Want Safe Dividend Income in 2024 and Beyond? Invest in the Following 3 Ultra-High-Yield Stocks.

Finding stocks with healthy dividend yields isn’t too tough of a task. Finding above-average yields based on dividends that will be sustained into the foreseeable future, however, is a different story. Sometimes yields are only high because investors are dumping a stock, sensing bad news is on the horizon.

With that in mind, here’s a closer look at three ultra-high-yield stocks paying dividends that are indeed well protected, and should remain so for a long while.

1. British American Tobacco

You likely recognize that the worldwide smoking-cessation movement is still gaining traction, posing a threat to British American Tobacco (NYSE: BTI). Although the parent to cigarette brands Pall Mall, Camel, and Lucky Strike is also developing vaping and heated-tobacco businesses, smoking remains its breadwinner, accounting for more than 80% of its top line.

Except, smoking isn’t anywhere as close to its end as you might think.

Although smoking prevalence is down from 33% of the global population in 2000, the World Health Organization reports there are still roughly 1.3 billion regular smokers on the planet today. Population growth has offset much of the effort to encourage quitting. This progress is slowing down, too. The WHO predicts that by 2030, 18% of the world’s population will still be smoking on a regular basis.

That’s not a suggestion to simply ignore the eventual end looming here. British American Tobacco itself says it’s “committed to building a smokeless world” by developing alternatives to smoking tobacco. It’s just that this inevitable end is years down the road, and even though the company’s top line is now shrinking, there’s still plenty of profit left to not only prolong the business’s fruitful life, but continue funding its dividend as well.

That’s a dividend, by the way, that’s steadily grown for years now, loosely in step with modest profit growth that’s apt to persist. Today’s newcomers will be buying it while the stock’s forward-looking yield stands at a hefty 8.4%.

2. Verizon

If you know Verizon Communications (NYSE: VZ) at all (and you most likely do), then you likely recognize how modest its growth prospects are. Its number of landline phones is shrinking, and Pew Research reports that 97% of adults living in the United States also already own a mobile phone. At best, Verizon can only hope to poach a few competitors’ mobile subscribers without losing any of its own paying customers in the meantime.

What this telecom company lacks in growth potential, however, it more than makes up for in a consistent profitability that supports its equally reliable dividend.

Fact: People are fiercely addicted to their cellphones. Owners are staring at them on the order of four hours per day, checking them several dozen times even without a chime or vibration, according to a survey by Reviews.org. Indeed, most mobile phone owners report feeling anxious without their phone, while some indicate feeling a sense of panic when their device’s battery is nearly depleted.

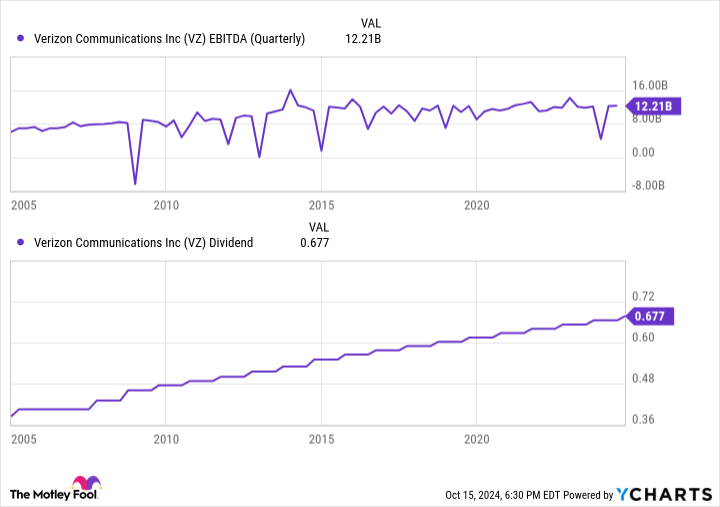

Looking past the mental health concerns raised by the data, it’s clear that consumers aren’t willing — or even able — to let go of their phones now. They’ll pay to remain connected. Verizon just needs to offer them a competitive price. Given its market-leading scale, that’s typically not a problem for Verizon. The company has reported positive earnings before interest, taxes, depreciation, and amortization (EBITDA) every quarter for well over a decade.

More relevant to income-minded investors, Verizon has not only paid a quarterly dividend like clockwork since the company was formed as consumers know it back in 2000, but has also raised its annual dividend payment every year since 2005. You can plug into this reliable growth while the stock’s forward-looking dividend yield is a solid 6.3%.

3. Ambev

Last but certainly not least, add Ambev S.A. (NYSE: ABEV) to your list of ultra-high-yield dividend stocks to buy while its forward-looking yield stands at just under 6.5%.

Ambev is the combination of a handful of beer companies, with the most noteworthy of these combinations being 2004’s merger with Belgium’s Interbrew, followed by 2008’s acquisition of Anheuser-Busch. You’re of course familiar with Anheuser-Busch’s Budweiser, Michelob, and Busch brands. Ambev owns a far greater number of less familiar craft brands, however, some of which you can only find overseas. In fact, the bulk of the company’s revenue actually comes from Latin America.

That hasn’t exactly mattered a whole lot of late. Although beer consumption is holding up better outside of the United States than it is within it, it’s not exactly seeing robust growth anywhere. Inflation is taking its toll on consumers, crimping demand. In this vein, Ambev’s total volume of beer sold through the first half of this year is barely better than even with last year’s comps.

The message being delivered by the data, however, looks past a couple of key points about the business.

The first of these is simply that true beer fans remain willing to pay a premium for the higher-end beers that Ambev S.A. offers. Industry research house GlobalData notes sales of premium beers are outpacing non-premium beer sales, and are likely to continue doing so for the foreseeable future. This theme jibes with Ambev’s recent revenue growth outpacing its volume growth.

And the second noteworthy detail to consider? Beer is somewhat cyclical anyway. It’s a bit out of favor now, ceding to growing interest in wine and spirits. But give it time. Consumers have a way of coming back around, perpetually searching for something different.

Ambev’s dividend payments are anything but consistent, for the record — the result of an overseas company doing so much foreign business of its own. So, plan accordingly. With its strong yield and track record of long-term growth though, the erratic payouts are worth it.

Should you invest $1,000 in British American Tobacco right now?

Before you buy stock in British American Tobacco, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and British American Tobacco wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $839,122!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 14, 2024

James Brumley has no position in any of the stocks mentioned. The Motley Fool recommends British American Tobacco P.l.c. and Verizon Communications and recommends the following options: long January 2026 $40 calls on British American Tobacco and short January 2026 $40 puts on British American Tobacco. The Motley Fool has a disclosure policy.

Want Safe Dividend Income in 2024 and Beyond? Invest in the Following 3 Ultra-High-Yield Stocks. was originally published by The Motley Fool

Leave a Reply