Billionaire Philippe Laffont Sold Coatue's Entire Stake in Palantir and Is Piling Into an Electrifying Growth Stock Instead

On Wall Street, investors are never hurting for data. We’re currently kicking off a six-week period (affably known as “earnings season”) where a majority of S&P 500 companies will lift the hood on their most recent quarterly operating performance. In addition to a barrage of operating results, economic data releases occur almost every day. It can be easy to miss something important.

On Aug. 14, you may have missed what can easily be described as the most pivotal data release of the third quarter. This date marked the filing deadline for institutional investors with at least $100 million in assets under management (AUM) to file Form 13F with the Securities and Exchange Commission. A 13F provides investors with a concise snapshot of what Wall Street’s brightest and historically successful money managers purchased and sold in the latest quarter (in this case, the June-ended quarter).

Although Berkshire Hathaway‘s Warren Buffett is arguably the most-followed of all billionaire asset managers, there are more than a dozen high-profile billionaire money managers that garner a lot of attention, including Coatue Management’s Philippe Laffont.

Laffont’s hedge fund, which is primarily focused on game-changing tech stocks, closed out June with approximately $25.7 billion in AUM spread across 74 holdings.

What might come as a bit of a surprise to investors is that Laffont was a big-time seller of one of Wall Street’s hottest artificial intelligence (AI) stocks, Palantir Technologies (NYSE: PLTR). While Coatue’s brightest minds, including Laffont, we’re showing Palantir to the door, they were piling into a growth stock that stands out in a notoriously slow-growing sector.

Laffont completely exited Coatue’s stake in Palantir

Let me preface the following discussion by pointing out that Coatue Management is an actively managed fund. The average top-10 holding has been held for less than a year. Further, Laffont reduced his fund’s stake in 30 companies and completely sold out of 23 during the second quarter. In other words, Palantir was far from the only stock to be sent to the chopping block.

Nevertheless, the 4,816,195 shares sold by Coatue marked one of the largest shares sales of Palantir stock during the June-ended quarter.

Profit-taking is the most-logical reason Laffont and his team may have chosen to ring the register. Palantir had been a continuous holding for Coatue since the first quarter of 2023. At that time, shares could have been purchased for roughly $8. With Palantir’s stock hovering in the low-$20s during the second quarter, it looks as if Coatue banked a triple-digit gain on its initial stake.

Laffont may have also been skittish about Palantir’s premium valuation. On one hand, there is no substitute for the company’s AI-driven Gotham platform, which helps federal governments plan missions and collect data, or its enterprise-focused Foundry platform. Irreplaceability at scale is a trait that investors will gladly pay a premium for on Wall Street.

On the other hand, Palantir’s stock is currently near an all-time high and valued at almost 100 times forward-year earnings and 29 times forward-year sales. These are eye-popping multiples for a company growing sales by roughly 20% per year. Though Foundry has the potential to reaccelerate growth for Palantir in the future, the company’s valuation premium right now is borderline unjustifiable.

Despite being an artificial intelligence bull, the third reason Laffont may have chosen to dump Coatue’s entire stake in Palantir is the possibility of an AI bubble brewing.

Since the internet began going mainstream roughly three decades ago, there hasn’t been a game-changing technology that’s avoided an early stage bubble. Without fail, investors overestimate how quickly new innovations, trends, or technologies will be utilized by consumers and/or businesses. This recipe eventually leads to disappointment and a bubble-bursting event.

Although direct AI players, such as Nvidia, would be hit the hardest if the AI bubble bursts, Palantir is likely to be hampered by a slowdown in Ai-related spending.

Laffont’s Coatue Management is piling into this electrifying growth stock

But while Laffont and his team were busy sending shares of Palantir to the chopping block, they were avid buyers of America’s leading electric utility, NextEra Energy (NYSE: NEE).

During the June-ended quarter, Laffont’s fund gobbled up 282,544 additional shares of NextEra, which increased Coatue’s stake by 36% in three months to 1,066,083 shares. If this position remained static during the third quarter, it’d be worth more than $88 million, as of the closing bell on Oct. 15.

Traditionally, the utility sector is slow-growing and, for lack of a better word, boring. Investors buy utility stocks for their dividends and the consistency of their cash flow. It’s a sector that tends to outperform during periods of economic uncertainty and low interest rates.

However, seemingly none of this applies to NextEra Energy, which has delivered consistent high-single-digit earnings growth for more than a decade.

The factor that’s differentiated NextEra from the dozens of other publicly traded, slow-growing utilities is its focus on renewable energy. Management laid out a plan to invest a cumulative $85 billion to $95 billion in American infrastructure between 2022 and 2025, a majority of which is tied to clean-energy resources.

As of June 2024, the company had 72 gigawatts (GW) in capacity, 34 GW of which can be traced back to its renewable energy portfolio. No electric utility in the world is generating more capacity from solar or wind power than NextEra.

While investing in the future hasn’t been cheap, it’s notably reduced the company’s electricity generation costs and provided a tangible lift to the company’s bottom line and dividends. If future policy proposals from Capitol Hill necessitate a green shift for America’s electric utilities, NextEra would be miles ahead of the curve.

In addition to low-cost generation and a superior growth rate to its peers, NextEra still enjoys the advantages that come with being an electric utility. This includes being a monopoly or duopoly in the areas it services and generating predictable cash flow year after year.

The final thing worth mentioning about NextEra is that the other half of its 72 GW in capacity — i.e., its traditional electric utility operations, via Florida Power & Light, which aren’t powered by renewables — is regulated by the Florida Public Service Commission (FPSC). The advantage of being a regulated utility and needing approval from the FPSC to raise rates is that it ensures no exposure to wholesale electricity pricing.

NextEra Energy may not be a traditional “growth” stock, but it has a lengthy track record of delivering for its shareholders.

Should you invest $1,000 in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $806,459!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 14, 2024

Sean Williams has positions in NextEra Energy. The Motley Fool has positions in and recommends Berkshire Hathaway, NextEra Energy, Nvidia, and Palantir Technologies. The Motley Fool has a disclosure policy.

Billionaire Philippe Laffont Sold Coatue’s Entire Stake in Palantir and Is Piling Into an Electrifying Growth Stock Instead was originally published by The Motley Fool

Netflix earnings, subscriber growth top estimates as investors eye potential price hikes

Netflix (NFLX) stock rose as much as 5% in after-hours trading Thursday as the streaming giant beat third quarter EPS and revenue estimates and projected sales for the current quarter that came in ahead of Wall Street’s expectations.

Revenue beat Bloomberg consensus estimates of $9.78 billion to hit $9.83 billion in Q3, an increase of 15% compared to the same period last year, as the streamer continued to lean on revenue initiatives like its crackdown on password sharing and ad-supported tier, in addition to last year’s price hikes on certain subscription plans.

Netflix guided to fourth quarter revenue of $10.13 billion, a beat compared to consensus estimates of $10.01 billion.

For full-year 2025, the company sees revenue hitting between $43 billion and $44 billion compared to consensus estimates of $43.4 billion. This would represent growth of 11% to 13% from the company’s expected 2024 revenue guidance of $38.9 billion.

It expects full-year operating margins to hit 27%, an increase from the previous 26%, after the metric hit nearly 30% in the third quarter.

Diluted earnings per share (EPS) also beat estimates in the quarter, with the company reporting EPS of $5.40, above consensus expectations of $5.16 and well ahead of the $3.73 EPS figure it reported in the year-ago period. Netflix guided to fourth quarter EPS of $4.23, ahead of consensus calls for $3.90.

Subscribers also came in strong with another 5 million-plus subscribers added on the heels of breakout programming like “The Perfect Couple” and “Nobody Wants This.”

Subscriber additions of 5.07 million beat expectations of 4.5 million and follows the 8.05 million net additions the streamer added in the second quarter. The company had added 8.8 million paying users in Q3 2023.

“We expect paid net additions to be higher in Q4 than in Q3’24 due to normal seasonality and a strong content slate,” the company said, citing upcoming releases like “Squid Game” Season 2, the Jake Paul vs. Mike Tyson fight, and two NFL games on Christmas Day.

Investors have praised the company’s foray into sports and live events. Meanwhile, its ad tier continues to gain traction, accounting for over 50% of sign-ups in the countries where it’s offered during the third quarter.

“We continue to build our advertising business and improve our offering for advertisers,” the company said in the earnings release. “Ads membership was up 35% quarter on quarter, and our ad tech platform is on track to launch in Canada in Q4 and more broadly in 2025.”

Last quarter, Netflix revealed it secured “a 150% plus increase in upfront ad sales commitments over 2023.” The company has previously said its goal is to make ads “a more substantial revenue stream that contributes to sustained, healthy revenue growth in 2025 and beyond.”

On the earnings call, Netflix co-CEO Greg Peters said that while ads won’t be a primary driver of revenue next year as “we’re still scaling that audience and that inventory faster than our ability to monetize it,” the company sees an “opportunity to close that gap.”

Leading up to the results, Netflix’s stock had been on a tear, with shares up around 45% since the start of the year and trading near all-time highs.

Analysts expect another price hike by the end of the year, which will likely serve as yet another catalyst for shares. But the stock’s recent run-up has led to some apprehension on Wall Street.

Price hike to come?

The company recently revealed subscribers watched over 94 billion hours on the platform from January to June as part of its latest biannual viewership report, although year-over-year engagement levels came in roughly flat — a potential headwind when it comes to pricing power, which has become especially important for streaming companies as consumers become more picky.

On average, US consumers subscribe to four streaming services and spend about $61 per month, according to the latest Digital Media Trends report from Deloitte. Retaining loyal subscribers over time is a challenge due to consumers churning out of, or canceling, their subscription plans.

Netflix last raised the price of its Standard plan in January 2022, upping the monthly cost to $15.49 from $13.99. It also raised the price of its Premium tier by $2 to $19.99 a month at the same time; the company again raised the cost of that plan last October to $22.99.

The company has yet to raise the price of its ad-supported offering, introduced less than two years ago, which remains one of the cheapest ad plans among all of the major streaming players at $6.99 a month.

“Given Netflix’s low cost per viewed hour, we see scope for the firm to raise US prices by 12% in 2025,” Citi analyst Jason Bazinet said ahead of the report.

The company recently phased out its lowest-priced ad-free streaming plan, making the $15.49 Standard plan its cheapest offering for an ad-free experience.

Alexandra Canal is a Senior Reporter at Yahoo Finance. Follow her on X @allie_canal, LinkedIn, and email her at alexandra.canal@yahoofinance.com.

Click here for the latest stock market news and in-depth analysis, including events that move stocks

Read the latest financial and business news from Yahoo Finance.

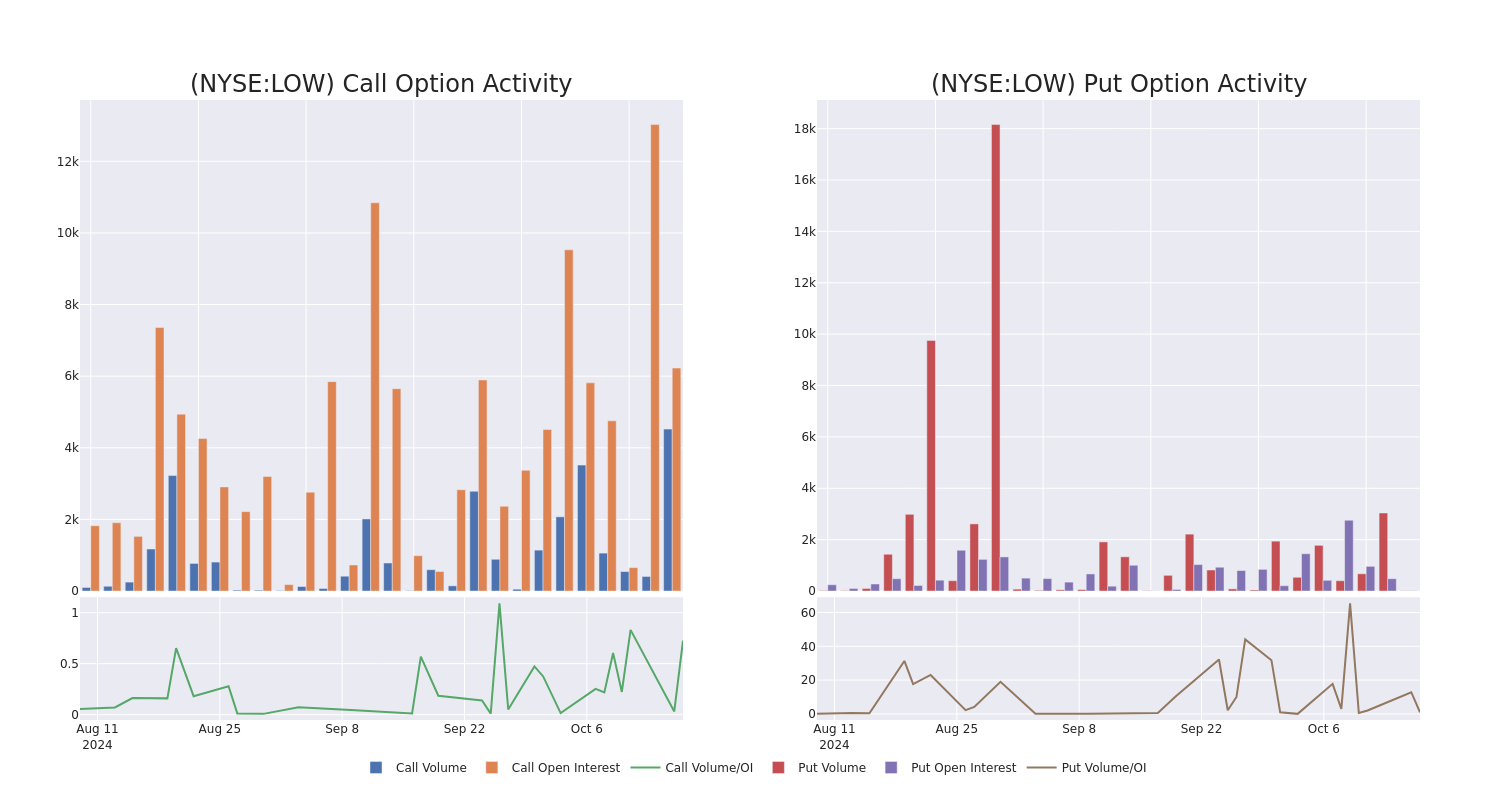

Decoding Lowe's Companies's Options Activity: What's the Big Picture?

High-rolling investors have positioned themselves bearish on Lowe’s Companies LOW, and it’s important for retail traders to take note.

This activity came to our attention today through Benzinga’s tracking of publicly available options data. The identities of these investors are uncertain, but such a significant move in LOW often signals that someone has privileged information.

Today, Benzinga’s options scanner spotted 13 options trades for Lowe’s Companies. This is not a typical pattern.

The sentiment among these major traders is split, with 23% bullish and 76% bearish. Among all the options we identified, there was one put, amounting to $107,900, and 12 calls, totaling $827,556.

Projected Price Targets

Based on the trading activity, it appears that the significant investors are aiming for a price territory stretching from $250.0 to $390.0 for Lowe’s Companies over the recent three months.

Analyzing Volume & Open Interest

Looking at the volume and open interest is a powerful move while trading options. This data can help you track the liquidity and interest for Lowe’s Companies’s options for a given strike price. Below, we can observe the evolution of the volume and open interest of calls and puts, respectively, for all of Lowe’s Companies’s whale trades within a strike price range from $250.0 to $390.0 in the last 30 days.

Lowe’s Companies Option Activity Analysis: Last 30 Days

Biggest Options Spotted:

| Symbol | PUT/CALL | Trade Type | Sentiment | Exp. Date | Ask | Bid | Price | Strike Price | Total Trade Price | Open Interest | Volume |

|---|---|---|---|---|---|---|---|---|---|---|---|

| LOW | CALL | SWEEP | BEARISH | 03/21/25 | $8.1 | $7.85 | $7.85 | $310.00 | $179.7K | 79 | 229 |

| LOW | CALL | SWEEP | BEARISH | 10/18/24 | $33.4 | $32.75 | $32.75 | $250.00 | $108.0K | 2.9K | 131 |

| LOW | PUT | TRADE | BULLISH | 01/17/25 | $109.45 | $107.9 | $107.9 | $390.00 | $107.9K | 10 | 10 |

| LOW | CALL | SWEEP | BEARISH | 10/18/24 | $32.65 | $32.6 | $32.6 | $250.00 | $94.5K | 2.9K | 73 |

| LOW | CALL | TRADE | BEARISH | 10/18/24 | $33.4 | $32.7 | $32.7 | $250.00 | $85.0K | 2.9K | 157 |

About Lowe’s Companies

Lowe’s is the second-largest home improvement retailer in the world, operating more than 1,700 stores in the United States, after the 2023 divestiture of its Canadian locations (RONA, Lowe’s Canada, Réno-Dépôt, and Dick’s Lumber). The firm’s stores offer products and services for home decorating, maintenance, repair, and remodeling, with maintenance and repair accounting for two thirds of products sold. Lowe’s targets retail do-it-yourself (around 75% of sales) and do-it-for-me customers as well as commercial and professional business clients (around 25% of sales). We estimate Lowe’s captures a high-single-digit share of the domestic home improvement market, based on US Census data and management’s market size estimates.

Following our analysis of the options activities associated with Lowe’s Companies, we pivot to a closer look at the company’s own performance.

Present Market Standing of Lowe’s Companies

- With a trading volume of 530,534, the price of LOW is down by -0.8%, reaching $281.79.

- Current RSI values indicate that the stock is may be overbought.

- Next earnings report is scheduled for 33 days from now.

What The Experts Say On Lowe’s Companies

Over the past month, 5 industry analysts have shared their insights on this stock, proposing an average target price of $293.2.

Turn $1000 into $1270 in just 20 days?

20-year pro options trader reveals his one-line chart technique that shows when to buy and sell. Copy his trades, which have had averaged a 27% profit every 20 days. Click here for access.

* Reflecting concerns, an analyst from Melius Research lowers its rating to Buy with a new price target of $290.

* An analyst from Truist Securities has decided to maintain their Buy rating on Lowe’s Companies, which currently sits at a price target of $306.

* An analyst from Oppenheimer upgraded its action to Outperform with a price target of $305.

* Maintaining their stance, an analyst from TD Cowen continues to hold a Hold rating for Lowe’s Companies, targeting a price of $265.

* An analyst from Loop Capital has elevated its stance to Buy, setting a new price target at $300.

Trading options involves greater risks but also offers the potential for higher profits. Savvy traders mitigate these risks through ongoing education, strategic trade adjustments, utilizing various indicators, and staying attuned to market dynamics. Keep up with the latest options trades for Lowe’s Companies with Benzinga Pro for real-time alerts.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Tennessee CEO fled Helene while some workers who were ordered to stay later drowned, lawsuit alleges

The family of a man killed as a result of Hurricane Helene floodwaters in Tennessee has filed a wrongful death lawsuit, alleging his employer “chose greed over the safety of its workers.”

Johnny Peterson, 55, was among the Impact Plastics employees who died on Sept. 27 after Helene’s flooding hit the small, rural town of Erwin in eastern Tennessee.

Surviving employees said they were not told they could leave until the factory lost power, and their cars had already been overtaken by water.

“They had no emergency action plan, despite the factory being located in a federally-designated flood plan,” the 28-page lawsuit filed on behalf of Peterson’s next of kin, Alexa Peterson, by attorney Alex Little in Unicoi County states.

The court-filed documents also allege Impact Plastics CEO Gerald O’Connor Jr. “and other senior management had stealthily exited the building out of the back door after securing some business documents from their own private offices.”

The suit states Peterson was the father of four children, with Alexa being the oldest, and that he had climbed into the bed of a semi-trailer in an attempt to escape.

Helene Devastation Hurts Western North Carolina’s Tourism Economy, Airbnb Owner Says

“He texted his daughter for the last time at 1:17 p.m. ‘I love you allllll,’ he managed to type out. This was the last text Alexa Peterson received from her father,” the suit states.

Peterson is one of five Impact Plastic employees who died as a result of Helene floodwaters, Knox News reports.

Peterson is described as a loving father whose “passing is an immense loss to his family and the community,” a statement from Litson PLLC states.

“Impact Plastics was aware of the flood risks, and while employees requested permission to leave, the company failed to act. We will hold them accountable,” the statement reads.

Click Here To Read More On Fox Business

The attorney FOX Business was referred to for comment about the lawsuit said he had “no additional information at this time,” but a previously shared statement to Fox News Digital quoted O’Connor stating, “We are devastated by the tragic loss of great employees.”

Original article source: Tennessee CEO fled Helene while some workers who were ordered to stay later drowned, lawsuit alleges

Zuckerberg sacks staff on six-figure salaries for abusing office’s food delivery scheme

Mark Zuckerberg’s Meta has sacked a number of staff after they abused the company’s $25 (£19) meal scheme to order household goods such as toothpaste and washing powder.

Almost 30 staff in the company’s Los Angeles office were dismissed after they were found to be routinely using takeaway credits to order groceries and cosmetics, employees said.

The sackings included high-paid engineers earning six-figure salaries, according to posts on the anonymous chat app Blind.

Meta, which is currently worth $1.5 trillion, provides staff with free breakfast, lunch and dinner at its larger offices.

Those in smaller offices without staff canteens instead receive vouchers for delivery apps such as Grubhub, which they can use to order food when working at the office.

However, Meta recently discovered that some employees were using the $25 vouchers to order household items from stores that feature on the apps.

In some cases, staff were using the scheme to buy wine glasses and laundry detergent, according to the Financial Times.

Meta and other Silicon Valley companies have long offered free food in their offices, which are seen as an incentive to come into the office instead of working from home, or in the case of breakfast and dinner, to encourage longer working hours.

Staff initially received warnings about abusing the meal voucher scheme but those who continued to do so were sacked last week.

The news came as Meta also laid off a larger number of staff across WhatsApp, Instagram and its virtual reality unit on Wednesday.

The company said it was restructuring certain departments, and moving some staff to other areas.

The redundancies are not believed to be as widespread as the mass layoffs in 2022 and 2023, when Meta cut tens of thousands of staff in what Mr Zuckerberg called a driver for “efficiency”.

A Meta spokesman said: “Today, a few teams at Meta are making changes to ensure resources are aligned with their long-term strategic goals and location strategy.

“This includes moving some teams to different locations, and moving some employees to different roles. In situations like this when a role is eliminated, we work hard to find other opportunities for impacted employees.”

Meta has cut down on perks introduced to encourage staff into the office in recent years, scrapping “to-go” boxes that allowed employees to take food home, as well as benefits such as laundry services.

Nvidia Stock vs. Arm Stock: Wall Street Says Buy One and Sell the Other

Grand View Research forecasts artificial intelligence (AI) chip sales will grow at 29% annually through 2030. Semiconductor companies Nvidia (NASDAQ: NVDA) and Arm Holdings (NASDAQ: ARM) are major players in that market, and shares have rocketed 166% and 100%, respectivley, year to date. But most Wall Street analysts expect the stocks to move in opposite directions over the next year.

-

Nvidia has a median 12-month price target of $150 per share. That implies 15% upside from its current share price of $131.

-

Arm has a median 12-month price target of $144 per share. That implies 5% downside from its current share price of $151.

Going forward, Nvidia and Arm should benefit as businesses continue to build out their AI infrastructure, but that does not necessarily make them good investments. Here are the important details.

1. Nvidia

Nvidia holds 98% market share in data center graphics processing units (GPU), chips used to accelerate computationally demanding workloads like training machine learning models and running artificial intelligence (AI) applications. That dominance is more than a decade in the making. In 2006, Nvidia introduced its CUDA programming model, which has evolved into an unmatched ecosystem of software development tools for GPU programmers.

More recently, Nvidia has added networking gear and central processing units (CPUs) to its hardware portfolio, and debuted software and cloud services that simplify AI application development. In that context, while many investors view Nvidia as a chipmaker, it is more accurately an accelerated computing company. And its ability to innovate across the entire data center computing stack — from hardware to software to services — affords Nvidia a competitive moat.

Nvidia beat estimates with its financial results in the second quarter of fiscal 2025 (ended July 2024). Revenue increased 122% to $30 billion due to strong demand for AI chips, networking, and enterprise software. And non-GAAP net income increased 152% to $0.68 per diluted share. Management also gave stronger guidance than Wall Street anticipated, such that revenue is forecast to jump 80% in the third quarter.

It goes without saying that Nvidia has a tremendous opportunity where AI is concerned, but the broader data center accelerator market is equally momentous. “We are at the beginning of our journey to modernize $1 trillion worth of data centers from general-purpose computing to accelerated computing,” CEO Jensen Huang recently told analysts. He expects that transition to play out over the next four to five years.

Wall Street expects Nvidia’s adjusted earnings to increase at 35% annually through fiscal 2027 (ends January 2027). That makes current valuation of 59 times adjusted earnings look fair. Personally, I think Nvidia is a must-own stock given its level of participation in the AI economy, not to mention its leadership in the data center accelerator market. The current price is a reasonable entry point for patient investors.

2. Arm Holdings

Arm develops central processing unit architectures and licenses the intellectual property (IP) to clients, who use the IP to build custom chips for a wide range of end markets, from mobile devices and industrial sensors to data center infrastructure. Arm also provides development tools that simplify the of writing and debugging of applications.

Arm CPUs are known for their energy efficient architecture, which has helped the company secure a leadership position in mobile devices. Most importantly, Arm has more than 99% market share in smartphone processors. However, the company is also gaining share in data centers and personal computers (PCs) because its chip are becoming increasingly powerful.

Arm is well positioned to benefit as the artificial intelligence boom progresses. Its CPUs are the foundation of Apple Intelligence; they handle simple AI tasks on devices like iPhones and more complex AI tasks on private data center servers. The major public clouds (Amazon Web Services, Microsoft Azure, and Alphabet‘s Google Cloud Platform) have designed Arm-based server CPUs. And several computer manufacturers have introduced AI PCs powered by Arm processors.

Arm reported solid financial results in the first quarter of fiscal 2025 (ended June 2024), beating estimates on the top and bottom lines. Revenue increased 39% to $939 million due to momentum in the smartphone and cloud computing markets, which itself was driven by strong adoption of Arm’s latest architecture (Armv9). Meanwhile, non-GAAP net income increased 67% to $0.40 per diluted share.

Wall Street expects Arm’s adjusted earnings to grow at 27% annually through fiscal 2027 (ends March 2027). That estimate makes the current valuation of 107 times adjusted earnings look outrageously expensive. So, I think prospective investors should stay on the sidelines right now, and present shareholders should consider trimming their positions, especially if those positions comprise a substantial portion of their portfolios.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $806,459!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 14, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Trevor Jennewine has positions in Amazon and Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Nvidia Stock vs. Arm Stock: Wall Street Says Buy One and Sell the Other was originally published by The Motley Fool

Netflix beats earnings targets with 5 million new customers

By Lisa Richwine and Dawn Chmielewski

LOS ANGELES (Reuters) -Netflix picked up 5.1 million streaming subscribers in the third quarter, topping Wall Street estimates by more than 1 million users, and said it expected higher customer growth around the holidays when Korean drama “Squid Game” returns.

Shares of Netflix rose 3.5% to $711.98 in after-hours trading following the earnings report on Thursday.

Investors had expected Netflix to bring in 4 million subscribers from July through September, according to analysts’ estimates compiled by LSEG. New programming during the period included murder mystery “The Perfect Couple” and romantic comedy “Nobody Wants This.”

Diluted earnings per share landed at $5.40, above the consensus forecast of $5.12. Revenue hit $9.825 billion, just ahead of the $9.769 billion consensus forecast.

The company projected its customer additions for the last three months of the year, traditionally a strong period around the Christmas holiday, would outpace the September quarter, though it did not provide a number.

Netflix has been trying to shift investor attention away from subscriber sign-ups to other metrics, including revenue growth and profit margins. The company said its operating margin hit 30% in the quarter, compared with 22% a year earlier.

“We’ve delivered on our plan to reaccelerate our business, and we’re excited to finish the year strong with a great Q4 slate,” the company said in a letter to shareholders. New programming will include the second season of Korean drama “Squid Game.”

The company said its programming volume had picked up following disruptions from last year’s Hollywood strikes. Engagement, the time spent watching Netflix, averaged two hours per day per member.

Nearly two years into its advertising business, Netflix is working to increase revenue from ad-supported plans but has said it does not expect advertising to become a primary growth driver until 2026.

In the September quarter, Netflix’s ad-supported service accounted for more than 50% of signups in countries where it was available.

Part of the plan centers around live events including sports, a big draw for advertisers. In November, Netflix will stream a fight between YouTube star Jake Paul and Mike Tyson, followed by its first NFL games in December.

“Advertisers want to be part of big cultural moments. Compelling live programming will always amass and unite people for a snapshot in time,” said Forrester’s research director, Mike Proulx. “For brands, that’s a captive audience who’s ripe for advertising messages.”

(Reporting by Lisa Richwine and Dawn Chmielewski in Los AngelesAdditional reporting by Harshita Mary Varghese in BengaluruEditing by Matthew Lewis)

Fannie Mae CEO says she has never seen a housing market like this before

After two decades working in housing policy, Priscilla Almodovar is intimately familiar with the challenges the U.S. faces when it comes to housing.

The Brooklyn native took the reins of the New York State Housing Finance Agency in 2007 amid a financial crisis that was fueled by a crash in subprime mortgages. Today, buyers are facing the opposite problem: Demand for homes is so insatiable that even as mortgage rates remain elevated and home-insurance costs soar, home prices keep inching up to new record highs.

Most Read from MarketWatch

As the chief executive of Fannie Mae FNMA, a government-sponsored enterprise that backs one in four residential mortgages in the U.S., Almodovar, 57, has a front-row seat to it all. That lands her on the MarketWatch 50 list of the most influential people in markets.

“It’s a highly unaffordable market right now. We are monitoring and following all these trends, things that we’ve never seen before,” Almodovar told MarketWatch in an interview.

“You have home prices the highest we’ve seen in two decades,” she said.

Home sales on track for worst year since 1995

Home buyers and renters are facing record-high housing costs. The issue has become such a big priority for average Americans that the presidential candidates are proposing various solutions to make homeownership more affordable.

Meanwhile, some renters are taking matters into their own hands with rent strikes, while some aspiring homeowners have abandoned the idea and decided to rent indefinitely, finding it far cheaper than owning.

Even though mortgage rates have come down after the 30-year rate posted a big jump to 8% in October 2023, the average mortgage payment — which includes principal and interest, as well as property taxes and homeowners insurance — hit a new record high of $2,070 in August, according to Intercontinental Exchange. That’s up 24% from before the pandemic.

Mortgage rates are unlikely to drop back down to prepandemic levels anytime soon, Almodovar said. Regarding the 3% rate seen during the pandemic, she said, “we probably will never see that again in our lifetime.”

Even if buyers can afford the price of a home, there aren’t many options to choose from. The market is still enduring the lock-in effect, with current homeowners seeing little benefit in selling their current property and buying a more expensive one at higher interest rates.

The lock-in effect in particular is an unusual phenomenon that has stalled the housing market. Homeowners’ unwillingness to sell resulted in home sales that were 57% lower in the fourth quarter of 2023 than in the same quarter the previous year, the Federal Housing Finance Agency estimated in March.

Put another way, the lock-in effect “prevented” the sale of 1.33 million homes, the agency said.

Addressing the nation’s housing challenges will likely take more than initiatives from whoever wins the presidential election. Bringing the cost of housing down will also require policy makers at the federal, state and local levels to get involved, Almodovar said.

“There’s a consensus today that part of the solution is more supply,” she said. That means preserving the nation’s old existing homes and also building new units, she added.

Many of the obstacles to increasing housing supply are controlled at the local level, she noted.

“It’s zoning. It’s not-in-my-backyard NIMBY-ism,” Almodovar said. “The No. 1 issue is the local. That’s where decisions really get made.”

Homeownership is still part of the American dream

The pressure brought on by high rates and high prices has stalled the housing market. Fannie Mae’s economists expect only 4 million existing homes to be sold in the U.S. through 2024, the lowest number since 1995.

Nonetheless, most Americans aspire to own a home. About 84% of respondents in a 2023 survey by LendingTree said that homeownership is part of their American dream.

Almodovar grew up in New York City, and her parents bought their first home when she was 5 years old. In reaching that milestone, they felt like they had achieved the American dream, she recalled, noting that the idea is still “very much ingrained in what we think, and the mindset of our country.”

For that reason, the current environment has made housing “one of the most important domestic policy issues that we have to tackle,” Almodovar said.

Housing costs pushed up by unstable variables

It’s not just the challenges of saving for a down payment and of navigating elevated mortgage rates that are making homeownership unaffordable for many Americans. Rising insurance costs also mean homeowners are struggling more to fit their monthly payments into their budget.

Unlike a monthly mortgage payment, which remains the same throughout the life of a fixed-rate loan, insurance costs have surged over the last few years, adding instability to an otherwise stable 30-year loan.

Recent natural disasters — including hurricanes Milton and Helene, which caused significant damage in parts of the southeastern U.S. — illustrate the challenges climate change is posing to homeowners and to the housing industry.

Climate risk is something Fannie Mae is monitoring closely, Almodovar said.

As real-estate companies race to bring climate-risk information to prospective home buyers and homeowners, government agencies are revving up not only to offer assistance to affected homeowners but also to impose a moratorium on foreclosures of mortgages insured by the Federal Housing Administration.

They are also trying to stay ahead of the risk by encouraging people to make their homes more resilient to climate disasters.

Because it guarantees one in four mortgages in the U.S., Fannie Mae has skin in the game — and officials there are worried.

There is a gap between how much risk is understood by homeowners and what private-sector companies know, Almodovar said.

The federal government publishes maps of places that are expected to flood, but Hurricane Helene demonstrated how locales that are further inland and have historically not been prone to flooding can end up inundated. “So it is something that concerns us,” Almodovar said.

Ultimately, “climate is one of those areas where there’s no one silver bullet,” she said. Instead, “it’s really all sectors working together, and all industries working together.”

Most Read from MarketWatch

'I'm In A Pickle' – 53-Year-Old Broke Truck Driver With No Retirement Savings, Owes The IRS And Wants A Divorce Asks Ramsey For Advice

Donnie’s “pickle” is more like a jar of problems – financial chaos, a struggling marriage and some serious tax issues.

The 53-year-old truck driver, who called into The Ramsey Show, painted a picture of financial highs and lows. At one point, things were great: debt-free, savings stacked up and no need for credit cards. But then, things took a sharp turn when his wife, who had been managing the money, started racking up credit card debt, drained their savings and let the IRS bills pile up, resulting in a whopping $30,000 tax bill. To top it off, Donnie wants a divorce and has nothing saved for retirement. His total debt is $50,000.

Don’t Miss:

“I’m in a pickle,” Donnie says, to which Dave Ramsey’s co-host John Delony adds, “Sounds like you’re in a jar of pickles.” The three men chuckle, but the situation is far from amusing.

According to the hosts, the core of the issue isn’t just the taxes or the debt. It’s the fact that Donnie and his wife have been dancing around their problems, communicating poorly and working at cross purposes. Sure, they got debt-free at one point, but as Ramsey pointed out, “You didn’t achieve y’all’s goal, you achieved your goal.” Ouch. The cracks in their financial plan reflect deeper issues in their relationship. While they once found common ground on their finances, their marriage was clearly unraveling in the background.

Trending: Studies show 50% of consumers think Financial Advisors cost much more than they do — to debunk this, this company provides matching for free and a complimentary first call with the matched advisor.

“You guys suck at communication in your marriage beyond belief.” He explains that unless they find alignment – agreeing on both their financial and marital goals – the money issues will continue to pile up, whether or not they stay married. And as harsh as it sounds, if they can’t get on the same page, the only thing left to do will be to fix the money mess after the inevitable divorce.

In terms of the IRS debt, Ramsey tells Donnie to sit down with one of his Ramsey Solutions tax pros and negotiate a payment plan to pay off the debt. But that only solves the debt issue.

Donnie’s struggle is relatable for many. While things may seem financially smooth at one point, underlying problems – whether in communication, trust or joint goals – can bring everything down.

Trending: Many are using this retirement income calculator to check if they’re on pace — here’s a breakdown on how on what’s behind this formula.

The bottom line here is that no amount of financial planning can fix a falling-apart marriage if both partners aren’t truly aligned. It’s a pickle that requires more than just crunching numbers; it needs real communication, a shared vision and a hefty dose of honesty.

Whether navigating life solo or teaming up as a couple, consulting a financial advisor can make a difference in situations like Donnie’s. Getting an expert to help untangle financial messes can save you from future headaches. Don’t let your “pickle” become a whole jar – talk to a financial advisor and get on the path to stability, one step at a time.

Read Next:

UNLOCKED: 5 NEW TRADES EVERY WEEK. Click now to get top trade ideas daily, plus unlimited access to cutting-edge tools and strategies to gain an edge in the markets.

Get the latest stock analysis from Benzinga?

This article ‘I’m In A Pickle’ – 53-Year-Old Broke Truck Driver With No Retirement Savings, Owes The IRS And Wants A Divorce Asks Ramsey For Advice originally appeared on Benzinga.com

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

El Pollo Loco Holdings, Inc. to Announce Third Quarter 2024 Results on Thursday, October 31, 2024

COSTA MESA, Calif., Oct. 17, 2024 (GLOBE NEWSWIRE) — El Pollo Loco Holdings, Inc. (“El Pollo Loco”) LOCO today announced that it will host a conference call to discuss its third quarter 2024 financial results on Thursday, October 31, 2024 at 4:30 PM Eastern Time. Hosting the call will be Liz Williams, Chief Executive Officer, and Ira Fils, Chief Financial Officer. A press release with third quarter 2024 financial results will be issued that same day, shortly after the market close.

The conference call can be accessed live over the phone by dialing 201-493-6780. A replay will be available after the call and can be accessed by dialing 412-317-6671; the passcode is 13748557. The replay will be available until Thursday, November 14, 2024.

The conference call will also be webcast live from the Company’s corporate website at investor.elpolloloco.com under the “Events & Presentations” page. An archive of the webcast will be available at the same location on the corporate website shortly after the call has concluded.

About El Pollo Loco

El Pollo Loco LOCO is the nation’s leading fire-grilled chicken restaurant known for its craveable, flavorful, and better-for-you offerings. Our menu features innovative meals with Mexican flavors all made in our restaurants daily using quality ingredients. At El Pollo Loco, inclusivity is at the heart of our culture. Our community of over 4,000 employees reflects our commitment to creating a workplace where everyone has a seat at our table. Since 1980, El Pollo Loco has successfully expanded its presence, operating more than 495 company-owned and franchised restaurants across seven U.S. states: Arizona, California, Colorado, Nevada, Texas, Utah and Louisiana. The Company has also extended its footprint internationally, with ten licensed restaurant locations in the Philippines. For more information or to place an order, visit the Loco Rewards APP or ElPolloLoco.com. Follow us on Instagram, TikTok, Facebook, or X.

Investor Contact:

Jeff Priester

ICR

Investors@elpolloloco.com

![]()

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.