Gold Moves Higher; Medtronic Posts Upbeat Results

U.S. stocks traded mixed toward the end of trading, with the Nasdaq Composite gaining by around 1% on Tuesday.

The Dow traded down 0.03% to 43,374.79 while the NASDAQ rose 1.03% to 18,985.21. The S&P 500 also rose, gaining, 0.49% to 5,922.41.

Check This Out: This Apollo Global Management Analyst Begins Coverage On A Bullish Note; Here Are Top 5 Initiations For Tuesday

Leading and Lagging Sectors

Information technology shares rose by 0.6% on Tuesday.

In trading on Tuesday, materials shares fell by 0.6%.

Top Headline

Medtronic Plc MDT reported better-than-expected results for its second quarter and raise its outlook.

The company posted second-quarter 2025 sales of $8.40 billion, beating the consensus of $8.27 billion. The medical device maker reported adjusted EPS of $1.26, beating the consensus of $1.25.

Medtronic raised its fiscal year 2025 organic revenue growth guidance to 4.75%-5%, up from the prior 4.5%-5%. If recent foreign currency exchange rates hold, 2025 revenue growth on an adjusted basis would be 3.4%-3.9%. Medtronic expects 2025 adjusted EPS guidance to be $5.44-$5.50 versus previous guidance of $5.42-$5.50 and consensus of $5.45.

Equities Trading UP

- Super Micro Computer, Inc. SMCI shares shot up 29% to $27.84 after the company announced the appointment of BDO USA as its independent auditor and the filing of a compliance plan with Nasdaq.

- Shares of PainReform Ltd. PRFX got a boost, surging 172% to $1.4600. The company announced a 1-for-4 reverse stock split.

- Interactive Strength Inc. TRNR shares were also up, gaining 30% to $3.30. The company, which makes specialty fitness equipment under the CLMBR and FORME brands, disclosed that Armah Sports Group‘s B_FIT is installing CLMBRs in three of its nine locations in Saudi Arabia.

Equities Trading DOWN

- NWTN Inc. NWTN shares dropped 12% to $1.06. NWTN received Nasdaq staff delisting determination for non-compliance with Listing Rule 5250(c)(1).

- Shares of Incyte Corporation INCY were down 13% to $66.74 after the company announced that data from its Phase 2 study evaluating MRGPRX4 (INCB000547) in cholestatic pruritus does not support further development.

- Codere Online Luxembourg, S.A. CDRO was down, falling 11% to $6.77 after the company received a Nasdaq delisting notice due to its public reports rule.

Commodities

In commodity news, oil traded down 0.1% to $69.12 while gold traded up 0.7% at $2,632.40.

Silver traded up 0.3% to $31.305 on Tuesday, while copper rose 0.6% to $4.1435.

Euro zone

European shares closed lower today. The eurozone’s STOXX 600 fell 0.45%, Germany’s DAX fell 0.67% and France’s CAC 40 fell 0.67%. Spain’s IBEX 35 Index fell 0.74%, while London’s FTSE 100 fell 0.13%.

Hourly labor costs in the Eurozone rose by 4.6% year-over-year in the third quarter compared to a revised 5% gain in the prior quarter. Annual inflation in the Eurozone rose to 2% in October from 1.7% in September.

Asia Pacific Markets

Asian markets closed higher on Tuesday, with Japan’s Nikkei 225 gaining 0.51%, Hong Kong’s Hang Seng Index gaining 0.44%, China’s Shanghai Composite Index gaining 0.67% and India’s BSE Sensex gaining 0.31%.

Malaysia’s trade surplus narrowed to MYR 12.0 billion in October from MYR 13.0 billion in the year-ago month.

Economics

- Housing starts in the U.S. declined by 3.1% to 1.311 million in October versus a revised 1.353 million in the previous month.

- U.S. building permits declined by 0.6% to an annual rate of 1.416 million in October.

Now Read This:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Insider Decision: Mark Silver Offloads $221K Worth Of Ryerson Holding Stock

Mark Silver, EVP at Ryerson Holding RYI, reported an insider sell on November 18, according to a new SEC filing.

What Happened: A Form 4 filing with the U.S. Securities and Exchange Commission on Monday outlined that Silver executed a sale of 9,000 shares of Ryerson Holding with a total value of $221,040.

Tracking the Tuesday’s morning session, Ryerson Holding shares are trading at $24.78, showing a down of 0.0%.

About Ryerson Holding

Ryerson Holding Corp provides a metals service center, and value-added processor and is a distributor of industrial metals with operations in the United States, Canada, and Mexico. In addition to its North American operations, it conducts processing and distribution operations in China. Its customers range from local, independently owned fabricators and machine shops to large, international original equipment manufacturers. It carries a full line of products in stainless steel, aluminum, carbon steel, and alloy steels and a limited line of nickel and red metals in various shapes and forms. The company generates substantially all of its revenue from sales of metal products. Geographically, the majority is from the United States.

Ryerson Holding: Financial Performance Dissected

Revenue Growth: Ryerson Holding’s revenue growth over a period of 3 months has faced challenges. As of 30 September, 2024, the company experienced a revenue decline of approximately -9.63%. This indicates a decrease in the company’s top-line earnings. As compared to competitors, the company encountered difficulties, with a growth rate lower than the average among peers in the Materials sector.

Insights into Profitability:

-

Gross Margin: The company excels with a remarkable gross margin of 17.93%, indicating superior cost efficiency and profitability compared to its industry peers.

-

Earnings per Share (EPS): With an EPS below industry norms, Ryerson Holding exhibits below-average bottom-line performance with a current EPS of -0.2.

Debt Management: With a high debt-to-equity ratio of 1.07, Ryerson Holding faces challenges in effectively managing its debt levels, indicating potential financial strain.

Evaluating Valuation:

-

Price to Earnings (P/E) Ratio: A higher-than-average P/E ratio of 39.33 suggests caution, as the stock may be overvalued in the eyes of investors.

-

Price to Sales (P/S) Ratio: The current P/S ratio of 0.18 is below industry norms, suggesting potential undervaluation and presenting an investment opportunity for those considering sales performance.

-

EV/EBITDA Analysis (Enterprise Value to its Earnings Before Interest, Taxes, Depreciation & Amortization): Ryerson Holding’s EV/EBITDA ratio, surpassing industry averages at 11.1, positions it with an above-average valuation in the market.

Market Capitalization Perspectives: The company’s market capitalization falls below industry averages, signaling a relatively smaller size compared to peers. This positioning may be influenced by factors such as perceived growth potential or operational scale.

Now trade stocks online commission free with Charles Schwab, a trusted and complete investment firm.

Illuminating the Importance of Insider Transactions

In the complex landscape of investment decisions, investors should approach insider transactions as part of a comprehensive analysis, considering various elements.

When discussing legal matters, the term “insider” refers to any officer, director, or beneficial owner holding more than ten percent of a company’s equity securities, as stipulated in Section 12 of the Securities Exchange Act of 1934. This includes executives in the c-suite and significant hedge funds. Such insiders are required to report their transactions through a Form 4 filing, which must be completed within two business days of the transaction.

A new purchase by a company insider is a indication that they anticipate the stock will rise.

On the other hand, insider sells may not necessarily indicate a bearish view and can be motivated by various factors.

A Closer Look at Important Transaction Codes

Examining transactions, investors often concentrate on those unfolding in the open market, meticulously detailed in Table I of the Form 4 filing. A P in Box 3 denotes a purchase, while S signifies a sale. Transaction code C indicates the conversion of an option, and transaction code A denotes a grant, award, or other acquisition of securities from the company.

Check Out The Full List Of Ryerson Holding’s Insider Trades.

Insider Buying Alert: Profit from C-Suite Moves

Benzinga Edge reveals every insider trade in real-time. Don’t miss the next big stock move driven by insider confidence. Unlock this ultimate sentiment indicator now. Click here for access.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Jacobs Solutions Q4: Revenue Beats, EPS Misses, Muted FY25 Outlook & More

Jacobs Solutions Inc. J shares are trading lower after the company reported mixed fourth-quarter results.

The company reported fourth-quarter revenue growth of 4.4% year-over-year to $2.96 billion, beating the consensus of $2.368 billion. Adjusted revenue rose 4.3% YoY to $2.118 billion.

Adjusted EPS was $1.37, up from $1.07 a year ago, below the consensus of $1.54.

Gross margin was flat at 24.8% YoY and rose 4.2% to $735.21 million. Operating margin expanded 70 bps to 6.6% YoY, and operating profit rose 16.5% to $195.21 million.

Jacobs Recorded $187 million in mark-to-market gains on investment in AMTM, increasing GAAP net income.

The quarterly backlog reached $21.8 billion, marking a 22.5% year-over-year increase. The Q4 book-to-bill ratio was 1.67x (1.35x on a trailing twelve-month basis).

Operating cash flow for the quarter totaled $196.53 million, down from $219.36 million a year ago.

“Our GAAP net income margin and adjusted EBITDA margin showed strong sequential growth in Q4, and we plan to build on this strong performance in FY25. Furthermore, our balance sheet remains in excellent condition following the separation transaction. This financial strength positions us well to continue investing in organic growth while repurchasing shares and growing our dividend over the long-term,” commented CFO Venk Nathamuni.

Jacobs’ Chair and CEO Bob Pragada highlighted the company’s progress in its strategic shift toward a streamlined, higher-value portfolio, marked by the completion of the separation transaction for its Critical Mission Solutions and Cyber & Intelligence businesses. He noted strong demand in key end markets and continued momentum driving higher gross profit.

Looking ahead to FY25, Pragada expressed confidence in positive trends across Water and Environmental, Critical Infrastructure, and Life Sciences and Advanced Manufacturing, supported by a simplified structure, global delivery model, and operational efficiencies.

2025 Outlook: Jacobs Solutions projects Adjusted EPS in the range of $5.80 to $6.20. Adjusted net revenue is expected to grow at a mid-to-high single-digit rate.

The company anticipates an Adjusted EBITDA margin of 13.8% to 14.0% and forecasts reported free cash flow (FCF) conversion to exceed 100% of net income.

Price Action: J shares are trading lower by 1.83% at $137.79 at the last check Tuesday.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

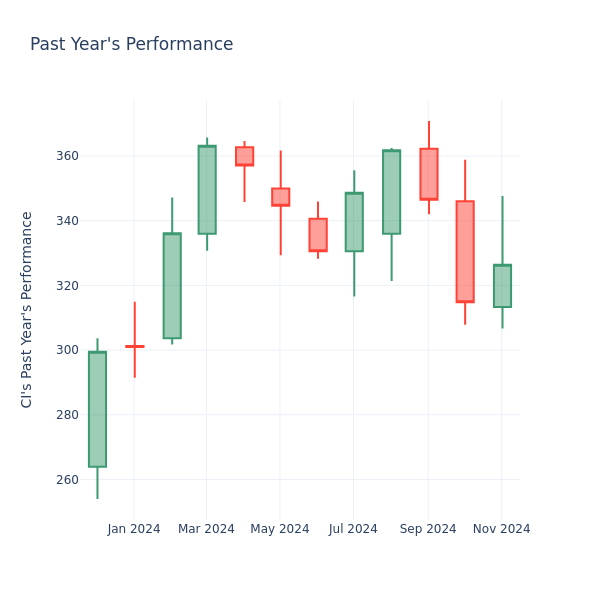

Price Over Earnings Overview: Cigna

In the current session, the stock is trading at $326.05, after a 1.12% increase. Over the past month, Cigna Inc. CI stock increased by 2.82%, and in the past year, by 13.21%. With performance like this, long-term shareholders are optimistic but others are more likely to look into the price-to-earnings ratio to see if the stock might be overvalued.

Evaluating Cigna P/E in Comparison to Its Peers

The P/E ratio is used by long-term shareholders to assess the company’s market performance against aggregate market data, historical earnings, and the industry at large. A lower P/E could indicate that shareholders do not expect the stock to perform better in the future or it could mean that the company is undervalued.

Compared to the aggregate P/E ratio of the 42.22 in the Health Care Providers & Services industry, Cigna Inc. has a lower P/E ratio of 30.56. Shareholders might be inclined to think that the stock might perform worse than it’s industry peers. It’s also possible that the stock is undervalued.

In summary, while the price-to-earnings ratio is a valuable tool for investors to evaluate a company’s market performance, it should be used with caution. A low P/E ratio can be an indication of undervaluation, but it can also suggest weak growth prospects or financial instability. Moreover, the P/E ratio is just one of many metrics that investors should consider when making investment decisions, and it should be evaluated alongside other financial ratios, industry trends, and qualitative factors. By taking a comprehensive approach to analyzing a company’s financial health, investors can make well-informed decisions that are more likely to lead to successful outcomes.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Kingsoft Cloud Q3 Earnings: Revenue Surges 16%, AI Growth Fuels Profits, CEO Shares Optimistic Outlook

Kingsoft Cloud Holdings KC reported a fiscal third-quarter 2024 revenue of 1.89 billion Chinese yuan ($268.7 million), up by 16.0% year-on-year, beating the analyst consensus estimate of $247.46 million.

The accelerated growth of high-quality businesses, such as AI, has offset the decline in the low-margin CDN business due to strategic proactive adjustments.

Kingsoft clocked an adjusted loss per ADS of 14 cents, which aligns with the analyst estimate. The stock price climbed after the print.

Revenues from public cloud services increased by 15.6% year over year to $167.5 million, mainly due to the growth of AI demands. Revenues from enterprise cloud services were $101.2 million, an increase of 16.7% Y/Y.

The adjusted gross profit was 307.6 million Chinese yuan ($43.8 million) versus 196.3 million Chinese yuan Y/Y.

The margin expanded by 420 bps to 16.3% due to strategic revenue mix adjustment, optimized enterprise cloud project selection, and efficient cost control measures.

Kingsoft held $230.6 million in cash and equivalents as of September end.

Kingsoft Cloud’s CEO, Tao Zou, emphasized the company’s commitment to its “High-quality and Sustainable Development Strategy,” which drove 16% topline growth in third-quarter of 2024. The AI business expanded to 362 million Chinese yuan, representing 31% of public cloud revenue. Revenues from the Xiaomi and Kingsoft Ecosystem surged by 36% year-over-year, capitalizing on opportunities in sectors like EVs, LLM, and WPS AI, reinforcing confidence in the company’s strategic direction.

CFO Henry He highlighted the company’s strong quarterly performance, marked by double-digit revenue growth to 1.89 billion Chinese yuan and significant profitability improvements. Gross profit and EBITDA profit growth outpaced industry averages. The adjusted EBITDA margin saw a remarkable turnaround, reflecting the success of the company’s revenue structure adjustment and AI-focused transformation.

Outlook: The company anticipates robust growth in the fourth quarter of 2024, driven by stable performance in public and enterprise cloud segments. It expects an accelerated revenue growth rate during the quarter and continued improvements in profitability. Operating profit and adjusted operating profit will likely show significant progress.

Kingsoft Cloud Holdings stock surged over 21% year-to-date.

Price Action: KC stock is up 3.48% at $4.49 at the last check on Tuesday.

Also Read:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Suze Orman Warns $3 Million Isn't Enough For Retirement, Even At A Mere 3% Withdrawal Rate – She Says You Need $10 Million Or More

Think $3 million is a solid retirement fund? Suze Orman has a reality check for you.

Speaking on the “Afford Anything” podcast, she explained why even this seemingly hefty amount might leave you struggling in retirement – especially if life throws a few curveballs your way.

Don’t Miss:

Orman was asked whether $3 million, paired with a conservative 3% withdrawal rate, could fund a secure early retirement. Her response? A flat-out no. She didn’t even hesitate to poke holes in the idea, calling $3 million “far from enough” for the unexpected costs life can throw at you.

The host, Paula Pant, asked Orman, “What would be a safe amount at which a person can say, ‘All right, at this point, given the size of my portfolio, I’m comfortable enough that if I did get hit by a bus, I would be fine.’?”

Orman answered, “It would have to be in the millions.” Pant, wanting a clearer answer, pressed further: “How many million?” That’s when Orman started doing the math – it wasn’t pretty.

“It depends where you live, what your expenses are,” Orman said. “Do you own your home outright? So, what are your expenses? But just think about it logically.”

And then she did exactly that: broke it down, line by line.

Trending: Deloitte’s fastest-growing software company partners with Amazon, Walmart & Target – You can still get 4,000 of its pre-IPO shares for with $1,000 for just $0.25/share

“Let’s say you need help. Remember, I took care of my mother and it cost me, like I said, $30,000 a month. $30,000 a month,” Orman emphasized. “So, you’re talking about, very possibly, for full-time help and everything – because good luck getting insurance and things to pay for it now – you’re talking about maybe $300,000, $400,000 a year.”

If that wasn’t sobering enough, she added: “Now you have other expenses – food and everything. Let’s just say you need another $100,000 a year to live. So now you’re at $350,000 a year after taxes.”

Trending: Can you guess how many retire with a $5,000,000 nest egg? The percentage may shock you.

To generate $350,000 annually after taxes without touching your principal, Orman said you’d need a portfolio yielding at least 5%. That means a whopping $10 million in assets, if not more.

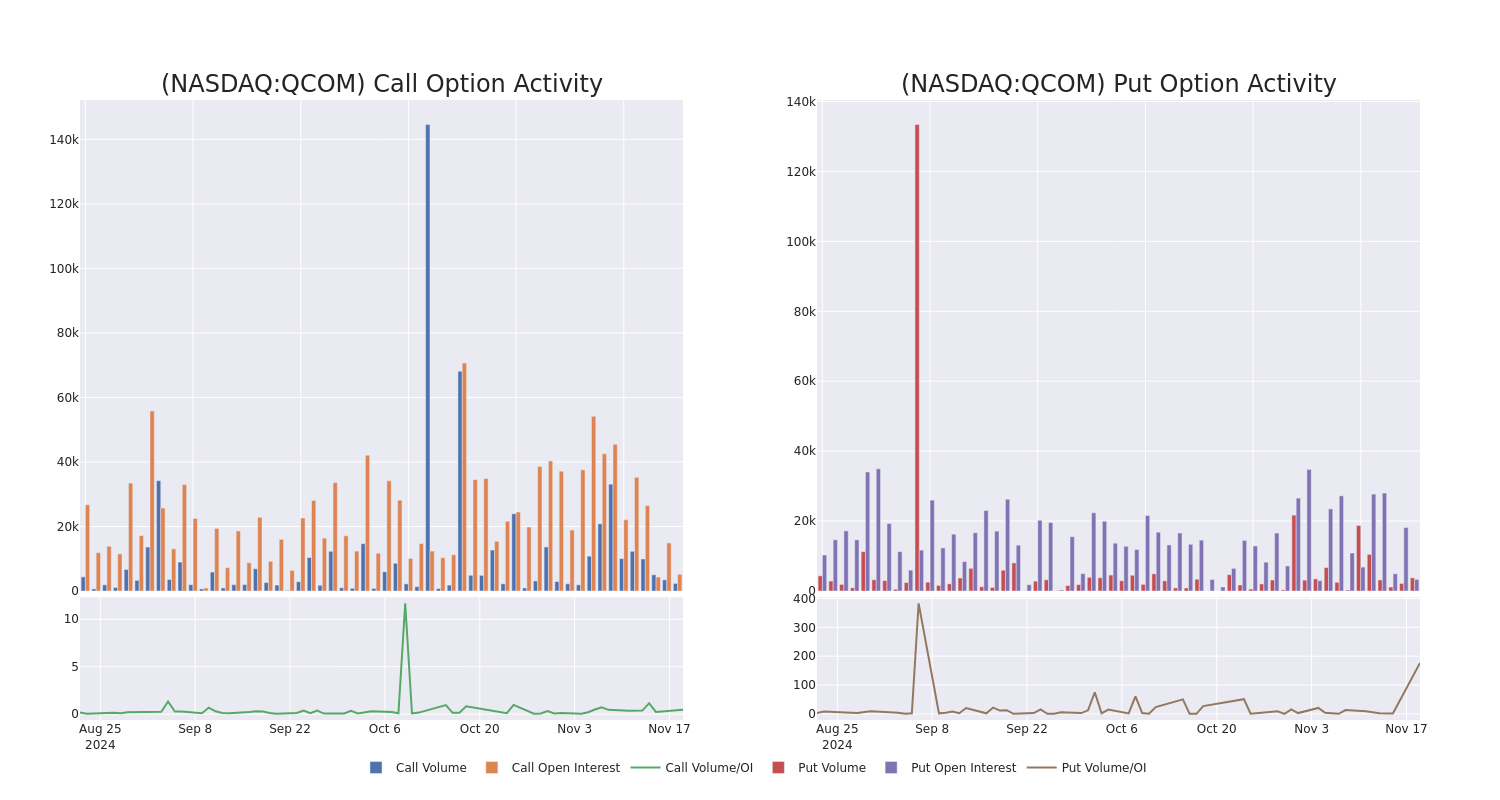

Qualcomm Unusual Options Activity

Whales with a lot of money to spend have taken a noticeably bearish stance on Qualcomm.

Looking at options history for Qualcomm QCOM we detected 13 trades.

If we consider the specifics of each trade, it is accurate to state that 38% of the investors opened trades with bullish expectations and 46% with bearish.

From the overall spotted trades, 7 are puts, for a total amount of $2,092,331 and 6, calls, for a total amount of $217,041.

What’s The Price Target?

Taking into account the Volume and Open Interest on these contracts, it appears that whales have been targeting a price range from $150.0 to $230.0 for Qualcomm over the last 3 months.

Volume & Open Interest Development

Assessing the volume and open interest is a strategic step in options trading. These metrics shed light on the liquidity and investor interest in Qualcomm’s options at specified strike prices. The forthcoming data visualizes the fluctuation in volume and open interest for both calls and puts, linked to Qualcomm’s substantial trades, within a strike price spectrum from $150.0 to $230.0 over the preceding 30 days.

Qualcomm Option Activity Analysis: Last 30 Days

Largest Options Trades Observed:

| Symbol | PUT/CALL | Trade Type | Sentiment | Exp. Date | Ask | Bid | Price | Strike Price | Total Trade Price | Open Interest | Volume |

|---|---|---|---|---|---|---|---|---|---|---|---|

| QCOM | PUT | SWEEP | BEARISH | 04/17/25 | $14.6 | $14.5 | $14.54 | $165.00 | $758.5K | 119 | 1.0K |

| QCOM | PUT | SWEEP | BEARISH | 04/17/25 | $14.55 | $14.45 | $14.55 | $165.00 | $699.9K | 119 | 1.0K |

| QCOM | PUT | TRADE | BULLISH | 07/18/25 | $11.15 | $10.8 | $10.8 | $150.00 | $324.0K | 2 | 300 |

| QCOM | PUT | SWEEP | BULLISH | 04/17/25 | $17.35 | $17.3 | $17.3 | $170.00 | $197.2K | 1.8K | 114 |

| QCOM | CALL | SWEEP | BULLISH | 11/22/24 | $2.38 | $2.3 | $2.42 | $165.00 | $55.9K | 2.6K | 659 |

About Qualcomm

Qualcomm develops and licenses wireless technology and designs chips for smartphones. The company’s key patents revolve around CDMA and OFDMA technologies, which are standards in wireless communications that are the backbone of all 3G, 4G, and 5G networks. Qualcomm’s IP is licensed by virtually all wireless device makers. The firm is also the world’s largest wireless chip vendor, supplying nearly every premier handset maker with leading-edge processors. Qualcomm also sells RF-front end modules into smartphones, as well as chips into automotive and Internet of Things markets.

Qualcomm’s Current Market Status

- With a trading volume of 2,592,300, the price of QCOM is down by -0.28%, reaching $164.04.

- Current RSI values indicate that the stock is is currently neutral between overbought and oversold.

- Next earnings report is scheduled for 71 days from now.

What The Experts Say On Qualcomm

A total of 5 professional analysts have given their take on this stock in the last 30 days, setting an average price target of $196.8.

Turn $1000 into $1270 in just 20 days?

20-year pro options trader reveals his one-line chart technique that shows when to buy and sell. Copy his trades, which have had averaged a 27% profit every 20 days. Click here for access.

* In a cautious move, an analyst from Loop Capital downgraded its rating to Hold, setting a price target of $180.

* An analyst from UBS has decided to maintain their Neutral rating on Qualcomm, which currently sits at a price target of $190.

* An analyst from Evercore ISI Group has decided to maintain their In-Line rating on Qualcomm, which currently sits at a price target of $199.

* Consistent in their evaluation, an analyst from Bernstein keeps a Outperform rating on Qualcomm with a target price of $215.

* Consistent in their evaluation, an analyst from JP Morgan keeps a Overweight rating on Qualcomm with a target price of $200.

Options are a riskier asset compared to just trading the stock, but they have higher profit potential. Serious options traders manage this risk by educating themselves daily, scaling in and out of trades, following more than one indicator, and following the markets closely.

If you want to stay updated on the latest options trades for Qualcomm, Benzinga Pro gives you real-time options trades alerts.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Keysight Earnings Are Imminent; These Most Accurate Analysts Revise Forecasts Ahead Of Earnings Call

Keysight Technologies, Inc. KEYS will release earnings results for its fourth quarter, after the closing bell on Tuesday, Nov. 19.

Analysts expect the Santa Rosa, California-based bank to report quarterly earnings at $1.57 per share, down from $1.99 per share in the year-ago period. Keysight projects to report revenue of $1.26 billion for the recent quarter, compared to $1.31 billion a year earlier, according to data from Benzinga Pro.

On Oct. 28, Keysight and Analog Devices, Inc. ADI collaborated to create a comprehensive test solution for Gigabit Multimedia Serial Link (GMSL2TM) devices.

Keysight shares gained 1.4% to close at $151.42 on Monday.

Benzinga readers can access the latest analyst ratings on the Analyst Stock Ratings page. Readers can sort by stock ticker, company name, analyst firm, rating change or other variables.

Let’s have a look at how Benzinga’s most-accurate analysts have rated the company in the recent period.

- Barclays analyst Tim Long upgraded the stock from Equal-Weight to Overweight and raised the price target from $158 to $180 on Nov. 5. This analyst has an accuracy rate of 76%.

- Deutsche Bank analyst Matthew Niknam maintained a Buy rating and raised the price target from $163 to $175 on Aug. 26. This analyst has an accuracy rate of 61%.

- Baird analyst Richard Eastman maintained an Outperform rating and increased the price target from $160 to $163 on Aug. 22. This analyst has an accuracy rate of 79%.

- B of A Securities analyst David Ridley-Lane maintained an Underperform rating and raised the price target from $135 to $150 on Aug. 21. This analyst has an accuracy rate of 65%.

- JP Morgan analyst Samik Chatterjee maintained a Neutral rating and increased the price target from $155 to $165 on Aug. 21. This analyst has an accuracy rate of 73%.

Considering buying KEYS stock? Here’s what analysts think:

Read This Next:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

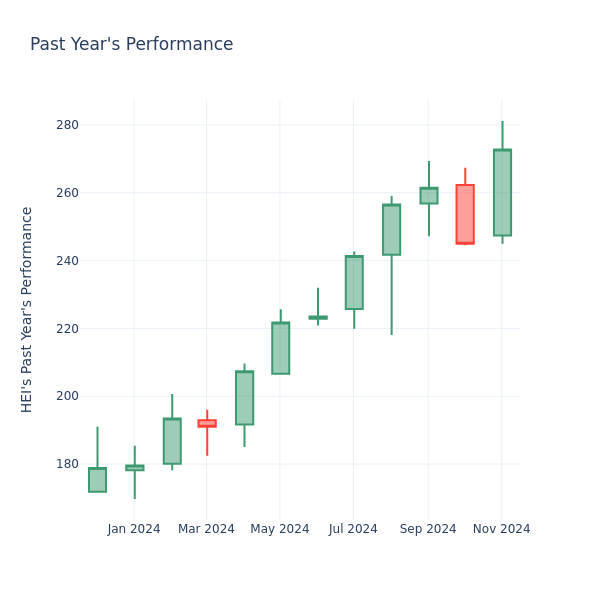

A Look Into Heico Inc's Price Over Earnings

In the current session, the stock is trading at $272.56, after a 1.08% increase. Over the past month, Heico Inc. HEI stock increased by 6.76%, and in the past year, by 57.14%. With performance like this, long-term shareholders are optimistic but others are more likely to look into the price-to-earnings ratio to see if the stock might be overvalued.

How Does Heico P/E Compare to Other Companies?

The P/E ratio measures the current share price to the company’s EPS. It is used by long-term investors to analyze the company’s current performance against it’s past earnings, historical data and aggregate market data for the industry or the indices, such as S&P 500. A higher P/E indicates that investors expect the company to perform better in the future, and the stock is probably overvalued, but not necessarily. It also could indicate that investors are willing to pay a higher share price currently, because they expect the company to perform better in the upcoming quarters. This leads investors to also remain optimistic about rising dividends in the future.

Heico has a better P/E ratio of 79.08 than the aggregate P/E ratio of 70.63 of the Aerospace & Defense industry. Ideally, one might believe that Heico Inc. might perform better in the future than it’s industry group, but it’s probable that the stock is overvalued.

In summary, while the price-to-earnings ratio is a valuable tool for investors to evaluate a company’s market performance, it should be used with caution. A low P/E ratio can be an indication of undervaluation, but it can also suggest weak growth prospects or financial instability. Moreover, the P/E ratio is just one of many metrics that investors should consider when making investment decisions, and it should be evaluated alongside other financial ratios, industry trends, and qualitative factors. By taking a comprehensive approach to analyzing a company’s financial health, investors can make well-informed decisions that are more likely to lead to successful outcomes.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

JLL and Slate Asset Management announce technology joint venture to tackle data challenges for real estate investors

JLL Asset Beacon integrates data across the commercial real estate asset management lifecycle, paving the way for AI-generated insights

CHICAGO, Nov. 19, 2024 /PRNewswire/ — JLL and Slate Asset Management (Slate) today announced a joint venture to commercialize Slate’s best-in-class technology platform for commercial real estate (CRE) professionals. The result is JLL Asset Beacon, a software-as-a-service (SaaS) technology platform that integrates data across asset management functions to create a real-time, end-to-end view of performance—whether it’s a single asset, fund, or the entire portfolio.

JLL Asset Beacon provides CRE professionals with accurate, integrated data to make informed decisions faster, optimize portfolio performance, mitigate risks, and identify opportunities for value creation. This private and secure hub captures all financial, operational, and leasing data and documents to provide a single source of truth with robust and customizable data visualization and reporting capabilities.

JLL’s generative AI capabilities, powered by the recently launched JLL Falcon platform, such as lease abstraction, entity resolution, and natural language query functionality will be integrated into JLL Asset Beacon, allowing users to unlock the potential of AI to organize and derive insights from their proprietary data.

“Our software gives real estate professionals a powerful competitive edge by providing better data insights and transparency that, in turn, enable faster and more informed decision making and ultimately drive value creation,” said Blair Welch, founding partner of Slate. “We have been developing, refining, and evolving this platform since Slate’s inception, and it has been a key to our strategic growth. Together with JLL, we can take this platform to the next level and make it available to a broader group of users, including investment managers, allocators, asset managers and limited partners.”

According to JLL Research, CRE portfolio diversification has grown over the past decade, making active asset management even more challenging. Advanced SaaS platforms such as JLL Asset Beacon validate, consolidate, and reconcile large amounts of data—helping investors maximize value through dynamic decision making.

“Active asset management is the driving force behind unlocking and enhancing value in real estate investments,” said Richard Bloxam, CEO of Capital Markets at JLL. “As the market recovers, capital deployment will focus on strategies offering returns that are competitive against the higher cost of capital. By leveraging data-driven insights, JLL Asset Beacon will help clients optimize their investments throughout the asset management lifecycle, across geographies and asset classes, to enable better decisions that deliver superior returns.”

Amit Koren, CEO of Leasing and Capital Markets Technology Group at JLL, added: “Slate’s powerful asset management hub, combined with JLL’s domain expertise and advanced AI capabilities, sets a new standard for data-driven, proactive asset management for our clients. JLL Asset Beacon will empower asset and portfolio managers with unparalleled insights, agility and efficiency for more precise decision-making about investment strategies in an increasingly complex market landscape.”

JLL’s Amir Leitersdorf and Iri Amirav will serve as co-CEOs of the joint venture. Both are seasoned technology entrepreneurs who joined JLL in 2021 when their company, Skyline AI, was acquired by JLL as a strategic addition to JLL’s technology portfolio.

About JLL

For over 200 years, JLL JLL, a leading global commercial real estate and investment management company, has helped clients buy, build, occupy, manage and invest in a variety of commercial, industrial, hotel, residential and retail properties. A Fortune 500® company with annual revenue of $20.8 billion and operations in over 80 countries around the world, our more than 111,000 employees bring the power of a global platform combined with local expertise. Driven by our purpose to shape the future of real estate for a better world, we help our clients, people and communities SEE A BRIGHTER WAYSM. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com.

About Slate Asset Management

Slate Asset Management is a global alternative investment platform. We focus on fundamentals with the objective of creating long-term value for our investors and partners. Slate’s platform focuses on four areas of real assets, including real estate equity, real estate credit, real estate securities, and infrastructure. We are supported by exceptional people and flexible capital, which enable us to originate and execute on a wide range of compelling investment opportunities. Visit slateam.com to learn more, and follow Slate Asset Management on LinkedIn, X (Twitter), and Instagram.

Contact: Jesse Tron

Phone: + 1 914 424 0299

Email: jesse.tron@jll.com

Contact: Karolina Kmiecik, Head of Communications

Phone: +1 224 848 0662

Email: karolina@slateam.com

![]()

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/jll-and-slate-asset-management-announce-technology-joint-venture-to-tackle-data-challenges-for-real-estate-investors-302310111.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/jll-and-slate-asset-management-announce-technology-joint-venture-to-tackle-data-challenges-for-real-estate-investors-302310111.html

SOURCE JLL-IR

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.