A Peek at Ally Financial's Future Earnings

Ally Financial ALLY will release its quarterly earnings report on Friday, 2024-10-18. Here’s a brief overview for investors ahead of the announcement.

Analysts anticipate Ally Financial to report an earnings per share (EPS) of $0.53.

Anticipation surrounds Ally Financial’s announcement, with investors hoping to hear about both surpassing estimates and receiving positive guidance for the next quarter.

New investors should understand that while earnings performance is important, market reactions are often driven by guidance.

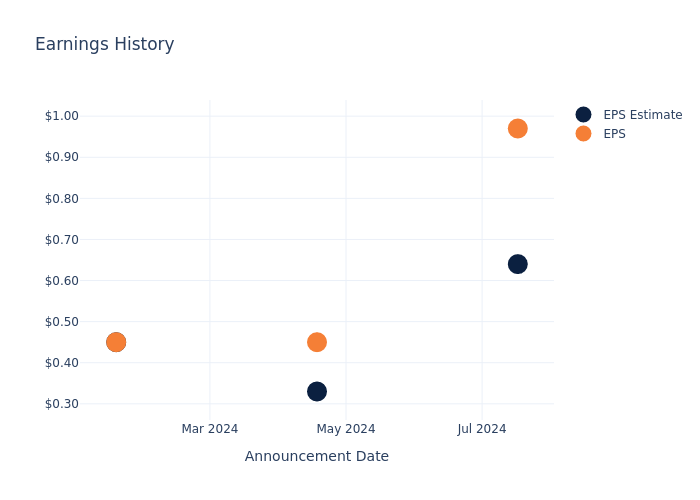

Earnings Track Record

The company’s EPS beat by $0.33 in the last quarter, leading to a 2.28% drop in the share price on the following day.

Here’s a look at Ally Financial’s past performance and the resulting price change:

| Quarter | Q2 2024 | Q1 2024 | Q4 2023 | Q3 2023 |

|---|---|---|---|---|

| EPS Estimate | 0.64 | 0.33 | 0.45 | 0.80 |

| EPS Actual | 0.97 | 0.45 | 0.45 | 0.83 |

| Price Change % | -2.0% | 1.0% | 11.0% | -4.0% |

Tracking Ally Financial’s Stock Performance

Shares of Ally Financial were trading at $35.94 as of October 16. Over the last 52-week period, shares are up 49.65%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

Analyst Opinions on Ally Financial

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on Ally Financial.

The consensus rating for Ally Financial is Outperform, based on 9 analyst ratings. With an average one-year price target of $38.78, there’s a potential 7.9% upside.

Peer Ratings Comparison

The analysis below examines the analyst ratings and average 1-year price targets of and Enova International, three significant industry players, providing valuable insights into their relative performance expectations and market positioning.

- The consensus among analysts is an Outperform trajectory for Enova International, with an average 1-year price target of $90.5, indicating a potential 151.81% upside.

Snapshot: Peer Analysis

The peer analysis summary offers a detailed examination of key metrics for and Enova International, providing valuable insights into their respective standings within the industry and their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Credit Acceptance | Sell | 12.42% | $330.70M | -2.94% |

| Enova International | Outperform | 25.83% | $299.24M | 4.69% |

Key Takeaway:

Ally Financial ranks higher than its peers in Revenue Growth and Gross Profit, indicating stronger performance in these areas. However, it lags behind in Consensus and Return on Equity metrics compared to its peers.

Delving into Ally Financial’s Background

Formerly the captive financial arm of General Motors, Ally Financial became an independent publicly traded firm in 2014 and is one of the largest consumer auto lenders in the country. While the firm has expanded its product offerings over time, it remains primarily focused on auto lending with more than 70% of its loan book in consumer auto loans and dealer financing. Ally also offers auto insurance, commercial loans, credit cards, and holds a portfolio of mortgage debt, giving the bank a diversified business model, which includes brokerage services.

Financial Insights: Ally Financial

Market Capitalization Analysis: Reflecting a smaller scale, the company’s market capitalization is positioned below industry averages. This could be attributed to factors such as growth expectations or operational capacity.

Decline in Revenue: Over the 3 months period, Ally Financial faced challenges, resulting in a decline of approximately -4.37% in revenue growth as of 30 June, 2024. This signifies a reduction in the company’s top-line earnings. When compared to others in the Financials sector, the company faces challenges, achieving a growth rate lower than the average among peers.

Net Margin: Ally Financial’s net margin is impressive, surpassing industry averages. With a net margin of 12.29%, the company demonstrates strong profitability and effective cost management.

Return on Equity (ROE): Ally Financial’s ROE falls below industry averages, indicating challenges in efficiently using equity capital. With an ROE of 2.33%, the company may face hurdles in generating optimal returns for shareholders.

Return on Assets (ROA): Ally Financial’s ROA lags behind industry averages, suggesting challenges in maximizing returns from its assets. With an ROA of 0.14%, the company may face hurdles in achieving optimal financial performance.

Debt Management: Ally Financial’s debt-to-equity ratio is below the industry average. With a ratio of 1.53, the company relies less on debt financing, maintaining a healthier balance between debt and equity, which can be viewed positively by investors.

To track all earnings releases for Ally Financial visit their earnings calendar on our site.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Leave a Reply