Prediction: This Will Be the Best Stock in the Dow Jones Next Year

The Dow Jones Industrial Average is comprised of 30 stocks, but one stands out from the pack.

The “Magnificent Seven” is a moniker used to collectively describe a market-moving cluster of some of the world’s largest technology enterprises: Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta Platforms, and Tesla. Each is putting its own stamp on the artificial intelligence (AI) landscape, and all have received a lot of attention from media outlets and investors alike.

But another AI stock that gets less press has handily outperformed five of the Magnificent Seven over the past two years. Enterprise software leader and Dow Jones Industrial Average (DJIA) component Salesforce (CRM 0.87%) has gained a whopping 98% in just two years.

Even with that impressive run-up behind it, I think Salesforce’s next growth phase is just beginning. In fact, given the lucrative opportunity the company has in AI, I think Salesforce could be the top-performing stock in the Dow next year.

What about the rest of the Dow Jones?

Asserting that Salesforce could be the top performer in the Dow next year is a bold claim. After all, what about the other 29 companies?

The Dow is a curated index that includes some of the world’s largest companies across most major industry sectors. In my opinion, both financial services and consumer goods stocks still carry some risk. Specifically, I see both of these industries as particularly vulnerable to macroeconomic forces including inflation and interest rates. While inflation has been cooling for quite some time and the Federal Reserve has instituted an interest rate tapering protocol, I do not think the broader economy is quite out of the woods just yet.

Moreover, I think energy stocks are going to experience excessive volatility for the time being. Broadly speaking, energy policies tend to differ between which parties are in control of Congress. Even after the results of the 2024 election shake out next month, I could easily see energy stocks moving pretty dramatically depending on any policy changes that could go into effect.

This leaves the technology sector, where the DJIA includes major tech players including Amazon, Apple, Cisco, IBM, Intel, and Microsoft. While I’m bullish on Amazon and Microsoft, I think both companies are facing a lot of pressure and scrutiny to drive consistent impressive results, considering that they have both poured billions into their AI initiatives.

Meanwhile, Apple’s AI roadmap is in its early stages — making it hard to predict how its decisions will pan out. Unfortunately, I think Intel’s best days may be behind it. And IBM and Cisco are stuck competing in saturated markets. For all of these reasons, I think Salesforce has the most upside compared to its peers.

Image Source: Getty Images.

A huge opportunity for Salesforce

If you’ve been paying attention to artificial intelligence narratives over the last couple of years, you’ve heard the term “generative AI” ad nauseam. But what does it actually mean?

In simple terms, generative AI is software that has the capability to digest datasets to help answer complicated questions extremely quickly. When generative AI tools are at their best, employees across a company’s workforce are running sophisticated queries and creating robust data-driven dashboards — leading to enhanced productivity and efficiency. No more spinning your wheels and burning the midnight oil.

One of the leading types of applications in generative AI right now is the virtual agent. Microsoft has been a big winner in this regard thanks to its CoPilot assistant, which runs on ChatGPT and has been integrated throughout the company’s ecosystem, spanning cloud computing, productivity tools, and software development.

Salesforce has taken note of Microsoft’s success and decided to challenge its big tech cohort. Enter Agentforce, a virtual assistant that can help customers with things such as scheduling appointments, billing resolutions, cybersecurity threat analysis, and a host of other use cases. Salesforce’s vision is to remove the friction of human-led customer service and allow AI-powered agents to resolve customers’ needs.

Salesforce already has a deep penetration among large-scale corporations and small and midsize enterprises thanks to its customer relationship management (CRM) platform, data analytics tools powered by Tableau, and messenger tool Slack. To me, Agentforce should be an easy cross-selling opportunity to Salesforce’s existing customer base, and the company has a unique chance to emerge as a strong pillar supporting digital solutions.

Is Salesforce stock a buy right now?

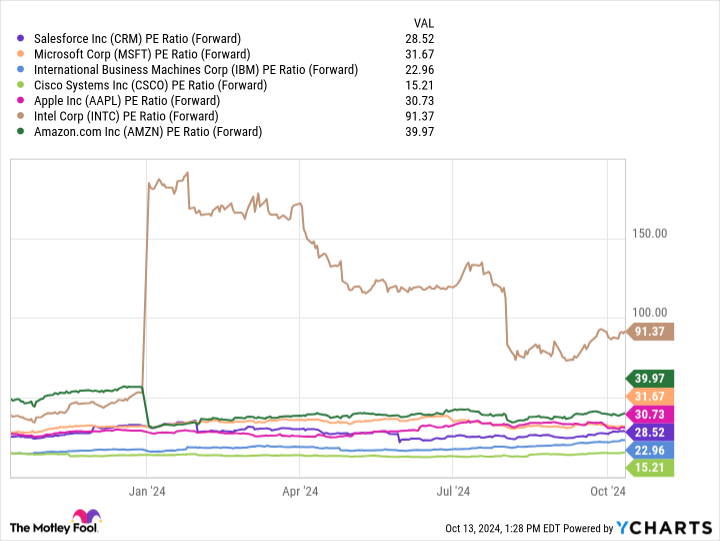

Right now, Salesforce shares trade at a forward price-to-earnings (P/E) multiple of 28.5. This is a healthy premium compared to the S&P 500‘s forward P/E of 22.9.

CRM PE Ratio (Forward) data by YCharts.

Although Salesforce may be valued as a superior investment compared to the broader market, the company is trading at a discount to the majority of its technology industry counterparts in the DJIA.

I think Agentforce is going to be a major tailwind for Salesforce so long as the AI narrative holds up. Investors may want to be on the lookout over the next year to see how the adoption of Agentforce is progressing and what kind of growth it’s driving for Salesforce.

If Microsoft CoPilot serves as any proxy, I think much better days are ahead for Salesforce, and I expect to see the stock soaring over the next year.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Cisco Systems, Meta Platforms, Microsoft, Nvidia, Salesforce, and Tesla. The Motley Fool recommends Intel and International Business Machines and recommends the following options: long January 2026 $395 calls on Microsoft, short January 2026 $405 calls on Microsoft, and short November 2024 $24 calls on Intel. The Motley Fool has a disclosure policy.

Leave a Reply