Got $3,000? 2 Artificial Intelligence (AI) Stocks to Buy and Hold for the Long Term.

Artificial intelligence (AI) is the hottest topic on Wall Street and is expanding quickly to Main Street as businesses adopt these solutions at lightning speeds. Open AI’s ChatGPT caused a search and query revolution, while Nvidia’s unprecedented growth helped power the Nasdaq Composite and S&P 500 to new highs.

AI is a vast field, and investors have oodles of options, from companies that provide tech research, like Gartner, to those providing integrated software, like Microsoft’s Copilot, to data center memory suppliers like Micron Technology. But most of us don’t have unlimited funds to invest in everything.

If you have a few thousand dollars in a retirement account or rattling around in the bank, I have a couple of ideas. I thought I would focus on two extraordinarily different companies that could provide long-term profits.

SoundHound AI

Rising costs and a lack of available workers have made drive-thru and fast-casual restaurants explore alternatives. Meanwhile, automakers are looking for next-gen conversational intelligence. Voice recognition conversational intelligence solves both problems, and SoundHound’s software offers this to many familiar brands, such as White Castle, Jersey Mikes, Stellantis, and Honda.

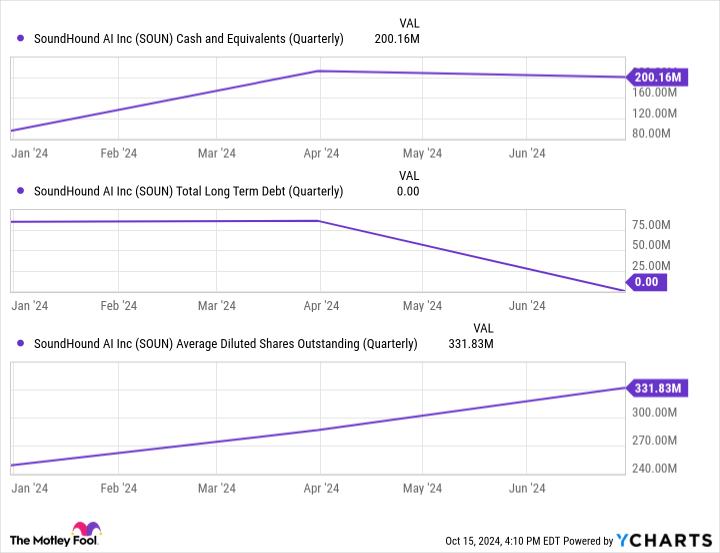

I’ve been critical of SoundHound AI (NASDAQ: SOUN) in the past. At the end of 2022, the company’s cash balance bottomed out at just $10 million against $35 million in debt. $10 million makes growth extremely difficult for an unprofitable company with negative cash flow — it’s not a recipe for success.

However, management drastically improved its position to $200 million in cash and no debt last quarter, as shown below, although the company increased its share count substantially to do it.

The increase in share count is a tough pill for the existing shareholders, but the dilution should drastically slow now that the company is on solid footing.

SoundHound trades for 26 times sales, which seems high for an unprofitable, cash-flow-negative company. However, the valuation drops drastically when accounting for the rapid growth. SoundHound hit $13.5 million in sales in Q2 on 54% year-over-year growth. It expects revenue to leap from $80 million in 2024 to $150 million next year. This brings the price-to-sales ratio to a more palatable 12.5.

SoundHound isn’t a stock for everyone; smaller companies are typically riskier, albeit with massive upside potential. Areas like voice-enabled smart TVs, home devices, carryout ordering, and retail are virtually untapped. Still, it’s best not to put all your eggs in one basket, so here’s a more mainstream idea.

Amazon

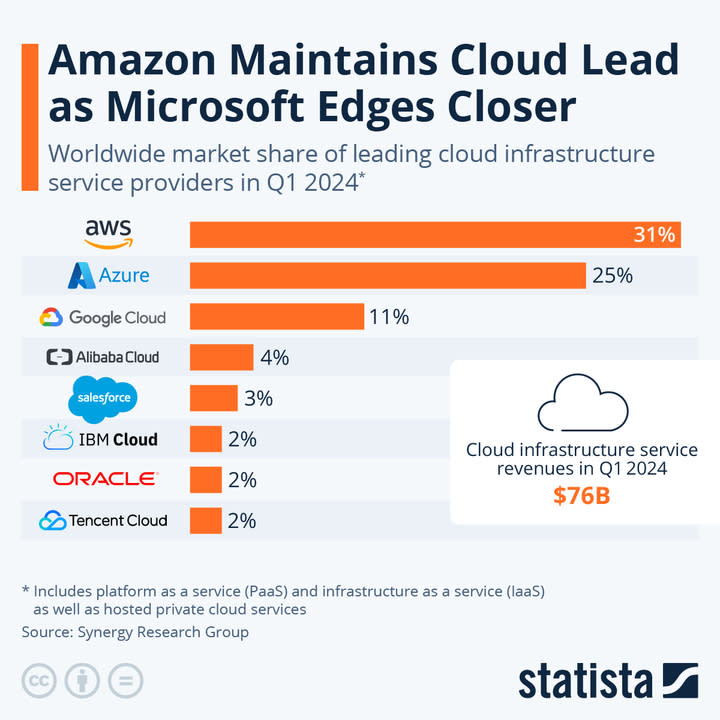

Amazon (NASDAQ: AMZN) is about 1,000 times larger than SoundHound by market capitalization. It’s also a critical cog in the AI machine. We use more data than ever, and the need for it keeps growing. Cloud service providers, like Amazon Web Services (AWS), are critical to power data-guzzling AI applications. As shown below, AWS is the largest provider, with nearly a third of the market.

AWS accounts for a growing portion of Amazon’s total revenue — 18% in Q2 2024 compared to 16% in Q2 2023. This is terrific for Amazon as AWS is highly profitable, posting a 36% operating margin last quarter compared to 10% for the company as a whole. If you still think of Amazon as a product company, think again; 58% of total sales last quarter were from services like AWS, digital advertising, Prime, and third-party seller services.

This should excite investors since services tend to be more profitable than products. The continued migration to services and the resurgence of AWS on the back of AI pushed operating profits to $30 billion for the first six months of 2024 compared to just $12 billion for the same period of 2023.

Amazon has other irons in the AI fire, like Amazon Bedrock, which provides foundational models that customers can customize to suit their needs, and forays into designing AI chips. The company has the resources to be a major player in the industry.

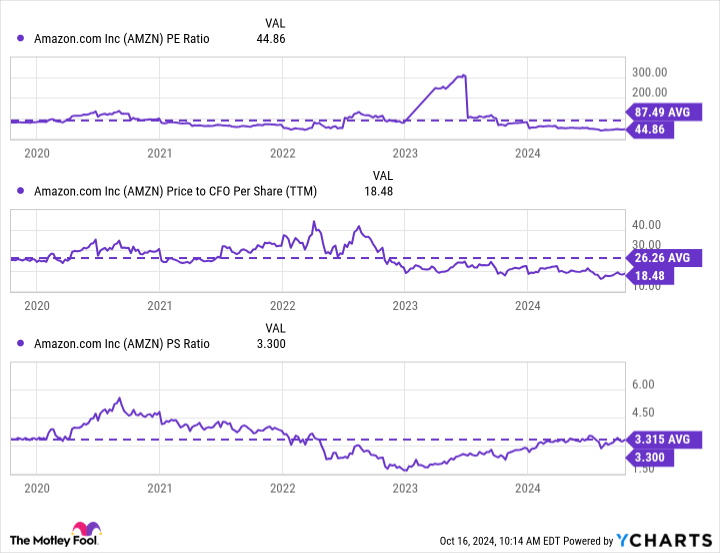

Now, let’s look at the stock, which trades below its recent averages based on earnings, cash flow, and sales, as depicted below.

Investors should always consider their risk tolerance (what’s yours? Try this quiz to find out) when choosing how to divide their money between investments. In this case, SoundHound is riskier than Amazon but has a more explosive potential upside because of its smaller size.

A typical long-term investor with medium risk tolerance should consider weighting their dollars heavily toward Amazon with a smaller speculative position in SoundHound. In contrast, an aggressive investor could do the opposite.

Should you invest $1,000 in SoundHound AI right now?

Before you buy stock in SoundHound AI, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and SoundHound AI wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $839,122!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 14, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Bradley Guichard has positions in Amazon and Micron Technology and has the following options: long January 2025 $2 calls on SoundHound AI. The Motley Fool has positions in and recommends Amazon, Microsoft, and Nvidia. The Motley Fool recommends Gartner and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Got $3,000? 2 Artificial Intelligence (AI) Stocks to Buy and Hold for the Long Term. was originally published by The Motley Fool

Leave a Reply