INVESTOR DEADLINE NEXT WEEK: Robbins Geller Rudman & Dowd LLP Announces that CVS Health Corporation Investors with Substantial Losses Have Opportunity to Lead Class Action Lawsuit

SAN DIEGO, Sept. 03, 2024 (GLOBE NEWSWIRE) — Robbins Geller Rudman & Dowd LLP announces that purchasers or acquirers of CVS Health Corporation CVS securities between May 3, 2023 and April 30, 2024, inclusive (the “Class Period”), have until Tuesday, September 10, 2024 to seek appointment as lead plaintiff of the CVS class action lawsuit. Captioned Nixon v. CVS Health Corporation, No. 24-cv-05303 (S.D.N.Y.), the CVS class action lawsuit charges CVS and certain of CVS’s top current and former executives with violations of the Securities Exchange Act of 1934.

If you suffered substantial losses and wish to serve as lead plaintiff of the CVS class action lawsuit, please provide your information here:

https://www.rgrdlaw.com/cases-cvs-health-corporation-class-acton-lawsuit-cvs.html

You can also contact attorneys J.C. Sanchez or Jennifer N. Caringal of Robbins Geller by calling 800/449-4900 or via e-mail at info@rgrdlaw.com.

CASE ALLEGATIONS: CVS is a healthcare company.

The CVS class action lawsuit alleges that defendants throughout the Class Period made false and/or misleading statements and/or failed to disclose that: (i) the forecasts CVS used to determine plan premiums were ineffective at accounting for medical cost trends and health care utilization patterns; (ii) as a result, CVS was likely to incur significant expenses to cover cost increases that were not accounted for in CVS’s forecasts and thus not covered by plan premiums; (iii) accordingly, CVS had overstated the profitability of its Health Care Benefits segment; and (iv) contrary to defendants’ assurances, the revenues generated from CVS’s other primary segments were insufficient to offset the negative financial impact of the increasing expenditures within the Health Care Benefits segment.

The CVS class action lawsuit further alleges that on August 2, 2023, CVS revealed that it was revising its diluted earnings-per-share (“EPS”) guidance range to $6.53 to $6.75 from $6.90 to $7.12 and that operating income “decreased $1.4 billion, or 30.7%, in the three months ended June 30, 2023 compared to the prior year primarily due to declines in the Health Care Benefits segment.” On this news, the price of CVS stock fell, according to the complaint.

The complaint further alleges that on February 7, 2024, CVS revealed that it was revising its diluted EPS guidance range to at least $7.06 from at least $7.26, its adjusted EPS guidance range to at least $8.30 from at least $8.50, and its cash flow from operations guidance to at least $12.0 billion from at least $12.5 billion. On this news, the price of CVS stock fell, according to the complaint.

Finally, on May 1, 2024, the CVS class action lawsuit alleges that CVS reported $88.4 billion in revenue, missing expectations of $89 billion, stating that higher utilization of healthcare services, meaning more insurance dollars spent, weighed on its results in addition to Medicare reimbursement rate cuts that will continue to pressure CVS for the remainder of the year. On this news, the price of CVS stock fell nearly 17%, according to the complaint.

ABOUT ROBBINS GELLER: Robbins Geller Rudman & Dowd LLP is one of the world’s leading complex class action firms representing plaintiffs in securities fraud cases. Over the last decade, our Firm has been ranked #1 on the ISS Securities Class Action Services law firm rankings for six out of the last ten years for securing the most monetary relief for investors. In the last four years, Robbins Geller recovered $6.6 billion for investors in securities-related class action cases – over $2.2 billion more than any other law firm during that time. With 200 lawyers in 10 offices, Robbins Geller is one of the largest plaintiffs’ firms in the world and the Firm’s attorneys have obtained many of the largest securities class action recoveries in history, including the largest securities class action recovery ever – $7.2 billion – in In re Enron Corp. Sec. Litig. Please visit the following page for more information:

https://www.rgrdlaw.com/services-litigation-securities-fraud.html

Attorney advertising.

Past results do not guarantee future outcomes.

Services may be performed by attorneys in any of our offices.

Contact:

Robbins Geller Rudman & Dowd LLP

J.C. Sanchez, Jennifer N. Caringal

655 W. Broadway, Suite 1900, San Diego, CA 92101

800-449-4900

info@rgrdlaw.com

![]()

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Prediction: Alphabet Will Be the Robotaxi Leader, Not Tesla

The robotaxi wars are heating up. After an initial delay, Tesla (NASDAQ: TSLA) has a planned robotaxi event in October, while General Motors‘ (NYSE: GM) Cruise recently struck a deal with Uber to offer autonomous vehicles on the ride-sharing company’s platform next year.

However, there is currently one company ahead of the pack and that is Waymo, owned by Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL). Let’s take a look at why I think Alphabet will be the robotaxi leader moving forward.

First-mover advantage

At this point, Waymo is way ahead of the pack, with customers actually using its robotaxi services. The company recently announced that it is providing 100,000 paid robotaxi trips a week, which is about 100,000 more than Tesla and Cruise combined are currently offering.

This is double the number of trips Waymo was providing in May. Currently, the company is operating in four U.S. cities: San Francisco, Phoenix, Austin, and Los Angeles. It plans to expand into other cities within the corresponding states. At present, only California, Texas, and Arizona permit autonomous-taxi services.

Waymo also recently unveiled its sixth-generation, self-driving technology, which will look to reduce the costs of the vehicles. The new technology will lower the number of cameras around the vehicles from 29 to 13 and the number of lidar sensors from five to four. Waymo is currently testing the new-generation technology on public roads with professional drivers on board. In addition to cost savings, the new technology has also been designed to handle more weather conditions.

With Waymo the only robotaxi service currently operating in the U.S., the company has a nice first-mover advantage. Customers are already using its fleet without major incident, which will only build confidence in its offering as it expands. Meanwhile, driving down costs with its vehicles is also important, as this will make the economics for the service better.

Earlier this year, Alphabet announced that it would invest another $5 billion into Waymo to help the company continue to ramp up its business.

Tesla has history of overpromising and underdelivering

While Tesla has a big robotaxi event planned for October, thus far, the company has not delivered any paid rides to customers. And yet, for years Tesla has been telling everyone it would turn customer vehicles into fully autonomous cars with a software update.

In 2016, the company famously wrote a blog post that all its cars were now produced with self-driving hardware. However, seven years have passed, and none of Tesla’s driving systems are fully autonomous; they all need to be supervised with a driver. Meanwhile, the older hardware has needed upgrading to run its latest “Full Self-Driving” (FSD) service at the cost of the customer, which has led to lawsuits.

And in December 2023, Tesla had to recall more than 2 million vehicles to install new Autopilot safeguards. However, the National Highway Traffic Safety Administration (NHTSA) had to investigate the recall after 20 reported crashes followed the installation of the updated software. Over the last few years, there have been about 1,000 auto accidents reported involving Tesla’s Auto Pilot system.

Critics of Tesla’s robotaxi efforts abound. In July, Rolling Stone questioned if Tesla even has the technology to build a robotaxi, citing a number of critics of the company. The publication followed that up in August with a test drive using the company’s self-driving technology. The author of the Rolling Stone article said they did not feel safe and that the technology almost caused an accident.

Rolling Stone, though, isn’t the only news source to question Tesla’s autonomous-driving technology; InsideEVs reported that in a test drive, bad weather compromised the vehicle’s FSD system. It noted that the car dangerously stopped in the middle of a highway to let a car pass, and also tried to turn off the road and into a furniture store. It said that a lack of supplemental radar and lidar could be to blame.

While Tesla bulls, like Ark Investment, will parrot that Tesla is training its autonomous vehicles with more data and thus will give it an advantage, so far its real-world applications appear to be falling short.

Cruise has had past issues

GM’s Cruise unit, meanwhile, has had its own issues. One of its robotaxis was involved in an incident in which the vehicle dragged a pedestrian after the person was hit by another vehicle. California subsequently suspended its license last October, and Cruise then decided to pause all operations.

The incident led to a number of key leaders at the unit being dismissed. Meanwhile, Cruise has been bleeding money since GM acquired it in 2016.

While the deal with Uber is a good step, this safety issue does leave a bit of a cloud over the company. It is currently authorized to operate in three cities: Dallas, Houston, and Phoenix.

Time to buy Alphabet stock

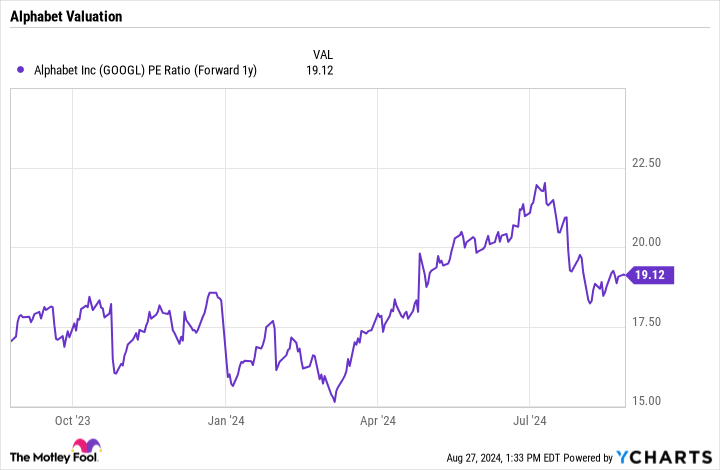

With Alphabet trading at a forward price-to-earnings (P/E) ratio of 19 next year’s analyst estimates, the stock looks cheap.

GOOGL PE Ratio (Forward 1y) data by YCharts.

At this point, given Alphabet’s valuation, investors are basically getting a free call option on Waymo. If it becomes a big success, investors will win, but if it fails, it really won’t hurt them. That is a big difference compared to Tesla, where a lot of the bullish thesis around the stock centers around its future robotaxi business as electric vehicle (EV) growth slows.

Should you invest $1,000 in Alphabet right now?

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $731,449!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 26, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Geoffrey Seiler has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Tesla, and Uber Technologies. The Motley Fool recommends General Motors. The Motley Fool has a disclosure policy.

Prediction: Alphabet Will Be the Robotaxi Leader, Not Tesla was originally published by The Motley Fool

Intel CEO's cost-cutting pitch to include Altera spin-out and retreat from German plant, source says

(Reuters) — Intel (INTC) CEO Pat Gelsinger and key executives are expected to present a plan later this month to the company’s board of directors to slice off unnecessary businesses and revamp capital spending, according to a source familiar with the matter, as they try to revive the once-dominant chipmaker’s fortunes.

The plan will include ideas on how to shave overall costs by selling businesses, including its programmable chip unit Altera, that Intel can no longer afford to fund from the company’s once-sizeable profit.

Gelsinger and other high-ranking executives at Intel are expected to present the plan at a mid-September board meeting, the same source said.

Details of Gelsinger’s proposal is reported here for the first time.

Intel declined to comment.

The proposal does not yet include plans to split Intel and sell off its contract manufacturing operation, or foundry, to a buyer such as Taiwan Semiconductor Manufacturing Co. (TSM, 2330.TW), according to the source and another person familiar with the matter.

The presentation, including the plans around its manufacturing operations, are not yet finalized and could change ahead of the meeting.

Intel has already broken off its foundry business from its design business, and has been reporting its financial results separately since the first calendar quarter of this year.

The company has erected a wall between the design and manufacturing businesses to assure that potential customers of the design division would have no access to technology secrets of customers using Intel’s factories, known as fabs, to manufacture their chips.

Intel is suffering through one of its worst periods as it attempts to play catchup in the AI era against the likes of Nvidia (NVDA), the dominant AI chipmaker with a $3 trillion market capitalization. In contrast, Intel’s has now sunk to below $100 billion after a disastrous second-quarter earnings report in August.

The proposal Gelsinger and others will present is likely to include plans to further reduce the company’s capital spending on factory expansion. The pitch may include plans to pause or altogether halt its $32 billion factory in Germany, a project that has reportedly been delayed, the source said.

In August, Intel said it expects to cut capital spending to $21.5 billion in 2025, down 17% from this year, and issued a weaker-than-expected third-quarter forecast.

In addition to the CEO and executive plans, Intel has retained Morgan Stanley and Goldman Sachs to advise the board on what businesses Intel can sell and what it needs to retain, according to two sources with knowledge of the company’s advisory plans.

Intel has not yet asked for bids on the product units, but will likely do so once the board endorses a plan, according to the two sources familiar with the company’s advisory plans.

Altera spin-out

The mid-September board meeting is pivotal for the one-time chipmaking king. Intel reported a disastrous second quarter in August, which included pausing the company’s dividend payments and a 15% staff cut, aimed at saving $10 billion.

Weeks later, chip industry veteran Lip-Bu Tan resigned from the board after months of debate over the company’s future, Reuters reported, creating a vacuum of deep semiconductor business experience on the board.

Last Thursday, after the Reuters report, Gelsinger sought to reassure investors about the company’s weak financial performance.

“It’s been a difficult few weeks,” Gelsinger said at a Deutsche Bank conference. “And we’ve been working hard to address the issues.”

Gelsinger said the company is “taking seriously” what investors have said and that Intel is focused on phase two of the company’s turnaround plan.

Part of those plans will remain unresolved until the mid-September meeting. Then, the company’s directors will likely make crucial decisions about which businesses Intel will keep and which it will shed.

One potential unit the company may look to unload is its programmable chip business, Altera, which Intel acquired for $16.7 billion in 2015. Intel has already taken steps to spin it out as a separate but still wholly owned subsidiary and has said it planned to sell a portion of its stake in an initial public offering in the future, though it has not set a date.

But Altera could also be sold entirely to another chipmaker interested in growing its portfolio, and the company has quietly begun exploring whether a sale would be possible, according to one source familiar with its advisory plans and one of the sources familiar with the plans to cut businesses.

Infrastructure chipmaker Marvell is one potential buyer for such a transaction, according to one of the sources.

Bloomberg earlier reported various options for Intel including a potential split of Intel’s product design and manufacturing businesses that is expected to be discussed at the board meeting.

(Reporting by Max A. Cherney in San Francisco and Milana Vinn in New York; Editing by Kenneth Li, Anirban Sen, Paritosh Bansal, Deepa Babington and Mark Porter)

Cathay Pacific inspects Airbus A350 fleet after engine part failure

By Joanna Plucinska and Tim Hepher

(Reuters) -Hong Kong’s Cathay Pacific Airways said on Monday it had started inspecting all its Airbus A350 jets after the in-flight failure of an engine component, sending shares in British engine supplier Rolls-Royce down sharply.

The carrier said it had cancelled 24 return flights operating until the end of Tuesday, and that a number of aircraft would be out of service for several days while the process, which it described as precautionary, was completed.

An Airbus spokesperson referred questions to the airline and to Rolls-Royce, which said it was aware of the incident and was committed to working closely with Cathay, Airbus and authorities conducting an investigation.

Shares in the company – the sole engine provider for the Airbus A350 family of long-haul jets – closed down more than 6% and dragged Europe’s defence and aerospace index down 2.8%

According to Flightradar24 data, the problem apparently unfolded several minutes after take-off as flight CX383 initially headed out over the sea, south of Hong Kong.

Instead of immediately turning north for the roughly 12-hour journey to Zurich, the aircraft performed two wide circles before returning to Hong Kong where it landed safely about 75 minutes after take-off, according to the tracking data.

Cathay did not describe the failed engine component in detail but said it was the first of its type to suffer such failure on any A350 aircraft worldwide.

“Thus far we have identified a number of the same engine components that need to be replaced. Spare parts have been secured and repair work is underway,” it said.

A person familiar with the matter said the incident involved a problem with a fuel nozzle, a component that directs fuel inside the engine.

Experts say such problems are rare but, barring a deeper flaw, generally raise fewer alarms than the failure of one of the major rotating parts such as a turbine blade. However, any widespread further inspections could be disruptive to airlines.

HONG KONG PROBE

Industry sources said Hong Kong’s Air Accident Investigation Authority had quickly launched an investigation. The bureau could not be reached for comment outside office hours.

Britain’s Air Accidents Investigation Branch said it would support any investigation carried out in Hong Kong.

According to Flightradar24 data, the diverted aircraft is an A350-1000, the larger of two models of twin-engined A350. These are powered by the XWB-97, Rolls’ largest civil jet engine.

Cathay operates 18 of the largest twin-engined Airbus planes as part of a mixed fleet of Airbus and Boeing jets.

It is one of the largest users of the A350-1000 alongside British Airways, which also has 18 in operation, but behind the largest operator, Qatar Airways, according to Airbus data.

There were no immediate reports of similar findings at other airlines. Other operators of the A350-1000 did not immediately respond to requests for comment.

The European Union Aviation Safety Agency (EASA), which is responsible for overseeing Airbus jets and has the power to order fleet-wide checks or repairs, did not rule out taking action but said it would wait for the results of the probe.

“We will be monitoring any information coming out of the technical investigation and will take decisions on any fleet level action as required,” a spokesperson said.

In total, Cathay operates 48 A350 jets including the smaller and more widely used A350-900, which runs on a different member of the Rolls-Royce Trent XWB engine family called the XWB-84.

The airline said it was coordinating with the Hong Kong Civil Aviation Department and the jet and engine manufacturers.

Cathay has around 100 planes currently on order including freighters, narrow-bodies and wide-bodies, with rights to acquire another 80.

(Additional reporting by Himanshi Akhand in Bengaluru; Editing by Alex Richardson, Christina Fincher and Tomasz Janowski)

Dow Jones Futures Fall With S&P 500 In Power Trend; Tesla Rival Leads 7 Stocks In Buy Zones

Dow Jones futures fell Tuesday morning, along with S&P 500 futures and Nasdaq futures after the Labor Day weekend.

The stock market rally showed mixed action last week. The Dow Jones hit a record high while the S&P 500 edged higher and Russell 2000 edged lower. The Nasdaq composite lagged, as Nvidia (NVDA) earnings failed to impress. But the tech-heavy composite did recover its 50-day line in a solid Friday bounce.

The S&P 500, just below a record high, has entered a power trend, a positive sign for the market rally. A number of stocks broke out or set up in the past week.

↑

X

S&P 500 Enters Power Trend; Broadcom, Comfort Systems, NextEra Energy In Focus

ServiceNow (NOW), Netflix (NFLX), AppLovin (APP), Comfort Systems (FIX), NextEra Energy (NEE) and Spotify (SPOT) are all in buy areas.

So is China EV giant BYD (BYDDF). The Tesla (TSLA) archrival broke out Friday, with BYD reporting a big jump in sales on Sunday. Several other China EV makers reported August deliveries as well.

Broadcom (AVGO), Samsara (IOT) and Dick’s Sporting Goods (DKS) are around buy points with earnings due this coming week.

On Friday, investors will get the August jobs report.

Nvidia and ServiceNow stock are on IBD Leaderboard. Comfort Systems is on IBD SwingTrader. Nvidia stock, Netflix, Samsara and Comfort Systems are on the IBD 50.

The video embedded in this article discussed the market action on Friday and for the week. It also analyzes Broadcom stock, Comfort Systems and NextEra Energy.

Dow Jones Futures Today

Dow Jones futures fell 0.5% vs. fair value. S&P 500 futures retreated 0.5% and Nasdaq 100 futures declined 0.6%.

Crude oil futures fell more than 1%.

U.S. stock markets were closed Monday for Labor Day, though other exchanges around the world were open.

The official China manufacturing index dipped 0.3 point in August to 49.1, further below the break-even 50 level and under views for an unchanged 49.4. However, the Caixin manufacturing index edged up 0.6 point to 50.4 vs. views for 50.

Remember that overnight action in Dow futures and elsewhere doesn’t necessarily translate into actual trading in the next regular stock market session.

Join IBD experts as they analyze leading stocks and the market on IBD Live

Stock Market Rally

The stock market rally had mixed action during the week, but had a strong finish Friday.

The Dow Jones Industrial Average rose 0.9% in last week’s stock market trading. The S&P 500 index climbed 0.2%. The Nasdaq composite fell 0.9%, but gained 1.1% on Friday. The small-cap Russell 2000 lost a fraction.

The S&P 500 closed Friday a fraction below the top of its recent range and less than 0.4% below all-time highs. On Friday, the benchmark index entered a power trend. It’s a positive sign, but not a buy signal itself. Mike Webster, IBD’s chief market strategist, said on IBD Live Friday:

“It’s very important to know that (the start of a power trend) … is not a buy signal. It is just a different phase. So what it does is you treat additional buy signals differently. Doesn’t mean you take extra action today but if we get more buy signals next week or the week after while the power trend is still going, if you were going to go on margin, if there’s stuff to buy, if you’re making progress and the power trend is still on, that would be the time to do it.”

The Nasdaq has some work to do before getting to its own power trend. Right now, it needs to decisively reclaim the 50-day line, then clear its recent range and the 18,000 level. On the flip side, there’s the risk that the Nasdaq could break below its 21-day line.

Nasdaq futures suggest the composite will fall back below the 50-day line and perhaps test the 21-day line at Tuesday’s open.

More broadly, the recent action in the Nasdaq, Nvidia and megacaps suggests that the tech sector may lag the non-tech sector for a while.

The 10-year Treasury yield rose 10 basis points to 3.91%, but it’s down 77 basis points over the last four months.

U.S. crude oil futures fell 1.7% to $73.55 a barrel last week.

ETFs

Among growth ETFs, the Innovator IBD 50 ETF (FFTY) fell 1.85% last week. The iShares Expanded Tech-Software Sector ETF (IGV) advanced 0.5%. ServiceNow stock is a big IGV position, with Samsara also in the ETF. The VanEck Vectors Semiconductor ETF (SMH) slumped 2%. Nvidia stock is the dominant SMH holding, with Broadcom also a key member.

SPDR S&P Metals & Mining ETF (XME) edged up about 0.1% last week. The Global X U.S. Infrastructure Development ETF (PAVE) climbed 0.5%. The SPDR S&P Homebuilders ETF (XHB) declined 1.5%. The Energy Select SPDR ETF (XLE) rose 1% and the Health Care Select Sector SPDR Fund (XLV) gained 1.1%.

The Industrial Select Sector SPDR Fund (XLI) rallied 1.7% while the Financial Select SPDR ETF (XLF) leapt 2.95%.

Reflecting more-speculative story stocks, ARK Innovation ETF (ARKK) slumped 3.1% last week and ARK Genomics ETF (ARKG) declined 2.15%. Tesla stock is still a major holding across Ark Invest’s ETFs. Cathie Wood also has built up a significant position in Nvidia and owns a small stake in BYD stock.

Time The Market With IBD’s ETF Market Strategy

Nvidia Stock

NVDA stock sold off 7.7% last week to 119.37. Shares rose 1.5% on Friday but still closed just below its 50-day line.

Nvidia fell modestly Tuesday morning.

Nvidia reported a 152% EPS gain late Wednesday and guided up for Q3 revenue. But the beat-and-raise wasn’t as large as in prior quarters.

After Friday’s close, Nvidia stock has a handle, giving it a lower official buy point of 131.26.

Stocks In Buy Zones

ServiceNow rose 3.2% to 855 last week, continuing a rebound from the Aug. 5 low. On Friday, NOW stock broke out past an 850.33 buy point from a new flat base.

AppLovin stock climbed 3% to 92.87. On Friday, APP stock finally closed above a 91.91 buy point from a V-shaped consolidation after several intraday attempts. The relative strength line, which tracks a stock’s performance vs. the S&P 500, is almost at a multiyear high.

Netflix stock climbed 2.1% to 701.35 last week, just above a 697.49 cup-base buy point.

Comfort Systems stock climbed 4.4% to 353.52. The AI-adjacent heating and cooling play on Friday closed above a 347.73 handle buy point as well as an alternate entry at 352.47, the top of the base.

NextEra stock rose 1.1% to 80.51, just reclaiming an 80.47 buy point on Aug. 26.

Spotify stock edged up 0.1% to 342.88, but held support at the 21-day line and remains within range of a 331.08 flat-base buy point, according to MarketSurge. Shares have been trading tightly for weeks. Investors could use 350.32 as a de facto four-weeks-tight entry within an emerging consolidation.

BYD stock broke out of a cup-with-handle base on Friday, jumping 5.2% to 30.50 for the week. Up 10.2% in 2024, BYD is the only EV maker that’s positive this year.

China EV Sales

On Sunday, BYD reported August sales of373,083, a big jump vs. July’s record 342,383, though there had been buzz that it would get closer to 400,000.

Among fellow China EV makers, Li Auto (LI) reported August deliveries fell vs. July’s record. Nio (NIO) deliveries edged down, but held above 20,000 for a fourth straight month. XPeng (XPEV) and Zeekr (ZK) reported big month-to-month gains. All four EV stocks are down sharply in 2024.

Tesla stock popped 3.8% Friday, but fell 2.8% for the week to 214.11, dropping below its 50-day. Shares rose slightly early Tuesday.

On Monday, industry data showed Tesla China sold 86,697 EVs in August, including exports, up 17% vs. July and 3% vs. a year earlier.

Stock Market Analysis

While the market rally is pausing, it’s made a lot of progress from the Aug. 5 low. More stocks are setting up bases that are no longer so V-shaped, with handles also coming into shape.

The S&P 500 entering a power trend reflects this broader picture.

Investors who made a series of buys since the Aug. 13 follow-through day may want to be cautious about significantly adding exposure until the current pause resolves itself.

If the S&P 500 and Nasdaq can clear their recent short-term ranges, that would be highly bullish, almost certainly coinciding with a number of breakouts.

But if the Nasdaq breaks clearly below the 50-day and 21-day lines, many recent buys and setups would falter, especially in tech.

Don’t be too exposed to AI and tech. Finance, utility and some retail and footwear stocks are showing strength, along with a variety of medicals.

Make sure you have your watchlists up to date and review your portfolio.

Read The Big Picture every day to stay in sync with the market direction and leading stocks and sectors.

Please follow Ed Carson on Threads at @edcarson1971 and X/Twitter at @IBD_ECarson for stock market updates and more.

YOU MIGHT ALSO LIKE:

Best Growth Stocks To Buy And Watch

IBD Digital: Unlock IBD’s Premium Stock Lists, Tools And Analysis Today

Tesla Struggles Below Key Level As BYD Breaks Out

S&P 500 Giants Meta, Eli Lilly Lead 5 Stocks Near Buy Points

Huawei To Release New Apple, Tesla Rivals Hours After iPhone Event

Morningstar Gives the 4% Rule a Thumbs Up – Can You Trust It for Your Retirement?

There’s been an ongoing debate about whether retirees should abandon the “4% rule” for withdrawals from retirement accounts, a retirement income rule of thumb for decades. The market volatility of recent years made that rule suspect for many new retirees, but a new study from Morningstar finds that the rule can still apply.

Do you have questions about building a long-term plan for retirement? Speak with a financial advisor today.

What Is the 4% Rule?

Created in 1994 by a financial planner named William Bengen, the 4% rule posits that retirees can make a well-structured retirement fund last 30 years by withdrawing no more than 4% of the balance in the first year of retirement, then adjusting subsequent withdrawals for inflation. Bengen’s research was based on each 30-year period of market returns and conditions dating back to 1926. He found that even during the worst three decades for markets – a stretch from October 1968 to 1998 – a retiree wouldn’t run out of money.

The popularity of the rule has fluctuated, and the strategy comes with some associated criticism. That’s because during down markets the sequence of returns risk can come into play, which occurs when the first years of withdrawals take place when the value of the retirement portfolio is down. Earlier this year, personal finance expert Suze Orman argued that the rule no longer made sense and that retirees should prolong working and withdraw as little money as possible, but no more than 3%.

How Morningstar’s Study Factors In

The investment analysis firm Morningstar has examined the safe rate of withdrawal for the first year of retirement for a few years running. Morningstar’s newest research finds that with the partial recovery of stocks, withdrawing up to 4% is once again a safe starting point.

“I estimate that retirees drawing down income from an investment portfolio can now afford to withdraw as much as 4.0% as an initial spending rate, assuming a 90% probability of still having funds remaining after a 30-year time horizon,” writes Morningstar portfolio strategist Amy C. Arnott, CFA.

Morningstar’s research on the optimum initial safe withdrawal rate started in 2021 when the analysis recommended a 3.3% withdrawal rate. For 2022, that rate increased to 3.8%. The research assumes a 90% chance of success for a portfolio where stocks make up 20% to 40% of the holdings. At the end of 30 years, the portfolio would still have value.

The big factor in this year’s assessment was a change in the estimate for long-term inflation that fell to 2.42% this year against 2.84% in 2022, along with improvements in returns on fixed-income investments, such as bonds and cash accounts. The projected 30-year fixed-income returns (including cash) increased from 4.44% in 2022 to 4.81% in 2023. The study noted that while the performance of stocks has improved so far this year, the projected 30-year returns on stocks decreased this year, slipping to 9.41% from 9.88% in 2022.

The study notes that retirees who take a more flexible approach to withdrawals than a strict rate of 4% adjusted annually for inflation could be able to withdraw more money at the beginning of retirement when retirees often spend more money as they establish a new retirement lifestyle. Those retirees would need to accept that their cash withdrawals would fluctuate from year to year and that they might have less money left after 30 years. Consider speaking with a financial advisor to build a personalized plan based on your goals.

Bottom Line

The popularity of the 4% rule comes and goes but it can be a good starting point for creating a safe strategy for retirement withdrawals. An important consideration is how much money is withdrawn in the first years of retirement, especially if the portfolio has lost value.

Retirement Planning Tips

-

A financial advisor can help you build an income plan for retirement. Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three vetted financial advisors who serve your area, and you can have a free introductory call with your advisor matches to decide which one you feel is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

-

Social Security plays a significant role in most people’s plans for retirement. SmartAsset’s Social Security calculator can help you estimate how much your benefits will be worth based on when you plan to claim them.

-

Keep an emergency fund on hand in case you run into unexpected expenses. An emergency fund should be liquid — in an account that isn’t at risk of significant fluctuation like the stock market. The tradeoff is that the value of liquid cash can be eroded by inflation. But a high-interest account allows you to earn compound interest. Compare savings accounts from these banks.

-

Are you a financial advisor looking to grow your business? SmartAsset AMP helps advisors connect with leads and offers marketing automation solutions so you can spend more time making conversions. Learn more about SmartAsset AMP.

Photo credit: ©iStock.com/Vadym Pastukh, ©iStock.com/Natalia Shabasheva

The post The 4% Rule for Retirement Withdrawals Might Finally Be Safe to Use Again, Says Morningstar appeared first on SmartReads by SmartAsset.

SoftBank, Walmart-Backed Robotics Giant Sees $9B Wipeout In Founder's Wealth After Company Stock That Surged Nearly 325% Last Year Takes A Steep Decline

Rick Cohen, founder of Symbotic SYM, has seen $9 billion erased from his net worth following a significant drop in his AI-powered company’s stock price.

What Happened: Cohen, who owns and chairs C&S Wholesale Grocers, founded Symbotic which manufactures AI-driven warehouse robots. Symbotic went public in mid-2022 via a special-purpose acquisition vehicle and has been backed by Masayoshi Son‘s SoftBank Group Corp. SFTBY and American retail Walmart Inc. WMT.

Cohen’s net worth was $21.4 billion at the start of January, placing him 94th on the Bloomberg Billionaires Index. However, his wealth has plummeted by 41% to $12.6 billion this year, dropping him to 178th place, Business Insider reported on Tuesday.

Symbotic’s stock, which surged over 325% last year, has fallen more than 60% in 2024. According to Benzinga Pro, the stock closed at $19.20 on Monday. The company’s value has now decreased to under $10 billion.

The decline is attributed to construction delays and increased implementation costs, which have squeezed profit margins. Symbotic also faces a class-action lawsuit alleging it misled the market about its growth prospects.

See Also: Rudy Giuliani’s Legal Troubles Deepen: Former Georgia Election Workers Seek To Seize Assets

Why It Matters: The dramatic decline in Symbotic’s stock price comes on the heels of its third-quarter financial results. Symbotic’s shares plummeted in after-hours trading following the release of these results. The company reported increased costs and delays in its projects, which have significantly impacted its profitability.

These financial troubles have not only affected the company’s stock but have also led to a substantial decrease in the net worth of its founder. A class-action lawsuit, filed today, further compounds the company’s woes, alleging that Symbotic misled investors about its growth potential.

Read Next:

Image via Symbotic

This story was generated using Benzinga Neuro and edited by Pooja Rajkumari

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

roofquotes.com Enables Homeowners to Find Best Roofers in Chattanooga Metro Area

Discover the best roofing deals in Chattanooga with a new site. Compare quotes effortlessly to find top-quality roofing at unbeatable prices.

CHATTANOOGA, Tenn., Sept. 02, 2024 (GLOBE NEWSWIRE) — roofquotes.com, an online roofing quote comparison tool for homeowners in need of a new roof and a reliable roofing contractor, today announced that it enables customers to find the best roofers in the Chattanooga metro area. The site homeowners’ shop for the best roofers in a specific geographic location. Experts guide the process with no pressure, so people are not overcharged for a new roof. Its free tool lets users compare roofing quotes from top providers, so they can find the most competitive prices.

Image by roofquotes.com

“We are so excited to be serving the greater Chattanooga, Tennessee area and promise that there is no upcharge to you. Our platform is free to use. Commissions are already included in the roofing company’s pricing, because they would have normally paid their own in-house sales representative. Your rates are the rates provided and do not change once quoted. Customers will never pay extra to use our service.”

roofquotes.com is a professional organization that ensures that customers receive the best prices. The service is spam free and fee free. Clients are provided with real quotes, not estimates.

According to the spokesperson, “Homeowners must be 100% satisfied with the roof work. We hold a portion of the roofing company’s payment until we get the thumbs up from you and the local building inspector.”

“We are a network of vetted partners who will ensure optimum quality,” the spokesperson added. “Our partners are the top 5% roofing companies that serve your area. Their performance has earned the trust of customers from across the United States.”

Roofers on roofquotes.com are required to register for rigorous background and credit checks. All licenses and insurance policies will be thoroughly verified. The site just needs the customers’ home address and basic contact details to get started. Using the latest technology, roofquotes.com will create a blueprint of the customer’s roof using aerial photos to determine exact specifications. The site then sends the plans to its network of trusted local roofers, who will perform a site visit if necessary.

Within 24 hours, clients will receive three to five quotes from local roofing experts, who will then explain each quote to help decide which one is best for the client’s property.

roofquotes.com helps homeowners find the best roofing contractor for the best price. Highlights of the service include:

- Focus on home roofing

- Service is free

- Compare prices from top local roofers

- Provide real prices, not guesses

- Experts help from start to finish

- Roofer paid in full only when the customer is satisfied

roofquotes.com does not sell any personal information or send spam.

For more information and to get a quote, visit www.roofquotes.com.

Media Contact:

Samual Newson

roofquotes.com

(629) 276-4161

hello@roofquotes.com

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/b1e819e9-8925-4e25-a98d-18997e1db99f

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

3 Monster Biotech Stocks to Buy Before 2025

Many investors rightfully identify biotech stocks as being riskier than average, and those stocks certainly have a habit of earning their reputation. Still, there are a few up-and-coming biotechs that have revenue and a clear path to generating even more in the near term, which makes them notably steadier than their earlier-stage peers that don’t yet have the certainty of selling anything at all.

With that in mind, let’s examine three monster biotechs that are worth buying before the close of this year.

1. Iovance Biotherapeutics

Buying Iovance Biotherapeutics (NASDAQ: IOVA) stock before the end of the year means getting exposure to a quickly growing business that’s lined up many more opportunities for further expansion.

Amtagvi, its cell therapy for advanced melanoma, is its first product, and will also likely be the main driver of growth through the end of the decade.

Since Amtagvi’s approval in the middle of the first quarter, the therapy’s rollout has proceeded swimmingly; the company brought in $31.1 million in total sales during the second quarter. That’s just the start; management expects as much as $475 million in revenue for its 2025 fiscal year. To accomplish that, it’s applying for approval in international jurisdictions right now, and should be hearing back in early 2025 from key regions like the E.U.

Beyond the next year, Iovance also has a pipeline full of programs investigating whether Amtagvi could be useful to treat other cancers, as a monotherapy or as a combination treatment with other oncology drugs. Most of those programs are in mid-stage clinical trials. So within the next three years, it’s feasible that the company could get approval for the additional indications under investigation, and its addressable market could expand.

And that’s why it’s worth buying the stock sooner rather than later. It may not get any cheaper in the long run than it is right now.

2. CRISPR Therapeutics

With its first cell therapy Casgevy successfully marketed for a pair of hereditary blood disorders, CRISPR Therapeutics (NASDAQ: CRSP) is in a state of maturity similar to Iovance.

So far, only 20 patients have been treated with the therapy, which is a functional cure for both sickle cell disease (SCD) and beta thalassemia. Wall Street analysts estimate on average that CRISPR Therapeutics will report revenue of $51 million this year — and around $288 million next year, once more of the company’s authorized treatment centers (ATCs) are set up around the globe.

Casgevy’s addressable market could be somewhat expanded with additional research and development (R&D), but fundamentally it targets a pair of rare diseases, so its total addressable market size is destined to be small. Therefore the biotech’s roadmap for growth will likely stem from its cell therapies for oncology indications, four of which are in clinical-stage development.

As those programs proceed toward their shot at approval and commercialization, favorable clinical data could drive the stock up in advance of any actual revenue — and at least one program will report data this year.

3. Zealand Pharma

Zealand Pharma (OTC: ZLDP.F) collects royalties and milestone payments from its medicines by licensing them out to pharma companies rather than taking on the burden of commercializing products on its own. In Q2, that revenue totaled just $4.9 million, but it’s unlikely to remain that low for much longer. Its pipeline is focused on developing drugs in one potentially very profitable field: weight loss.

Zealand’s most advanced program is already in phase 3 trials, and it has a big pharma partner, Boehringer Ingelheim, ready to go in the event that the candidate gets approved. More than one of Zealand’s programs has reported favorable clinical trial data, which suggests that it might be able to find a slice of the market due to unique advantages compared to the leading products made by leaders like Eli Lilly and Novo Nordisk. That means it probably won’t matter too much that it will show up to the market a bit late.

One other thing that positions Zealand Pharma strongly is its massive amount of cash. As of its fiscal second quarter, it had more than $1.2 billion in cash, equivalents, and short-term investments, whereas its quarterly total operating costs were just $42.1 million. This biotech won’t need to take out debt or issue more shares to generate capital any time soon — so shareholders will get to retain more of its earnings when they start to trickle in once again.

Should you invest $1,000 in Iovance Biotherapeutics right now?

Before you buy stock in Iovance Biotherapeutics, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Iovance Biotherapeutics wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $731,449!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 26, 2024

Alex Carchidi has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CRISPR Therapeutics and Iovance Biotherapeutics. The Motley Fool recommends Novo Nordisk. The Motley Fool has a disclosure policy.

3 Monster Biotech Stocks to Buy Before 2025 was originally published by The Motley Fool

Should You Buy Nvidia Before the Blackwell Launch? Here's What History Says

Nvidia (NASDAQ: NVDA) has been a stock market star over the past few years, soaring alongside demand for its artificial intelligence (AI) chips. The company dominates the AI chip market, with its graphics processing units (GPUs) holding an 80% share. And this has helped revenue climb in the triple digits quarter after quarter. As a result, Nvidia stock has advanced more than 2,700% over the past five years.

And Nvidia has a potentially big development just ahead. The technology giant is set to launch its new Blackwell architecture and chip later this year. The company expects to ramp up production in the fourth quarter and even generate major revenue from the platform. Should you buy Nvidia stock before this big launch? Let’s take a look at what history says.

Blackwell’s game-changing technologies

First, let’s consider why Blackwell itself is such an important development for Nvidia. This architecture is designed to run generative AI applications while consuming just 4% of the energy than Nvidia’s earlier platform, Hopper. The total cost of ownership should follow suit with a drop in the same range. And Hopper will include six game-changing technologies, including the world’s most powerful AI chip and high-performance networking, security, and reliability features.

For example, Blackwell’s fifth-generation NVLink offers high-speed communication among as many as 576 GPUs. And the new Blackwell GPU holds 208 billion transistors — there are 80 billion in Nvidia’s current top chip, the H100. More transistors equals greater processing power, a major plus for customers launching generative AI projects.

Nvidia says demand for Blackwell has surpassed supply and predicts this will continue into the next fiscal year. And investors won’t have to wait long to see revenue emerging from this new platform. The chip designer expects “several billion dollars” of Blackwell revenue in the fourth quarter.

Will Nvidia’s shares take off following the Blackwell launch? The stock dipped recently, falling nearly 20% from the start of July through the early days of August. Still, it rebounded from that decline and is now heading for a 140% increase since the start of the year.

Will Nvidia’s momentum continue?

Could the Blackwell launch keep the momentum going? Let’s look at how Nvidia stock performed following the launches of its two previous architectures, Hopper and Ampere. Nvidia released Hopper in the fall of 2022 and Ampere in the spring of 2020. In both cases, the stock rose by double digits in the three months following the launch — 22% following the release of Hopper and 44% following the release of Ampere.

But there’s no guarantee that history will repeat itself. And this brings me to the importance of long-term investing.

No matter what Nvidia stock does in the three months following the Blackwell launch, there are plenty of reasons to be positive about the shares over the long term. The company, which has promised annual updates to its chips, is likely to maintain its AI chip leadership. This should make it very difficult for rivals to unseat Nvidia.

Nvidia’s big customers

The chip designer has also expanded well beyond the GPU, offering entire platforms for AI and selling its products through major cloud service providers. Many of the world’s biggest technology companies, like Microsoft and Meta Platforms, rely on Nvidia’s GPUs to power their AI projects. And all of this is happening in a high-growth environment. Market research firm MarketsandMarkets expects the AI market to expand from about $200 billion right now to more than $1 trillion by the end of the decade.

Meanwhile, Nvidia shares are trading for about 42 times forward earnings estimates. While this isn’t dirt cheap, it’s a very reasonable price for a company that’s delivered so much growth in recent years and is likely to keep that momentum going thanks to its focus on innovation.

So even if Nvidia doesn’t surge after the launch of Blackwell, the long-term picture remains bright — and that makes it a fantastic stock to snap up today and hang on to for the long haul.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $731,449!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 26, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Adria Cimino has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Should You Buy Nvidia Before the Blackwell Launch? Here’s What History Says was originally published by The Motley Fool