MSCI Shares Up 7% in a Year: Should You Buy, Hold or Sell the Stock?

MSCI MSCI shares moved up 6.7% in the past year compared with the broader Zacks Computer and Technology sector’s return of 39.8% and the Zacks Business – Software Services sector’s rise of 29.2%.

The underperformance is likely to have been caused by a tighter spending environment and longer sales cycles due to challenging macroeconomic conditions.

Increasing pricing pressure is also a major concern, primarily due to the growing availability of free indices from providers like Morningstar MORN.

As Morningstar continues to offer more accessible options, self-indexing and lower spending by asset managers on gathering data are other headwinds.

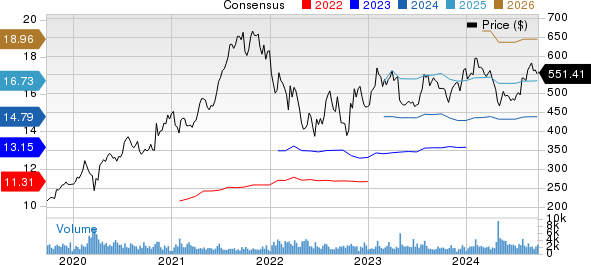

MSCI Inc Price and Consensus

MSCI Inc price-consensus-chart | MSCI Inc Quote

Despite these challenges, MSCI is benefiting from strong demand for custom and factor index modules, recurring revenue business models and the growing adoption of its ESG and Climate solutions in the investment process.

Hence, investors should ask this question — is now the right time to invest in MSCI’s shares given the current market challenges and MSCI’s performance?

Will MSCI’s Strong Portfolio Drive Growth?

MSCI’s expanding portfolio along with robust adoption of its Climate and ESG solutions, have been a major growth driver.

In July, the company announced a partnership with Moody’s, marking a milestone in advancing ESG (Environmental, Social and Governance) transparency in financial markets.

MSCI announced a partnership with Moody’s. The partnership will leverage MSCI’s robust sustainability data and models, widely utilized by major asset managers worldwide, to bolster Moody’s offerings across banking, insurance and corporate sectors.

Moody’s will also integrate MSCI’s industry-leading ESG ratings and content into its solutions, gradually replacing its own ESG data offerings. The agreement also entails MSCI gaining access to Moody’s extensive Orbis database, paving the way for expanded private company ESG coverage and exploration into advanced solutions for the private credit market.

MSCI’s partnership with Microsoft has further expanded its clientele and is considered a major positive for the company.

The partnership with Microsoft aims to enhance the global investment industry by leveraging Microsoft’s cloud and AI technologies to modernize MSCI’s products and drive ESG solutions.

In second-quarter 2024, MSCI achieved 10% organic revenue growth, driven by strong performance across various segments, including Analytics, ESG and Index Investments. The company witnessed growth in its ESG and Climate solutions, with organic run rate growth of 14%.

Acquisitions have also played a significant role in shaping the company’s growth trajectory. In April, MSCI completed the acquisition of Foxberry, a London-based index provider, aimed at enhancing custom index production capabilities and providing simulation and back-testing capabilities for institutional investors.

MSCI’s Earnings Estimates Show Upward Movement

MSCI’s diverse portfolio and strategic acquisitions are contributing to its growth prospects continuously and driving top-line growth.

The Zacks Consensus Estimate for third-quarter 2024 revenues is currently pegged at $710.74 million, suggesting 13.64% growth year over year.

The consensus mark for earnings is currently pegged at $3.75 per share, unchanged in the past 30 days.

MSCI Shares are Overvalued

MSCI stock is not so cheap, as the Value Score of D suggests a stretched valuation at this moment.

The forward 12-month Price/Sales ratio for MSCI stands at 16.16X, higher than its Zacks Business – Software Services industry’s 11.26X, reflecting a stretched valuation.

MSCI currently carries Zacks Rank #3 (Hold), suggesting that it may be wise to wait for a more favorable entry point in the stock.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Leave a Reply