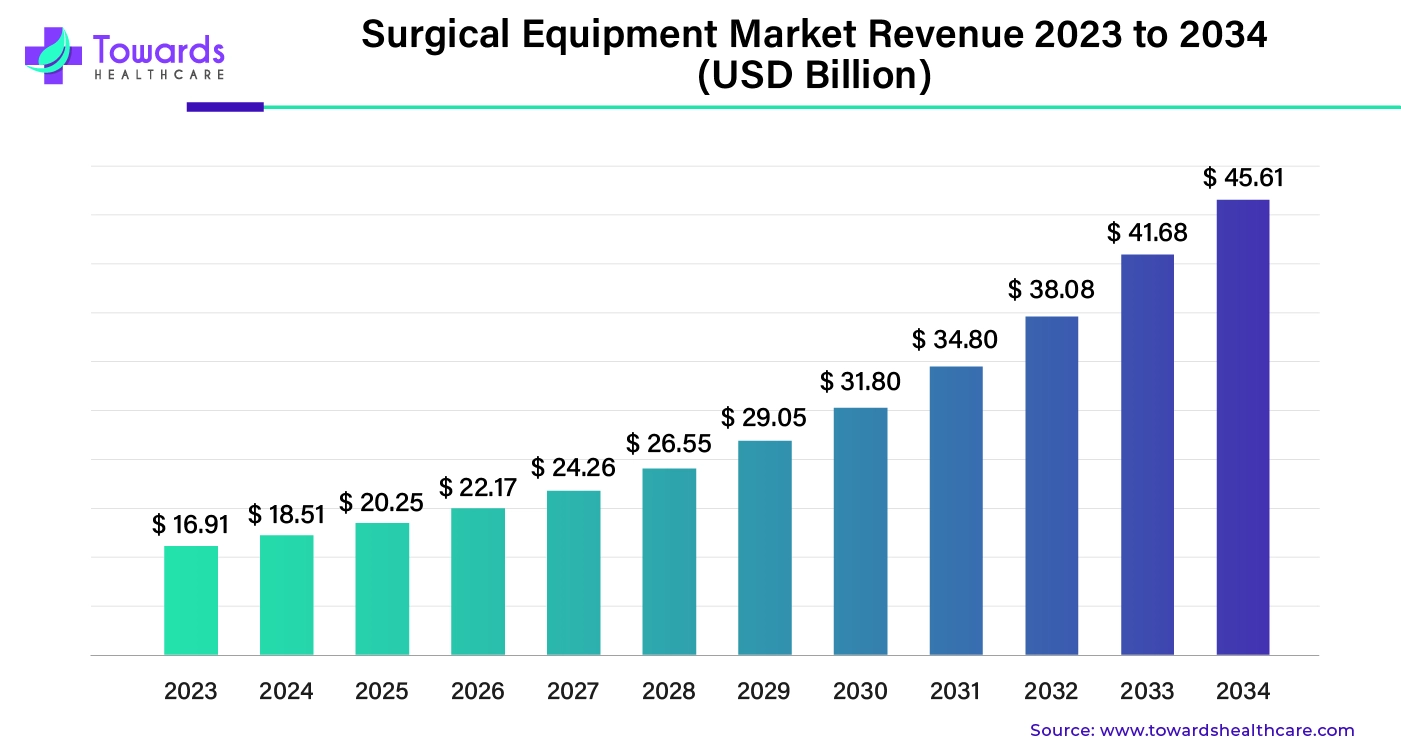

Surgical Equipment Market Size to Achieve USD 45.61 Bn by 2034

Ottawa, Oct. 31, 2024 (GLOBE NEWSWIRE) — The global surgical equipment market size is predicted to increase from USD 20.25 billion in 2025 to approximately USD 45.61 billion by 2034, according to a study published by Towards Healthcare a sister firm of Precedence Statistics. The industry is representing a solid CAGR of 9.44% during the forecast period. North America dominated the market with the largest market share of 41% in 2023.

Download a sample of this report @ https://www.towardshealthcare.com/download-statistics/5240

Key Takeaways

- Advancements in surgical techniques, the development of minimally invasive surgery techniques has increased the demand for specialized surgical equipment that allows for smaller incisions and faster recovery times.

- Rising prevalence of chronic diseases, the growing burden of chronic diseases such as heart disease, cancer and diabetes has led to an increase in surgical procedures.

- Technological innovations and advancements in medical technology including robotics, imaging and material science have led to the development of new and improved surgical equipment.

Regional Insights:

North America, Cosmetic Surgery Driving the Market

The region North America held the largest share of the surgical equipment market in 2023. The increasing number of surgical procedures, advancements in healthcare infrastructure and the presence of leading industry players are some of the factors which are driving the market in North America. The United States performs around 40 to 50 million surgeries annually which makes it a key contributor to the region’s market. For instance, in 2023, 9.5 million neuro modular procedures were conducted for wrinkle reduction, reflecting the growing demand for cosmetic surgeries.

Technological innovations in surgical tools and favorable government policies are also propelling market growth. For instance, in May of 2023, Crothall Healthcare Partnered with Ascendco Health to introduce advanced tracking systems for sterile surgical instruments in United States healthcare facilities. This partnership highlights the increasing focus on safety, quality and technological improvement.

Get the latest insights on healthcare industry segmentation with our Annual Membership: https://www.towardshealthcare.com/get-an-annual-membership

Asia Pacific on to Grow and is Fastest Growing Market

In the coming years Asia Pacific is expected to grow at the fastest rate in surgical equipment market. This growth is driven by a combination of factors such as rising geriatric population, Increasing surgical procedures and rapid healthcare infrastructure development. In the country India around 30 million surgical procedures are performed each year, and the country has attracted significant foreign direct investments in medical and surgical appliances which is over USD 3.28 billion from April 2000 to March 2024.

Countries like China, South Korea and Japan are global leaders in plastic surgeries ranking third, fourth and fifth respectively. Government policies are further fueling market growth in the region. For instance, in 2022 the Chinese government introduced a USD 29 billion loan incentive policy to upgrade medical facilities which is helping boost demand for advanced surgical tools.

- In June 2024, the Tamil Nadu state government in India announced plans to sell affordable surgical equipment to the public through government run medical shops. This initiative underscores the government’s focus on expanding access to high quality surgical equipment across the country.

Related Markets Impacted by Surgical Equipment Market:

3D Printed Medical Devices Market

The 3D printed medical devices market is closely connected to the surgical equipment market as both sectors rely on cutting edge technology and innovations to improve patient outcomes. 3D medical devices ranging from imaging equipment like MRI machines 2 monitoring devices and implants, are observed to gain momentum in the upcoming years. The increasing demand for advanced surgical tools naturally push the need for complementary medical devices that assist in diagnosis, monitoring and rehabilitation. Custom devices like hearing aids, orthotics, and surgical tools can be designed with precise measurements, offering a superior fit and enhancing patient comfort compared to mass-produced alternatives.

Medical Device Gaskets & Seals Market

The medical device gaskets & seals market was estimated at US$ 0.92 billion in 2023 and is projected to grow to US$ 1.57 billion by 2034, rising at a compound annual growth rate (CAGR) of 5% from 2024 to 2034. The surgical equipment market has positively impacted the Medical Device Gaskets & Seals Market in several significant ways, primarily driven by the growing demand for high-quality, reliable components in medical devices. As the surgical equipment market expands due to advancements in technology, increasing surgical procedures, and stringent regulatory standards, the need for effective gaskets and seals has surged.

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Surgical Equipment Market Opportunity

Growing Demand for Power Tools in Surgical Procedures:

In recent years, the increasing demand for power tools in surgical procedures is set to drive the growth of the surgical equipment market. With the rise of minimally invasive surgeries power tools such as saws, trains and reamers are becoming essential for surgeons. These tools provide precision, reduce operative time and enhance overall surgical outcomes. Battery driven cordless surgical power tools are one of the key developments in this field which is shifting the market.

- In March 2023, Stryker, a global leader in medical technology introduced a new line of battery powered surgical power tools. Their innovative system of 9 cordless surgical power tools uses lithium-ion batteries which offers longer operational time and enhanced performance. Surgeons have reported improved precision and workflow particularly in orthopedic surgeries.

Surgical Equipment Market Segments:

- By product, in 2023 the surgical structures and staplers segment held the largest share of the surgical equipment market. Structures and staplers are critical for wound closures in various types of surgeries, from minor procedures to major operations like cardiovascular and gastrointestinal surgeries. Their widespread use across different specialities and advancements in structure materials and stapling technology have driven the demand.

- By type, in 2023 disposable surgical equipment segment dominated the surgical equipment market. With growing concerns over hospital acquired infections and the need for sterile surgical environments, disposable tools like scalpels, forceps, and scissors are preferred for single use. They minimize cross contamination risks and ensure safety for both patients and healthcare professionals. In the July of 2023, Madeline Industries launched a new range of eco-friendly disposable surgical kits that offer enhanced safety while addressing environmental concerns by using biodegradable materials.

- By application, the others segment which includes various general and specialized surgeries like plastic surgery, urology and obstetrics, let the surgical equipment market in 2023. These surgeries are becoming more frequent due to an aging population, rising cancer cases and an increase in elective cosmetic procedures.

Recent Developments and News of the Market:

| Company | Indraprastha Apollo Hospital |

| Headquarter | New Delhi, India, Asia Pacific |

| Development | In March 2024, At Indraprastha Apollo Hospital in New Delhi, Apollo Hospitals introduced ZAP-X, a gyroscopic radiosurgery platform for the treatment of brain tumors. The US-based medical equipment manufacturer Zap Surgical is set to launch the platform in India. Apollo stated in an official statement that “ZAP-X will offer patients a non-invasive, pain-free alternative to traditional surgical interventions for brain tumors, with sessions lasting just 30 minutes and without the necessity of anesthesia. |

| Company | Crothall Healthcare |

| Headquarter | United States, North America |

| Development | May 2024, Crothall Healthcare (Crothall), a leading provider of sterile processing and support services, and Ascendco Health (Ascendco), a leading innovator in health technology, announced a groundbreaking partnership that will usher in a new era for instrument tracking and overall sterile processing quality within healthcare facilities across the nation. This partnership has the potential to significantly elevate standards within the field of sterile processing. |

Browse More Insights of Towards Healthcare:

- The drug-device combination products market size was estimated at $150.3 billion in 2023 and is projected to grow to $337.81 billion by 2034, with a CAGR of 7.64% from 2024 to 2034.

- The mycobacterium tuberculosis market was estimated at US$ 730.00 million in 2023 and is projected to grow to US$ 1,385.79 million by 2034, rising at a CAGR of 6% from 2024 to 2034.

- The safety lancets market was estimated at $2.1 billion in 2023 and is expected to grow to $6.32 billion by 2034, with a CAGR of 10.54% from 2024 to 2034.

- The peripheral nerve conduit market was estimated at $140 million in 2023 and is projected to grow to $411.58 million by 2034, with a CAGR of 10.3% from 2024 to 2034.

- The vet ultrasound system market was estimated at $400 million in 2023 and is projected to grow to $845.41 million by 2034, with a CAGR of 7.04% from 2024 to 2034.

- The ambulatory electrocardiography (ECG) market was estimated at $630 million in 2023 and is expected to grow to $1,561.24 million by 2034, with a CAGR of 8.6% from 2024 to 2034.

- The blood product market was estimated at $36.52 billion in 2023 and is projected to grow to $59.89 billion by 2034, with a CAGR of 4.6% from 2024 to 2034.

- The personal protective equipment (PPE) market was estimated at $79.57 billion in 2023 and is projected to grow to $171.66 billion by 2034, with a CAGR of 7.24% from 2024 to 2034.

- The cell therapy human raw materials market size was estimated at $2.91 billion in 2023 and is projected to grow to $22.75 billion by 2034, with a CAGR of 22.38% from 2023 to 2034.

- The biomaterials market size was estimated at $178.16 billion in 2023 and is projected to grow to $761.23 billion by 2033, with a CAGR of 15.63% from 2024 to 2033.

Surgical Equipment Market Top Companies

- Aesculap Implant Systems, Inc.

- ARCH Medical Solutions

- Arthrex

- BioRad Medisys Pvt. Ltd.

- Bricon GmbH

- InTech Medical

- KLS Martin Group

- Medtronic Plc

- Miraclus Orthotech Pvt. Ltd.

- Precision Spine, Inc.

- Trauson Medical Instruments

Segments Covered in the Report

By Product

- Surgical Sutures & Staplers

- Electrosurgical Devices

- Handheld Surgical Devices

- Forceps & Spatulas

- Retractors

- Dilators

- Graspers

- Auxiliary Instruments

- Cutter instruments

- Others

By Type

By Application

- Neurosurgery

- Plastic & Reconstructive Surgery

- Wound Closure

- Obstetrics & Gynecology

- Cardiovascular

- Orthopedic

- Others

By Region

- North America

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Latin America

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Discover our detailed Table of Contents (TOC) for the Industry, providing a thorough examination of market segments, material, emerging technologies and key trends. Our TOC offers a structured analysis of market dynamics, emerging innovations, and regional dynamics to guide your strategic decisions in this rapidly evolving healthcare field – https://www.towardshealthcare.com/table-of-content/surgical-equipment-market-sizing

Acquire our comprehensive analysis today @ https://www.towardshealthcare.com/price/5240

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Gain access to the latest insights and statistics in the healthcare industry by subscribing to our Annual Membership. Stay updated on healthcare industry segmentation with detailed reports, market trends, and expert analysis tailored to your needs. Stay ahead of the curve with valuable resources and strategic recommendations. Join today to unlock a wealth of knowledge and opportunities in the dynamic world of healthcare: Get a Subscription

About Us

Towards Healthcare is a leading global provider of technological solutions, clinical research services, and advanced analytics to the healthcare sector, committed to forming creative connections that result in actionable insights and creative innovations. We are a global strategy consulting firm that assists business leaders in gaining a competitive edge and accelerating growth. We are a provider of technological solutions, clinical research services, and advanced analytics to the healthcare sector, committed to forming creative connections that result in actionable insights and creative innovations.

Browse our Brand-New Journals:

https://www.towardspackaging.com

https://www.precedenceresearch.com

https://www.towardsevsolutions.com/

For Latest Update Follow Us: https://www.linkedin.com/company/towards-healthcare

Get Our Freshly Printed Chronicle: https://www.healthcarewebwire.com

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Cohen & Company Sets Release and Conference Call Date for Third Quarter 2024 Financial Results

PHILADELPHIA and NEW YORK, Oct. 31, 2024 (GLOBE NEWSWIRE) — Cohen & Company Inc. COHN will release its financial results for the third quarter 2024 on Monday, November 4, 2024. The Company will host a conference call at 10:00 a.m. Eastern Time (ET) that day to discuss these results.

The conference call will be available via webcast. Interested parties can access the webcast by clicking the webcast link on the Company’s homepage at www.cohenandcompany.com. Those wishing to listen to the conference call with operator assistance can dial (877) 524-8416 (domestic) or +1 (412) 902-1028 (international). A replay of the call will be available for three days following the call by dialing (877) 660-6853 or (201) 612-7415, with participant passcode 13749865.

About Cohen & Company

Cohen & Company is a financial services company specializing in an expanding range of capital markets and asset management services. Cohen & Company’s operating segments are Capital Markets, Asset Management, and Principal Investing. The Capital Markets segment consists of fixed income sales, trading, and gestation repo financing as well as new issue placements in corporate and securitized products, and advisory services, operating primarily through Cohen & Company’s subsidiaries, J.V.B. Financial Group, LLC in the United States and Cohen & Company Financial (Europe) S.A. in Europe. A division of JVB, Cohen & Company Capital Markets is the Company’s leading boutique investment bank that provides innovative strategic and financial advice in M&A, capital markets, and SPAC advisory. The Asset Management segment manages assets through collateralized debt obligations, managed accounts, and investment funds. As of September 30, 2024, the Company managed approximately $2.4 billion in primarily fixed income assets in a variety of asset classes including US and European trust preferred securities, subordinated debt, and corporate loans. The Principal Investing segment is comprised primarily of investments the Company holds related to its SPAC franchise and other investments the Company has made for the purpose of earning an investment return rather than investments made to support its trading or other capital markets business activity. For more information, please visit www.cohenandcompany.com.

| Contact: | |

| Investors – | Media – |

| Cohen & Company Inc. | Joele Frank, Wilkinson Brimmer Katcher |

| Joseph W. Pooler, Jr. | Joseph Sala or Zach Genirs |

| Executive Vice President and | 212-355-4449 |

| Chief Financial Officer | |

| 215-701-8952 | |

| investorrelations@cohenandcompany.com |

![]()

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Longmont Homeowners Association Wins $6.413 Million Arbitration Award Against Dream Finders Homes for Construction Defects

LONGMONT, Colo., Oct. 31, 2024 /PRNewswire/ — The construction defect law firm Kerrane Storz, P.C. achieved a major win this month for the Parkes at Stonebridge Townhome Owners Association against Dream Finders Homes.

Dream Finders built the 92-unit townhome community known as Parkes at Stonebridge in Longmont, Colorado from 2018 to 2021. Dream Finders promised homeowners “peace of mind” when they sold the homes to Coloradans but failed to deliver on that promise. Soon after moving in, the new homeowners noticed serious construction issues throughout the community including crumbling driveways, heaving sidewalks, and sagging garage awnings.

Depending on the season, sidewalks became dangerous due to ice buildup, ponding water, and slippery algae growth. These conditions caused injury to multiple homeowners who slipped and fell. When homeowners reported their safety concerns, Dream Finders responded with haphazard, negligent repairs that failed to fix the construction problems and caused new hazards.

After multiple failed attempts to negotiate a settlement, the Association proceeded to arbitration against Dream Finders. The Association prevailed on its claims of negligence, breach of contract, breach of express warranty, and breach of implied warranty against Dream Finders. The Arbiter awarded the Association $5,733,471 for its cost of repairs and $679,732 for its litigation costs for a total award of $6,413,204. In addition, the Arbiter awarded the Association post-judgment interest on unpaid amounts until the award plus interest is paid in full.

Dream Finders objected to the award for litigation costs, arguing that the purchase agreements for the townhomes – which their lawyers drafted – prevented the recovery of these costs. The Arbiter disagreed, holding:

“Colorado law clearly provides for an award of costs to the prevailing party in a construction defect arbitration. Any express waiver or limitations on these rights are void as against public policy. Of course, actual damages include costs.”

“We are thrilled with this award for our client and look forward to seeing the community make much-needed repairs,” said Heidi Storz, lead attorney for the community. “This decision will serve other Colorado homeowners by putting developer/builders on notice that they will be held accountable for poor construction despite boilerplate, take-it-or-leave-it waivers they may include in purchase agreements.”

Dream Finders has paid part of the arbitration award. As of today’s date, however, Dream Finders has not satisfied its obligation to pay the post-judgment interest awarded to the Association by the Arbiter. On October 30, 2024, the Association filed a motion in Boulder County District Court seeking entry of judgment on the arbitration award. The Association plans to enforce the judgment as necessary to hold Dream Finders accountable for all they owe.

As of June 2024, Dream Finders Homes had built and sold almost 2,000 homes across the Front Range. Dream Finders Homes is now selling homes in newly built communities in Arvada, Aurora, Brighton, Broomfield, Littleton, Parker, Strasburg, Berthoud, Fort Collins, and Longmont.

The law firm of Kerrane Storz, P.C. represents Colorado and Texas homeowners and community associations in construction defect matters.

Contact:

Heidi Storz

hstorz@kerranestorz.com

www.kerranestorz.com

![]() View original content:https://www.prnewswire.com/news-releases/longmont-homeowners-association-wins-6-413-million-arbitration-award-against-dream-finders-homes-for-construction-defects-302293452.html

View original content:https://www.prnewswire.com/news-releases/longmont-homeowners-association-wins-6-413-million-arbitration-award-against-dream-finders-homes-for-construction-defects-302293452.html

SOURCE Kerrane Storz, P.C.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Mortgage Rates Increase for the Fifth Consecutive Week

MCLEAN, Va., Oct. 31, 2024 (GLOBE NEWSWIRE) — Freddie Mac FMCC today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 6.72 percent.

“Increasing for the fifth consecutive week, mortgage rates reached their highest level since the beginning of August,” said Sam Khater, Freddie Mac’s Chief Economist. “With several potential inflection points happening over the next week, including the jobs report, the 2024 election, and the Federal Reserve interest rate decision, we can expect mortgage rates to remain volatile. Although uncertainty will remain, it does appear mortgage rates are cresting, and we do not expect them to reach the highs that we saw earlier this year.”

News Facts

- The 30-year FRM averaged 6.72 percent as of October 31, 2024, up from last week when it averaged 6.54 percent. A year ago at this time, the 30-year FRM averaged 7.76 percent.

- The 15-year FRM averaged 5.99 percent, up from last week when it averaged 5.71 percent. A year ago at this time, the 15-year FRM averaged 7.03 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit. For more information, view our Frequently Asked Questions.

Freddie Mac’s mission is to make home possible for families across the nation. We promote liquidity, stability, affordability and equity in the housing market throughout all economic cycles. Since 1970, we have helped tens of millions of families buy, rent or keep their home. Learn More: Website | Consumers | X | LinkedIn | Facebook | Instagram | YouTube

MEDIA CONTACT:

Angela Waugaman

(703)714-0644

Angela_Waugaman@FreddieMac.com

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/99b1a671-9ac3-4dff-b69e-b6cf87bdb78f

![]()

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Fed Interest Rate Cuts Expected, But Economists Warn Of 'Bumpy Course In This Last Mile' To Curb Inflation

A 0.25% interest rate cut at the Federal Reserve’s Nov. 7 meeting, just two days after the U.S. presidential election, is almost fully priced in by markets, with another similar cut likely in December as cooling inflation allows the Fed to gradually ease its policy stance.

The latest inflation data from September, as measured by the Personal Consumption Expenditure (PCE) price index, showed a deceleration that aligns with the Fed’s 2% target, giving policymakers a green light to consider further easing.

The annual PCE inflation rate cooled to 2.1% in September, down from 2.3% in August, broadly matching analyst expectations.

Economists have largely welcomed the Fed’s most-watched inflation report, but with some caveats as consumer prices, especially in services, remain somewhat sticky.

Fed Nears Inflation Target, But Core Pressures Signal Caution

“The Fed’s inflation target is now essentially at 2%,” Joseph Brusuelas RSM US LLP principal & chief economist, commented on the data.

Extended to three decimal points, the PCE stands at 2.095%, with a month-over-month increase of 0.175%. Inflation is rising at a 1.4% rate on a three-month basis and 1.9% over six months, the expert explained.

“The Fed has re-established price stability,” Brusuelas added.

According to Jeffrey Roach, chief economist at LPL Financial, the slowdown in core services prices, excluding housing, could keep the Fed on track for two rate cuts by the end of the year.

Yet, Roach also warned investors of potential “head fakes” in inflation data, as the path to sustained 2% inflation is expected to be long and difficult.

Bill Adams, chief economist at Comerica Bank, echoed a similar sentiment, stating that while headline inflation has slowed close to the Fed’s target, the persistence of higher core inflation could still affect the central bank’s approach.

“The Fed will likely cut by a quarter percent at their post-election decision,” Adams said, though he added that the Fed must remain vigilant as core pressures are far from fully subdued.

However, some Fed watchers are more cautious about declaring victory just yet. Core PCE inflation, which excludes food and energy, came in at 2.7% year-over-year, holding steady from August and surpassing estimates of 2.6%.

Mohamed El Erian, Allianz adviser and president at Queen’s College, commented “I suspect that, on the whole, this is not what the Federal Reserve expected data-wise when it suddenly decided last month to increase the pace of interest rate reductions from 25 basis points to 50 bps.”

El Erian added that the distribution of the price increases “will also capture the Fed’s attention.” Moreover, the robust 0.4% increase in real consumer spending, which suggests consumer demand is still resilient, is seen as a factor that could complicate the Fed’s efforts to maintain control over inflation.

Yet, he welcomed the reading in the Employment Cost Index (ECI) for the third quarter, which rose by 0.8%, the smallest gain since mid-2021.

Quincy Krosby, chief global strategist at LPL Financial, highlighted that the year-over-year core PCE print, which came in at 2.7%, indicates that inflation isn’t entirely under control.

“The Fed is still on a bumpy course in this last mile to quell inflation and declare victory,” Krosby said, emphasizing that the central bank’s journey to stable 2% inflation may face additional hurdles.

“The Fed will need to acknowledge that with still resilient consumer spending, higher wages from a series of successful strikes, and a solid labor market, they will need to adopt the gradual approach towards lowering rates,” Krosby added.

Read now:

Image created using artificial intelligence via Midjourney.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Jobs Report Preview: Could October Nonfarm Payrolls Defy Hurricane Disruptions, Strikes And Election Uncertainty?

Traders are eagerly awaiting October’s official jobs data, set for release on Friday at 8:30 a.m. ET — widely viewed as the week’s most crucial economic event.

The Employment Situation report is expected to provide valuable insights into the resilience of the U.S. labor market, especially in light of recent disruptions from hurricanes, strikes and uncertainties surrounding the imminent U.S. elections.

What are economists forecasting, and how have markets responded to recent jobs reports?

See Also: US Economy Grows Less Than Expected In Q3, Yet Private Employment Soars By 233,000 In October

October Jobs Report: What Do Economists Expect?

The consensus among Wall Street economists is forecasting a sharp deceleration in the pace of employment growth in October.

Nonfarm payrolls are expected to slow down from 254,000 in September to 113,000 in October, an outcome that would represent the lowest monthly employment gain since April, suggesting that U.S. firms have hold back in their hiring plans.

“We expect nonfarm payrolls to rise by 100,000 in October after coming in at 254,000 in September. Although this is below consensus, we’d still view it as a solid print, since we estimate that Hurricane Milton and the Boeing strike temporarily lowered payrolls in October,” Bank of America economist Shruti Mishra stated.

According to Bank of America, Hurricane Milton’s landfall in Florida on Oct. 9, which coincided with the jobs survey week, likely weighed on payroll figures, particularly in sectors like leisure and hospitality. Additionally, lingering effects from Hurricane Helene, which struck in late September, may have added a slight drag on employment.

Bank of America analysts also noted that the Bureau of Labor Statistics estimates a 41,000 increase in striking workers from September to October, largely driven by the Boeing Co. BA strike. Taken together, these factors could have reduced October payrolls by at least 50,000 jobs.

On the positive side, government payrolls may see a 25,000 boost due to temporary hiring for election-related roles.

Looking at other indicators in the October jobs report, the unemployment rate is expected to hold steady at 4.1%, suggesting that the pace of job losses has also not advanced.

Wages are broadly expected to hold their recent trend, as average hourly earnings are expected to surge 0.3% month-over-month, down from 0.4% in September, and by 4.1% year-over-year as seen in the previous month.

Recent Data Shows Potential For Positive Employment Surprises

Earlier this week, the ADP National Employment report showed that private payrolls surged by 233,000 in October, sharply accelerating from 143,000 in September and well above economist expectations of 115,000, as tracked by TradingEconomics.

Nearly the whole increase in private employment came from services, with education, health services, trade, transportation, utilities and leisure and hospitality being the most active in the monthly increases.

The ADP data — which uses anonymized payroll data of more than 25 million U.S. employees – offered encouraging insights ahead of Friday’s official jobs report, suggesting the U.S. economy likely maintained robust job growth throughout the month.

“Even amid hurricane recovery, job growth was strong in October. As we round out the year, hiring in the U.S. is proving to be robust and broadly resilient,” said Nela Richardson, chief economist at ADP.

Stock Reactions To Recent Jobs Reports

The last three jobs reports have highlighted how market sentiment shifts depending on whether employment numbers come in hotter or cooler than expected.

In the July jobs report, released on Aug. 2, the U.S. economy added 114,000 jobs, later revised up to 144,000 — significantly below the consensus estimate of 175,000. On that day, the S&P 500, tracked by the SPDR S&P 500 ETF Trust SPY, dropped 1.9% as investors grew concerned about potential economic slowdown.

Another cooler-than-expected report arrived with the August jobs data, published on Sep. 6. The U.S. added 142,000 jobs in August, missing forecasts of 160,000. The S&P 500 responded with a 1.7% decline, reflecting ongoing worries about weakening labor market momentum.

In contrast, the September jobs report, released on Oct. 4, showed the U.S. economy added a robust 254,000 jobs, well above the revised 159,000 in August and far exceeding expectations of 140,000. This marked the strongest job growth in six months, significantly above the prior 12-month average of 203,000.

The S&P 500 responded positively, rallying 0.9% on the day as investors saw this as a sign of resilience in the labor market.

Read Next:

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Stocks Tumble, Nasdaq 100 Selloffs As Tech Giants Disappoint, Crypto Companies Plummet: What's Driving Markets Thursday?

Risk aversion swept across markets on Thursday as investor disappointment over third-quarter tech earnings triggered the steepest drop in major U.S. indices in nearly two months.

Microsoft Corp. MSFT plummeted over 5% by midday trading in New York, on track for its worst session in two years. Although the company surpassed earnings estimates, it forecasted slower growth in its Azure cloud business, dampening future revenue expectations.

Meta Platforms Inc. META also declined by over 4% despite a strong quarterly performance, as the social media giant projected “significant” capital expenditure growth next year, particularly for AI infrastructure.

The elite “Magnificent Seven” tech group shed nearly $500 billion in market capitalization within a single day after reaching a record high of $16.8 trillion. Apple Inc. AAPL and Amazon.com Inc. AMZN are set to report earnings after the market close.

In economic news, inflation sent mixed signals for September. The Personal Consumption Expenditures (PCE) price index slowed as expected to 2.1% annually, while the Fed’s preferred inflation measure, the core PCE price index, remained at 2.7% year over year, slightly above the expected 2.6%.

The S&P 500 dropped 1.4%, and the tech-heavy Nasdaq 100 slid 2.2%, both tracking their worst session since Sept. 6. The CBOE Volatility Index (VIX) surged 12%.

Risk aversion also weighed on commodities, with gold prices dropping 1.7%, marking their worst day since July, and silver plunging 3% after a 2% decline on Wednesday.

Bitcoin BTC/USD slid 2.4%, and crypto-related stocks suffered significant losses. Coinbase Global Inc. COIN tumbled over 10% on disappointing earnings, eyeing its worst day since May.

Thursday’s Performance In Major US Indices, ETFs

| Major Indices | Price | 1-day %chg |

| Dow Jones | 41,832.30 | -0.7% |

| Russell 2000 | 2,213.10 | -0.9% |

| S&P 500 | 5,729.43 | -1.4% |

| Nasdaq 100 | 19,943.07 | -2.2% |

According to Benzinga Pro data:

- The SPDR S&P 500 ETF Trust SPY fell 1.5% to $571.51.

- The SPDR Dow Jones Industrial Average DIA fell 0.8% to $418.60.

- The tech-heavy Invesco QQQ Trust Series QQQ tumbled 2.2% to $485.78.

- The iShares Russell 2000 ETF IWM fell 0.7% to $219.65.

- The Utilities Select Sector SPDR Fund XLU outperformed, rising 1.4%. The Technology Select Sector SPDR Fund XLK lagged, down 2.4%.

Thursday’s Stock Movers

Stocks reacting to corporate earnings were:

- Booking Holdings Inc. BKNG, up over 5%,

- Amgen Inc. AMGN, up 1.7%,

- Starbucks Corp. SBUX, down 0.6%,

- eBay Inc. EBAY, down over 8%,

- MicroStrategy Inc. MSTR, up 1.9%,

- Carvana Co. CVNA, up 24%,

- Mastercard Inc. MA, down 1.8%,

- Merck & Company Inc. MRK, down 2.8%,

- Linde plc LIN, down 2.9%,

- Comcast Corp. CMCSA, up 2.9%,

- Uber Technologies Inc. UBER, down over 11%,

- Eaton Corp. plc ETN, down 5%,

- ConocoPhillips COP, up 6%,

- Bristo-Myers Squibb Co. BMY, up 3.3%,

- Southern Company SO, up 2.2%,

- Altria Group Inc. MO, up 7.6%,

- Regeneron Pharmaceuticals Inc. REGN, down 9%,

- The Cigna Group CI, up 3%,

- Norwegian Cruise Line Holdings Ltd. NCLH, up over 9%.

- Cheniere Energy Inc. LNG, up over 5%.

Large-cap companies slated to report their earnings after the close include Apple Inc, Amazon.com Inc, Intel Corp. INTC, Atlassian Corp. TEAM and Coterra Energy Inc. CTRA.

Read Next:

Image created using artificial intelligence via Midjourney.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

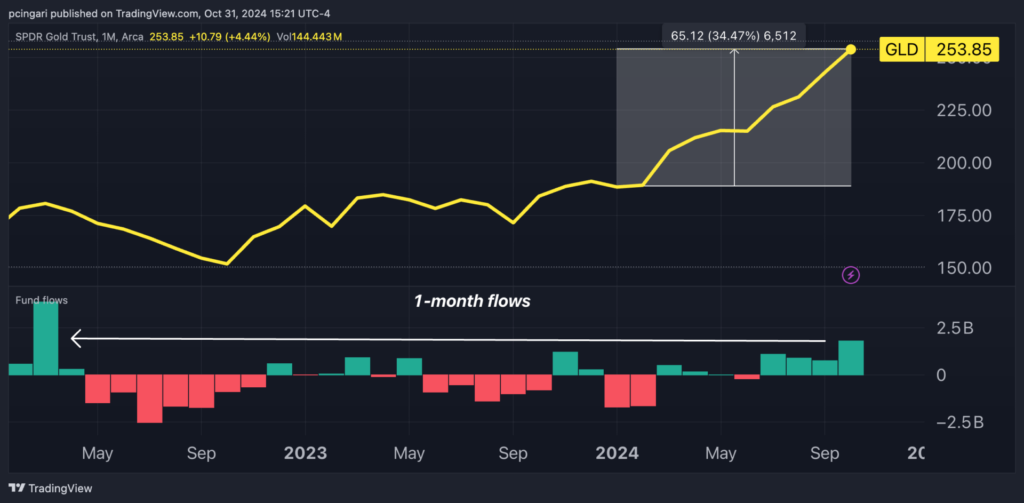

Biggest Gold ETF Posts Highest Monthly Inflows In 2.5 Years As Investors Rush To Safe Haven Ahead Of Presidential Election

The SPDR Gold Trust GLD, the largest physically backed gold ETF, saw a significant influx of capital this month as economic and policy uncertainties surrounding the upcoming U.S. presidential election drive investors toward safe-haven assets.

GLD’s assets under management reached $79.7 billion as of Oct. 30, bolstered by $1.8 billion in net inflows for October — the fund’s strongest monthly inflow since March 2022, data from TradingView shows.

Additionally, the ETF notched its fourth consecutive month of gains and its eleventh positive month out of the last 13, with a remarkable 50% rally from the lows of October 2023.

Gold Demand Surges As ETF Investments Soar

Global demand for gold surged 5% year-over-year in the third quarter of 2024, reaching 1,313 tonnes, a record level for the third quarter, according to a report from the World Gold Council released this week.

This increase reflects a rising appetite for the precious metal as macroeconomic concerns and market uncertainty drive both institutional and retail investors toward gold-backed assets.

Gold prices touched new record highs throughout the quarter as demand continued to build.

A key factor behind this growth was a resurgence in gold ETF investment, with global gold ETF inflows reaching 95 tonnes in the third quarter, the first quarter of positive inflows since the first quarter of 2022.

This marked a sharp year-over-year turnaround from the third quarter of 2023, when ETFs saw outflows of 139 tonnes.

“Gold is continuing its relentless rally and may even have the $3,000 level in its sights before too long,” said Michael Gayed, CFA.

The pace of central bank buying slowed to 186 tonnes in the third quarter, yet year-to-date purchases remain on track with 2022 levels, the World Gold Council wrote.

Central banks, particularly in emerging market economies, continue to diversify away from the U.S. dollar, reflecting a strong and steady institutional demand for gold as a reserve asset.

Fiscal, Geopolitical Uncertainty Sparks Investor Rush to Gold

Gold prices have surged 33% in 2024, positioning the commodity for its third-strongest year in the last 50. Notably, this rally has defied traditional drivers like falling Treasury yields or a weakening dollar that typically boost gold.

Instead, two primary factors are fueling investor demand for the safe-haven asset.

The first driver is concern over the U.S. government’s fiscal policies, which some fear could trigger renewed inflationary pressures.

“Gold is rising as the market begins to price in the likelihood of a Fed forced to cut rates further, despite persistent inflation,” said Otavio Costa, macro strategist at Crescat Capital.

Bank of America analysts agree, noting that regardless of the outcome of the upcoming presidential election, both political parties seem reluctant to tackle the precarious budget deficit and soaring national debt.

“Gold may be the last perceived safe haven asset standing,” wrote Bank of America commodity analyst Michael Widmer, emphasizing the risks posed by unchecked government spending.

A second key factor is the evolving role of gold as “a hedge against U.S. economic sanctions.”

Veteran Wall Street investor Ed Yardeni recently described gold as an asset that can protect nations from Western financial controls.

After Russia invaded Ukraine in February 2022, the U.S. and its allies froze Russia’s foreign exchange reserves held abroad. Since then, there have been proposals to seize nearly $300 billion of these assets to support Ukraine’s defense and reconstruction — a move that has sent a clear signal to other nations.

“China and other countries have been increasing their allocations of gold in their countries’ international reserves,” Yardeni added, suggesting that gold is becoming a preferred reserve asset for nations looking to insulate themselves from potential U.S.-led sanctions.

By holding more gold, countries can reduce their dependence on assets vulnerable to Western financial controls, diversifying away from the U.S. dollar.

Read Next:

Photo via Shutterstock.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

VIX Index Notches Third-Strongest October Spike In An Election Year, S&P 500 Snaps 5-Month Winning Streak: Why Volatility 'Is Unlikely To Pull Back,' Analyst Says

The CBOE Volatility Index (VIX), often referred to as the market’s “fear gauge,” saw a sharp 34% increase in October, signaling intensified investor concern as the U.S. presidential election looms.

This spike marks the third-strongest October VIX increase for an election year, with only 2008 and 2020 witnessing larger jumps.

Excluding the extraordinary 52% spike in October 2008, driven by the financial crisis, and the 44% rise in October 2020 amid the COVID-19 pandemic, October 2024’s surge marks the highest volatility for an election-year October since the VIX’s index inception in 1990.

| Election Year | CBOE VIX (% change) | VIX Level (Close on 31/10) |

|---|---|---|

| October 1992 | 13.1 | 16.15 |

| October 1996 | 6.8 | 18.11 |

| October 2000 | 14.9 | 23.63 |

| October 2004 | 22.0 | 16.27 |

| October 2008 | 52.0 | 59.89 |

| October 2012 | 18.2 | 18.6 |

| October 2016 | 28.4 | 17.6 |

| October 2020 | 44.2 | 38.02 |

| October 2024 | 34.1 | 22.43 |

Political uncertainty is a significant driver of this volatility, with Vice President Kamala Harris and former President Donald Trump neck-and-neck in polling data, though Trump holds a substantial lead in betting markets.

Market-implied odds from CFTC-regulated platform Kalshi currently give Trump a 57% chance of re-election.

Concerns over the candidates’ fiscal policies and the country’s ballooning national debt levels are adding to market tension, as neither candidate has outlined a plan to tackle the fiscal risk.

S&P 500 Ends Five-Month Rally

Alongside political anxiety, disappointing earnings from major tech companies fueled a late-month selloff.

The S&P 500, as measured by the SPDR S&P 500 ETF Trust SPY, fell in October, snapping a five-month winning streak. Microsoft Corp. MSFT led the decline, dropping 6% on Thursday — its worst single-day performance in over two years — as guidance over 2025 revenue disappointed earnings.

Quincy Krosby, chief global strategist at LPL Financial, highlighted that mega-cap tech’s forward guidance disappointed markets, particularly around AI spending and the slower-than-expected integration of AI into Microsoft’s cloud services. “The market overall has been disappointed with mega tech guidance,” she said, highlighting the potential impact on market sentiment as the election draws near.

Analysts Warn of Further Volatility

Many analysts see no immediate end to the current bout of market anxiety.

Michael Gayed, CFA, commented, “I think the markets could be a little more prepared for a Trump win this time around, but I wouldn’t be surprised to see the VIX start to pick up again.”

David Morrison, senior market analyst at Trade Nation, echoed this sentiment, warning that “volatility remains elevated and is unlikely to pull back until there’s certainty over the result of next week’s Presidential Election.”

Morrison added that a decisive election outcome could alleviate some market fears, but with polling data as tight as it is, uncertainty is likely to persist.

Now Read:

Image:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Progress Completes Acquisition of ShareFile

ShareFile’s AI-powered, document-centric collaboration platform expands Progress’ industry-leading product portfolio and marks a major milestone in the company’s Total Growth Strategy

BURLINGTON, Mass., Oct. 31, 2024 (GLOBE NEWSWIRE) — Progress PRGS, the trusted provider of AI-powered infrastructure software, today announced the completion of the acquisition of ShareFile, a business unit of Cloud Software Group, Inc., providing a SaaS-native, AI-powered, document-centric collaboration platform, focusing on industry segments including business and professional services, financial services, industrial and healthcare.

“This acquisition marks the latest major milestone in Progress’ Total Growth Strategy, which is built on three pillars: Invest and Innovate, Acquire and Integrate and Drive Customer Success. The addition of ShareFile significantly enhances our product capabilities, benefiting our customers and meaningfully expanding the customer base we serve,” said Yogesh Gupta, CEO of Progress. “We are thrilled to welcome ShareFile customers and employees to the Progress community and look forward to a bright future with ShareFile now part of Progress.”

Progress products help organizations to develop, deploy and manage responsible AI-powered applications and experiences. ShareFile fits strategically with Progress’ Digital Experience portfolio to enable customers to deliver more efficient and effective client and team collaboration, while simplifying the sharing of documents and prioritizing security.

As previously announced, Progress acquired ShareFile for a purchase price of $875 million, funded with a combination of cash and Progress’ existing revolving credit facility. ShareFile is expected to add more than $240M in annual revenue and more than 86,000 customers to Progress.

About Progress

Progress PRGS empowers organizations to achieve transformational success in the face of disruptive change. Our software enables our customers to develop, deploy and manage responsible AI-powered applications and experiences with agility and ease. Customers get a trusted provider in Progress, with the products, expertise and vision they need to succeed. Over 4 million developers and technologists at hundreds of thousands of enterprises depend on Progress. Learn more at www.progress.com.

Note Regarding Forward-Looking Statements

This press release contains statements that are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Progress has identified some of these forward-looking statements with words like “believe,” “may,” “could,” “would,” “might,” “should,” “expect,” “intend,” “plan,” “target,” “anticipate” and “continue,” the negative of these words, other terms of similar meaning or the use of future dates. Risks, uncertainties and other important factors that could cause actual results to differ from those expressed or implied in the forward-looking statements include: uncertainties as to the effects of disruption from the acquisition of ShareFile (i.e., making it more difficult to maintain relationships with employees, licensees, other business partners or governmental entities); other business effects, including the effects of industry, economic or political conditions outside of Progress’ or ShareFile’s control; transaction costs; actual or contingent liabilities; uncertainties as to whether anticipated synergies will be realized; and uncertainties as to whether ShareFile’s business will be successfully integrated with Progress’ business. For further information regarding risks and uncertainties associated with Progress’ business, please refer to Progress’ filings with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the fiscal year ended November 30, 2023. Progress undertakes no obligation to update any forward-looking statements, which speak only as of the date of this press release.

| Press Inquiries: Erica McShane VP, Corporate Communications Progress Software +1 781-280-4000 pr@progress.com |

Investor Relations: Mike Micciche SVP, Investor Relations Progress Software +1 781-280-4000 Investor-relations@progress.com |

![]()

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.