Petrobras to distribute up to $55bn in dividends by 2029

Brazilian state-controlled oil company Petrobras has unveiled a plan to distribute up to $55bn in dividends up to 2029 as part of its five-year business strategy, aiming to maintain its commitment to returning cash to investors, as reported by Bloomberg.

The company stated in a recent securities filing that it may also disburse up to $10bn in extraordinary dividends during this period.

Payment of an additional 20bn reais ($3.4bn) in extraordinary dividends to shareholders has also been approved by the company.

Analysts have responded positively to the continued shareholder payouts, with 83% rating the stock as a buy, according to Bloomberg data.

Petrobras has confirmed a 9% increase in its strategic plan to $111bn, though it has reduced estimated capital spending for 2025 to $18.5bn from $21bn.

A significant portion of the expenditure, $77.3bn, is allocated to exploration and production projects both within and outside the country. The business plan includes ten new offshore production units, with an additional five vessels planned post-2029.

Petrobras is also considering six more production vessels, including a 12th platform for the Buzios field in the pre-salt region of the Atlantic.

The company has raised its debt ceiling from $65bn to $75bn while increasing investments for the expansion of oil and gas production. Its minimum cash holding is lowered to $6bn.

Petrobras CFO Fernando Melgarejo stated in an interview in September 2024 that the increased debt ceiling does not necessarily imply more debt but offers increased flexibility in debt management.

Petrobras is under pressure to balance rewarding shareholders with dividends and investing sufficiently to help the government achieve its economic growth targets.

The company’s next five-year plan of renewable spending allocates $11bn to gas, energy and low-carbon projects, with only 27% of this spending directed at projects currently underway. The remainder is still under evaluation.

The renewables strategy includes solar, onshore wind and biofuels, with a return to ethanol production.

“Petrobras to distribute up to $55bn in dividends by 2029” was originally created and published by Offshore Technology, a GlobalData owned brand.

The information on this site has been included in good faith for general informational purposes only. It is not intended to amount to advice on which you should rely, and we give no representation, warranty or guarantee, whether express or implied as to its accuracy or completeness. You must obtain professional or specialist advice before taking, or refraining from, any action on the basis of the content on our site.

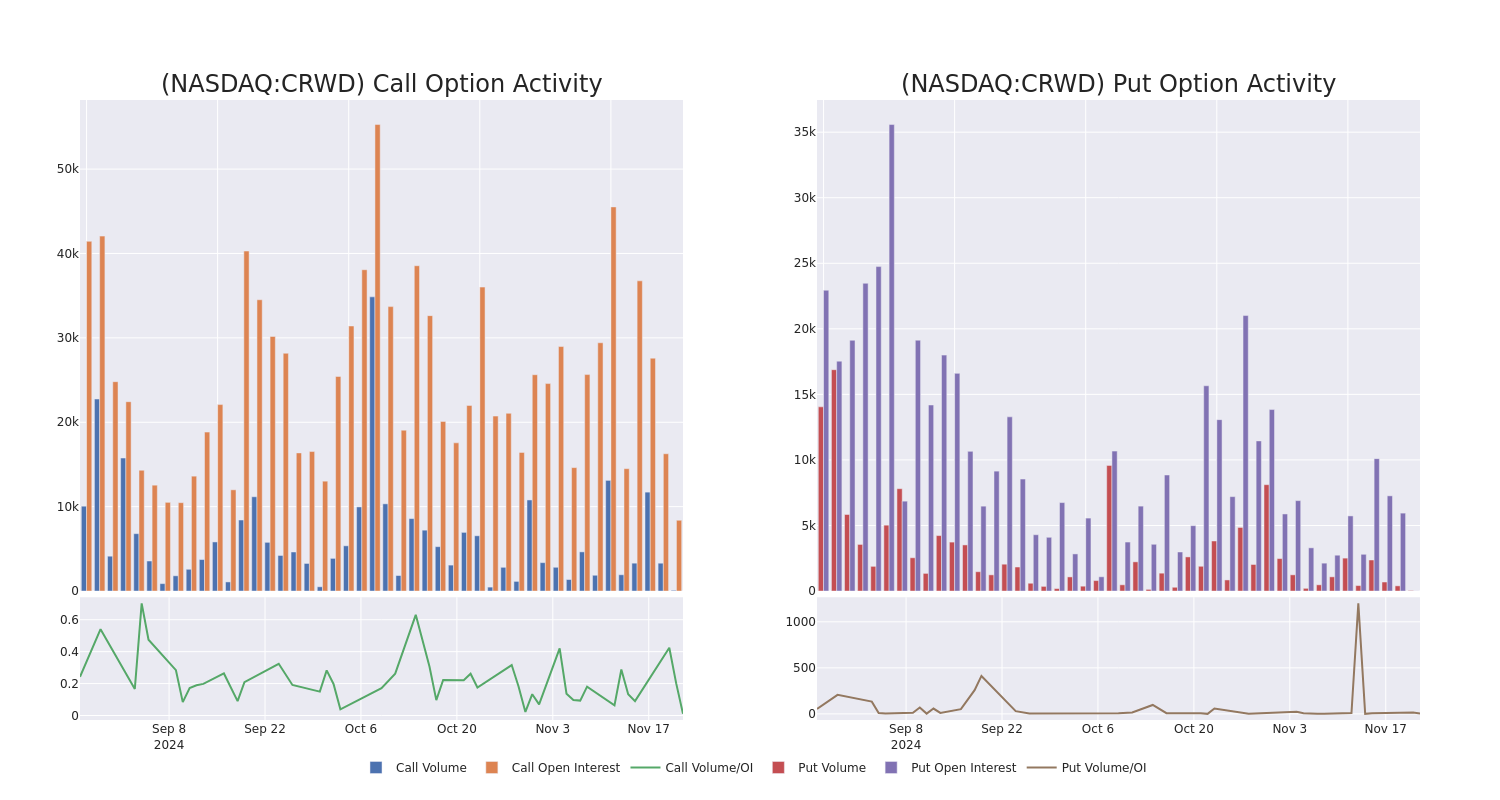

Market Whales and Their Recent Bets on CRWD Options

High-rolling investors have positioned themselves bearish on CrowdStrike Holdings CRWD, and it’s important for retail traders to take note.

This activity came to our attention today through Benzinga’s tracking of publicly available options data. The identities of these investors are uncertain, but such a significant move in CRWD often signals that someone has privileged information.

Today, Benzinga’s options scanner spotted 9 options trades for CrowdStrike Holdings. This is not a typical pattern.

The sentiment among these major traders is split, with 22% bullish and 55% bearish. Among all the options we identified, there was one put, amounting to $61,500, and 8 calls, totaling $240,940.

Predicted Price Range

Based on the trading activity, it appears that the significant investors are aiming for a price territory stretching from $80.0 to $370.0 for CrowdStrike Holdings over the recent three months.

Volume & Open Interest Development

In today’s trading context, the average open interest for options of CrowdStrike Holdings stands at 932.67, with a total volume reaching 124.00. The accompanying chart delineates the progression of both call and put option volume and open interest for high-value trades in CrowdStrike Holdings, situated within the strike price corridor from $80.0 to $370.0, throughout the last 30 days.

CrowdStrike Holdings Option Activity Analysis: Last 30 Days

Significant Options Trades Detected:

| Symbol | PUT/CALL | Trade Type | Sentiment | Exp. Date | Ask | Bid | Price | Strike Price | Total Trade Price | Open Interest | Volume |

|---|---|---|---|---|---|---|---|---|---|---|---|

| CRWD | PUT | TRADE | BEARISH | 12/13/24 | $21.05 | $19.3 | $20.5 | $365.00 | $61.5K | 7 | 38 |

| CRWD | CALL | SWEEP | BULLISH | 12/20/24 | $87.15 | $84.7 | $86.5 | $280.00 | $34.6K | 967 | 4 |

| CRWD | CALL | TRADE | BEARISH | 12/06/24 | $26.3 | $23.0 | $23.0 | $350.00 | $34.5K | 369 | 0 |

| CRWD | CALL | TRADE | NEUTRAL | 12/20/24 | $21.4 | $20.2 | $20.84 | $370.00 | $31.2K | 1.5K | 18 |

| CRWD | CALL | SWEEP | BEARISH | 12/20/24 | $30.05 | $29.7 | $29.7 | $350.00 | $29.7K | 2.7K | 41 |

About CrowdStrike Holdings

CrowdStrike is a cloud-based cybersecurity company specializing in next-generation security verticals such as endpoint, cloud workload, identity, and security operations. CrowdStrike’s primary offering is its Falcon platform that offers a proverbial single pane of glass for an enterprise to detect and respond to security threats attacking its IT infrastructure. The Texas-based firm was founded in 2011 and went public in 2019.

Having examined the options trading patterns of CrowdStrike Holdings, our attention now turns directly to the company. This shift allows us to delve into its present market position and performance

Present Market Standing of CrowdStrike Holdings

- Currently trading with a volume of 328,151, the CRWD’s price is up by 1.61%, now at $363.32.

- RSI readings suggest the stock is currently may be overbought.

- Anticipated earnings release is in 4 days.

Professional Analyst Ratings for CrowdStrike Holdings

A total of 5 professional analysts have given their take on this stock in the last 30 days, setting an average price target of $358.4.

Turn $1000 into $1270 in just 20 days?

20-year pro options trader reveals his one-line chart technique that shows when to buy and sell. Copy his trades, which have had averaged a 27% profit every 20 days. Click here for access.

* An analyst from Barclays persists with their Overweight rating on CrowdStrike Holdings, maintaining a target price of $372.

* In a cautious move, an analyst from CICC downgraded its rating to Market Perform, setting a price target of $295.

* An analyst from JMP Securities downgraded its action to Market Outperform with a price target of $400.

* An analyst from Cantor Fitzgerald persists with their Overweight rating on CrowdStrike Holdings, maintaining a target price of $370.

* Consistent in their evaluation, an analyst from Morgan Stanley keeps a Overweight rating on CrowdStrike Holdings with a target price of $355.

Options are a riskier asset compared to just trading the stock, but they have higher profit potential. Serious options traders manage this risk by educating themselves daily, scaling in and out of trades, following more than one indicator, and following the markets closely.

If you want to stay updated on the latest options trades for CrowdStrike Holdings, Benzinga Pro gives you real-time options trades alerts.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Insights into Central Garden & Pet's Upcoming Earnings

Central Garden & Pet CENT is gearing up to announce its quarterly earnings on Monday, 2024-11-25. Here’s a quick overview of what investors should know before the release.

Analysts are estimating that Central Garden & Pet will report an earnings per share (EPS) of $-0.20.

The announcement from Central Garden & Pet is eagerly anticipated, with investors seeking news of surpassing estimates and favorable guidance for the next quarter.

It’s worth noting for new investors that guidance can be a key determinant of stock price movements.

Past Earnings Performance

The company’s EPS beat by $0.11 in the last quarter, leading to a 5.84% increase in the share price on the following day.

Here’s a look at Central Garden & Pet’s past performance and the resulting price change:

| Quarter | Q3 2024 | Q2 2024 | Q1 2024 | Q4 2023 |

|---|---|---|---|---|

| EPS Estimate | 1.21 | 0.80 | -0.14 | 0.06 |

| EPS Actual | 1.32 | 0.99 | 0.01 | 0.08 |

| Price Change % | 6.0% | 11.0% | 6.0% | -10.0% |

Performance of Central Garden & Pet Shares

Shares of Central Garden & Pet were trading at $38.36 as of November 21. Over the last 52-week period, shares are up 21.81%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

Analyst Views on Central Garden & Pet

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Central Garden & Pet.

A total of 2 analyst ratings have been received for Central Garden & Pet, with the consensus rating being Buy. The average one-year price target stands at $44.0, suggesting a potential 14.7% upside.

Comparing Ratings with Competitors

This comparison focuses on the analyst ratings and average 1-year price targets of Spectrum Brands Holdings, Energizer Hldgs and WD-40, three major players in the industry, shedding light on their relative performance expectations and market positioning.

- As per analysts’ assessments, Spectrum Brands Holdings is favoring an Neutral trajectory, with an average 1-year price target of $94.0, suggesting a potential 145.05% upside.

- For Energizer Hldgs, analysts project an Neutral trajectory, with an average 1-year price target of $37.25, indicating a potential 2.89% downside.

- WD-40 is maintaining an Buy status according to analysts, with an average 1-year price target of $308.0, indicating a potential 702.92% upside.

Peers Comparative Analysis Summary

The peer analysis summary outlines pivotal metrics for Spectrum Brands Holdings, Energizer Hldgs and WD-40, demonstrating their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Central Garden & Pet | Buy | -2.63% | $317.06M | 5.14% |

| Spectrum Brands Holdings | Neutral | 4.46% | $288.10M | 1.35% |

| Energizer Hldgs | Neutral | -0.67% | $306.80M | 36.73% |

| WD-40 | Buy | 11.06% | $84.34M | 7.39% |

Key Takeaway:

Central Garden & Pet ranks at the top for Revenue Growth with a negative growth rate, indicating potential challenges. In terms of Gross Profit, it is at the top, showcasing strong profitability. However, its Return on Equity is at the bottom, suggesting lower returns for shareholders compared to peers. Overall, Central Garden & Pet’s performance is mixed compared to its peers in the analysis.

Delving into Central Garden & Pet’s Background

Central Garden & Pet Co understands that home is central to life and has nurtured happy and healthy homes for over forty years. The segments of the company are the pet segment and garden segment. The company’s trusted products are dedicated to helping lawns grow greener, gardens bloom bigger, pets live healthier and communities grow stronger. Central is home to a portfolio of more than sixty-five brands including Pennington, Nylabone, Kaytee, Amdro, and Aqueon, manufacturing and distribution capabilities, and a passionate, entrepreneurial growth culture. Central Garden and Pet is based in Walnut Creek, California, and has offices across North America and Europe.

Central Garden & Pet: A Financial Overview

Market Capitalization Analysis: Reflecting a smaller scale, the company’s market capitalization is positioned below industry averages. This could be attributed to factors such as growth expectations or operational capacity.

Revenue Challenges: Central Garden & Pet’s revenue growth over 3 months faced difficulties. As of 30 June, 2024, the company experienced a decline of approximately -2.63%. This indicates a decrease in top-line earnings. In comparison to its industry peers, the company trails behind with a growth rate lower than the average among peers in the Consumer Staples sector.

Net Margin: Central Garden & Pet’s net margin falls below industry averages, indicating challenges in achieving strong profitability. With a net margin of 8.0%, the company may face hurdles in effective cost management.

Return on Equity (ROE): Central Garden & Pet’s ROE lags behind industry averages, suggesting challenges in maximizing returns on equity capital. With an ROE of 5.14%, the company may face hurdles in achieving optimal financial performance.

Return on Assets (ROA): Central Garden & Pet’s ROA is below industry standards, pointing towards difficulties in efficiently utilizing assets. With an ROA of 2.23%, the company may encounter challenges in delivering satisfactory returns from its assets.

Debt Management: Central Garden & Pet’s debt-to-equity ratio is below industry norms, indicating a sound financial structure with a ratio of 0.87.

To track all earnings releases for Central Garden & Pet visit their earnings calendar on our site.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

US Business Activity Soars To 31-Month Highs In November: Small Caps Rally, Dow Tops 44,000

The U.S. private sector activity posted its fastest pace of expansion in more than two and a half years in November, driven by exceptional growth in the services sector, which continues to far exceed even the most optimistic forecasts by economists.

Business sentiment indicators in both the services and manufacturing sectors, as measured by S&P Global’s Purchasing Managers’ Index (PMI), improved in November. The services sector recorded its strongest growth since March 2022, while manufacturing saw a slower pace of contraction.

US November S&P Global’s PMI Report: Key Highlights

- The Flash Composite PMI rose from 54.1 in October to 55.3 in November, marking the strongest growth since April 2022.

- The Flash Services PMI also soared from 55 to 57, surpassing estimates of 57.2 as tracked by TradingEconomics.

- The Flash Manufacturing PMI inched up from 48.5 to 48.8, matching expectations.

- Companies’ outlook for the year ahead rose to their highest levels since May 2022, fueled by optimism over potential interest rate cuts, stronger economic growth, and more favorable business policies anticipated by the new administration in 2025.

- Employment declined for the fourth consecutive month, while output price inflation eased to its lowest level since June 2020.

- While growth remained concentrated in the services sector, increased optimism and renewed hiring in manufacturing signaled the potential for a broader recovery in the months ahead.

“The rise in the headline flash PMI indicates that economic growth is accelerating in the fourth quarter, while at the same time inflationary pressures are cooling,” said Chris Williamson, chief business economist at S&P Global Market Intelligence.

According to Williamson, the survey’s price index for goods and services suggests that consumer inflation is running significantly below the Federal Reserve’s 2% target.

Williamson also highlighted the increasing optimism for next-year output from goods-producing businesses. “The promise of greater protectionism and tariffs has helped lift confidence in the U.S. good producing sector, which is already feeding through to higher factory employment,” he said.

Market reactions: Stocks rise, dollar holds at 2-year highs

A new round of strong economic data fueled a rally in U.S. stocks, particularly among those most sensitive to domestic economic momentum.

Small-cap stocks, tracked by the iShares Russell 2000 ETF IWM, rallied 1.2% on Friday, aiming for their fifth consecutive session of gains.

Blue-chip stocks also posted solid performances, with the Dow Jones, represented by the SPDR Dow Jones Industrial Average ETF DIA, climbing 0.5% and surpassing the 44,000 mark.

The U.S. dollar index (DXY), tracked via the Invesco DB USD Index Bullish Fund ETF UUP, held steady with a 0.6% gain after touching fresh two-year highs earlier in the session.

Meanwhile, Treasury yields remained flat, and gold advanced 1.1%, also targeting its fifth straight session of gains.

Read Next:

Photo: Shutterstock

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Natural Grocers By Vitamin Cottage, Elastic, Matthews International, Gap And Other Big Stocks Moving Higher On Friday

U.S. stocks were mixed, with the Dow Jones index gaining more than 150 points on Friday.

Shares of Natural Grocers by Vitamin Cottage, Inc. NGVC rose sharply during Friday’s session following quarterly results.

Natural Grocers reported quarterly earnings of 39 cents per share, representing a 50% increase over earnings of 26 cents per share from the same period last year. The company reported $322.66 million in sales this quarter.

Natural Grocers by Vitamin Cottage shares jumped 15.3% to $41.78 on Friday.

Here are some other big stocks recording gains in today’s session.

- Replimune Group, Inc. REPL shares jumped 41.5% to $15.64 after the company on Thursday announced it received breakthrough therapy designation status for RP1 and will submit an RP1 biologics license application to the FDA under an accelerated approval pathway.

- Omeros Corporation OMER shares surged 26.4% to $9.75.

- D-Wave Quantum Inc. QBTS jumped 20.6% to $2.3750 after the company issued expectations for quarter-over-quarter fourth-quarter revenue growth.

- Navitas Semiconductor Corporation NVTS gained 18.8% to $2.4000.

- Elastic N.V. ESTC gained 16.6% to $109.82 after the company reported better-than-expected second-quarter financial results and issued FY25 guidance above estimates.

- Matthews International Corporation MATW surged 16.6% to $29.74 following upbeat earnings.

- Wolfspeed, Inc. WOLF rose 16.2% to $7.48.

- Viasat, Inc. VSAT gained 14.3% to $9.52.

- Protagonist Therapeutics, Inc. PTGX jumped 12.3% to $46.81.

- Super Micro Computer, Inc. SMCI gained 10.7% to $32.90.

- SoundHound AI, Inc. SOUN shares rose 10.66% to $7.72.

- Polestar Automotive Holding UK PLC PSNY shares jumped 9.1% to $1.2000

- Atkore Inc. ATKR gained 8.6% to $92.44.

- The Gap, Inc. GAP jumped 6% to $23.35 following upbeat earnings.

- Carpenter Technology Corporation CRS gained 5.3% to $190.29 JP Morgan analyst Bennett Moore initiated coverage on Carpenter Tech with an Overweight rating and announced a price target of $220.

Now Read This:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

UPS to Pay $45 Million SEC Penalty Over Improper Valuation

(Bloomberg) — United Parcel Service Inc. will pay $45 million to settle claims by the US Securities and Exchange Commission that the courier misrepresented its financial results by improperly valuing its freight business.

Most Read from Bloomberg

The company failed to follow generally accepted accounting principles when it evaluated its less-than-truckload operations in 2019 and 2020, the SEC said Friday in a statement. “Had UPS properly valued Freight, its earnings and other reported items would have been materially lower,” the agency said.

UPS, which didn’t admit or deny the findings, agreed to avoid future violations, the SEC said.

The company said in an emailed statement that it recorded a non-cash goodwill impairment charge in 2020 relating to the investigation. “The settlement will not have a material effect on our business, financial condition, results of operation, or liquidity,” UPS said.

Goodwill is a non-cash asset companies record on their balance sheets when they buy another business and have to calculate how they came up with the purchase price. US accounting rules require companies to keep the asset as a line on their balance sheets, only marking it down when there’s a sign it has permanently lost value. Companies must test goodwill at least yearly for signs of it losing value.

The SEC’s order alleges that UPS used an outside consultant to value the freight business without providing certain information such as the company’s own internal analysis of the operations. UPS didn’t tell the consultant it had concluded that “a prospective buyer would expect Freight to generate significantly less profit after it was sold because it would no longer benefit from synergies and other cost savings it was getting as part of UPS,” according to the order.

UPS sold its freight business to TFI International in 2021 for $800 million.

Shares of UPS rose 1.9% as of 10:15 a.m. in New York.

–With assistance from Nicola M. White.

(Updates with company comment in fourth paragraph.)

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Earnings Preview: Bath & Body Works

Bath & Body Works BBWI is gearing up to announce its quarterly earnings on Monday, 2024-11-25. Here’s a quick overview of what investors should know before the release.

Analysts are estimating that Bath & Body Works will report an earnings per share (EPS) of $0.47.

Anticipation surrounds Bath & Body Works’s announcement, with investors hoping to hear about both surpassing estimates and receiving positive guidance for the next quarter.

New investors should understand that while earnings performance is important, market reactions are often driven by guidance.

Past Earnings Performance

During the last quarter, the company reported an EPS beat by $0.01, leading to a 4.0% drop in the share price on the subsequent day.

Here’s a look at Bath & Body Works’s past performance and the resulting price change:

| Quarter | Q2 2024 | Q1 2024 | Q4 2023 | Q3 2023 |

|---|---|---|---|---|

| EPS Estimate | 0.36 | 0.32 | 1.87 | 0.35 |

| EPS Actual | 0.37 | 0.38 | 2.06 | 0.48 |

| Price Change % | -4.0% | 5.0% | -0.0% | -2.0% |

Stock Performance

Shares of Bath & Body Works were trading at $30.55 as of November 21. Over the last 52-week period, shares are up 2.21%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

To track all earnings releases for Bath & Body Works visit their earnings calendar on our site.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

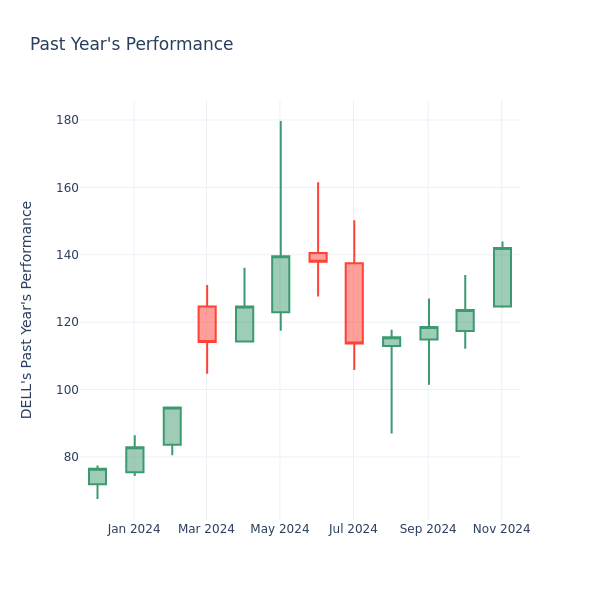

Price Over Earnings Overview: Dell Technologies

In the current session, the stock is trading at $142.32, after a 2.45% increase. Over the past month, Dell Technologies Inc. DELL stock increased by 15.96%, and in the past year, by 90.85%. With performance like this, long-term shareholders are optimistic but others are more likely to look into the price-to-earnings ratio to see if the stock might be overvalued.

A Look at Dell Technologies P/E Relative to Its Competitors

The P/E ratio is used by long-term shareholders to assess the company’s market performance against aggregate market data, historical earnings, and the industry at large. A lower P/E could indicate that shareholders do not expect the stock to perform better in the future or it could mean that the company is undervalued.

Compared to the aggregate P/E ratio of the 32.64 in the Technology Hardware, Storage & Peripherals industry, Dell Technologies Inc. has a lower P/E ratio of 25.58. Shareholders might be inclined to think that the stock might perform worse than it’s industry peers. It’s also possible that the stock is undervalued.

In summary, while the price-to-earnings ratio is a valuable tool for investors to evaluate a company’s market performance, it should be used with caution. A low P/E ratio can be an indication of undervaluation, but it can also suggest weak growth prospects or financial instability. Moreover, the P/E ratio is just one of many metrics that investors should consider when making investment decisions, and it should be evaluated alongside other financial ratios, industry trends, and qualitative factors. By taking a comprehensive approach to analyzing a company’s financial health, investors can make well-informed decisions that are more likely to lead to successful outcomes.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

S&P 500 Faces Volatile 2025 As 'Inflation Boom' Could Return: Bank Of America Strategist

The S&P 500 index is wrapping up a historic two-year run of consecutive over 20% gains, a feat achieved only four times in the past 150 years. Yet, Michael Hartnett, chief investment strategist at Bank of America, says the party may not last forever.

According to Hartnett’s latest Flow Show report, published Friday, the U.S. equity market is poised for another “double-digit move” in 2025 — though investors shouldn’t rule out the possibility of a second wave of inflation that could derail the bull market.

The Bank of America’s Investment Clock — a key barometer that shows the prevailing economic scenario in a given year — is transitioning from a “recovery” in 2024 to an “inflation boom” in 2025.

The S&P 500 — as tracked by the SPDR S&P 500 ETF Trust SPY — surged 24% in 2024, mirroring its 24% rally in 2023.

This back-to-back streak of 20%-plus returns happened just four times in the past century and a half: during 1927-’28, 1935-’36, 1954-’55, and 1995-’96.

However, history shows that the years following such rallies often see wild market swings, for better or worse.

- 1927-28: Followed by a -12% loss in 1929 and a catastrophic -28% drop in 1930.

- 1935-36: After two years of outsized returns, 1937 saw a brutal -39% decline.

- 1954-55: Markets cooled, with modest gains of +3% in 1956 and a -14% slide in 1957.

- 1995-96: Continued strength with a +31% gain in 1997 but slowed to +12% in 1998.

Will 2025 follow a similar script? Hartnett says a major move — up or down — should be expected.

Hartnett highlights three key drivers that can pave the way for the bull market to continue in 2025.

- A “boomy” economic backdrop: Companies are front-loading operations ahead of potential tariffs, labor hoarding remains rampant amid tighter immigration controls and unemployment claims have tumbled.

- Goldilocks bond yields: Despite $36 trillion in U.S. debt and a 7% GDP deficit, central banks are expected to cut rates in 2025 — Bank of America is forecasting 124 global rate cuts.

- Political incentives: The Trump administration is heavily invested in propping up risk assets like equities and cryptocurrencies to stimulate “animal spirits,” making a bear market unlikely heading into an election year.

With the S&P 500’s trailing price-to-earnings ratio now at 26.5x, it ranks as the fourth-highest valuation in 125 years, behind only December 1921, June 1999 and June 2021.

The U.S. stock market is sitting at 75-year highs relative to international equities, with just 10 companies accounting for a staggering 37% of market cap.

This concentration has been driven by the so-called “Magnificent Seven” tech giants — stocks whose collective market capitalization surged by $4 trillion in 2024.

But Hartnett indicates the narrative of U.S. exceptionalism, particularly in artificial intelligence, may be peaking cyclically.

Crunching the numbers, he highlighted that the S&P 500’s secular bull market, which began at 666 points in March 2009, could potentially climax at 6,666 in 2025.

Bank of America’s Investment Clock model indicates 2024 marked an equity-bullish “recovery” phase, driven by lower rates and higher corporate earnings.

But 2025 could transition into an “inflation boom” phase, where rising rates and price pressures become the dominant themes.

While Hartnett is bullish on commodities as a hedge against this scenario, he warns credit and equities may peak in early 2025.

Read Now:

Photo: Shutterstock

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

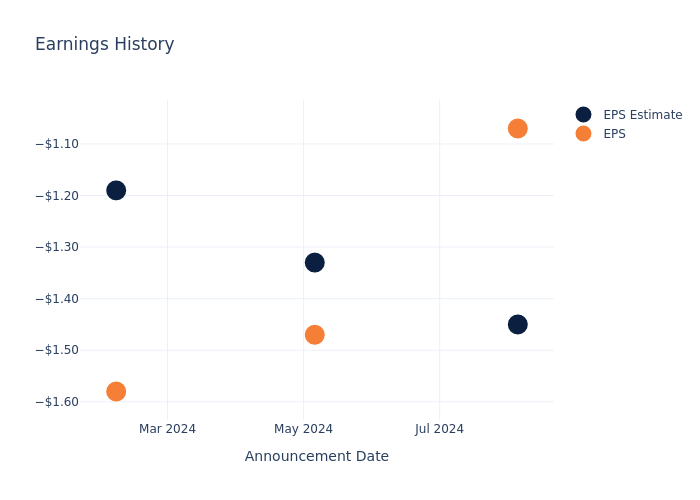

Enanta Pharma's Earnings Outlook

Enanta Pharma ENTA is gearing up to announce its quarterly earnings on Monday, 2024-11-25. Here’s a quick overview of what investors should know before the release.

Analysts are estimating that Enanta Pharma will report an earnings per share (EPS) of $-1.16.

The announcement from Enanta Pharma is eagerly anticipated, with investors seeking news of surpassing estimates and favorable guidance for the next quarter.

It’s worth noting for new investors that guidance can be a key determinant of stock price movements.

Historical Earnings Performance

In the previous earnings release, the company beat EPS by $0.38, leading to a 1.17% increase in the share price the following trading session.

Here’s a look at Enanta Pharma’s past performance and the resulting price change:

| Quarter | Q3 2024 | Q2 2024 | Q1 2024 | Q4 2023 |

|---|---|---|---|---|

| EPS Estimate | -1.45 | -1.33 | -1.19 | -2 |

| EPS Actual | -1.07 | -1.47 | -1.58 | -1.33 |

| Price Change % | 1.0% | -10.0% | 1.0% | 12.0% |

Stock Performance

Shares of Enanta Pharma were trading at $9.31 as of November 21. Over the last 52-week period, shares are down 1.98%. Given that these returns are generally negative, long-term shareholders are likely upset going into this earnings release.

Analyst Views on Enanta Pharma

For investors, grasping market sentiments and expectations in the industry is vital. This analysis explores the latest insights regarding Enanta Pharma.

A total of 3 analyst ratings have been received for Enanta Pharma, with the consensus rating being Outperform. The average one-year price target stands at $23.67, suggesting a potential 154.24% upside.

Comparing Ratings with Peers

The analysis below examines the analyst ratings and average 1-year price targets of and Macrogenics, three significant industry players, providing valuable insights into their relative performance expectations and market positioning.

Overview of Peer Analysis

The peer analysis summary presents essential metrics for and Macrogenics, unveiling their respective standings within the industry and providing valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Macrogenics | Neutral | 964.81% | $108.84M | 63.31% |

Key Takeaway:

Enanta Pharma ranks in the middle among its peers for Consensus rating. It is at the top for Revenue Growth, indicating strong performance in this area. Enanta Pharma also leads in Gross Profit, showcasing efficient cost management. However, it falls behind in Return on Equity compared to its peers.

Delving into Enanta Pharma’s Background

Enanta Pharmaceuticals Inc is an American biotechnology company focused on the research and development of molecule drugs to cure viral infections and liver diseases. The targeted diseases are hepatitis C, hepatitis B, nonalcoholic steatohepatitis, and the respiratory syncytial virus. The novelty of company research is a specific direct-acting antiviral inhibitor against the hepatitis C virus. The company’s inhibitors have been developed in collaboration with AbbVie. AbbVie markets the protease inhibitor, paritaprevir, while other inhibitors are in the pipeline.

Financial Milestones: Enanta Pharma’s Journey

Market Capitalization Highlights: Above the industry average, the company’s market capitalization signifies a significant scale, indicating strong confidence and market prominence.

Decline in Revenue: Over the 3 months period, Enanta Pharma faced challenges, resulting in a decline of approximately -4.88% in revenue growth as of 30 June, 2024. This signifies a reduction in the company’s top-line earnings. In comparison to its industry peers, the company trails behind with a growth rate lower than the average among peers in the Health Care sector.

Net Margin: Enanta Pharma’s net margin excels beyond industry benchmarks, reaching -126.08%. This signifies efficient cost management and strong financial health.

Return on Equity (ROE): Enanta Pharma’s ROE is below industry standards, pointing towards difficulties in efficiently utilizing equity capital. With an ROE of -14.38%, the company may encounter challenges in delivering satisfactory returns for shareholders.

Return on Assets (ROA): The company’s ROA is below industry benchmarks, signaling potential difficulties in efficiently utilizing assets. With an ROA of -5.58%, the company may need to address challenges in generating satisfactory returns from its assets.

Debt Management: Enanta Pharma’s debt-to-equity ratio surpasses industry norms, standing at 0.34. This suggests the company carries a substantial amount of debt, posing potential financial challenges.

To track all earnings releases for Enanta Pharma visit their earnings calendar on our site.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.