Alibaba Upgrades To Dual Primary Listing In Hong Kong

Alibaba has announced plans to voluntarily change its secondary listing status on the Hong Kong Stock Exchange to a primary listing, effective Aug. 28.

The Hangzhou-based technology behemoth will have a dual primary listing on the HKEx and the New York Stock Exchange.

More from WWD

The switch would enable Alibaba to tap into a pool of 220 million stock investors in mainland China. These investors can access Alibaba shares via Stock Connect, a mutual market access program between the Shanghai Stock Exchange, Shenzhen Stock Exchange and HKEx.

First introduced in 2014, the Stock Connect allows mainland investors to access Hong Kong shares, or Southbound capital, and Hong Kong and overseas investors to trade qualified A shares, or Northbound capital, within a daily quota.

Alibaba will then seek approval from the exchange operators in Shenzhen and Shanghai before making its cross-channel market debut in early September.

Morgan Stanley estimates that mainland Chinese investors will be able to access the stock as soon as Sept. 9.

“Southbound could own around 7 percent of all shares by six months after inclusion; in the long term the percentage may stabilize around the low teens. When we look at a longer-term period, including Tencent, Southbound ownership represents an average of 11 percent of total shares of these companies,” Morgan Stanley said in a report published last June.

Alibaba’s stock rose 0.7 percent in Hong Kong on Friday, taking its gains to 10 percent year-to-date. The e-commerce giant’s revenue growth slowed to 4 percent in the second quarter as it navigates an economic slowdown while seeking growth via its AI and cloud businesses.

During the Paris Olympics, Alibaba showcased “the future of shopping” with virtual try-ons, avatars and an IRL runway in a four-room pavilion on the Avenue des Champs-Elysées. The sleek, open-air pavilion showcased how the technology can be used in the beauty and fashion categories, all powered by Alibaba’s proprietary Qwen LLM.

The company also debuted its Smart Virtual Boxing project at Wonder Avenue, using the Qwen AI to analyze moves and performances of each contestant in a virtual boxing match, providing real-time commentary and predicting future performance.

Best of WWD

3 Warren Buffett Stocks That Are Screaming Buys Right Now

Are you looking to load up on some new long-term stocks? There are myriad ways of finding them. One of the best means of doing so, however, is still poaching a few of Warren Buffett’s picks. They don’t call him the Oracle of Omaha for nothing, after all.

With that as the backdrop, here’s a closer look at three of Buffett’s Berkshire Hathaway portfolio’s holdings. Most of Berkshire’s picks are solid long-term names. However, these particular three picks are screaming buys right now largely because they’re undeservedly beaten down.

1. Occidental Petroleum

Contrary to a common assumption, oil isn’t a dying business. It’s still growing, in fact. The United States Energy Information Administration predicts liquid fuels derived from crude oil will still be the planet’s top source of energy production as far down the road as 2050. The world’s just not ready to make a sweeping shift to alternative energy.

The oil industry will continue evolving during this time, however. Namely, oil companies will become smarter about keeping themselves in business.

Enter Occidental Petroleum (NYSE: OXY). It is not the energy business’s most familiar name. There’s a reason Buffett loves it enough to continue buying it, though. Not only is it well-versed when it comes to fracking, the company is willing to restructure itself in order to optimize its operation. As Buffett wrote of Occidental’s CEO Vicki Hollub in a 2023 letter to Berkshire Hathaway shareholders, “Vicki does know how to separate oil from rock, and that’s an uncommon talent, valuable to her shareholders and to her country.”

Then there’s the other, unexpected reason Buffett’s Berkshire now owns nearly 28% of Occidental (a 255-million-share, $14.7 billion stake). That’s its work on the carbon-capture front. Simply put, carbon capture is the process of removing carbon — in the form of carbon dioxide — from the ambient air so it doesn’t damage the environment. The science is still relatively new and not yet fully refined. It does work, though, and it is being commercialized.

An outlook from Polaris Market Research suggests that the annual Direct Air Capture Systems (DACS) market is set to grow at an average yearly pace of 58% through 2032, when it will be worth nearly $4 billion (although it’s an estimate that could ultimately prove too conservative). Whatever the case, the tech has the potential to prolong the planet’s usage of oil.

Occidental Petroleum shares are down 16% from April’s high, largely in step with crude oil’s price pullback. That’s only a temporary swoon, though — for both of them.

2. Bank of America

You’re likely already aware that Berkshire shed a big piece of its stake in Bank of America (NYSE: BAC) just a few weeks ago. Namely, so far, it’s sold nearly $4 billion worth of the bank stock. It’s certainly conceivable that more could be dumped in the near future, too.

Investors are interpreting the move as a red flag, and understandably so. After all, BofA’s second-quarter results weren’t exactly thrilling. Net income fell on a year-over-year basis despite modest revenue growth. Falling interest rates are making lending less profitable at a time when borrowers are struggling to continue making payments on their outstanding loans; charge-offs on soured loans nearly doubled year over year as well.

The end to the underlying economic headwind isn’t exactly visible on the horizon, either. That’s why nobody blames Buffett for paring back on the position, particularly in light of potential increases in capital gains tax rates. The assumption, however, ignores a couple of details.

First and foremost, while Berkshire Hathaway admittedly sold a sizable swath of its Bank of America stake, it still owns so much more. As of the latest known tally, the conglomerate is still holding more than 940 million shares of the bank collectively worth $37 billion. Buffett’s hardly abandoned the position. He may have simply been taking some profits and rebalancing a portfolio that sorely needed it while it makes sense to do so.

Second, Buffett loves value stocks that generate lots of reliable cash. Headwinds or not, BofA still offers both. Shares are priced at less than 11 times next year’s projected earnings, which are still expected to be better than this year’s, and its forward-looking dividend yield stands at a healthy 2.7%. You can find higher yields, but you won’t find higher yields in the banking business at a comparable risk profile.

3. Kraft Heinz

Finally, add The Kraft Heinz Company (NASDAQ: KHC) to your list of Warren Buffett stocks that are screaming buys right now, while shares are still down 65% from their 2017 peak and still near their 2020 low.

Kraft Heinz is one of Buffett’s rare missteps. He helped orchestrate the 2015 merger of then-separate Kraft and Heinz into a single company with the expectation that synergies would be achieved. The market even agreed for a while, driving the newly minted stock higher following the union.

Reality finally set in by early 2017, though. That’s when shares began a long, sharp sell-off, reflecting the fact that this pairing just wasn’t working as hoped. In 2019, Buffett conceded, “I was wrong in a couple of ways on Kraft Heinz,” adding that “We [Berkshire] overpaid for Kraft.” By then, however, it was too late. The mess was made. Many investors have since simply given up on the company, presuming there’s just too much to fix following the merger.

Not Buffett, though. Berkshire Hathaway still owns nearly 326 million shares of the beaten-down stock, seemingly anticipating an eventual recovery.

The thing is, it’s not a crazy expectation. Relatively new CEO Carlos Abrams-Rivera understands what needs to be fixed and knows how to fix it. Innovation is prioritized again, as are smart branding partnerships. For example, its Taco Bell at-home Crunchwrap Supreme quesadillas are a hit with consumers. Kraft Heinz is also (finally) giving meaningful thought to running a cost-effective operation and is leveraging technology when and where appropriate to do so. While not much, these and other initiatives are starting to produce consistent, measurable growth.

There are legitimate concerns here, to be sure. Chief among them is the fact that Kraft Heinz has raised its dividend payment since lowering it in early 2019 in an effort to deal with some of the uglier concerns on its balance sheet. The company’s more than able to cover its current payouts, though, and with earnings on the rise, dividend increases in the foreseeable future aren’t out of the question.

Should you invest $1,000 in Kraft Heinz right now?

Before you buy stock in Kraft Heinz, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Kraft Heinz wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $779,735!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Bank of America is an advertising partner of The Ascent, a Motley Fool company. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bank of America and Berkshire Hathaway. The Motley Fool recommends Kraft Heinz and Occidental Petroleum. The Motley Fool has a disclosure policy.

3 Warren Buffett Stocks That Are Screaming Buys Right Now was originally published by The Motley Fool

Why Charles Schwab Stock Got Socked on Thursday

Charles Schwab (NYSE: SCHW) saw a dip in its share price on Thursday due to events outside the company’s control. That’s because the top news item for the brokerage was that a major shareholder unloaded some of its Schwab holdings at a discount.

Schwab’s stock price sagged in sympathy. By the end of the trading session, the company’s shares had lost 0.5% of their value. That compared favorably, but only just, with the S&P 500 index’s 0.8% decline on the day.

Brokerage for sale, cheap

Within its fiscal third quarter of fiscal 2024 earnings report, Canada-based Toronto-Dominion Bank (NYSE: TD) divulged that it sold 40.5 million shares of Schwab’s common stock. It earned roughly $2.5 billion on the sale, putting the average share price at $61.73. That’s notably under the brokerage’s most recent closing price of $64.27 per share.

The move was part of an attempt to shore up the lender’s finances. For the quarter, it booked a 2.6 billion Canadian dollar ($1.9 billion) provision to pay fines that are expected to be handed down by the U.S. Department of Justice (DoJ). That agency is currently in the midst of a probe into the bank‘s anti-money laundering (AML) efforts.

The share sale reduces Toronto-Dominion’s stake in Schwab to slightly over 10%. Before the divestment, that figure stood at 12.3%.

Already not in the market’s good graces

Although extenuating circumstances were the driving force behind Toronto-Dominion’s divestment, investors have generally been cold on Schwab lately. Earlier this summer, the company said it was slimming down its banking operations, and some market players weren’t too happy about that strategy. Meanwhile, its second-quarter earnings featured a headline net income number that barely budged from the year-ago figure.

Should you invest $1,000 in Charles Schwab right now?

Before you buy stock in Charles Schwab, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Charles Schwab wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $787,394!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 22, 2024

Charles Schwab is an advertising partner of The Ascent, a Motley Fool company. Eric Volkman has positions in Charles Schwab. The Motley Fool has positions in and recommends Charles Schwab. The Motley Fool recommends the following options: short September 2024 $77.50 calls on Charles Schwab. The Motley Fool has a disclosure policy.

Why Charles Schwab Stock Got Socked on Thursday was originally published by The Motley Fool

2 Stock-Split Stocks to Buy Before They Soar 47% and 57%, According to Certain Wall Street Analysts

Smart investors pay attention to stock splits because they are often an indirect indicator of quality businesses. To elaborate, forward stock splits are only necessary after substantial and sustained share price appreciation, and that rarely happens to mediocre businesses.

Not surprisingly, stocks that split tend to beat the S&P 500 (SNPINDEX: ^GSPC), at least temporarily, according to Bank of America. Since 1980, stocks have generated an average return of 25% during the one-year period following a stock split announcement, while the S&P 500 returned 12% during the same period.

This year, Walmart (NYSE: WMT) announced a 3-for-1 stock split on Jan. 30, and completed the split after market close on Feb. 23. Shares have surged 35% since the announcement, but Simeon Gutman at Morgan Stanley has set a bull-case target of $109 per share. That forecast implies 47% upside from its current share price of $74.

Similarly, Nvidia (NASDAQ: NVDA) announced a 10-for-1 stock split on May 22, and completed the split after market close on June 7. Shares have surged 34% since the announcement, but Rosenblatt analyst Hans Mosesmann has set a target of $200 per share. That forecast implies 57% upside from its current share price of $127.

Here’s what investors should know about Walmart and Nvidia.

1. Walmart

Walmart is the largest retailer in the world and the second-largest e-commerce business in the United States. That scale affords the company an important cost advantage. It can buy inventory from suppliers in bulk and pass savings to consumers. In turn, Walmart can sell a wide assortment of products at low prices, including perishable groceries that online retailers typically lack.

The promise of bargain prices across a broad range of goods brings consumers to Walmart more frequently than any other superstore. The company accounted for 62% of superstore visits during the first four months of 2024, according to Placer.ai. That consistent foot traffic reinforces the ubiquity of the Walmart brand, keeping the company top of mind for consumers.

Walmart reported encouraging financial results in the second quarter. Revenue increased 4.8% to $169 billion on particularly strong sales growth in e-commerce, membership fees, and advertising. Meanwhile, gross profit margin expanded 43 basis points because of pricing power, lower delivery costs per order, and a sales mix shift toward more profitable products like advertising services. In turn, non-GAAP net income increased 10% to $0.67 per diluted share.

CEO Doug McMillon said, “Each part of our business is growing — store and club sales are up, e-commerce is compounding as we layer on pickup and even faster growth in delivery as our speed improves.” He also said new businesses like advertising, memberships, and the online marketplace for third-party merchants are “diversifying profits and reinforcing the resilience of our business model.”

Going forward, Wall Street expects adjusted earnings to grow at 10% annually through fiscal 2027 (ends January 2027). That consensus estimate makes the current valuation of 31 times earnings look expensive, which makes the 47% return implied by Morgan Stanley’s bull-case price target seem unlikely. Personally, I would keep Walmart on my watchlist until shares look a little cheaper.

2. Nvidia

Nvidia accounted for 98% of data center graphics processing unit (GPU) shipments last year, and its market share was similar in the previous year. GPUs can perform technical calculations more quickly and efficiently than central processing units (CPUs), which makes them good at accelerating demanding workloads like rendering 3D graphics, training machine learning models, and running artificial intelligence (AI) applications.

Nvidia’s long-standing dominance in data center GPUs means the company was perfectly positioned to benefit when ChatGPT launched in 2022, eliciting an exponential increase in demand for AI infrastructure. Nvidia holds over 80% market share in AI chips, and Forrester Research recently wrote, “Nvidia sets the pace for AI infrastructure worldwide. Without Nvidia GPUs, modern AI wouldn’t be possible.”

Nvidia reported first-quarter financial results that beat expectations on the top and bottom lines. Revenue surged 262% to $26 billion on momentum in the data center segment. That was fueled by “strong and accelerating demand for generative AI training and inference on the Hopper platform,” according to CEO Jensen Huang. Meanwhile, non-GAAP net income jump 461% to $6.12 per diluted share.

Investors should know that shipments of Nvidia Blackwell GPUs — chips that offer faster training and inference speeds than the previous Hopper architecture — will be delayed by three months. Technology-focused news company The Information broke the story earlier this month, citing design flaws discovered “unusually late in the production process” as the reason for the delay.

Management will likely address the issue when the company announces second-quarter financial results on Aug. 28. The stock could move sharply in either direction depending on the context, so shareholders should be ready. That said, the long-term investment thesis remains intact. Nvidia GPUs are the industry standard in AI computing, and the graphics processor market is forecasted to grow at 28% annually through 2030, according to Grand View Research.

Wall Street expects Nvidia’s adjusted earnings to grow at 39% annually through fiscal 2027 (ends January 2027). In that context, the current valuation of 71 times adjusted earnings looks a little expensive, so I doubt Nvidia will return 57% in the next 12 months. However, I think investors can buy a small position in the stock today, provided they are comfortable with the possibility of a significant decline post earnings.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $779,735!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Bank of America is an advertising partner of The Ascent, a Motley Fool company. Trevor Jennewine has positions in Nvidia. The Motley Fool has positions in and recommends Bank of America, Nvidia, and Walmart. The Motley Fool has a disclosure policy.

2 Stock-Split Stocks to Buy Before They Soar 47% and 57%, According to Certain Wall Street Analysts was originally published by The Motley Fool

5 Enjoyable Retirement Hobbies That Won't Drain Your Wallet

Retirement marks one of the great transitions in your life. For most people, until your late-teens or early-twenties you define your time by going to school. After that your schedule is shaped around the need to work and earn a living. Retirement is the third stage. Nobody has assigned you to a classroom and no outside forces (whether boss, customers or growing seasons) have fixed you with a schedule. You get to decide what to do with your time.

You can do great things in your retirement, but first you’ll need to figure out what you want to get out of this phase of your life. To help you figure that out, here are a few places to start. For help getting ready for retirement or managing your money as you get older, consider working with a financial advisor.

Writing, Photography and Art

A lot of people have an inner artist that they’ve never set loose. Whether you want to write a memoir, a history or a novel, you’re not alone. The same is true for if you have paintings inside of you, or sculptures. Or if you’ve always wanted to pick up a camera and figure out exactly how to make the most of ISO and aperture.

All of this takes time, and perhaps you’ve never had it before. Now, you do.

For retirees, now is the time to get serious about that inner artist. Maybe you want to actually pitch your manuscripts. Maybe you want to start a website or an Instagram to publish your visual works and photography. Maybe you don’t want any of that and are seeking the simple pleasure of creating something that makes you happy — not everything has to be for material gain, after all.

No matter what you’re looking for, you have the time and opportunity to turn this from an idle idea into something real. However you define that.

If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

Education

For many retirees, going back to school is a very popular option. You can pick up subjects that you never learned before, things that were always fascinating but you never had the time. Making this even better, most universities have no- or low-cost options such as auditing for students who just want the education and aren’t seeking a degree.

And if you like the social and campus environment of a school, but aren’t interested in taking any more exams, perhaps now’s a good time to consider giving the tests instead. You have an entire career’s worth of expertise under your belt. Look into teaching a few courses at your local community college, or mentoring students who need extra help in your field.

It can be the perfect combination of purpose and time commitment.

Travel

Perhaps the single most popular answer for “what to do in retirement” is travel. That doesn’t make it wrong, though, or any less exciting.

If your retirement savings went well, this is when you can have the best intersection of time and money. In your youth, you had plenty of time but no money to afford those big adventures. In your working years, you may have had the money but much less time. Now, for many people, you have both. Compounding all of that is the reality of health in retirement. Today’s retirees are healthier and stronger than ever.

So make the most of it. Take trips both big and small. In particular, embrace the advantages of your situation. You have complete control of your own schedule, so plan spontaneous trips as the mood strikes you. Jump in the car on a random morning and take a road trip to see new cities. Call a couple of hotels on the way. Save some money by heading out on a Tuesday, when rates are low.

Or go the opposite direction. Plan a three month trip to parts of the world you ordinarily couldn’t see. Traveling around Indonesia can take days at a time just to get from one island to the next, for example. That’s a hassle for someone burning their way through vacation time, but much less so for a retiree with a wide open schedule and no rush to get home.

Traveling in retirement is indeed a popular hobby, but don’t just travel. Take advantage of your schedule to do things you otherwise couldn’t.

Athletics

It goes without saying by now that pickleball has taken off for many people, especially retirees. Maybe you love the idea of trying out this hot kinda-new game. Maybe you don’t.

But let’s take it back to first principles.

Picking up a sport in retirement is a fantastic idea. Sports are fun, social events. They get you out and exercising, and a lot of people love the competition. This is a good idea all around. The key is to pick a sport that works for you. After all, arguably the single most defining part of retirement is that you are getting older, which makes physical activity that much harder.

So look at what makes pickleball such a good fit. It is:

-

Social

-

Low-impact

-

Low-commitment

Sports are a great option for a hobby in retirement. If you aren’t sure what to pick up, this is a great profile to start with. Pick a sport that doesn’t need a lot of training, equipment or experience to enjoy. Be mindful of any sports that will stress trouble spots like your joints or back; the sweet spot is something that has you breaking a sweat without causing pain. And make it something social, so that you can have a good time playing.

Coding

Generation X will hit their 60s soon enough, and they like their tech.

Your retirement is a great time to pick up new things and new ideas, and in the 21st Century one of the best ways to express a new idea is through code. Whether you want to build an app, a website or a full program, this can be the perfect hobby for a retiree who wants to transition into something new.

Have you ever wanted to create a video game? Now you can. Was there something in your work life that always seemed like it could be done better? Get around to fixing that problem. Do you just want to pull up Atom and see what happens? Go for it.

Coding offers the combination of education and expression, letting you learn something new while creating at the same time. As far as hobbies go, you can’t get much better than that.

The Bottom Line

How you finance your retirement is an essential question for your working life. How you use that retirement is arguably the defining question of your retired life. Here are five ideas to get you started.

Retirement Planning Tips

-

Nothing here jumping out at you? Don’t worry, there are more options.

-

A financial advisor can help you get set up for a fun retirement. Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three vetted financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

-

Keep an emergency fund on hand in case you run into unexpected expenses. An emergency fund should be liquid — in an account that isn’t at risk of significant fluctuation like the stock market. The tradeoff is that the value of liquid cash can be eroded by inflation. But a high-interest account allows you to earn compound interest. Compare savings accounts from these banks.

-

Are you a financial advisor looking to grow your business? SmartAsset AMP helps advisors connect with leads and offers marketing automation solutions so you can spend more time making conversions. Learn more about SmartAsset AMP.

Photo credit: ©iStock.com/Drazen Zigic, ©iStock.com/BraunS, ©iStock.com/RichLegg

The post Five Fun Hobbies to Take Up in Retirement appeared first on SmartAsset Blog.

This is a fair price range for Nvidia stock according to these analysts

Nvidia (NASDAQ:NVDA) continues to be one of the most demanded stocks in the tech sector, with Itau BBA analysts offering a detailed assessment of its prospects and a fair price range for the semiconductor company’s shares.

The analysts recently reviewed several factors impacting Nvidia, including delays in the Blackwell chip and potential concerns around capital expenditure (capex) overbuild by major tech companies.

Despite these challenges, Itau BBA expresses increasing confidence in Nvidia’s earnings performance for the next two to three quarters.

They believe that the Blackwell delay, contrary to popular opinion, may actually serve as a tailwind for short-term numbers, particularly with the H200 chip proving more accretive than the B100 or B200 models.

However, the analysts also highlight potential risks to Nvidia’s implied growth in calendar year 2026 (CY26). “To command a 30x P/E CY25, we believe that NVDA should have a CY26 EPS growth of at least 20%,” writes Itau BBA.

A capex exercise based on Microsoft (NASDAQ:MSFT)’s spending suggests that if Nvidia continues to grow at these levels, Microsoft’s capex could reach 100% of its cash flow from operations or EBIT by FY26, raising concerns about sustainability.

To alleviate these concerns, the analysts point to the importance of faster AI adoption. They cite Microsoft’s bullish tone in a recent earnings call, where a mass rollout of M365 Copilot was highlighted as a potential driver for increased AI infrastructure investment, which could benefit Nvidia.

“All-in, we continue to see NVDA delivering a USD5-6 EPS in CY25. However, we believe that we could see a semi infrastructure digestion at some point in CY26, adds the firm.

Itau BBA currently maintains its Outperform rating on the stock, explaining that its EPS projection could result in a fair price range of $150 to $180 a share for NVDA (based on a 30x P/E ratio).

Related Articles

This is a fair price range for Nvidia stock according to these analysts

Analyst Report: Clorox Co.

Summary

Clorox manufactures and markets a wide array of consumer products ranging from bleach to cat litter to Hidden Valley Ranch dressing. The company’s operations are divided into four operating segments: Health and Wellness, Household, Lifestyle, and International. The company has approximately 8,000 employees. CLX shares are part of the S&P 500 and the S&P Div

Upgrade to begin using premium research reports and get so much more.

Exclusive reports, detailed company profiles, and best-in-class trade insights to take your portfolio to the next level

Bennifer's House Is On Zillow: Guess The Taxes J Lo, Ben Affleck Paid On Their Up-For-Sale California Home

Benzinga and Yahoo Finance LLC may earn commission or revenue on some items through the links below.

Jennifer Lopez officially filed for divorce from Ben Affleck, ending the Hollywood relationship after two years of marriage. The couple has also put their former home, a 38,000-square-foot mansion in Beverley Hills, up for sale.

Trending Now:

And while red-carpet superstars don’t look like us, eat like us or dress like us, they do sell their homes the same way we do—by listing it on Zillow. Zillow Group (NASDAQ:Z)(NASDAQ:ZG) has the property listed for $68 million, around $7 million more than the house was bought for in 2023.

The house comes with a large pool, and an even larger tax bill. Zillow shows that the California property tax for the house was more than $400,000 last year, a little higher than 1% of the home’s assessed value.

And despite California’s reputation for high taxes, the state’s property tax rate is actually lower than most other states, according to Bankrate. If Bennifer’s house were located in Connecticut, for example, the property tax would be around $800,000.

In addition to the pool, the house features an indoor pickleball/basketball court, 12 bedrooms and 24 bathrooms. The house also has a fitness center and gym, a rooftop patio on the second floor and more.

Don’t miss the real AI boom – here’s how to use just $10 to invest in high growth private tech companies.

This is a paid advertisement. Carefully consider the investment objectives, risks, charges and expenses of the Fundrise Innovation Fund before investing. This and other information can be found in the Fund’s prospectus. Read them carefully before investing.

You Can Profit From Real Estate Without Owning Property

The current high-interest-rate environment has created an incredible opportunity for income-seeking investors to earn massive yields and you don’t have to own property to do it…

The Arrived Homes investment platform has created a Private Credit Fund, which provides access to a pool of short-term loans backed by residential real estate with a target 7% to 9% net annual yield paid to investors monthly. The best part? Unlike other private credit funds, this one has a minimum investment of only $100.

Don’t miss out on this opportunity to take advantage of high-yield investments while rates are high. Check out Benzinga’s favorite high-yield offerings.

This article Bennifer’s House Is On Zillow: Guess The Taxes J Lo, Ben Affleck Paid On Their Up-For-Sale California Home originally appeared on Benzinga.com

An oil tycoon sold his company for $26 billion this year — but died before the deal closed

-

Autry Stephens agreed to sell his company for $26 billion in cash and stock in February.

-

The oil tycoon was set to become one of the world’s 100 richest people, but he died this month.

-

Stephens wasn’t fussed about lavish living, and his family will still profit if the deal closes.

Autry Stephens struck a deal in February that would have made him America’s richest oilman and one of the world’s 100 wealthiest people — but he died before it closed.

The founder and owner of Endeavor Energy Resources agreed to sell the Texas oil producer to Diamondback Energy for $26 billion this spring. A cancer diagnosis spurred his decision to cash out, he told The Wall Street Journal at the time. Stephens was 86 when he died last week.

The planned merger, still expected to close in the fourth quarter, has added $17.5 billion to Stephens’ net worth this year, according to the Bloomberg Billionaires Index. The late entrepreneur’s fortune has nearly quadrupled since January from about $6 billion to $23.4 billion, placing him 85th on the list.

Only 14 people on Bloomberg’s rich list have made more money this year, and none of them rank lower than 18th. Stephens has even outpaced the world’s richest person, Elon Musk (up $15.1 billion), as well as the likes of former Microsoft CEO Steve Ballmer (up $16.3 billion) and Asia’s richest person, Mukesh Ambani (up $16.4 billion).

Stephens’ immediate family members are the sole owners of Endeavor following his demise, according to Bloomberg. They’re poised to receive the $8 billion in cash and 117.3 million Diamondback shares from the deal in his stead. The stake was worth about $17 billion just before the tie-up was announced and is now valued at $22 billion because of Diamondback’s rising stock price.

Stephens may have decided that, given his ill health and the lack of an obvious heir to take over the family business, it was best to secure his family’s future.

The oil tycoon was still a multibillionaire when he died, but he appears to have shared the investor Warren Buffett’s taste for a simple life.

Stephens grew up on a peanut and watermelon farm, drove a beaten-up Toyota Land Cruiser, and eschewed private jets for cheap flights with Southwest Airlines, the Journal reported.

Read the original article on Business Insider

Forget ExxonMobil: Buy This High-Yield Dividend Stock Instead

ExxonMobil (NYSE: XOM) is a fine and worthy dividend-stock candidate for investors looking for exposure to oil, but it doesn’t trade at Devon Energy‘s (NYSE: DVN) cash-flow valuation. Moreover, while ExxonMobil’s stock is up almost 19% this year, Devon’s stock is flat this year and presents an excellent value for investors. Here’s why.

Devon Energy continues to progress

Devon Energy’s recent second-quarter results contained several positives that helped confirm the investment case for the stock, including the company’s upgraded production target. In a year when management decided to focus investment in its core assets in the Delaware Basin, it’s reasonable to expect an improvement in well productivity and total production. Indeed, management started the year predicting a 10% improvement in well productivity and the production of 650,000 barrels of oil equivalent per day (Boe/d) in 2024.

The good news is that management reaffirmed the target for well-productivity improvement and, for the second time this year, upgraded its full-year production target to a new range of 677,000 Boe/d to 688,000 Boe/d — a 5% upgrade from the original target. It’s an even better result when considering that the price of oil started the year at around $70 a barrel but has spent most of it above $75 a barrel.

Cash-flow valuation

As noted above, Devon Energy trades at a more attractive valuation than many other oil stocks. For example, Wall Street analysts expect ExxonMobil to generate $34.7 billion in free cash flow (FCF) in 2024. Based on ExxonMobil’s current market cap of $527.5 billion, that FCF is equivalent to 6.6% of the company’s market cap.

It’s an attractive cash-flow yield, but Devon’s is even higher. Based on the company’s market cap of around $26.8 billion at the time of the results, Devon’s management believes it will trade at a 9% FCF yield at a price of oil of $70 a barrel in 2024, 11% at $80 a barrel, and 13% at $90 a barrel. Looking at the current market cap puts these figures at roughly 8.5% at $79 a barrel, 10.3% at $80 a barrel, and 12.2% at $90 a barrel.

With the current price of oil at $76 a barrel, Devon clearly trades at a very attractive FCF valuation.

An acquisition isn’t in the numbers

Devon’s management expects to complete the acquisition of the Williston Basin business of Grayson Mill Energy for $5 billion ($3.25 billion in cash and $1.75 billion in stock) by the end of the third quarter. Investors should note that neither the upgraded production forecast nor the FCF yield calculations assume any contribution from this acquisition in 2024.

Capital-allocation policy

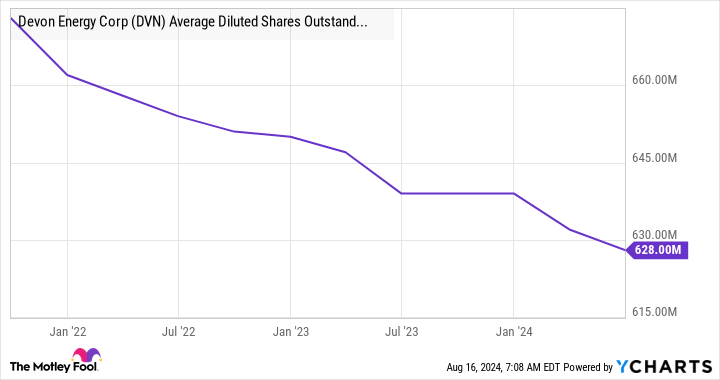

Devon Energy’s capital allocation policy targets using 30% of FCF to support the balance sheet, partly in connection with the acquisition. (Devon will initiate a $2.5 billion debt-reduction program.) The remaining 70% will be used for share repurchases, a quarterly fixed dividend of $0.22 per share, and a variable dividend.

The total dividend in the first quarter was $0.35 per share, and $0.44 per share in the second quarter, with management prioritizing share repurchases over the variable dividend. While some investors may not like that, it reduces shares in issue and increases the claim of existing shareholders on future cash flow.

Putting things into perspective, the abovementioned FCF yields make it clear that Devon could potentially pay significantly higher dividends if it so desired. However, the idea of investing in a company is that management can generate better returns on investment than an investor can, so it makes sense to let them do that by retaining cash to add value.

A stock to buy

Devon’s FCF generation (which will be boosted by the acquisition in the third quarter) and its policy of returning cash to shareholders in the form of share buybacks and dividends ensures that investors can look forward to significant returns from Devon in the coming years, provided the price of oil stays relatively high.

Should you invest $1,000 in Devon Energy right now?

Before you buy stock in Devon Energy, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Devon Energy wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $779,735!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Forget ExxonMobil: Buy This High-Yield Dividend Stock Instead was originally published by The Motley Fool