience in retail leasing. Prior to joining Asana Partners, Walsh was a Senior Leasing Representative at Brookfield Properties Retail Group (BPRG), where she led restaurant leasing efforts in the Western region. Prior to BPRG, Walsh worked for EDENS, a privately held REIT, where she was responsible for retail leasing efforts in the Mid-Atlantic region.

“Clare assumed overall leadership of retail leasing in 2022 and is a well-respected leader within the firm, throughout the retail marketplace, and with our investors,” said Sam Judd, Managing Partner. “Clare’s creative vision and deep relationships with top retailers have been instrumental in the successful activation of countless neighborhoods throughout the United States.”

Walsh graduated from American University with a Bachelor of Arts in International Business and Marketing and is an active member of the International Council of Shopping Centers.

About Asana Partners

Asana Partners is a retail real estate investment firm creating value in vibrant neighborhoods by leveraging vertically integrated capabilities and retail expertise. With more than $7 billion of neighborhood assets under management, the firm is active in growth markets throughout the United States and is driven to make a positive impact within communities. Asana Partners champions a strong collaborative culture with offices in Charlotte, Columbia, Atlanta, Los Angeles, Denver, Boston, and New York. For more information, visit www.asanapartners.com or follow @asanapartners.

Media Contact

Julie Ducworth: (803) 465-1198; julie@jcdcommunications.com

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/asana-partners-promotes-clare-walsh-to-managing-director-302237180.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/asana-partners-promotes-clare-walsh-to-managing-director-302237180.html

SOURCE Asana Partners

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.