2 High-Yield Dividend Stocks to Buy Now and Help You Generate Passive Income

Companies with high dividend yields have a much better chance of providing investors with predictable income regardless of what the broader stock market is doing. The key, of course, is to stick with companies that can afford their payouts. After all, a dividend expense is only as good as the company paying it.

And companies that don’t have a runway for future earnings growth won’t be able to raise their dividend without jeopardizing their balance sheet. With that in mind, here’s why United Parcel Service (NYSE: UPS) and Kinder Morgan (NYSE: KMI) stand out as two top dividend stocks to buy now.

UPS has more work to do to regain investor excitement

UPS will report third-quarter 2024 earnings on Oct. 24. With the stock trading less than 9% from its four-year low, it will be a “show me” quarter for the delivery giant.

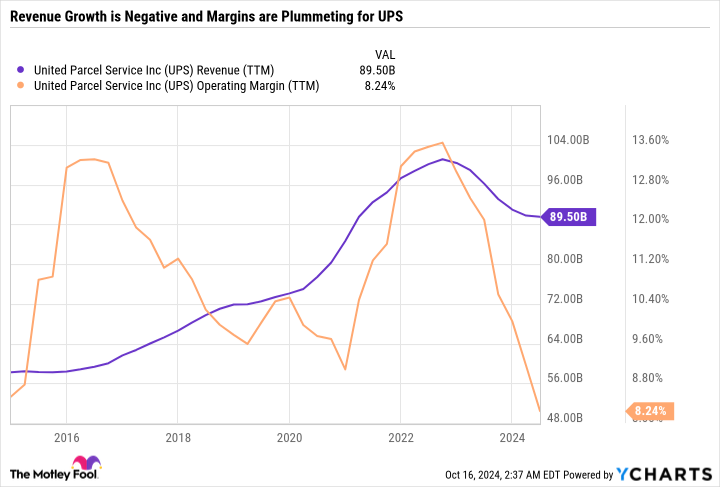

In its last quarterly report, UPS guided for full-year consolidated revenue of $93 billion, a consolidated operating margin of 9.4%, and capital expenditures of $4 billion. UPS has pulled back on spending to cut costs and restore its margins, which went from a 10-year high to a 10-year low in less than two years.

In March, UPS held an investor presentation and announced new three-year financial targets of $108 billion to $114 billion in consolidated revenue by 2026, an adjusted operating margin above 13%, and $17 billion to $18 billion in free cash flow. The plan had two phases, with 2024 focusing on volume and adjusted operating profit dollar growth, and 2025 and 2026 focused on volume and adjusted operating profit margin growth.

Last quarter, UPS returned to domestic volume growth for the first time in nine quarters — which was a step in the right direction toward achieving its 2024 goal. But as for now, the three-year targets look out of reach and could be delayed until 2027.

UPS must implement more concrete measures to get back on track and accelerate sales growth momentum into next year. In the meantime, UPS yields a hefty 4.9%, and management has indicated that maintaining its current payout is a top priority.

Oil and gas infrastructure is proving its value

Between 2016 and the end of 2023, Kinder Morgan stock’s price increased less than 20% compared to a 133% rise in the S&P 500 index. Factoring in dividends, Kinder Morgan returned a much better 77%, but it was still a drastic underperformance from the S&P 500’s 170% total return during that period.

So, heading into 2024, Kinder Morgan investors had grown used to mediocrity. The main draw of buying and holding the stock was the dividend. But Kinder Morgan’s stock price has surged over 40% year to date. Even after that rise, Kinder Morgan still yields 4.6% — illustrating just how high its yield was when the stock was more beaten down.

Pipeline and infrastructure companies like Kinder Morgan have been on a tear this year due to expectations for increased natural gas domestic demand, and the opportunity for higher exports to Mexico and overseas by cooling and condensing gas into liquid form. Higher demand is vital for justifying new project investment. When Kinder Morgan is at its best, it builds new projects that can return steady cash flow over time, funneling a portion of that cash into even more projects and paying a growing dividend to shareholders.

Part of the reason Kinder Morgan has been such a poor-performing stock over the last decade or so is due to concerns that its infrastructure assets could lose value over time as natural gas demand weakened and the energy mix shifted more toward renewables. Less natural gas production could also lead to less justification for new projects, jeopardizing Kinder Morgan’s business model.

Those concerns certainly haven’t gone away, but there are signs that natural gas could remain a part of the energy mix well into the medium term. In addition to the demand drivers mentioned, natural gas could also power data centers and support the energy needs of artificial intelligence.

Kinder Morgan generates plenty of cash to reinvest in the business and fuel its growing payout, making it a reliable high-yield dividend stock to consider now.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,285!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,456!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $411,959!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 14, 2024

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Kinder Morgan. The Motley Fool recommends United Parcel Service. The Motley Fool has a disclosure policy.

2 High-Yield Dividend Stocks to Buy Now and Help You Generate Passive Income was originally published by The Motley Fool

Leave a Reply