Jim Cramer Warns Apple Stock Should Have 'Never Been Up That Much' After Q3 Earnings Even As This Analyst Defends iPhone 16 Launch

After Apple Inc.’s AAPL forecast cuts following the company’s fourth-quarter results, “Mad Money” host Jim Cramer cautions that “the stock should never have been up that much,” while Dan Ives defends the company’s strong iPhone 16 launch.

What Happened: On Thursday, Cramer took to X, formerly Twitter, and suggested that Apple’s lowered financial forecast, indicating a slowdown, has now been “absorbed” by the market, which he thinks brings down overhyped expectations to a more “reasonable” level

Cramer also implied Apple hasn’t faced as much criticism for spending on AI compared to other tech giants, possibly because investors don’t think Apple’s AI efforts are as significant or game-changing.

“Oh and, tell me, please, who was surprised by the forecast guidedown? The stock should never have been up that much…,” he stated.

Contrarily, Wedbush analyst Ives defended Apple’s fourth-quarter performance. He lauded the successful launch of iPhone 16 and forecasted a robust December quarter for the company, propelled by the rollout of Apple Intelligence.

Ives also conveyed his conviction that the strong performance will persist throughout the rest of the fiscal year 2025, despite a lower guide delta for wearables, Mac, and iPad.

Why It Matters: Apple announced fiscal fourth-quarter revenue of $94.9 billion, surpassing analyst predictions of $94.56 billion. The company also reported adjusted earnings of $1.64 per share for the quarter, exceeding expectations of $1.60 per share.

This marks the seventh consecutive quarter that Apple has exceeded analyst forecasts for both revenue and earnings, according to Benzinga Pro.

During the earnings call on Thursday, Apple CEO Tim Cook said that the adoption rate of iOS 18.1 has doubled that of its predecessor, iOS 17.1, indicating a strong demand for the new iPhone 16.

However, previously it was reported that Apple had to resort to aggressive pricing strategies, including discounts on Alibaba’s Tmall, to counter the initial lukewarm response to the iPhone 16 in China.

Price Action: Apple’s stock fell 1.8% on Thursday to close at $225.91, and fell over 1.2% in premarket trading on Friday. Year-to-date, Apple’s shares are up 21.7%, according to Benzinga Pro data.

Read Next:

Disclaimer: This content was partially produced with the help of Benzinga Neuro and was reviewed and published by Benzinga editors.

Photo courtesy: Apple

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Boeing Sweetens Deal With 38% Wage Hike, $12K Bonus And More To End 7-Week Strike: Vote Set For Monday

Striking employees at Boeing Co. BA are poised to vote on a new contract proposal on Monday. The proposal, which includes a 38% wage increase over four years and a larger signing bonus, has received backing from the workers’ union.

What Happened: The International Association of Machinists and Aerospace Workers (IAM) stated that they have negotiated the best possible terms with Boeing. Previously, union members had turned down two offers from the company.

Reuters reported on Friday that this new offer comes as Boeing attempts to stabilize its finances amid a seven-week strike involving over 33,000 factory workers on the U.S. West Coast. The strike has significantly affected Boeing’s cash flow and halted production of key aircraft models.

Acting U.S. Secretary of Labor Julie Su facilitated recent negotiations, lauding both parties for their efforts. President Joe Biden also praised the union and Boeing for reaching a new contract proposal, highlighting the sacrifices made by Boeing’s machinists.

See Also: Cathie Wood Shuffles Her Tech Deck: Continues Dumping Tesla And Palantir, Stocks Up On AMD And Meta

Boeing’s latest offer includes a $12,000 ratification bonus, integrating previous bonuses into workers’ 401(k) retirement accounts. Despite the improved terms, approval remains uncertain as some workers express dissatisfaction due to the absence of a defined-benefit pension.

Why It Matters: The ongoing strike has already cost Boeing an estimated $2 billion over the last five weeks. The machinists’ rejection of previous offers has added further uncertainty to Boeing’s financial recovery efforts.

In a bid to bolster its finances, Boeing recently expanded its stock offering, aiming for a $20.7 billion windfall. The company priced its public offerings at 112.5 million shares of common stock at $143.00 each.

Price Action: Boeing saw its stock climb higher by 2.77% during the after-hours market after it closed at $149.31 on Thursday, according to Benzinga Pro.

Read Next:

Image via Shutterstock

This story was generated using Benzinga Neuro and edited by Pooja Rajkumari

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

RE/MAX HOLDINGS, INC. REPORTS THIRD QUARTER 2024 RESULTS

Total Revenue of $78.5 Million, Adjusted EBITDA of $27.3 Million

DENVER, Oct. 31, 2024 /PRNewswire/ —

![]()

Third Quarter 2024 Highlights

(Compared to third quarter 2023 unless otherwise noted)

- Total Revenue decreased 3.4% to $78.5 million

- Revenue excluding the Marketing Funds1 decreased 3.3% to $58.4 million, driven by negative 3.0% organic growth2 and 0.3% adverse foreign currency movements

- Net income attributable to RE/MAX Holdings, Inc. of $1.0 million and earnings per diluted share (GAAP EPS) of $0.05

- Adjusted EBITDA3 increased 2.0% to $27.3 million, Adjusted EBITDA margin3 of 34.8% and Adjusted earnings per diluted share (Adjusted EPS3) of $0.38

- Total agent count increased 174 agents, or 0.1%, to 145,483 agents

- U.S. and Canada combined agent count decreased 4.4% to 78,201 agents

- Total open Motto Mortgage franchises decreased 3.3% to 234 offices4

RE/MAX Holdings, Inc. (the “Company” or “RE/MAX Holdings”) RMAX, parent company of RE/MAX, one of the world’s leading franchisors of real estate brokerage services, and Motto Mortgage (“Motto”), the first and only national mortgage brokerage franchise brand in the U.S., today announced operating results for the quarter ended September 30, 2024.

“We continue to drive operational efficiency across the enterprise, which helped generate better-than-forecasted third-quarter financial results,” said Erik Carlson, RE/MAX Holdings Chief Executive Officer. “Our team is developing new revenue opportunities while working to run our core business better each day. That effort has contributed to our strong margin performance the past two quarters, which is an encouraging trend.”

Carlson continued: “Business optimization, having a growth mindset, and delivering the absolute best customer experience possible are the cornerstones of our playbook. We are making measurable progress on each of these. With increasing optimism about the trajectory of future interest rates, our growing global agent count, and our bold new initiatives – including providing innovative and enhanced technology products to our RE/MAX affiliates, improving the agent-customer experience by cultivating leads, and starting to monetize our digital assets – we are well-positioned to finish the year with positive momentum.”

Third Quarter 2024 Operating Results

Agent Count

The following table compares agent count as of September 30, 2024 and 2023:

|

As of September 30, |

Change |

||||||||

|

2024 |

2023 |

# |

% |

||||||

|

U.S. |

52,808 |

56,494 |

(3,686) |

(6.5) |

|||||

|

Canada |

25,393 |

25,288 |

105 |

0.4 |

|||||

|

Subtotal |

78,201 |

81,782 |

(3,581) |

(4.4) |

|||||

|

Outside the U.S. & Canada |

67,282 |

63,527 |

3,755 |

5.9 |

|||||

|

Total |

145,483 |

145,309 |

174 |

0.1 |

|||||

Revenue

RE/MAX Holdings generated revenue of $78.5 million in the third quarter of 2024, a decrease of $2.7 million, or 3.4%, compared to $81.2 million in the third quarter of 2023. Revenue excluding the Marketing Funds was $58.4 million in the third quarter of 2024, a decrease of $2.0 million, or 3.3%, versus the same period in 2023. The decrease in Revenue excluding the Marketing Funds was attributable to negative organic revenue growth of 3.0% and adverse foreign currency movements of 0.3%. Negative organic revenue growth was principally driven by a decrease in U.S. agent count and a reduction in revenue from previous acquisitions, partially offset by an increase in Broker fee revenue.

Recurring revenue streams, which consist of continuing franchise fees and annual dues, decreased $1.5 million, or 3.8%, compared to the third quarter of 2023 and accounted for 66.4% of Revenue excluding the Marketing Funds in the third quarter of 2024 compared to 66.7% of Revenue excluding the Marketing Funds in the prior-year period.

Operating Expenses

Total operating expenses were $63.3 million for the third quarter of 2024, a decrease of $39.0 million, or 38.1%, compared to $102.2 million in the third quarter of 2023. During the third quarter of 2023, the Company agreed to pay $55.0 million to settle various industry class-action lawsuits, which was recorded in the third quarter of 2023. A $24.9 million gain on reduction in tax receivable agreement liability was also recorded in the third quarter of 2023.

Selling, operating and administrative expenses were $35.9 million in the third quarter of 2024, a decrease of $7.2 million, or 16.6%, compared to the third quarter of 2023 and represented 61.5% of Revenue excluding the Marketing Funds, compared to 71.4% in the prior-year period. Third quarter 2024 selling, operating and administrative expenses decreased primarily due to lower personnel costs and a decrease in bad debt, legal, and other technology expenses.

Net Income (Loss) and GAAP EPS

Net income attributable to RE/MAX Holdings was $1.0 million for the third quarter of 2024 compared to net loss of ($59.5) million for the third quarter of 2023. Reported basic and diluted GAAP earnings per share were $0.05 each for the third quarter of 2024 compared to basic and diluted GAAP loss per share of ($3.28) each in the third quarter of 2023.

Adjusted EBITDA and Adjusted EPS

Adjusted EBITDA was $27.3 million for the third quarter of 2024, an increase of $0.5 million, or 2.0%, compared to the third quarter of 2023. Third quarter 2024 Adjusted EBITDA increased primarily due to a decrease in bad debt, legal, personnel, and other technology expenses, partially offset by a decrease in U.S. agent count. Adjusted EBITDA margin was 34.8% in the third quarter of 2024, compared to 32.9% in the third quarter of 2023.

Adjusted basic and diluted EPS were $0.39 and $0.38, respectively, for the third quarter of 2024 compared to Adjusted basic and diluted EPS of $0.40 each for the third quarter of 2023. The ownership structure used to calculate Adjusted basic and diluted EPS for the quarter ended September 30, 2024, assumes RE/MAX Holdings owned 100% of RMCO, LLC (“RMCO”). The weighted average ownership RE/MAX Holdings had in RMCO was 60.0% for the quarter ended September 30, 2024.

Balance Sheet

As of September 30, 2024, the Company had cash and cash equivalents of $83.8 million, an increase of $1.2 million from December 31, 2023. As of September 30, 2024, the Company had $441.8 million of outstanding debt, net of an unamortized debt discount and issuance costs, compared to $444.6 million as of December 31, 2023.

Share Repurchases and Retirement

As previously disclosed, in January 2022 the Company’s Board of Directors authorized a common stock repurchase program of up to $100 million. During the three months ended September 30, 2024, the Company did not repurchase any shares. As of September 30, 2024, $62.5 million remained available under the share repurchase program.

Impact of Hurricanes Helene and Milton

Several of the Company’s affiliates were impacted by the recent hurricanes. While the extent of the hurricanes’ full impact on the Company’s networks is not entirely known at this time, the Company currently estimates that its fourth quarter revenue will be lower than previously expected as financial support is provided to affected affiliates for a limited time. As a result, the Company’s fourth quarter and full year revenue (below) was reduced by approximately $1.0 million to $1.5 million, of which approximately 40% relates to the Marketing Funds, to reflect expected foregone revenue in the form of fee waivers provided to affiliates impacted by these storms.

Outlook

The Company’s fourth quarter and full year 2024 Outlook includes the impact of the fee waivers to hurricane-impacted affiliates and assumes no further currency movements, acquisitions, or divestitures.

For the fourth quarter of 2024, RE/MAX Holdings expects:

- Agent count to change 0.0% to 1.0% over fourth quarter 2023;

- Revenue in a range of $71.0 million to $76.0 million (including revenue from the Marketing Funds in a range of $18.5 million to $20.5 million); and

- Adjusted EBITDA in a range of $20.5 million to $23.5 million.

For the full year 2024, the Company now expects:

- Agent count to change 0.0% to 1.0% over full year 2023, changed from negative 1.0% to positive 1.0%;

- Revenue in a range of $306.0 million to $311.0 million (including revenue from the Marketing Funds in a range of $78.5 million to $80.5 million), changed from $305.0 million to $315.0 million (including revenue from the Marketing Funds in a range of $78.0 million to $82.0 million); and

- Adjusted EBITDA in a range of $95.0 million to $98.0 million, changed from $93.0 million to $98.0 million.

Webcast and Conference Call

The Company will host a conference call for interested parties on Friday, November 1, 2024, beginning at 8:30 a.m. Eastern Time. Interested parties can register in advance for the conference call using the link below:

https://registrations.events/direct/Q4I941153

Interested parties also can access a live webcast through the Investor Relations section of the Company’s website at http://investors.remaxholdings.com. Please dial-in or join the webcast 10 minutes before the start of the conference call. An archive of the webcast will be available on the Company’s website for a limited time as well.

Basis of Presentation

Unless otherwise noted, the results presented in this press release are consolidated and exclude adjustments attributable to the non-controlling interest.

Footnotes:

1Revenue excluding the Marketing Funds is a non-GAAP measure of financial performance that differs from U.S. Generally Accepted Accounting Principles (“U.S. GAAP”) and a reconciliation to the most directly comparable U.S. GAAP measure is as follows (in thousands):

|

Three Months Ended |

Nine Months Ended |

|||||||||||

|

September 30, |

September 30, |

|||||||||||

|

2024 |

2023 |

2024 |

2023 |

|||||||||

|

Revenue excluding the Marketing Funds: |

||||||||||||

|

Total revenue |

$ |

78,478 |

$ |

81,223 |

$ |

235,218 |

$ |

249,071 |

||||

|

Less: Marketing Funds fees |

20,098 |

20,853 |

60,331 |

63,272 |

||||||||

|

Revenue excluding the Marketing Funds |

$ |

58,380 |

$ |

60,370 |

$ |

174,887 |

$ |

185,799 |

||||

2The Company defines organic revenue growth as revenue growth from continuing operations excluding (i) revenue from Marketing Funds, (ii) revenue from acquisitions, and (iii) the impact of foreign currency movements. The Company defines revenue from acquisitions as the revenue generated from the date of an acquisition to its first anniversary (excluding Marketing Funds revenue related to acquisitions where applicable).

3Adjusted EBITDA, Adjusted EBITDA margin and Adjusted EPS are non-GAAP measures. These terms are defined at the end of this release. Please see Tables 5 and 6 appearing later in this release for reconciliations of these non-GAAP measures to the most directly comparable GAAP measures.

4Total open Motto Mortgage franchises includes only “bricks and mortar” offices with a unique physical address with rights granted by a full franchise agreement with Motto Franchising, LLC and excludes any “virtual” offices or BranchiseSM offices.

# # #

About RE/MAX Holdings, Inc.

RE/MAX Holdings, Inc. RMAX is one of the world’s leading franchisors in the real estate industry, franchising real estate brokerages globally under the RE/MAX® brand, and mortgage brokerages within the U.S. under the Motto® Mortgage brand. RE/MAX was founded in 1973 by Dave and Gail Liniger, with an innovative, entrepreneurial culture affording its agents and franchisees the flexibility to operate their businesses with great independence. Now with more than 140,000 agents in nearly 9,000 offices and a presence in more than 110 countries and territories, nobody in the world sells more real estate than RE/MAX, as measured by total residential transaction sides. Dedicated to innovation and change in the real estate industry, RE/MAX launched Motto Franchising, LLC, a ground-breaking mortgage brokerage franchisor, in 2016. Motto Mortgage, the first and only national mortgage brokerage franchise brand in the U.S., has grown to over 225 offices across more than 40 states.

Forward-Looking Statements

This press release includes “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements are often identified by the use of words such as “believe,” “intend,” “expect,” “estimate,” “plan,” “outlook,” “project,” “anticipate,” “may,” “will,” “would” and other similar words and expressions that predict or indicate future events or trends that are not statements of historical matters. Forward-looking statements include statements related to agent count; Motto open offices; franchise sales; revenue; operating expenses and cost management; the Company’s outlook for the fourth quarter and full year 2024; non-GAAP financial measures; housing and mortgage market conditions; interest rates; the amount of fee waivers to affiliates affected by recent hurricanes and the impact of such fee waivers on our fourth quarter and full year 2024 outlook; operational efficiencies; business optimization and delivering the absolute best customer experience; development of new revenue opportunities; our strong margin performance being an encouraging trend; increasing optimism about future interest rates; our growing global agent count and our bold new initiatives, including enhanced technology, improved customer experience with leads, and monetizing our digital assets; and being well positioned to finish the year with positive momentum. Forward-looking statements should not be read as a guarantee of future performance or results and will not necessarily accurately indicate the times at which such performance or results may be achieved. Forward-looking statements are based on information available at the time those statements are made and/or management’s good faith belief as of that time with respect to future events and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. These risks and uncertainties include, without limitation, (1) changes in the real estate market or interest rates and availability of financing, (2) changes in business and economic activity in general, (3) the Company’s ability to attract and retain quality franchisees, (4) the Company’s franchisees’ ability to recruit and retain real estate agents and mortgage loan originators, (5) changes in laws and regulations, (6) the Company’s ability to enhance, market, and protect its brands, (7) the Company’s ability to implement its technology initiatives, (8) risks related to the Company’s leadership transition, (9) fluctuations in foreign currency exchange rates, (10) the nature and amount of the exclusion of charges in future periods when determining Adjusted EBITDA is subject to uncertainty and may not be similar to such charges in prior periods, and (11) those risks and uncertainties described in the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in the most recent Annual Report on Form 10-K and Quarterly Reports on Form 10-Q filed with the Securities and Exchange Commission (“SEC”) and similar disclosures in subsequent periodic and current reports filed with the SEC, which are available on the investor relations page of the Company’s website at www.remaxholdings.com and on the SEC website at www.sec.gov. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date on which they are made. Except as required by law, the Company does not intend, and undertakes no obligation, to update this information to reflect future events or circumstances.

|

TABLE 1 |

||||||||||||

|

RE/MAX Holdings, Inc. |

||||||||||||

|

Consolidated Statements of Income (Loss) |

||||||||||||

|

(In thousands, except share and per share amounts) |

||||||||||||

|

(Unaudited) |

||||||||||||

|

Three Months Ended |

Nine Months Ended |

|||||||||||

|

September 30, |

September 30, |

|||||||||||

|

2024 |

2023 |

2024 |

2023 |

|||||||||

|

Revenue: |

||||||||||||

|

Continuing franchise fees |

$ |

30,798 |

$ |

31,834 |

$ |

92,223 |

$ |

96,011 |

||||

|

Annual dues |

7,969 |

8,456 |

24,345 |

25,661 |

||||||||

|

Broker fees |

14,915 |

14,255 |

40,159 |

39,468 |

||||||||

|

Marketing Funds fees |

20,098 |

20,853 |

60,331 |

63,272 |

||||||||

|

Franchise sales and other revenue |

4,698 |

5,825 |

18,160 |

24,659 |

||||||||

|

Total revenue |

78,478 |

81,223 |

235,218 |

249,071 |

||||||||

|

Operating expenses: |

||||||||||||

|

Selling, operating and administrative expenses |

35,932 |

43,090 |

116,488 |

132,417 |

||||||||

|

Marketing Funds expenses |

20,098 |

20,853 |

60,331 |

63,272 |

||||||||

|

Depreciation and amortization |

7,237 |

8,195 |

22,489 |

24,236 |

||||||||

|

Settlement and impairment charges |

— |

55,000 |

— |

55,000 |

||||||||

|

Gain on reduction in tax receivable agreement liability |

— |

(24,917) |

— |

(24,917) |

||||||||

|

Total operating expenses |

63,267 |

102,221 |

199,308 |

250,008 |

||||||||

|

Operating income (loss) |

15,211 |

(20,998) |

35,910 |

(937) |

||||||||

|

Other expenses, net: |

||||||||||||

|

Interest expense |

(9,249) |

(9,292) |

(27,696) |

(26,377) |

||||||||

|

Interest income |

885 |

1,173 |

2,835 |

3,318 |

||||||||

|

Foreign currency transaction gains (losses) |

74 |

125 |

(568) |

383 |

||||||||

|

Total other expenses, net |

(8,290) |

(7,994) |

(25,429) |

(22,676) |

||||||||

|

Income (loss) before provision for income taxes |

6,921 |

(28,992) |

10,481 |

(23,613) |

||||||||

|

Provision for income taxes |

(3,507) |

(53,680) |

(6,484) |

(56,494) |

||||||||

|

Net income (loss) |

$ |

3,414 |

$ |

(82,672) |

$ |

3,997 |

$ |

(80,107) |

||||

|

Less: net income (loss) attributable to non-controlling interest |

2,448 |

(23,218) |

2,679 |

(21,992) |

||||||||

|

Net income (loss) attributable to RE/MAX Holdings, Inc. |

$ |

966 |

$ |

(59,454) |

$ |

1,318 |

$ |

(58,115) |

||||

|

Net income (loss) attributable to RE/MAX Holdings, Inc. per share |

||||||||||||

|

Basic |

$ |

0.05 |

$ |

(3.28) |

$ |

0.07 |

$ |

(3.22) |

||||

|

Diluted |

$ |

0.05 |

$ |

(3.28) |

$ |

0.07 |

$ |

(3.22) |

||||

|

Weighted average shares of Class A common stock outstanding |

||||||||||||

|

Basic |

18,863,793 |

18,150,557 |

18,733,190 |

18,064,009 |

||||||||

|

Diluted |

19,483,798 |

18,150,557 |

19,063,279 |

18,064,009 |

||||||||

|

Cash dividends declared per share of Class A common stock |

$ |

— |

$ |

0.23 |

$ |

— |

$ |

0.69 |

||||

|

TABLE 2 |

||||||

|

RE/MAX Holdings, Inc. |

||||||

|

Consolidated Balance Sheets |

||||||

|

(In thousands, except share and per share amounts) |

||||||

|

(Unaudited) |

||||||

|

As of |

||||||

|

September 30, |

December 31, |

|||||

|

2024 |

2023 |

|||||

|

Assets |

||||||

|

Current assets: |

||||||

|

Cash and cash equivalents |

$ |

83,779 |

$ |

82,623 |

||

|

Restricted cash |

72,599 |

43,140 |

||||

|

Accounts and notes receivable, current portion, net of allowances |

30,598 |

33,427 |

||||

|

Income taxes receivable |

1,693 |

1,706 |

||||

|

Other current assets |

13,224 |

15,669 |

||||

|

Total current assets |

201,893 |

176,565 |

||||

|

Property and equipment, net of accumulated depreciation |

8,295 |

8,633 |

||||

|

Operating lease right of use assets |

19,209 |

23,013 |

||||

|

Franchise agreements, net |

87,346 |

101,516 |

||||

|

Other intangible assets, net |

15,297 |

19,176 |

||||

|

Goodwill |

240,102 |

241,164 |

||||

|

Other assets, net of current portion |

6,507 |

7,083 |

||||

|

Total assets |

$ |

578,649 |

$ |

577,150 |

||

|

Liabilities and stockholders’ equity (deficit) |

||||||

|

Current liabilities: |

||||||

|

Accounts payable |

$ |

5,347 |

$ |

4,700 |

||

|

Accrued liabilities |

105,132 |

107,434 |

||||

|

Income taxes payable |

1,274 |

766 |

||||

|

Deferred revenue |

22,625 |

23,077 |

||||

|

Current portion of debt |

4,600 |

4,600 |

||||

|

Current portion of payable pursuant to tax receivable agreements |

285 |

822 |

||||

|

Operating lease liabilities |

8,437 |

7,920 |

||||

|

Total current liabilities |

147,700 |

149,319 |

||||

|

Debt, net of current portion |

437,176 |

439,980 |

||||

|

Deferred tax liabilities |

11,281 |

10,797 |

||||

|

Deferred revenue, net of current portion |

15,482 |

17,607 |

||||

|

Operating lease liabilities, net of current portion |

25,044 |

31,479 |

||||

|

Other liabilities, net of current portion |

3,729 |

4,029 |

||||

|

Total liabilities |

640,412 |

653,211 |

||||

|

Commitments and contingencies |

||||||

|

Stockholders’ equity (deficit): |

||||||

|

Class A common stock, par value $.0001 per share, 180,000,000 shares authorized; 18,872,052 |

2 |

2 |

||||

|

Class B common stock, par value $.0001 per share, 1,000 shares authorized; 1 share issued |

— |

— |

||||

|

Additional paid-in capital |

562,594 |

550,637 |

||||

|

Accumulated deficit |

(139,524) |

(140,217) |

||||

|

Accumulated other comprehensive income (deficit), net of tax |

35 |

638 |

||||

|

Total stockholders’ equity attributable to RE/MAX Holdings, Inc. |

423,107 |

411,060 |

||||

|

Non-controlling interest |

(484,870) |

(487,121) |

||||

|

Total stockholders’ equity (deficit) |

(61,763) |

(76,061) |

||||

|

Total liabilities and stockholders’ equity (deficit) |

$ |

578,649 |

$ |

577,150 |

||

|

TABLE 3 |

||||||

|

RE/MAX Holdings, Inc. |

||||||

|

Consolidated Statements of Cash Flows |

||||||

|

(In thousands) |

||||||

|

(Unaudited) |

||||||

|

Nine Months Ended |

||||||

|

September 30, |

||||||

|

2024 |

2023 |

|||||

|

Cash flows from operating activities: |

||||||

|

Net income (loss) |

$ |

3,997 |

$ |

(80,107) |

||

|

Adjustments to reconcile net income (loss) to net cash provided by operating activities: |

||||||

|

Depreciation and amortization |

22,489 |

24,236 |

||||

|

Equity-based compensation expense |

14,443 |

14,050 |

||||

|

Bad debt expense |

1,039 |

4,903 |

||||

|

Deferred income tax expense (benefit) |

434 |

51,799 |

||||

|

Fair value adjustments to contingent consideration |

(300) |

(379) |

||||

|

Settlement payment, net |

— |

55,000 |

||||

|

Loss (gain) on sale or disposition of assets, net |

160 |

386 |

||||

|

Non-cash lease benefit |

(2,110) |

(2,242) |

||||

|

Non-cash debt charges |

646 |

644 |

||||

|

Payment of contingent consideration in excess of acquisition date fair value |

(360) |

— |

||||

|

Gain on reduction in tax receivable agreement liability |

— |

(24,917) |

||||

|

Other, net |

53 |

(73) |

||||

|

Changes in operating assets and liabilities |

2,376 |

(23,675) |

||||

|

Net cash provided by operating activities |

42,867 |

19,625 |

||||

|

Cash flows from investing activities: |

||||||

|

Purchases of property, equipment and capitalization of software |

(5,821) |

(4,249) |

||||

|

Other |

698 |

679 |

||||

|

Net cash used in investing activities |

(5,123) |

(3,570) |

||||

|

Cash flows from financing activities: |

||||||

|

Payments on debt |

(3,450) |

(3,450) |

||||

|

Distributions paid to non-controlling unitholders |

— |

(8,667) |

||||

|

Dividends and dividend equivalents paid to Class A common stockholders |

(591) |

(13,492) |

||||

|

Payments related to tax withholding for share-based compensation |

(2,548) |

(4,014) |

||||

|

Common shares repurchased |

— |

(3,408) |

||||

|

Payment of contingent consideration |

— |

(360) |

||||

|

Other financing |

(21) |

— |

||||

|

Net cash used in financing activities |

(6,610) |

(33,391) |

||||

|

Effect of exchange rate changes on cash |

(519) |

21 |

||||

|

Net increase (decrease) in cash, cash equivalents and restricted cash |

30,615 |

(17,315) |

||||

|

Cash, cash equivalents and restricted cash, beginning of period |

125,763 |

138,128 |

||||

|

Cash, cash equivalents and restricted cash, end of period |

$ |

156,378 |

$ |

120,813 |

||

|

TABLE 4 |

||||||||||||||||||

|

RE/MAX Holdings, Inc. |

||||||||||||||||||

|

Agent Count |

||||||||||||||||||

|

(Unaudited) |

||||||||||||||||||

|

As of |

||||||||||||||||||

|

September 30, |

June 30, |

March 31, |

December 31, |

September 30, |

June 30, |

March 31, |

December 31, |

September 30, |

||||||||||

|

2024 |

2024 |

2024 |

2023 |

2023 |

2023 |

2023 |

2022 |

2022 |

||||||||||

|

Agent Count: |

||||||||||||||||||

|

U.S. |

||||||||||||||||||

|

Company-Owned Regions |

46,283 |

46,780 |

47,302 |

48,401 |

49,576 |

50,011 |

50,340 |

51,491 |

52,804 |

|||||||||

|

Independent Regions |

6,525 |

6,626 |

6,617 |

6,730 |

6,918 |

6,976 |

7,110 |

7,228 |

7,311 |

|||||||||

|

U.S. Total |

52,808 |

53,406 |

53,919 |

55,131 |

56,494 |

56,987 |

57,450 |

58,719 |

60,115 |

|||||||||

|

Canada |

||||||||||||||||||

|

Company-Owned Regions |

20,515 |

20,347 |

20,151 |

20,270 |

20,389 |

20,354 |

20,172 |

20,228 |

20,174 |

|||||||||

|

Independent Regions |

4,878 |

4,846 |

4,885 |

4,898 |

4,899 |

4,864 |

4,899 |

4,892 |

4,844 |

|||||||||

|

Canada Total |

25,393 |

25,193 |

25,036 |

25,168 |

25,288 |

25,218 |

25,071 |

25,120 |

25,018 |

|||||||||

|

U.S. and Canada Total |

78,201 |

78,599 |

78,955 |

80,299 |

81,782 |

82,205 |

82,521 |

83,839 |

85,133 |

|||||||||

|

Outside U.S. and Canada |

||||||||||||||||||

|

Independent Regions |

67,282 |

64,943 |

64,332 |

64,536 |

63,527 |

62,305 |

61,002 |

60,175 |

59,167 |

|||||||||

|

Outside U.S. and Canada Total |

67,282 |

64,943 |

64,332 |

64,536 |

63,527 |

62,305 |

61,002 |

60,175 |

59,167 |

|||||||||

|

Total |

145,483 |

143,542 |

143,287 |

144,835 |

145,309 |

144,510 |

143,523 |

144,014 |

144,300 |

|||||||||

|

TABLE 5 |

|||||||||||||

|

RE/MAX Holdings, Inc. |

|||||||||||||

|

Adjusted EBITDA Reconciliation to Net Income (Loss) |

|||||||||||||

|

(In thousands, except percentages) |

|||||||||||||

|

(Unaudited) |

|||||||||||||

|

Three Months Ended |

Nine Months Ended |

||||||||||||

|

September 30, |

September 30, |

||||||||||||

|

2024 |

2023 |

2024 |

2023 |

||||||||||

|

Net income (loss) |

$ |

3,414 |

$ |

(82,672) |

$ |

3,997 |

$ |

(80,107) |

|||||

|

Depreciation and amortization |

7,237 |

8,195 |

22,489 |

24,236 |

|||||||||

|

Interest expense |

9,249 |

9,292 |

27,696 |

26,377 |

|||||||||

|

Interest income |

(885) |

(1,173) |

(2,835) |

(3,318) |

|||||||||

|

Provision for income taxes |

3,507 |

53,680 |

6,484 |

56,494 |

|||||||||

|

EBITDA |

22,522 |

(12,678) |

57,831 |

23,682 |

|||||||||

|

Settlement charge (1) |

— |

55,000 |

— |

55,000 |

|||||||||

|

Equity-based compensation expense |

4,618 |

4,891 |

14,443 |

14,050 |

|||||||||

|

Acquisition-related expense (2) |

— |

59 |

— |

160 |

|||||||||

|

Fair value adjustments to contingent consideration (3) |

(437) |

(280) |

(300) |

(379) |

|||||||||

|

Restructuring charges (4) |

(18) |

4,278 |

(59) |

4,245 |

|||||||||

|

Gain on reduction in tax receivable agreement liability (5) |

— |

(24,917) |

— |

(24,917) |

|||||||||

|

Other (6) |

605 |

395 |

2,444 |

1,471 |

|||||||||

|

Adjusted EBITDA (7) |

$ |

27,290 |

$ |

26,748 |

$ |

74,359 |

$ |

73,312 |

|||||

|

Adjusted EBITDA Margin (7) |

34.8 |

% |

32.9 |

% |

31.6 |

% |

29.4 |

% |

|||||

|

(1) |

Represents the settlement of industry class-action lawsuits. |

|

(2) |

Acquisition-related expense includes personnel, legal, accounting, advisory and consulting fees incurred in connection with acquisition activities and integration of acquired companies. |

|

(3) |

Fair value adjustments to contingent consideration include amounts recognized for changes in the estimated fair value of the contingent consideration liabilities. |

|

(4) |

During the third quarter of 2023, the Company announced a reduction in force and reorganization intended to streamline the Company’s operations and yield cost savings over the long term. |

|

(5) |

Gain on reduction in tax receivable agreement liability is a result of a valuation allowance on deferred tax assets recorded during the third quarter of 2023. |

|

(6) |

Other is primarily made up of employee retention related expenses from the Company’s CEO transition. |

|

(7) |

Non-GAAP measure. See the end of this press release for definitions of non-GAAP measures. |

|

TABLE 6 |

||||||||||||

|

RE/MAX Holdings, Inc. |

||||||||||||

|

Adjusted Net Income (Loss) and Adjusted Earnings per Share |

||||||||||||

|

(In thousands, except share and per share amounts) |

||||||||||||

|

(Unaudited) |

||||||||||||

|

Three Months Ended |

Nine Months Ended |

|||||||||||

|

September 30, |

September 30, |

|||||||||||

|

2024 |

2023 |

2024 |

2023 |

|||||||||

|

Net income (loss) |

$ |

3,414 |

$ |

(82,672) |

$ |

3,997 |

$ |

(80,107) |

||||

|

Amortization of acquired intangible assets |

4,672 |

5,768 |

15,085 |

17,299 |

||||||||

|

Provision for income taxes |

3,507 |

53,680 |

6,484 |

56,494 |

||||||||

|

Add-backs: |

||||||||||||

|

Settlement charge (1) |

— |

55,000 |

— |

55,000 |

||||||||

|

Equity-based compensation expense |

4,618 |

4,891 |

14,443 |

14,050 |

||||||||

|

Acquisition-related expense (2) |

— |

59 |

— |

160 |

||||||||

|

Fair value adjustments to contingent consideration (3) |

(437) |

(280) |

(300) |

(379) |

||||||||

|

Restructuring charges (4) |

(18) |

4,278 |

(59) |

4,245 |

||||||||

|

Gain on reduction in tax receivable agreement liability (5) |

— |

(24,917) |

— |

(24,917) |

||||||||

|

Other (6) |

605 |

395 |

2,444 |

1,471 |

||||||||

|

Adjusted pre-tax net income |

16,361 |

16,202 |

42,094 |

43,316 |

||||||||

|

Less: Provision for income taxes at 25% (7) |

(4,091) |

(4,051) |

(10,524) |

(10,829) |

||||||||

|

Adjusted net income (8) |

$ |

12,270 |

$ |

12,151 |

$ |

31,570 |

$ |

32,487 |

||||

|

Total basic pro forma shares outstanding |

31,423,393 |

30,710,157 |

31,292,790 |

30,623,609 |

||||||||

|

Total diluted pro forma shares outstanding |

32,043,398 |

30,710,157 |

31,622,879 |

30,623,609 |

||||||||

|

Adjusted net income basic earnings per share (8) |

$ |

0.39 |

$ |

0.40 |

$ |

1.01 |

$ |

1.06 |

||||

|

Adjusted net income diluted earnings per share (8) |

$ |

0.38 |

$ |

0.40 |

$ |

1.00 |

$ |

1.06 |

||||

|

(1) |

Represents the settlement of industry class-action lawsuits. |

|

(2) |

Acquisition-related expense includes personnel, legal, accounting, advisory and consulting fees incurred in connection with acquisition activities and integration of acquired companies. |

|

(3) |

Fair value adjustments to contingent consideration include amounts recognized for changes in the estimated fair value of the contingent consideration liabilities. |

|

(4) |

During the third quarter of 2023, the Company announced a reduction in force and reorganization intended to streamline the Company’s operations and yield cost savings over the long term. |

|

(5) |

Gain on reduction in tax receivable agreement liability is a result of a valuation allowance on deferred tax assets recorded during the third quarter of 2023. |

|

(6) |

Other is primarily made up of employee retention related expenses from the Company’s CEO transition. |

|

(7) |

The long-term tax rate assumes the exchange of all outstanding non-controlling interest partnership units for Class A Common Stock that (a) removes the impact of unusual, non-recurring tax matters and (b) does not estimate the residual impacts to foreign taxes of additional step-ups in tax basis from an exchange because that is dependent on stock prices at the time of such exchange and the calculation is impracticable. |

|

(8) |

Non-GAAP measure. See the end of this press release for definitions of non-GAAP measures. |

|

TABLE 7 |

||||||||

|

RE/MAX Holdings, Inc. |

||||||||

|

Pro Forma Shares Outstanding |

||||||||

|

(Unaudited) |

||||||||

|

Three Months Ended |

Nine Months Ended |

|||||||

|

September 30, |

September 30, |

|||||||

|

2024 |

2023 |

2024 |

2023 |

|||||

|

Total basic weighted average shares outstanding: |

||||||||

|

Weighted average shares of Class A common stock outstanding |

18,863,793 |

18,150,557 |

18,733,190 |

18,064,009 |

||||

|

Remaining equivalent weighted average shares of stock |

12,559,600 |

12,559,600 |

12,559,600 |

12,559,600 |

||||

|

Total basic pro forma weighted average shares outstanding |

31,423,393 |

30,710,157 |

31,292,790 |

30,623,609 |

||||

|

Total diluted weighted average shares outstanding: |

||||||||

|

Weighted average shares of Class A common stock outstanding |

18,863,793 |

18,150,557 |

18,733,190 |

18,064,009 |

||||

|

Remaining equivalent weighted average shares of stock |

12,559,600 |

12,559,600 |

12,559,600 |

12,559,600 |

||||

|

Dilutive effect of unvested restricted stock units (1) |

620,005 |

— |

330,089 |

— |

||||

|

Total diluted pro forma weighted average shares outstanding |

32,043,398 |

30,710,157 |

31,622,879 |

30,623,609 |

||||

|

(1) |

In accordance with the treasury stock method. |

|

TABLE 8 |

||||||

|

RE/MAX Holdings, Inc. |

||||||

|

Adjusted Free Cash Flow & Unencumbered Cash |

||||||

|

(Unaudited) |

||||||

|

Nine Months Ended |

||||||

|

September 30, |

||||||

|

2024 |

2023 |

|||||

|

Cash flow from operations |

$ |

42,867 |

$ |

19,625 |

||

|

Less: Purchases of property, equipment and capitalization of software |

(5,821) |

(4,249) |

||||

|

(Increases) decreases in restricted cash of the Marketing Funds (1) |

(1,959) |

12,222 |

||||

|

Adjusted free cash flow (2) |

35,087 |

27,598 |

||||

|

Adjusted free cash flow (2) |

35,087 |

27,598 |

||||

|

Less: Tax/Other non-dividend distributions to RIHI |

— |

— |

||||

|

Adjusted free cash flow after tax/non-dividend distributions to RIHI (2) |

35,087 |

27,598 |

||||

|

Adjusted free cash flow after tax/non-dividend distributions to RIHI (2) |

35,087 |

27,598 |

||||

|

Less: Debt principal payments |

(3,450) |

(3,450) |

||||

|

Unencumbered cash generated (2) |

$ |

31,637 |

$ |

24,148 |

||

|

Summary |

||||||

|

Cash flow from operations |

$ |

42,867 |

$ |

19,625 |

||

|

Adjusted free cash flow (2) |

$ |

35,087 |

$ |

27,598 |

||

|

Adjusted free cash flow after tax/non-dividend distributions to RIHI (2) |

$ |

35,087 |

$ |

27,598 |

||

|

Unencumbered cash generated (2) |

$ |

31,637 |

$ |

24,148 |

||

|

Adjusted EBITDA (2) |

$ |

74,359 |

$ |

73,312 |

||

|

Adjusted free cash flow as % of Adjusted EBITDA (2) |

47.2 % |

37.6 % |

||||

|

Adjusted free cash flow less distributions to RIHI as % of Adjusted EBITDA (2) |

47.2 % |

37.6 % |

||||

|

Unencumbered cash generated as % of Adjusted EBITDA (2) |

42.5 % |

32.9 % |

||||

|

(1) |

This line reflects any subsequent changes in the restricted cash balance (which under GAAP reflects as either (a) an increase or decrease in cash flow from operations or (b) an incremental amount of purchases of property and equipment and capitalization of developed software) to remove the impact of changes in restricted cash in determining adjusted free cash flow. |

|

(2) |

Non-GAAP measure. See the end of this press release for definitions of non-GAAP measures. |

Non-GAAP Financial Measures

The SEC has adopted rules to regulate the use in filings with the SEC and in public disclosures of financial measures that are not in accordance with U.S. GAAP, such as revenue excluding the Marketing Funds, Adjusted EBITDA and the ratios related thereto, Adjusted net income, Adjusted basic and diluted earnings per share (Adjusted EPS) and adjusted free cash flow. These measures are derived based on methodologies other than in accordance with U.S. GAAP.

Revenue excluding the Marketing Funds is calculated directly from our consolidated financial statements as Total revenue less Marketing Funds fees.

The Company defines Adjusted EBITDA as EBITDA (consolidated net income before depreciation and amortization, interest expense, interest income and the provision for income taxes, each of which is presented in the unaudited consolidated financial statements included earlier in this press release), adjusted for the impact of the following items that are either non-cash or that the Company does not consider representative of its ongoing operating performance: loss or gain on sale or disposition of assets and sublease, settlement and impairment charges, equity-based compensation expense, acquisition-related expense, gain on reduction in tax receivable agreement liability, expense or income related to changes in the estimated fair value measurement of contingent consideration, restructuring charges and other non-recurring items. Adjusted EBITDA margin represents Adjusted EBITDA as a percentage of revenue.

Because Adjusted EBITDA and Adjusted EBITDA margin omit certain non-cash items and other non-recurring cash charges or other items, the Company believes that each measure is less susceptible to variances that affect its operating performance resulting from depreciation, amortization and other non-cash and non-recurring cash charges or other items. The Company presents Adjusted EBITDA and the related Adjusted EBITDA margin because the Company believes they are useful as supplemental measures in evaluating the performance of its operating businesses and provides greater transparency into the Company’s results of operations. The Company’s management uses Adjusted EBITDA and Adjusted EBITDA margin as factors in evaluating the performance of the business.

Adjusted EBITDA and Adjusted EBITDA margin have limitations as analytical tools, and you should not consider these measures in isolation or as a substitute for analyzing the Company’s results as reported under U.S. GAAP. Some of these limitations are:

- these measures do not reflect changes in, or cash requirements for, the Company’s working capital needs;

- these measures do not reflect the Company’s interest expense, or the cash requirements necessary to service interest or principal payments on its debt;

- these measures do not reflect the Company’s income tax expense or the cash requirements to pay its taxes;

- these measures do not reflect the cash requirements to pay dividends to stockholders of the Company’s Class A common stock and tax and other cash distributions to its non-controlling unitholders;

- these measures do not reflect the cash requirements pursuant to the tax receivable agreements;

- these measures do not reflect the cash requirements for share repurchases;

- these measures do not reflect the cash requirements for the settlement of industry class-action lawsuits and other legal settlements;

- although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often require replacement in the future, and these measures do not reflect any cash requirements for such replacements;

- although equity-based compensation is a non-cash charge, the issuance of equity-based awards may have a dilutive impact on earnings per share; and

- other companies may calculate these measures differently so similarly named measures may not be comparable.

The Company’s Adjusted EBITDA guidance does not include certain charges and costs. The adjustments to EBITDA in future periods are generally expected to be similar to the kinds of charges and costs excluded from Adjusted EBITDA in prior quarters, such as gain or loss on sale or disposition of assets and sublease, settlement and impairment charges, equity-based compensation expense, acquisition-related expense, gains or losses from changes in the tax receivable agreement liability, expense or income related to changes in the fair value measurement of contingent consideration, restructuring charges and other non-recurring items. The exclusion of these charges and costs in future periods will have a significant impact on the Company’s Adjusted EBITDA. The Company is not able to provide a reconciliation of the Company’s non-GAAP financial guidance to the corresponding U.S. GAAP measures without unreasonable effort because of the uncertainty and variability of the nature and amount of these future charges and costs.

Adjusted net income is calculated as Net income attributable to RE/MAX Holdings, assuming the full exchange of all outstanding non-controlling interests for shares of Class A common stock as of the beginning of the period (and the related increase to the provision for income taxes after such exchange), plus primarily non-cash items and other items that management does not consider to be useful in assessing the Company’s operating performance (e.g., amortization of acquired intangible assets, gain on sale or disposition of assets and sub-lease, non-cash impairment charges, acquisition-related expense, restructuring charges and equity-based compensation expense).

Adjusted basic and diluted earnings per share (Adjusted EPS) are calculated as Adjusted net income (as defined above) divided by pro forma (assuming the full exchange of all outstanding non-controlling interests) basic and diluted weighted average shares, as applicable.

When used in conjunction with GAAP financial measures, Adjusted net income and Adjusted EPS are supplemental measures of operating performance that management believes are useful measures to evaluate the Company’s performance relative to the performance of its competitors as well as performance period over period. By assuming the full exchange of all outstanding non-controlling interests, management believes these measures:

- facilitate comparisons with other companies that do not have a low effective tax rate driven by a non-controlling interest on a pass-through entity;

- facilitate period over period comparisons because they eliminate the effect of changes in Net income attributable to RE/MAX Holdings, Inc. driven by increases in its ownership of RMCO, LLC, which are unrelated to the Company’s operating performance; and

- eliminate primarily non-cash and other items that management does not consider to be useful in assessing the Company’s operating performance.

Adjusted free cash flow is calculated as cash flows from operations less capital expenditures and any changes in restricted cash of the Marketing Funds, all as reported under GAAP, and quantifies how much cash a company has to pursue opportunities that enhance shareholder value. The restricted cash of the Marketing Funds is limited in use for the benefit of franchisees and any impact to adjusted free cash flow is removed. The Company believes adjusted free cash flow is useful to investors as a supplemental measure as it calculates the cash flow available for working capital needs, re-investment opportunities, potential Independent Region and strategic acquisitions, dividend payments or other strategic uses of cash.

Adjusted free cash flow after tax and non-dividend distributions to RIHI is calculated as adjusted free cash flow less tax and other non-dividend distributions paid to RIHI (the non-controlling interest holder) to enable RIHI to satisfy its income tax obligations. Similar payments would be made by the Company directly to federal and state taxing authorities as a component of the Company’s consolidated provision for income taxes if a full exchange of non-controlling interests occurred in the future. As a result and given the significance of the Company’s ongoing tax and non-dividend distribution obligations to its non-controlling interest, adjusted free cash flow after tax and non-dividend distributions, when used in conjunction with GAAP financial measures, provides a meaningful view of cash flow available to the Company to pursue opportunities that enhance shareholder value.

Unencumbered cash generated is calculated as adjusted free cash flow after tax and non-dividend distributions to RIHI less quarterly debt principal payments less annual excess cash flow payment on debt, as applicable. Given the significance of the Company’s excess cash flow payment on debt, when applicable, unencumbered cash generated, when used in conjunction with GAAP financial measures, provides a meaningful view of the cash flow available to the Company to pursue opportunities that enhance shareholder value after considering its debt service obligations.

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/remax-holdings-inc-reports-third-quarter-2024-results-302293156.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/remax-holdings-inc-reports-third-quarter-2024-results-302293156.html

SOURCE RE/MAX Holdings, Inc.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Hometown Hero Honors Veterans with $60,000 Donation to Support Texas VFW

AUSTIN, Texas, Nov. 01, 2024 (GLOBE NEWSWIRE) — Hometown Hero, the veteran-supporting cannabusiness of hemp-derived THC and cannabidiol-based products, will present officers from the Texas Department of the Veterans of Foreign Wars (VFW) with a $60K donation to help the organization continue its mission of providing essential resources and assistance for veterans.

| WHEN: | November 4, 2024 at 1 p.m. |

| WHERE: | Texas VFW Headquarters (8503 North Interstate 35, Austin, Texas 78753). |

| WHAT: | The ceremony will include remarks from Hometown Hero executives, Texas VFW leadership and local veterans, as well as a formal check presentation and group photo opportunities. |

| WHY: | Hometown Hero donates a portion of its profits to veteran-focused organizations that provide vital support, resources and care to veterans in need. The company also provides year-round discounts for active and retired military service members for its premium line of hemp-derived and cannabidiol-based products, which are increasingly being used by veterans as an alternative to opioids. Visit here to learn more about how Hometown Hero is supporting veterans. |

“Supporting our veterans is at the heart of everything we do at Hometown Hero,” said Lukas Gilkey, cofounder of Hometown Hero and a U.S. Coast Guard veteran. “This donation to the Texas VFW Foundation is our way of giving back to those who have sacrificed so much for our country. As we celebrate Veterans Day, we’re honored to help provide the resources and support veterans need, and we look forward to continuing this mission in every way we can.”

About Hometown Hero

Headquartered in Austin, Texas, Hometown Hero manufactures and distributes a variety of hemp-derived products, such as Delta-9 THC, Delta-8 THC, CBD, CBDA + CBGA, among others. Founded in 2015 by Lukas Gilkey and Lewis Hamer, the company donates a portion of all proceeds to various charities and organizations that support veterans. For more information, visit https://hometownhero.com/ or follow the brand on Twitter and Instagram @HometownHeroATX.

About the Texas VFW

The Texas Veterans of Foreign Wars (VFW) is a statewide organization committed to advocating for and supporting veterans who have served in overseas conflicts. With 288 posts and 60,000 members across Texas, the organization provides vital resources to veterans, such as access to healthcare, benefits assistance and educational programs. More information can be found by visiting https://www.texasvfw.org.

MEDIA CONTACT:

George Medici

PondelWilkinson

310.279.5968

gmedici@pondel.com

![]()

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Automotive Properties REIT Announces Agreements to Acquire One Automotive Property in Tampa and Two Construction Equipment Dealership Properties in Greater Montreal

/NOT FOR DISTRIBUTION TO U.S. NEWS WIRE SERVICES OR DISSEMINATION IN THE UNITED STATES/

TORONTO, Oct. 31, 2024 /CNW/ – Automotive Properties Real Estate Investment Trust APR (“Automotive Properties REIT” or the “REIT”) announced today that it has entered into two separate agreements to acquire a total of three properties (the “Acquisitions”). The first agreement is to acquire a Rivian-tenanted automotive property in Tampa, Florida (the “Tampa Property”) for a purchase price of approximately US$13.5 million. The second agreement is to acquire two heavy construction equipment dealership properties in the Greater Montreal Area (the “Greater Montreal Properties”) for a purchase price of approximately $25.4 million. The additions of the Tampa Property and the Greater Montreal Properties are expected to be accretive to the REIT’s Adjusted Funds from Operations (“AFFO”)¹ per unit.

“Our acquisition of this Rivian property in Tampa will mark our targeted entry into the U.S. market and increase our exposure to the electric vehicle retail and service market in North America. Our acquisition of these two heavy construction equipment dealership properties in Greater Montreal will mark our entry into a new industry vertical that has similar characteristics to automotive dealerships, including the essential nature of their business,” said Milton Lamb, President and CEO of Automotive Properties REIT. “Upon closing, these acquisitions will enhance the tenant and geographic diversification within our portfolio, and are expected to drive AFFO.”

The Tampa Property is a 25,000 square-foot Rivian sales, delivery and service facility that is situated on 2.75 acres of land located at 701 N. Dale Mabry Highway in Tampa, Florida, in close proximity to Interstate 275 and the Tampa International Airport. The Tampa Property is tenanted by Rivian LLC, which recently completed a major renovation to the facility, under a long term, triple-net lease that includes contractual fixed annual rent increases with renewal options. Rivian LLC is a leading American developer and manufacturer of electric vehicles and accessories that completed its US$13.7 billion initial public offering on the NASDAQ stock exchange in November 2021. The REIT expects to close the Tampa Property acquisition in the first quarter of 2025, subject to customary closing conditions.

The Greater Montreal Properties consist of a 31,000 square-foot Brandt Tractor Ltd. facility with a John Deere heavy construction equipment dealership that is situated on 6.6 acres of land located at 3855 Boulevard Matte in Brossard, Québec, and a 28,611 square-foot Strongco heavy construction equipment dealership (Volvo, and other equipment brands) that is situated on 5.1 acres of land located at 72 Chemin du Tremblay in Boucherville, Québec. The REIT expects to close the Greater Montreal Properties acquisition in December 2024, subject to customary closing conditions.

The triple-net lease on the Brandt Tractor Ltd. heavy construction equipment dealership property, is a mid-term lease, and includes contractual bi-annual fixed rent increases. Brandt Tractor Ltd. is the world’s largest John Deere construction and forestry dealer and a division of the Brandt Group of Companies, a privately-owned, Canadian based manufacturing and distribution company that was founded in 1932 and serves customers in industries such as agriculture, construction, forestry, rail, mining, steel, transportation, material handling, and energy in Canada, the United States, Australia, and New Zealand.

The Strongco heavy construction equipment dealership property is tenanted pursuant to a mid-term lease, and includes contractual annual fixed rent increases. Strongco is owned by Nors, S.A. Founded in 1933, Nors is a privately-owned, Portuguese based company that sells, rents and services construction, infrastructure, mining and forestry equipment, trucks, busses, cars and marine and industrial engines in 16 countries in four continents.

The REIT expects to fund the respective purchase prices of the Acquisitions with cash on hand and by drawing on its revolving credit facilities which had been paid down in full from the net proceeds of the previously announced closing of the sale of the REIT’s Markham, Ontario dealership property on October 1, 2024.

About Automotive Properties REIT

Automotive Properties REIT is an unincorporated, open-ended real estate investment trust focused on owning and acquiring primarily income-producing automotive dealership properties located in Canada. The REIT’s portfolio currently consists of 76 income-producing commercial properties, representing approximately 2.8 million square feet of gross leasable area, in metropolitan markets across British Columbia, Alberta, Saskatchewan, Manitoba, Ontario and Québec. Automotive Properties REIT is the only public vehicle in Canada focused on consolidating automotive dealership real estate properties. For more information, please visit: www.automotivepropertiesreit.ca.

(1) Non-IFRS Financial Measure

This news release contains a financial measure which is not defined under International Financial Reporting Standards (“IFRS”) and may not be comparable to similar measures presented by other real estate investment trusts or enterprises. AFFO is a key measure of earnings performance used by real estate businesses. This measure is not defined by IFRS and does not have a standardized meaning prescribed by IFRS, and therefore should not be construed as an alternative to net income or cash flow from operating activities calculated in accordance with IFRS. The REIT believes that AFFO is an important measure of economic earnings performance and is indicative of the REIT’s ability to pay distributions from earnings. The IFRS measurement most directly comparable to AFFO is net income. Please refer to the REIT’s Management Discussion & Analysis (“MD&A”) most recently filed on SEDAR+ for further discussion of this non-IFRS financial measure.

Forward-Looking Information

This news release contains forward-looking information within the meaning of applicable securities legislation, which reflects the REIT’s current expectations regarding future events and in some cases can be identified by such terms as “will”, “should”, “anticipates”, “could” and “expects”. Forward-looking information includes statements regarding the financial impact of the Acquisitions on the REIT’s AFFO per unit and the expected timing of closing the Acquisitions. Forward-looking information is based on a number of assumptions and is subject to a number of risks and uncertainties, many of which are beyond the REIT’s control that could cause actual results and events to differ materially from those that are disclosed in or implied by such forward-looking information. Such risks and uncertainties include, but are not limited to, the factors discussed under “Risks & Uncertainties, Critical Judgments & Estimates” in the REIT’s Management’s Discussion & Analysis (“MD&A”) for the three and six-month periods ended June 30, 2024 and in the REIT’s annual information form dated March 7, 2024, which are available on SEDAR+ (www.sedarplus.ca) and the REIT’s website (www.automotivepropertiesreit.ca). The REIT does not undertake any obligation to update such forward-looking information, whether as a result of new information, future events or otherwise, except as expressly required by applicable law. This forward-looking information speaks only as of the date of this news release.

SOURCE Automotive Properties Real Estate Investment Trust

![]() View original content: http://www.newswire.ca/en/releases/archive/October2024/31/c4924.html

View original content: http://www.newswire.ca/en/releases/archive/October2024/31/c4924.html

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

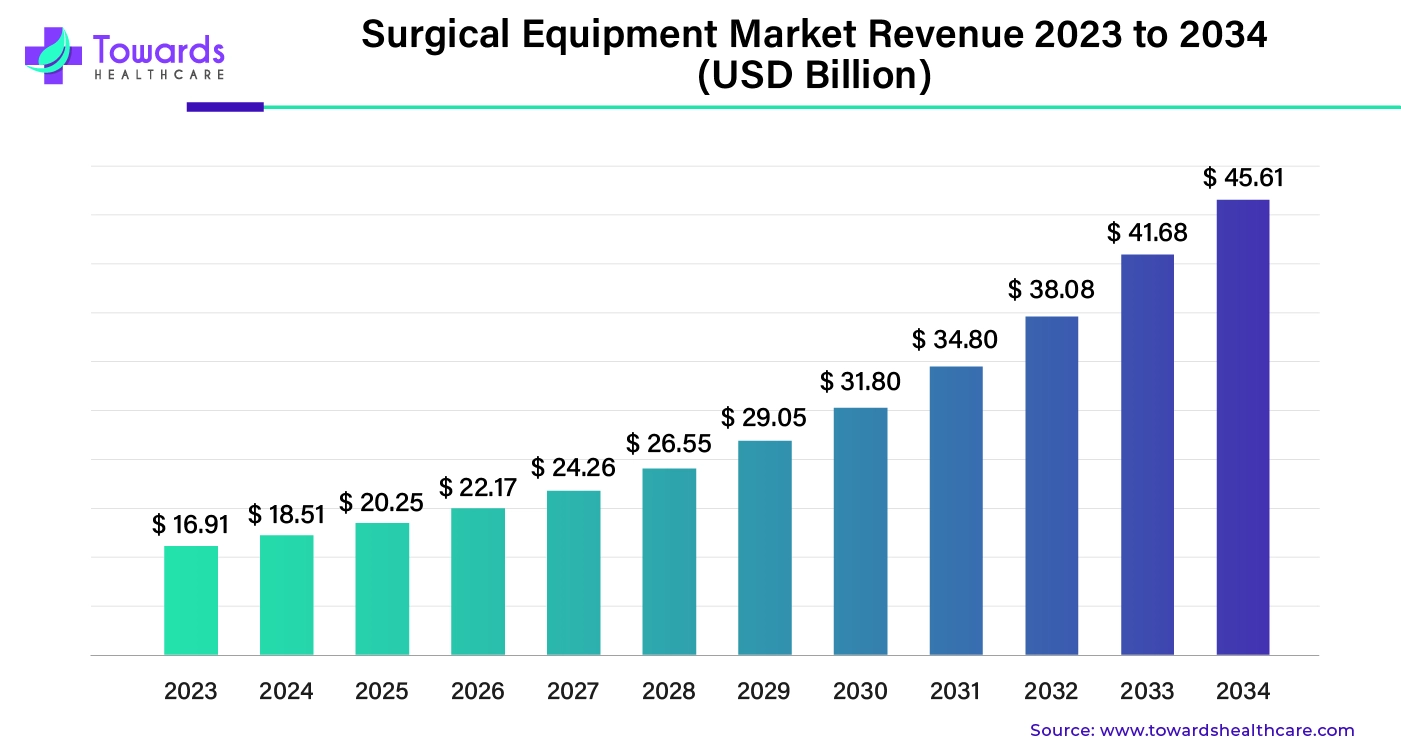

Surgical Equipment Market Size to Achieve USD 45.61 Bn by 2034

Ottawa, Oct. 31, 2024 (GLOBE NEWSWIRE) — The global surgical equipment market size is predicted to increase from USD 20.25 billion in 2025 to approximately USD 45.61 billion by 2034, according to a study published by Towards Healthcare a sister firm of Precedence Statistics. The industry is representing a solid CAGR of 9.44% during the forecast period. North America dominated the market with the largest market share of 41% in 2023.

Download a sample of this report @ https://www.towardshealthcare.com/download-statistics/5240

Key Takeaways

- Advancements in surgical techniques, the development of minimally invasive surgery techniques has increased the demand for specialized surgical equipment that allows for smaller incisions and faster recovery times.

- Rising prevalence of chronic diseases, the growing burden of chronic diseases such as heart disease, cancer and diabetes has led to an increase in surgical procedures.

- Technological innovations and advancements in medical technology including robotics, imaging and material science have led to the development of new and improved surgical equipment.

Regional Insights:

North America, Cosmetic Surgery Driving the Market

The region North America held the largest share of the surgical equipment market in 2023. The increasing number of surgical procedures, advancements in healthcare infrastructure and the presence of leading industry players are some of the factors which are driving the market in North America. The United States performs around 40 to 50 million surgeries annually which makes it a key contributor to the region’s market. For instance, in 2023, 9.5 million neuro modular procedures were conducted for wrinkle reduction, reflecting the growing demand for cosmetic surgeries.

Technological innovations in surgical tools and favorable government policies are also propelling market growth. For instance, in May of 2023, Crothall Healthcare Partnered with Ascendco Health to introduce advanced tracking systems for sterile surgical instruments in United States healthcare facilities. This partnership highlights the increasing focus on safety, quality and technological improvement.

Get the latest insights on healthcare industry segmentation with our Annual Membership: https://www.towardshealthcare.com/get-an-annual-membership

Asia Pacific on to Grow and is Fastest Growing Market

In the coming years Asia Pacific is expected to grow at the fastest rate in surgical equipment market. This growth is driven by a combination of factors such as rising geriatric population, Increasing surgical procedures and rapid healthcare infrastructure development. In the country India around 30 million surgical procedures are performed each year, and the country has attracted significant foreign direct investments in medical and surgical appliances which is over USD 3.28 billion from April 2000 to March 2024.

Countries like China, South Korea and Japan are global leaders in plastic surgeries ranking third, fourth and fifth respectively. Government policies are further fueling market growth in the region. For instance, in 2022 the Chinese government introduced a USD 29 billion loan incentive policy to upgrade medical facilities which is helping boost demand for advanced surgical tools.

- In June 2024, the Tamil Nadu state government in India announced plans to sell affordable surgical equipment to the public through government run medical shops. This initiative underscores the government’s focus on expanding access to high quality surgical equipment across the country.

Related Markets Impacted by Surgical Equipment Market:

3D Printed Medical Devices Market

The 3D printed medical devices market is closely connected to the surgical equipment market as both sectors rely on cutting edge technology and innovations to improve patient outcomes. 3D medical devices ranging from imaging equipment like MRI machines 2 monitoring devices and implants, are observed to gain momentum in the upcoming years. The increasing demand for advanced surgical tools naturally push the need for complementary medical devices that assist in diagnosis, monitoring and rehabilitation. Custom devices like hearing aids, orthotics, and surgical tools can be designed with precise measurements, offering a superior fit and enhancing patient comfort compared to mass-produced alternatives.

Medical Device Gaskets & Seals Market

The medical device gaskets & seals market was estimated at US$ 0.92 billion in 2023 and is projected to grow to US$ 1.57 billion by 2034, rising at a compound annual growth rate (CAGR) of 5% from 2024 to 2034. The surgical equipment market has positively impacted the Medical Device Gaskets & Seals Market in several significant ways, primarily driven by the growing demand for high-quality, reliable components in medical devices. As the surgical equipment market expands due to advancements in technology, increasing surgical procedures, and stringent regulatory standards, the need for effective gaskets and seals has surged.

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Surgical Equipment Market Opportunity

Growing Demand for Power Tools in Surgical Procedures:

In recent years, the increasing demand for power tools in surgical procedures is set to drive the growth of the surgical equipment market. With the rise of minimally invasive surgeries power tools such as saws, trains and reamers are becoming essential for surgeons. These tools provide precision, reduce operative time and enhance overall surgical outcomes. Battery driven cordless surgical power tools are one of the key developments in this field which is shifting the market.

- In March 2023, Stryker, a global leader in medical technology introduced a new line of battery powered surgical power tools. Their innovative system of 9 cordless surgical power tools uses lithium-ion batteries which offers longer operational time and enhanced performance. Surgeons have reported improved precision and workflow particularly in orthopedic surgeries.

Surgical Equipment Market Segments:

- By product, in 2023 the surgical structures and staplers segment held the largest share of the surgical equipment market. Structures and staplers are critical for wound closures in various types of surgeries, from minor procedures to major operations like cardiovascular and gastrointestinal surgeries. Their widespread use across different specialities and advancements in structure materials and stapling technology have driven the demand.

- By type, in 2023 disposable surgical equipment segment dominated the surgical equipment market. With growing concerns over hospital acquired infections and the need for sterile surgical environments, disposable tools like scalpels, forceps, and scissors are preferred for single use. They minimize cross contamination risks and ensure safety for both patients and healthcare professionals. In the July of 2023, Madeline Industries launched a new range of eco-friendly disposable surgical kits that offer enhanced safety while addressing environmental concerns by using biodegradable materials.

- By application, the others segment which includes various general and specialized surgeries like plastic surgery, urology and obstetrics, let the surgical equipment market in 2023. These surgeries are becoming more frequent due to an aging population, rising cancer cases and an increase in elective cosmetic procedures.

Recent Developments and News of the Market:

| Company | Indraprastha Apollo Hospital |

| Headquarter | New Delhi, India, Asia Pacific |

| Development | In March 2024, At Indraprastha Apollo Hospital in New Delhi, Apollo Hospitals introduced ZAP-X, a gyroscopic radiosurgery platform for the treatment of brain tumors. The US-based medical equipment manufacturer Zap Surgical is set to launch the platform in India. Apollo stated in an official statement that “ZAP-X will offer patients a non-invasive, pain-free alternative to traditional surgical interventions for brain tumors, with sessions lasting just 30 minutes and without the necessity of anesthesia. |

| Company | Crothall Healthcare |

| Headquarter | United States, North America |

| Development | May 2024, Crothall Healthcare (Crothall), a leading provider of sterile processing and support services, and Ascendco Health (Ascendco), a leading innovator in health technology, announced a groundbreaking partnership that will usher in a new era for instrument tracking and overall sterile processing quality within healthcare facilities across the nation. This partnership has the potential to significantly elevate standards within the field of sterile processing. |

Browse More Insights of Towards Healthcare:

- The drug-device combination products market size was estimated at $150.3 billion in 2023 and is projected to grow to $337.81 billion by 2034, with a CAGR of 7.64% from 2024 to 2034.

- The mycobacterium tuberculosis market was estimated at US$ 730.00 million in 2023 and is projected to grow to US$ 1,385.79 million by 2034, rising at a CAGR of 6% from 2024 to 2034.