Nasdaq Down 500 Points; Uber Shares Dip After Q3 Results

U.S. stocks traded lower toward the end of trading, with the Nasdaq Composite dipping around 500 points on Thursday.

The Dow traded down 0.62% to 41,880.03 while the NASDAQ fell 2.69% to 18,107.65. The S&P 500 also fell, dropping, 1.64% to 5,718.50.

Check This Out: Top 2 Real Estate Stocks You May Want To Dump This Quarter

Leading and Lagging Sectors

Utilities shares rose by 1.6% on Thursday.

In trading on Thursday, information technology shares fell by 3.4%.

Top Headline

Shares of Uber Technologies, Inc UBER dipped more than 10% on Thursday after the company reported quarterly results.

The company posted fiscal third-quarter 2024 revenue growth of 20% year-on-year to $11.188 billion, beating the analyst consensus of $10.97 billion. Uber reported GAAP EPS of 46 cents and adjusted EPS of 46 cents, which beat the analyst consensus of 41 cents.

Trips grew 17% year-over-year to 2.9 billion, or 31 million per day. Uber’s Monthly Active Platform Consumers reached 161 million, up 13% year-over-year.

Equities Trading UP

- Root, Inc. ROOT shares shot up 77% to $72.03 after the company reported better-than-expected third-quarter financial results.

- Shares of Alphatec Holdings, Inc. ATEC got a boost, surging 39% to $7.82 after the company reported better-than-expected third-quarter revenue results and raised its FY24 revenue guidance.

- Lemonade, Inc. LMND shares were also up, gaining 27% to $23.89 after the company reported third-quarter earnings and sales above estimates and raised its FY24 guidance.

Equities Trading DOWN

- Matinas BioPharma Holdings, Inc. MTNB shares dropped 65% to $0.6700 after the company announced the termination of negotiations under the previously disclosed non-binding term sheet regarding global rights to MAT2203. Matinas has implemented an 80% reduction in its workforce.

- Shares of Aurora Innovation, Inc. AUR were down 24% to $5.01 after reporting a wider-than-expected quarterly loss.

- COMPASS Pathways plc CMPS was down, falling 23% to $4.7750 after the company announced it pushed its topline data readout from its COMP005 Phase 3 trial to Q2 2025 and its COMP006 data will be announced after the 26-week time point.

Commodities

In commodity news, oil traded up 1% to $69.30 while gold traded down 1.8% at $2,751.50.

Silver traded down 3.7% to $32.820 on Thursday, while copper fell 0.1% to $4.3475.

Euro zone

European shares were lower today. The eurozone’s STOXX 600 dipped 1.20%, Germany’s DAX fell 0.93% and France’s CAC 40 slipped 1.05%. Spain’s IBEX 35 Index fell 0.36%, while London’s FTSE 100 fell 0.61%.

Asia Pacific Markets

Asian markets closed mostly lower on Thursday, with Japan’s Nikkei 225 falling 0.50%, Hong Kong’s Hang Seng Index falling 0.31%, China’s Shanghai Composite Index gaining 0.42% and India’s BSE Sensex falling 0.69%.

Economics

- U.S. initial jobless claims declined by 12,000 from the previous week to 216,000 in the week ending Oct. 26.

- U.S. personal income increased by 0.3% from the prior month to $24.948 trillion in September, while personal spending increased by 0.5% to an annualized rate of $20.024 trillion.

- The personal consumption expenditure price index rose 0.2% month-over-month in September following a 0.1% increase in August.

- U.S. natural-gas supplies rose 78 billion cubic feet to 8.863 trillion cubic feet in the week ended Oct. 25.

Now Read This:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Microsoft Stock Slides 5.6% In October Despite Another Quarter Of Double-Digit Growth; Why It's Not A Buy Now

Enterprise software juggernaut Microsoft (MSFT), like most tech stocks, had started September on the wrong foot. But Microsoft stock reversed bullishly, gaining more than 3% for the month. And in recent weeks, the megacap tech slowly regained more of its long-running mojo ahead of its fiscal first-quarter results.

↑

X

Want To Snag A 10-Bagger Stock Like Nvidia? Here’s How One Trader Did It.

However, investors got a Halloween scare.

After hours Wednesday, Microsoft stock rose to as high as 444.95. But shares later sank as much as 5% below the regular-session close of 432.53 on fiscal first-quarter results. On Thursday, shares tanked 6% lower and dipped to as low as 406.30. Volume soared to 53.9 million shares, the second busiest day for Microsoft this year so far. MSFT is now down 5% for the week, all but guaranteed to snap a three-week win streak.

MSFT also dropped 5.6% for the month of October, gutting September’s gain and then some.

The Nasdaq 100, meanwhile, has fallen 2.3% for the week and is challenging the rising 10-week moving average. The index, which tracks the Nasdaq’s 100 largest nonfinancial components, had been aiming at an eighth straight gain.

Microsoft Stock Sours On Q1 Numbers

After the close on Wednesday, the member of the Magnificent Seven megacap growth stocks reported earnings in the September-ended quarter of $3.30 a share, up 10% vs. a year earlier and 20 cents above the FactSet consensus view. Sales hit $65.6 billion, rising 16% and surpassing every analyst’s forecast tracked by Yahoo Finance.

Revenue in its server products and cloud computing services businesses jumped 23% vs. a year ago. That’s definitely healthy. Meanwhile, revenue in its intelligent cloud unit rose 20% to $24.1 billion. The Microsoft 365 commercial products unit saw 13% revenue growth; sales in the 365 consumer products area increased 5%.

Please read this tech story for more details on the quarterly report.

Before the earnings shock, the stock had quietly treaded water amid a general decline in daily turnover. The dull action came despite news that the Redmond, Wash., tech giant plans to launch autonomous AI (artificial intelligence) agents that could help workers perform and support tasks in the fields of sales, finance, supply chain management and other areas of business operations.

In fact, the last time shares in Microsoft stock vigorously exchanged hands came on Sept. 20, or the triple-witching session in which weekly and monthly stock and index options expired.

A New Rebound In Store?

However, on Oct. 22, MSFT rallied 2.1% to 427.51 and notched a session high of 429.42. Volume ran up to 25 million shares, a 41% faster pace than usual. In contrast, the Nasdaq composite struggled to stay above water, while the S&P 500 fell 0.3%.

That healthy gain in big turnover suggested strong institutional investor demand. Also, Jefferies analyst Brent Thill told CNBC during an afternoon show that he sees Microsoft, as a cloud computing titan, as among the best plays currently in the theme of artificial intelligence investing.

On Tuesday this week, shares again outperformed the stock market today, rising 1.3% vs. a nearly 0.3% gain by the S&P 500 in afternoon movement. The Economist reported that Microsoft accused Google operator Alphabet of running “shadow campaigns” against the company’s European cloud computing business. In September, Google filed an antitrust complaint against Microsoft to the European Commission. Microsoft stock rose more than 0.6% in Wednesday afternoon trading ahead of quarterly results due after the regular session close.

Microsoft stock began to decline on Sept. 18, following the Federal Reserve’s key decision to cut interest rates by half a point. Shares also experienced heavier selling pressure after an Oppenheimer research analyst reduced his forecast for Microsoft’s Azure cloud computing revenue for the fiscal year ending in June 2025.

Microsoft Stock Today

Microsoft stock had risen nicely above a key technical level, the 50-day moving average. Plus, the 50-day line is starting to rise again, a promising sign. But that bullish chart action got obliterated on Thursday.

Indeed, shares are not yet ready for a new breakout and a big run to all-time highs, which would make every investor owning Microsoft stock happy. But clearly a new set-up has emerged. Currently trading near 434, the Redmond, Wash., firm now trades 7% off its peak of 468.35.

The Big Picture: Time To Short This Fallen Angel In AI Sector?

So, is Microsoft stock, affectionately nicknamed by some investors as Mr. Softy, a buy now? Or, is it a sell?

This story examines the fundamental, technical and institutional sponsorship metrics of the Redmond, Wash., firm and whether it makes sense right now for individual investors to deploy their capital.

Long-Term Leader

The member of IBD’s Long-Term Leaders resides inside the pantheon of the greatest stock market winners in U.S. history. Not long after its IPO in March 1986, MSFT demonstrated true leadership on an initial breakout from a four-month base. Microsoft stock has shown leadership — and enriched investors by rising to new highs — in multiple bull markets since then.

Without question, the company has done a spectacular job of not only maintaining a high level of reliability and trust in its brand. Management has found new markets and industries in which to grow at a rapid clip. Company financials back up the story.

Microsoft stock has rallied as much as 24.5% since Jan. 1. It began the year at 376.04. However, Microsoft’s relative strength line has continued to fall, meaning it’s underperformed the S&P 500.

You’d prefer to see a stock’s RS line to rise, not fall. The very best stocks are able to rise more quickly during a confirmed market uptrend.

Tech News: Why DA Davidson Downgraded Microsoft Stock

June Fiscal Q4 Results

On July 30, the company reported earnings in the June-ended fiscal fourth quarter of $2.95 a share, up 10% vs. a year ago and a penny above the FactSet forecast. Revenue grew 15% to $64.7 billion, $300 million above views.

The company’s Azure and related cloud services sales jumped a healthy 29% to $28.5 billion. However, that missed the Visible Alpha consensus estimate of $28.7 billion. Devices revenue dropped 11%. LinkedIn revenue grew 10% while Xbox content and services rose 61%. Productivity and business process revenue came in at $20.3 billion. Microsoft chalked up $13.22 billion in product revenue and $15.9 billion in the area of personal computing.

Please read this IBD tech story for more color on analysts’ reactions.

Following a global data fiasco rendered by a Windows-related software update failure at CrowdStrike (CRWD), Microsoft stock slumped to the 200-day line, a key long-term technical level of support and resistance.

Nonetheless, Microsoft serves as a principal investment choice in the themes of artificial intelligence, enterprise software, digital hardware and cloud computing. It has gained 860% since the end of July 2014. The S&P 500 has rallied 189%.

Stock Market Forecast For The Next 6 Months: Eye These Factors, Risks

Big Earnings Boost Microsoft Stock

In fiscal 2018, Microsoft scored a profit of $3.88 a share. Six years later, profit totaled $11.80 a share, up 204% over that time frame. Over the past four quarters, Microsoft’s earnings per share on average rose 23.5% vs. year-ago levels. Simply incredible for a company with trailing 12-month sales topping $245 billion.

Sales have moved at a slower clip than earnings. But growth has remained steady, up 8%, 13%, 18% and 17% in the past four quarters ahead of Wednesday’s news. Gross margin edged back above 70% in the March-ended fiscal third quarter.

No wonder IBD Stock Checkup recently gave MSFT an Earnings Per Share Rating of 93. After Wednesday’s report, the EPS score dipped to 90.

In fiscal 2023, the company posted an impressive 37% return on equity (ROE), a measure of profit-generating efficiency. Its long-term debt to shareholders equity was reasonably low at 20%. Big stock market winners, such as Microsoft stock, tend to post high ROEs before they stage big price runs. Hence, MSFT also gets a top-drawer A grade for IBD’s SMR Rating (Sales + Margins + ROE).

Please see this Investor’s Corner for more on the SMR Rating.

Microsoft’s IBD Composite Rating fell hard on Thursday to a subpar 70. In general, the biggest stock market winners tend to show a Composite of 95 or higher at the start of their mighty runs.

The Relative Strength Rating for Microsoft stock also nose-dived on Thursday. At 45, it plunged 17 points and needs to improve. Back in August, the RS Rating stood at 83. A solid weekly gain could boost Microsoft’s RS score again.

A 45 RS Rating means Microsoft stock has outperformed 45% of all companies over the past 12 months. Highly unacceptable. In fact, the average Relative Strength Rating among the biggest stock market winners in recent decades when they began their gigantic price runs is 87, according to IBD research.

This means numerous big winner break out to new highs and produce big profits for investors willing to make a timely buy when their Relative Strength Rating is already strong, say at 95 or higher.

The 3-month RS Rating has ramped up to a 69 vs. 58 in recent days.

MSFT Stock: Nadella’s Take

The company has invested billions of dollars in OpenAI for its ChatGPT AI platform. “This next generation of AI will reshape every software category and every business, including our own,” CEO Satya Nadella stated in the company’s 2023 annual report. “Forty-eight years after its founding, Microsoft remains a consequential company because time and time again — from PC/Server, to Web/Internet, to Cloud/Mobile — we have adapted to technological paradigm shifts.”

Amid a new funding round for OpenAI, according to news reports, the company is now valued at $157 billion. On Thursday, OpenAI reportedly a launched a new web browser to compete in the internet search market.

On Sept. 17, shares rallied as much as 3% and hit a two-month high of 441.85 on news that the company is boosting its share buyback plan by up to $60 billion. That’s roughly 1.8% of the company’s stock market value of $3.23 trillion. A day later on Sept. 18, Microsoft announced it is teaming up with money management titan BlackRock (BLK) and MGX, a venture fund based in Abu Dhabi, UAE, to invest up to $30 billion in AI infrastructure, including datacenters and energy generation.

Which Stocks Are On IBD Long-Term Leaders? Check The List Here

Microsoft Stock And Institutional Activity

Microsoft stock has 7.433 billion shares outstanding. One of the few companies in the trillion-dollar club, its total market value recently exceeded $3.4 trillion.

Mutual funds, hedge funds, insurers, pension plans, sovereign wealth funds and the like dominate the long-term movement of share prices. MSFT stock is no exception. In the third quarter of 2023, as many as 10,119 mutual funds held MSFT stock, based on MarketSurge data. That number has since grown to as high as 10,509 funds as the end of the June quarter. In Q3, the figure eased to 10,362.

To determine the right time to buy MSFT stock, always consult a stock chart. The monthly chart offers an excellent view of a stock’s long-term trend. The weekly chart helps a savvy investor identify time-tested chart patterns that have repeatedly emerged among big stock market winners. Finally, the daily chart helps pinpoint an exact buy point.

During the 2022 bear market, Microsoft struggled like other growth companies. But in early November 2022, the stock bottomed out at 213.43 and began to grind higher. Three months later in February 2023, Microsoft stock attempted to break a 14-month downtrend. While it gained some ground, the attempt failed. But in March, Microsoft busted out of that downtrend in bullish form. Mr. Softy rallied 15.6% that month. Turnover climbed.

The monthly action highlighted a bullish character change in Microsoft stock.

Find Large Cap Stock Champions Here In This Unbiased Stock List

MSFT Stock: Weekly Chart Action

On a weekly chart, MSFT delivered a buy opportunity when it cleared 276.76, the high in the week ended Feb. 10, 2023, in enormous weekly turnover of 237 million shares. This strong move signaled unusually strong demand. Over 18 weeks, Microsoft rallied more than 32%, then dipped back into base-building phase.

A base allows a great stock to take a break as investors lock in gains. The price action becomes dull; general interest wanes. However, when institutions start getting greedy again, the stock begins to rally off lows and set up a potential breakout.

In the week ended Nov. 10, 2023, shares cleared a shallow saucer pattern with a 366.78 buy point. Shares went on to form a base-on-base pattern.

Not all breakouts succeed.

In the week ended May 24 this year, Microsoft stock poked above a 430.82 entry. Gains were minimal. On May 31, it fell 7% below the buy point, triggering the golden rule of investing: cut losses short. Two months later in July, Microsoft dove below its 10-week moving average.

Cheap Growth Stocks To Buy And Watch: Mining Plays Lead Market

Microsoft Stock: Daily Chart Action

On Sept. 18 and 19, IBD boosted its suggested investment exposure level twice. This has implications for new positions.

In recent weeks, Microsoft offered an aggressive entry near its 200-day moving average — drawn in black on a daily chart at Investors.com and in MarketSurge — for investors who already hold a big gain and would like to add to their positions. The 200-day moving average is rising steadily and has now surpassed 420.

This column noted in recent weeks that shares are trying to rally above the 200-day line. It makes sense to wait and see if the stock not only stabilizes but also rallies in robust fashion back above the 200-day line before possibly going long.

Given the whipsawing action, Microsoft stock needs to prove it can solidly regain support at the 200-day moving average before it is a new buy. So investors should wait and watch at this point.

Always stay wary of buying too far above the 200-day line on a price percentage basis. IBD suggests this rule: Buy within 5% of the buy point or moving average. At this point, with the right side of the base taking more shape, a potential trendline entry near 430 is also emerging. Also watch for a potential handle, or final shakeout of disgruntled shareholders before a potential big run, to complete.

Meanwhile, the stock continues to build a base; that’s another big reason to keep monitoring its chart action.

For long-term holders, MSFT is not a sell. But watch to see how it handles a potential test of its recent lows: 388.03 back in April and 385.59 set on Aug. 5.

Finally, if the nascent rebound withers and MSFT falls hard, traders need to cut losses on newly bought shares. Keeping losses at no larger than 7% remains the golden rule of investing.

Please follow Chung on X/Twitter: @saitochung and @IBD_DChung

YOU MIGHT ALSO LIKE:

Find Big Winners Like Microsoft Stock: Go Inside IBD Big Cap 20

Find The Best Growth Stocks Via This Highly Stringent Screen

Ready Capital Corporation Announces Third Quarter 2024 Results and Webcast Call

NEW YORK, Oct. 31, 2024 (GLOBE NEWSWIRE) — Ready Capital Corporation RC (the “Company”) today announced that the Company will release its third quarter 2024 financial results after the New York Stock Exchange closes on Thursday, November 7, 2024. Management will host a webcast and conference call on Friday, November 8, 2024 at 8:30 a.m. Eastern Time to provide a general business update and discuss the financial results for the quarter ended September 30, 2024.

Webcast:

The Company encourages use of the webcast due to potential extended wait times to access the conference call via dial-in. The webcast of the conference call will be available in the Investor Relations section of the Company’s website at www.readycapital.com. To listen to a live broadcast, go to the site at least 15 minutes prior to the scheduled start time in order to register, download and install any necessary audio software.

Dial-in:

The conference call can be accessed by dialing 877-407-0792 (domestic) or 201-689-8263 (international).

Replay:

A replay of the call will also be available on the Company’s website approximately two hours after the live call through November 22, 2024. To access the replay, dial 844-512-2921 (domestic) or 412-317-6671 (international). The replay pin number is 13748606.

About Ready Capital Corporation

Ready Capital Corporation RC is a multi-strategy real estate finance company that originates, acquires, finances and services lower-to-middle-market investor and owner occupied commercial real estate loans. The Company specializes in loans backed by commercial real estate, including agency multifamily, investor, construction, and bridge as well as U.S. Small Business Administration loans under its Section 7(a) program. Headquartered in New York, New York, the Company employs approximately 350 professionals nationwide.

Contact

Investor Relations

Ready Capital Corporation

212-257-4666

InvestorRelations@readycapital.com

![]()

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Milestone Reached: Foundation Poured for SPC Zach Parker's Accessible Home at Republic Grand Ranch

HOUSTON, Oct. 31, 2024 /PRNewswire/ — A significant milestone has been reached in the construction of the home for triple amputee and retired Army Specialist Zach Parker. On a beautiful morning at Republic Grand Ranch, the foundation was poured for the Parker family’s future home, marking an exciting step in this project. The home is being custom-built by Design Tech Homes, with support from the Helping A Hero initiative and generous donations from key partners in the construction industry.

The foundation pour was made possible through the contributions of Keystone, Heidelberg, and Builders Post Tension, whose generosity and commitment have helped make this home a reality for a well-deserving hero. The home is part of the Bass Pro Shops 100 Homes Challenge, which provides custom-built, fully accessible homes to wounded veterans like SPC Zach Parker.

“We spent the day touring the property with Zac and his family, determined to find the perfect homesite. It was a special moment to see this family’s vision coming to life at the foundation pour,” said Gary Sumner, managing partner of Patten Properties.

The home is situated on a beautiful two-acre lot within Republic Grand Ranch, intentionally selected to offer the Parker family privacy and access to nature. The custom home, crafted by Design Tech Homes, will be fully wheelchair accessible, allowing Zach to navigate his daily activities with ease and comfort.

As the project progresses, the Parker family and the entire community look forward to many more milestones, from framing to interior design, and ultimately, move-in day.

“We are truly honored to partner with Republic Grand Ranch, Patten Companies, Helping A Hero, and all the generous donors who helped make this home a reality. It’s incredible to see what a community can achieve when we come together for such a meaningful cause!” – Design Tech Homes

Stay tuned for more updates as we continue building this home for a true American hero. Follow here: IG, FB, LinkedIn & Republic Grand Ranch

About Patten Properties

Patten Properties and its partners are recognized as being among the industry’s foremost authorities on real estate investment and development across the nation. Our culture is founded on integrity and professionalism, which we proudly combine with a commitment to creating value and opportunity in today’s exciting real estate environment.

CONTACT:

Heather Robison

heather@pattenco.com

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/milestone-reached-foundation-poured-for-spc-zach-parkers-accessible-home-at-republic-grand-ranch-302293050.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/milestone-reached-foundation-poured-for-spc-zach-parkers-accessible-home-at-republic-grand-ranch-302293050.html

SOURCE Patten Properties

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Stocks Fall on Tech Results Ahead of US Jobs Data: Markets Wrap

(Bloomberg) — Asian equities fell after US stocks dropped on lackluster tech results. A rally in Treasuries favored the long end of the curve ahead of US jobs data due later Friday.

Most Read from Bloomberg

Shares in Japan, South Korea and Australia declined, while a gauge of US-listed Chinese companies dropped for a third straight day on Thursday. The S&P 500 lost 1.9% and the Nasdaq 100 dropped 2.4% Thursday, their worst sessions since early September. Elsewhere, oil extended gains on a report Iran may be planning fresh attacks on Israel.

Declines for US equities reflected investor unease over tech giants, including Microsoft Corp and Meta Platforms Inc. Apple Inc. shares were slightly softer in post-market trading after reporting weaker-than-anticipated sales in China. Amazon.com Inc. and Intel Corp. bucked the trend, rising in after-hours trade on optimistic outlooks, supporting a small advance for US stock futures early Friday.

“It makes some sense to trim some from those names that have worked so well over the past 12-18 months and look for AI laggards as well as other tech themes like cybersecurity, robotics and automation,” said Michael Landsberg, chief investment officer, Landsberg Bennett Private Wealth Management.

Treasuries were steady after minor gains Thursday. This did little to reverse the heavy selling of the past few weeks that left October as the worst month for Treasuries in two years. Those losses reflected a rethink on US interest rates given signs of resilience in the economy. An index of dollar strength was little changed after falling Thursday.

Australia’s 10-year bond yield rose to an 11-month high.

Weekly US jobless claims fell more than expected, according to figures released Thursday, indicating a robust employment market, and less reason for the Federal Reserve to cut rates. Friday’s nonfarm payroll figures are expected to show 100,000 jobs added to the US economy in October.

The pound was steady Friday after weakening alongside UK bonds and stocks Thursday as investors dumped British assets on inflation fears following the new Labour government’s budget.

Back in Asia, the yen was steady Friday after climbing as much as 1% against the greenback Thursday. The gains followed comments from Bank of Japan Governor Kazuo Ueda that currency markets have had a major impact on the economy, pointing to another potential rate hike in coming months.

QUAINT OAK BANCORP, INC. ANNOUNCES THIRD QUARTER EARNINGS

Southampton, PA , Oct. 31, 2024 (GLOBE NEWSWIRE) — Quaint Oak Bancorp, Inc. (the “Company”) QNTO, the holding company for Quaint Oak Bank (the “Bank”), announced today net income for the quarter ended September 30, 2024 of $243,000, or $0.09 per basic and diluted share, compared to net loss of $255,000, or $(0.11) per basic and diluted share, net, for the same period in 2023. Net income for the nine months ended September 30, 2024 of $1.2 million, or $0.47 per basic and diluted share, net, compared to net income of $878,000, or $0.40 per basic and $0.39 per diluted share, for the same period in 2023.

Robert T. Strong, President and Chief Executive Officer stated, “Our earnings for the quarter ended September 30, 2024, have improved over the same period of one year ago. Although we have not yet achieved our historic levels, this report signals a significant improvement. Similarly, our net income for the nine months ended September 30, 2024, registers a 38.5% improvement over the same period of one year ago.”

Mr. Strong added, “We are pleased to have experienced significant improvement in non-interest income during the quarter ended September 30, 2024, and the nine-month period ended September 30, 2024, when compared to the same periods of one year ago, excluding discontinued operations.”

Mr. Strong continued, “Although, there appears to be some market weakness in the small business lending category and although we have increased our allowance for credit losses as a percent of total loans receivable to 1.24% at September 30, 2024; our non-performing loans as a percent of total loans receivable, net along with our non-performing assets as a percent of total assets both remain below 1.00%.”

Mr. Strong commented, “We are pleased to report that our total risk-based capital ratio at this quarter end is 13.86%. Additionally, total stockholder equity increased $2.9 million at September 30, 2024, when compared to that of year end December 31, 2023. As previously reported, our Board of Directors approved the payment of a dividend, in the amount of $0.13 per share to shareholders of record on October 28, 2024, payable on November 12, 2024.”

Mr. Strong concluded, “As always, our current and continued business strategy focuses on maintaining healthy capital ratios coupled with long-term profitability and payment of dividends, each of which reflect our strong commitment to shareholder value.”

On March 29, 2024, Quaint Oak Bank sold its 51% interest in Oakmont Capital Holdings, LLC (“OCH”). The decision was based on a number of strategic priorities and other factors. As a result of this action, the Company classified the operations of OCH as discontinued operations under ASC 205-20. The Consolidated Balance Sheets and Consolidated Statements of Income present discontinued operations for the current period and retrospectively for prior periods.

Also on March 29, 2024, the Company discontinued the operations of Quaint Oak Real Estate, LLC (“Quaint Oak Real Estate”), a 100% wholly owned subsidiary of the Bank. Quaint Oak Real Estate was engaged in the real estate brokerage business. The Bank agreed to cease operations of Quaint Oak Real Estate and discontinue utilizing the services of the real estate agents it had been doing business with and had developed relationships with.

Comparison of Quarter-over-Quarter Operating Results

Net income amounted to $243,000 for the three months ended September 30, 2024, an increase of $498,000, or 195.3%, compared to net loss of $255,000 for the three months ended September 30, 2023. The increase in net income on a comparative quarterly basis was primarily the result of a decrease in interest expense of $427,000, a decrease in net loss from discontinued operations of $300,000, a decrease in non-interest expense of $221,000, an increase in non-interest income of $188,000, and a decrease in the provision for credit losses of $134,000, partially offset by a decrease in interest income of $639,000, and an increase in the net provision for income taxes of $133,000.

The $639,000, or 5.8%, decrease in interest income was primarily due to a decrease in the average balance of loans receivable, net, which decreased $114.7 million from $722.4 million for the three months ended September 30, 2023 to $607.6 million for the three months ended September 30, 2024 and had the effect of decreasing interest income $1.7 million. This decrease was partially offset by a 50 basis point increase in the average yield on loans receivable, net from 6.01% for the three months ended September 30, 2023 to 6.51% for the three months ended September 30, 2024, and had the effect of increasing interest income $767,000, and a $39.3 million increase in the average balance of due from banks – interest earning, which increased from $6.6 million for the three months ended September 30, 2023 to $45.9 million for the three months ended September 30, 2024, and had the effect of increasing interest income $413,000.

The $427,000, or 6.4%, decrease in interest expense for the three months ended September 30, 2024 over the comparable period in 2023 was driven by a $751,000, or 95.9%, decrease in the interest on Federal Home Loan Bank short-term borrowings due to a $52.4 million, or 97.1%, decrease in the average balance of Federal Home Loan Bank short-term borrowings which decreased from $54.0 million for the three months ended September 30, 2023 to $1.6 million for the three months ended September 30, 2024. Also contributing to the decreases in interest expense for the three months ended September 30, 2024 was $310,000, or 83.3%, decrease in the interest on Federal Home Loan Bank long-term borrowings due to a $33.7 million, or 81.0%, decrease in the average balance of Federal Home Loan Bank long-term borrowings which decreased from $41.7 million for the three months ended September 30, 2023 to $8.0 million for the three months ended September 30, 2024. Partially offsetting these decreases in interest expense for the three months ended September 30, 2024 was a $573,000, or 11.3%, increase in interest expense on deposits, primarily attributable to a 92 basis point increase in average rate of certificates of deposit, which increased from 3.35% for the three months ended September 30, 2023 to 4.27% for the three months ended September 30, 2024, and had the effect of increasing interest expense by $513,000. The average interest rate spread increased from 1.73% for the three months ended September 30, 2023 to 1.87% for the three months ended September 30, 2024 while the net interest margin increased from 2.42% for the three months ended September 30, 2023 to 2.58% for the three months ended September 30, 2024.

The $134,000, or 52.1%, decrease in the provision for credit losses for the three months ended September 30, 2024 over the three months ended September 30, 2023 was due to a decrease in loans receivable, net, partially offset by an increase in individually evaluated loans which increased the provision for credit losses by $259,000.

The $188,000, or 18.4%, increase in non-interest income for the three months ended September 30, 2024 over the comparable period in 2023 was primarily attributable to a $122,000, or 32.0%, increase in net gain on sale of loans, a $79,000, or 50.0%, increase in mortgage banking, equipment lending, and title abstract fees, a $29,000, or 30.5%, increase in gain on sale of SBA loans, and an $8,000, or 4.2%, increase in insurance commissions. These increases were partially offset by a $38,000, or 24.7%, decrease in other fees and service charges, and a $16,000, or 100.0%, decrease in real estate sales commissions, net.

The $221,000, or 4.3%, decrease in non-interest expense for the three months ended September 30, 2024 over the comparable period in 2023 was primarily due to a $229,000, or 89.8%, decrease in professional fees, a $116,000, or 26.0%, decrease in occupancy and equipment expense, a $56,000, or 51.9%, decrease in directors’ fees and expenses, and a $39,000, or 19.8%, decrease in FDIC deposit insurance assessment. These decreases were partially offset by a $182,000, or 5.5%, increase in salaries and employee benefits expense, a $27,000, or 5.7%, increase in other expense, and a $10,000, or 3.2%, increase in data processing expense. The decrease in professional fees was due to a $98,000 recovery of legal fees due to a loan payoff.

The provision for income tax from continuing operations increased $133,000, or 380.0%, from $35,000 for the three months ended September 30, 2023 to $168,000 for the three months ended September 30, 2024 due primarily to an increase in taxable income from continuing operations.

Comparison of Nine-Month Operating Results

Net income amounted to $1.2 million for the nine months ended September 30, 2024, an increase of $338,000, or 38.5%, compared to net income of $878,000 for the nine months ended September 30, 2023. The increase in net income on a comparative quarterly basis was primarily the result of an increase in non-interest income of $2.4 million, a decrease in non-interest expense of $207,000, and a decrease in net loss from discontinued operations of $28,000, partially offset by an increase in interest expense of $849,000, an increase in the provision for credit losses of $758,000, a decrease in interest income of $442,000, and an increase in the net provision for income taxes from continuing operations of $254,000.

The $442,000, or 1.3%, decrease in interest income was primarily due to a decrease in the average balance of loans receivable, net, which decreased $123.7 million from $748.6 million for the nine months ended September 30, 2023 to $624.9 million for the nine months ended September 30, 2024 and had the effect of decreasing interest income $5.5 million. These decreases were partially offset by a 59 basis point increase in the yield on average loans receivable, net, including loans held for sale, which increased from 5.91% for the nine months ended September 30, 2023 to 6.50% for the nine months ended September 30, 2024, and had the effect of increasing interest income $2.7 million, and a $66.7 million increase in the average balance of due from banks – interest earning, which increased from $6.1 million for the nine months ended September 30, 2023 to $72.7 million for the nine months ended September 30, 2024, and had the effect of increasing interest income $2.1 million, and a 93 basis point increase in the average yield on due from banks – interest earning which increased from 4.20% for the nine months ended September 30, 2023 to 5.13% for the nine months ended September 30, 2024, and had the effect of increasing interest income $504,000.

The $849,000, or 4.5%, increase in interest expense for the nine months ended September 30, 2024 over the comparable period in 2023 was driven by a $4.5 million, or 34.1%, increase in interest on average deposits. Also contributing to the increase in interest expense was a 51 basis point increase in the rate on average money market accounts which increased from 4.04% for the nine months ended September 30, 2023 to 4.55% for the nine months ended September 30, 2024 and had the effect of increasing interest expense by $828,000. Partially offsetting the increase in interest expense for the nine months ended September 30, 2024 was a $3.6 million, or 99.1%, decrease in the interest on Federal Home Loan Bank short-term borrowings due to an $89.3 million, or 99.0%, decrease in the average balance of Federal Home Loan Bank short-term borrowings which decreased from $90.1 million for the nine months ended September 30, 2023 to $861,000 for the nine months ended September 30, 2024. The average interest rate spread decreased from 2.03% for the nine months ended September 30, 2023 to 1.83% for the nine months ended September 30, 2024 while the net interest margin decreased from 2.62% for the nine months ended September 30, 2023 to 2.61% for the nine months ended September 30, 2024.

The $758,000, or 164.8%, increase in the provision for credit losses for the nine months ended September 30, 2024 over the nine months ended September 30, 2023 was due to an increase in the amount of non-performing loans. There were nineteen individually evaluated loans which increased the provision for credit losses by $913,000. This increase was partially offset by a decrease in the average balance of loans receivable, net.

The $2.4 million, or 78.4%, increase in non-interest income for the nine months ended September 30, 2024 over the comparable period in 2023 was primarily attributable to a $1.4 million gain on sale of Oakmont Capital Holdings, LLC, a $789,000, or 65.3%, increase in net gain on sale of loans, a $286,000, or 96.6%, increase in other fees and services charges, a $206,000, or 48.9%, increase in mortgage banking, equipment lending, and title abstract fees, and a $40,000, or 8.2%, increase in insurance commissions. These increases were partially offset by a $142,000 or 96.6%, decrease in net loan servicing income, a $95,000, or 27.5%, decrease in gain on sale of SBA loans, and a $68,000, or 77.3%, decrease in real estate sales commissions, net.

The $207,000, or 1.3%, decrease in non-interest expense for the nine months ended September 30, 2024 over the comparable period in 2023 was primarily due to a $274,000, or 45.9%, decrease in professional fees, a $175,000, or 26.2%, decrease in FDIC deposit insurance assessment, a $162,000, or 51.4%, decrease in directors’ fees and expenses, and a $142,000, or 12.5%, decrease in occupancy and equipment expense. The decrease in directors’ fees and expenses was primarily due to a reduction in director rates for the nine months ended September 30, 2024. The decrease in non-interest expense was partially offset by a $394,000, or 3.8%, increase in salaries and employee benefits expense, and a $157,000, or 21.3%, increase in data processing expense.

The provision for income tax on continuing operations increased $254,000, or 39.2%, from $648,000 for the nine months ended September 30, 2023 to $902,000 for the nine months ended September 30, 2024 due primarily to an increase in taxable income from continuing operations.

Comparison of Financial Condition

The Company’s total assets at September 30, 2024 were $701.6 million, a decrease of $52.5 million, or 7.0%, from $754.1 million at December 31, 2023. This decrease in total assets was primarily due to a $70.4 million, or 11.4%, decrease in loans receivable, net of allowance for credit losses. The largest decreases within the loan portfolio occurred in commercial real estate loans which decreased $31.0 million, or 9.4%, commercial business loans which decreased $23.4 million, or 16.5%, construction loans which decreased $11.7 million, or 32.9%, and one-to-four family non-owner occupied loans which decreased $6.2 million, or 15.3%. Partially offsetting these decreases were one-to-four family owner occupied loans which increased $1.5 million, or 6.4%, and multi-family residential which increased $783,000, or 1.7%. Partially offsetting the decrease in total assets was a $34.4 million, or 94.4%, increase in loans held for sale, a $3.3 million, or 5.8%, increase in cash and cash equivalents, an $899,000, or 25.7%, increase in accrued interest receivable, a $380,000, or 25.8%, increase in investment in Federal Home Loan Bank stock, at cost, and a $275,000, or 10.4%, increase in premises and equipment, net.

Loans held for sale increased $34.4 million, or 94.4%, from $36.4 million at December 31, 2023 to $70.9 million at September 30, 2024 as the Bank originated $51.6 million in equipment loans held for sale and sold $71.6 million of equipment loans during the nine months ended September 30, 2024. Partially offsetting this increase was $8.5 million of loan amortization and prepayments. On March 29, 2024, the Bank transferred $4.4 million of equipment loans held for sale into loans receivable as part of the discontinued operations of OCH. Additionally, the Bank’s mortgage banking subsidiary, Quaint Oak Mortgage, LLC, originated $99.6 million of one-to-four family residential loans during the nine months ended September 30, 2024 and sold $93.1 million of loans in the secondary market during this same period. In the third quarter of 2024, management identified $51.0 million of commercial real estate loans and $9.9 million of SBA loans within the loan portfolio and transferred to loans held for sale at amortized cost.

Total deposits decreased $48.3 million, or 7.6%, to $583.4 million at September 30, 2024 from $631.7 million at December 31, 2023. This decrease in deposits was primarily attributable to a decrease of $36.5 million, or 35.0%, in interest bearing checking accounts, a decrease of $23.8 million, or 25.8%, in non-interest bearing checking accounts, a decrease of $5.5 million, or 2.5%, in money market accounts, and a $236,000, or 28.1%, decrease in savings accounts. These decreases in deposits were partially offset by an increase of $17.6 million, or 8.2%, in certificates of deposit. The total decrease in interest bearing checking accounts was due to reduced correspondent banking activity.

Total Federal Home Loan Bank (FHLB) borrowings increased $9.8 million, or 33.9%, to $38.9 million at September 30, 2024 from $29.0 million at December 31, 2023. During the nine months ended September 30, 2024, the Company borrowed $65.0 million of FHLB short-term borrowings, paid down $25.2 million of FHLB long-term borrowings, and paid down $30.0 million of FHLB short-term borrowings.

Total stockholders’ equity from continuing operations increased $2.9 million, or 6.0%, to $51.4 million at September 30, 2024 from $48.5 million at December 31, 2023. Contributing to the increase was net income for the nine months ended September 30, 2024 of $1.2 million, shares issued of $2.4 million, amortization of stock awards and options under our stock compensation plans of $182,000, the reissuance of treasury stock under the Bank’s 401(k) Plan of $91,000, and other comprehensive income, net of $10,000. The increase in stockholders’ equity was partially offset by dividends paid of $996,000, and $48,000 purchase of treasury stock. In addition, there was a $3.1 million, or 100.0%, decrease in noncontrolling interest from discontinued operations. The $2.5 million of shares issued were due to two private placement offerings to two investors.

Non-performing loans at September 30, 2024 totaled $5.4 million, or 0.99%, of total loans receivable, net of allowance for credit losses, consisting of $5.0 million of loans on non-accrual status and $400,000 of loans 90-days or more delinquent. Non-accrual loans consist of one commercial real estate loan, one pool of equipment loans, and nine commercial business loans. Loans 90-days or more past due include one commercial real estate loan, which is still accruing. All non-performing loans are either well-collateralized or adequately reserved for. During the nine months ended September 30, 2024, 13 commercial business loans totaling $907,000, and one construction loan of $187,000, that were previously on non-accrual were charged-off through the allowance for credit losses. The allowance for credit losses as a percent of total loans receivable was 1.24% at September 30, 2024 and 1.11% at December 31, 2023. Non-performing loans at December 31, 2023 consisted of one SBA loan on non-accrual status in the amount of $51,000 and one one-to-four family owner occupied loan that was 90 days or more past due but still accruing in the amount of $401,000. During the year ended December 31, 2023, two commercial business loans, one SBA loan, one multi-family residential loan, and two equipment loans totaling $272,000 that were previously on non-accrual were charged-off through the allowance for credit losses. In addition, there was one commercial business loan in the amount of $652,000 that was partially charged off by $603,000.

Quaint Oak Bancorp, Inc., a Financial Services Company, is the parent company for the Quaint Oak Family of Companies. Quaint Oak Bank, a Pennsylvania-chartered stock savings bank and wholly-owned subsidiary of the Company, is headquartered in Southampton, Pennsylvania and conducts business through three regional offices located in the Delaware Valley, Lehigh Valley and Philadelphia markets. Quaint Oak Bank’s subsidiary companies include Quaint Oak Abstract, LLC, Quaint Oak Insurance Agency, LLC, Quaint Oak Mortgage, LLC, and Oakmont Commercial, LLC, a specialty commercial real estate financing company. All companies are multi-state operations.

Statements contained in this news release which are not historical facts may be forward-looking statements as that term is defined in the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are subject to risks and uncertainties which could cause actual results to differ materially from those currently anticipated due to a number of factors. Factors which could result in material variations include, but are not limited to, changes in interest rates which could affect net interest margins and net interest income, competitive factors which could affect net interest income and noninterest income, changes in demand for loans, deposits and other financial services in the Company’s market area; changes in asset quality, general economic conditions as well as other factors discussed in documents filed by the Company with the Securities and Exchange Commission from time to time. The Company undertakes no obligation to update these forward-looking statements to reflect events or circumstances that occur after the date on which such statements were made.

In addition to factors previously disclosed in the reports filed by the Company with the Securities and Exchange Commission and those identified elsewhere in this press release, the following factors, among others, could cause actual results to differ materially from forward-looking statements or historical performance: the strength of the United States economy in general and the strength of the local economies in which the Company conducts its operations; general economic conditions; legislative and regulatory changes; monetary and fiscal policies of the federal government; changes in tax policies, rates and regulations of federal, state and local tax authorities including the effects of the Tax Reform Act; changes in interest rates, deposit flows, the cost of funds, demand for loan products and the demand for financial services, competition, changes in the quality or composition of the Company‘s loan, investment and mortgage-backed securities portfolios; geographic concentration of the Company‘s business; fluctuations in real estate values; the adequacy of loan loss reserves; the risk that goodwill and intangibles recorded in the Company‘s financial statements will become impaired; changes in accounting principles, policies or guidelines and other economic, competitive, governmental and technological factors affecting the Company‘s operations, markets, products, services and fees.

| QUAINT OAK BANCORP, INC. |

| Consolidated Balance Sheets |

| (In Thousands) |

| At September 30, | At December 31, | |||||||

| 2024 | 2023 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Assets | ||||||||

| Cash and cash equivalents | $ | 61,342 | $ | 58,006 | ||||

| Investment in interest-earning time deposits | 912 | 1,912 | ||||||

| Investment securities available for sale at fair value | 1,841 | 2,341 | ||||||

| Loans held for sale | 70,855 | 36,448 | ||||||

| Loans receivable, net of allowance for credit losses (2024: $6,897; 2023: $6,758) | 547,303 | 617,701 | ||||||

| Accrued interest receivable | 4,401 | 3,502 | ||||||

| Investment in Federal Home Loan Bank stock, at cost | 1,854 | 1,474 | ||||||

| Bank-owned life insurance | 4,416 | 4,329 | ||||||

| Premises and equipment, net | 2,931 | 2,656 | ||||||

| Goodwill | 515 | 515 | ||||||

| Other intangible, net of accumulated amortization | 89 | 125 | ||||||

| Prepaid expenses and other assets | 5,146 | 5,134 | ||||||

| Assets from discontinued operations | – | 19,975 | ||||||

| Total Assets | $ | 701,605 | $ | 754,118 | ||||

| Liabilities and Stockholders‘ Equity | ||||||||

| Liabilities | ||||||||

| Deposits | ||||||||

| Non-interest bearing | $ | 68,459 | $ | 92,215 | ||||

| Interest-bearing | 514,960 | 539,484 | ||||||

| Total deposits | 583,419 | 631,699 | ||||||

| Federal Home Loan Bank short-term borrowings | 35,000 | – | ||||||

| Federal Home Loan Bank long-term borrowings | 3,855 | 29,022 | ||||||

| Subordinated debt | 22,000 | 21,957 | ||||||

| Accrued interest payable | 508 | 541 | ||||||

| Advances from borrowers for taxes and insurance | 2,874 | 3,730 | ||||||

| Accrued expenses and other liabilities | 2,554 | 2,438 | ||||||

| Liabilities from discontinued operations | – | 13,166 | ||||||

| Total Liabilities | 650,210 | 702,553 | ||||||

| Total Quaint Oak Bancorp, Inc. Stockholders‘ Equity | 51,395 | 48,491 | ||||||

| Noncontrolling Interest from Discontinued Operations | – | 3,074 | ||||||

| Total Stockholders‘ Equity | 51,395 | 51,565 | ||||||

| Total Liabilities and Stockholders‘ Equity | $ | 701,605 | $ | 754,118 | ||||

| At December 31, | ||||

| 2023 | ||||

| (Unaudited) | ||||

| Assets from Discontinued Operations | ||||

| Cash and cash equivalents | $ | 4,121 | ||

| Loans held for sale | 9,580 | |||

| Premises and equipment, net | 277 | |||

| Goodwill | 2,058 | |||

| Prepaid expenses and other assets | 3,939 | |||

| Total Assets from Discontinued Operations | $ | 19,975 | ||

| Liabilities and Stockholders‘ Equity from Discontinued Operations | ||||

| Liabilities from Discontinued Operations | ||||

| Other short-term borrowings | $ | 5,549 | ||

| Accrued interest payable | 565 | |||

| Accrued expenses and other liabilities | 7,052 | |||

| Total Liabilities from Discontinued Operations | 13,166 | |||

| Total Stockholders‘ Equity from Discontinued Operations | 6,809 | |||

| Total Liabilities and Stockholders‘ Equity from Discontinued Operations | $ | 19,975 | ||

QUAINT OAK BANCORP, INC.

Consolidated Statements of Income

(In Thousands, except share data)

| For the Three Months Ended | For the Nine Months Ended | |||||||||||||||

| September 30, | September 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||

| Interest and Dividend Income | ||||||||||||||||

| Interest on loans, including fees | $ | 9,895 | $ | 10,851 | $ | 30,445 | $ | 33,183 | ||||||||

| Interest and dividends on time deposits, investment securities, interest-bearing deposits with others, and Federal Home Loan Bank stock | 577 | 260 | 3,046 | 750 | ||||||||||||

| Total Interest and Dividend Income | 10,472 | 11,111 | 33,491 | 33,933 | ||||||||||||

| Interest Expense | ||||||||||||||||

| Interest on deposits | 5,641 | 5,068 | 17,795 | 13,273 | ||||||||||||

| Interest on Federal Home Loan Bank short-term borrowings | 32 | 783 | 32 | 3,583 | ||||||||||||

| Interest on Federal Home Loan Bank long-term borrowings | 62 | 372 | 471 | 1,003 | ||||||||||||

| Interest on Federal Reserve Bank long-term borrowings | – | 11 | – | 30 | ||||||||||||

| Interest on subordinated debt | 489 | 417 | 1,461 | 1,021 | ||||||||||||

| Total Interest Expense | 6,224 | 6,651 | 19,759 | 18,910 | ||||||||||||

| Net Interest Income | 4,248 | 4,460 | 13,732 | 15,023 | ||||||||||||

| Provision for Credit Losses – Loans | 143 | 270 | 1,227 | 279 | ||||||||||||

| (Recovery of) Provision for Credit Losses – Unfunded Commitments | (20 | ) | (13 | ) | (9 | ) | 181 | |||||||||

| Total Provision for Credit Losses | 123 | 257 | 1,218 | 460 | ||||||||||||

| Net Interest Income after Provision for Credit Losses | 4,125 | 4,203 | 12,514 | 14,563 | ||||||||||||

| Non-Interest Income | ||||||||||||||||

| Mortgage banking, equipment lending and title abstract fees | 237 | 158 | 627 | 421 | ||||||||||||

| Real estate sales commissions, net | – | 16 | 20 | 88 | ||||||||||||

| Insurance commissions | 198 | 190 | 526 | 486 | ||||||||||||

| Other fees and services charges | 116 | 154 | 582 | 296 | ||||||||||||

| Net loan servicing income | 2 | 2 | 5 | 147 | ||||||||||||

| Income from bank-owned life insurance | 30 | 26 | 87 | 75 | ||||||||||||

| Net gain on sale of loans | 503 | 381 | 1,998 | 1,209 | ||||||||||||

| Gain on sale of Oakmont Capital, LLC | – | – | 1,378 | – | ||||||||||||

| Gain on the sale of SBA loans | 124 | 95 | 251 | 346 | ||||||||||||

| Total Non-Interest Income | 1,210 | 1,022 | 5,474 | 3,068 | ||||||||||||

| Non-Interest Expense | ||||||||||||||||

| Salaries and employee benefits | 3,483 | 3,301 | 10,818 | 10,424 | ||||||||||||

| Directors’ fees and expenses | 52 | 108 | 153 | 315 | ||||||||||||

| Occupancy and equipment | 330 | 446 | 996 | 1,138 | ||||||||||||

| Data processing | 321 | 311 | 894 | 737 | ||||||||||||

| Professional fees | 26 | 255 | 323 | 597 | ||||||||||||

| FDIC deposit insurance assessment | 158 | 197 | 494 | 669 | ||||||||||||

| Advertising | 42 | 42 | 202 | 208 | ||||||||||||

| Amortization of other intangible | 12 | 12 | 36 | 36 | ||||||||||||

| Other | 500 | 473 | 1,368 | 1,367 | ||||||||||||

| Total Non-Interest Expense | 4,924 | 5,145 | 15,284 | 15,491 | ||||||||||||

| Income from Continuing Operations Before Income Taxes | $ | 411 | $ | 80 | $ | 2,704 | $ | 2,140 | ||||||||

| Income Taxes | 168 | 35 | 902 | 648 | ||||||||||||

| Net Income from Continuing Operations | $ | 243 | $ | 45 | $ | 1,802 | $ | 1,492 | ||||||||

| Loss from Discontinued Operations | – | (417 | ) | (814 | ) | (852 | ) | |||||||||

| Income Tax Benefit | – | (117 | ) | (228 | ) | (238 | ) | |||||||||

| Net Loss from Discontinued Operations | $ | – | $ | (300 | ) | $ | (586 | ) | $ | (614 | ) | |||||

| Net Income (Loss) | $ | 243 | $ | (255 | ) | $ | 1,216 | $ | 878 | |||||||

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||

| Per Common Share Data: | ||||||||||||||||

| Earnings per share from continuing operations – basic | $ | 0.09 | $ | 0.02 | $ | 0.70 | $ | 0.68 | ||||||||

| Earnings per share from discontinued operations – basic | $ | – | $ | (0.13 | ) | $ | (0.23 | ) | $ | (0.28 | ) | |||||

| Earnings per share, net – basic | $ | 0.09 | $ | (0.11 | ) | $ | 0.47 | $ | 0.40 | |||||||

| Average shares outstanding – basic | 2,631,048 | 2,244,163 | 2,560,993 | 2,221,441 | ||||||||||||

| Earnings per share from continuing operations – diluted | $ | 0.09 | $ | 0.02 | $ | 0.70 | $ | 0.66 | ||||||||

| Earnings per share from discontinued operations – diluted | $ | – | $ | (0.13 | ) | $ | (0.23 | ) | $ | (0.27 | ) | |||||

| Earnings per share, net – diluted | $ | 0.09 | $ | (0.11 | ) | $ | 0.47 | $ | 0.39 | |||||||

| Average shares outstanding – diluted | 2,631,048 | 2,244,163 | 2,560,993 | 2,255,315 | ||||||||||||

| Book value per share, end of period | $ | 19.52 | $ | 20.12 | $ | 19.52 | $ | 20.12 | ||||||||

| Shares outstanding, end of period | 2,633,374 | 2,273,051 | 2,633,374 | 2,273,051 | ||||||||||||

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||

| Selected Operating Ratios: | ||||||||||||||||

| Average yield on interest-earning assets | 6.37 | % | 6.02 | % | 6.36 | % | 5.91 | % | ||||||||

| Average rate on interest-bearing liabilities | 4.50 | % | 4.29 | % | 4.53 | % | 3.88 | % | ||||||||

| Average interest rate spread | 1.87 | % | 1.73 | % | 1.83 | % | 2.03 | % | ||||||||

| Net interest margin | 2.58 | % | 2.42 | % | 2.61 | % | 2.62 | % | ||||||||

| Average interest-earning assets to average interest-bearing liabilities | 118.69 | % | 118.94 | % | 120.80 | % | 118.01 | % | ||||||||

| Efficiency ratio | 90.22 | % | 101.55 | % | 79.59 | % | 85.63 | % | ||||||||

| Asset Quality Ratios (1) | ||||||||||||||||

| Non-performing loans as a percent of total loans receivable, net | 0.99 | % | 0.02 | % | 0.99 | % | 0.02 | % | ||||||||

| Non-performing assets as a percent of total assets | 0.77 | % | 0.02 | % | 0.77 | % | 0.02 | % | ||||||||

| Allowance for credit losses as a percent of non-performing loans | 126.88 | % | n/m | 126.88 | % | n/m | ||||||||||

| Allowance for credit losses as a percent of total loans receivable | 1.24 | % | 1.11 | % | 1.24 | % | 1.11 | % | ||||||||

| Texas Ratio (2) | 8.42 | % | 0.22 | % | 8.42 | % | 0.22 | % | ||||||||

(1) Asset quality ratios are end of period ratios.

(2) Total non-performing assets divided by tangible common equity plus the allowance for loan losses.

n/m – not meaningful

Quaint Oak Bancorp, Inc. Robert T. Strong, President and Chief Executive Officer (215) 364-4059

![]()

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

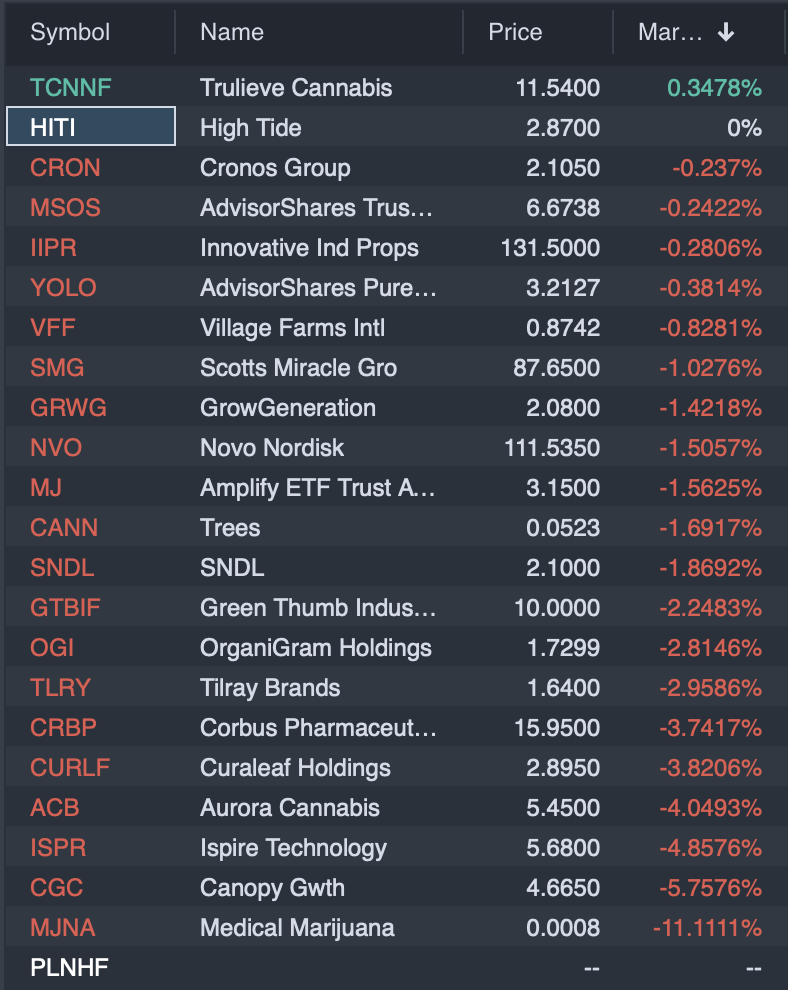

Cannabis Stocks Sink Amid Broader Market Decline And Election Jitters

Cannabis stocks are experiencing notable declines this Thursday, aligning with a general downturn across major economic indices. At the time of publication of this article, the S&P 500 index was trading down by 1.62%, the Nasdaq 100 by 2.44%, and the Dow Jones Industrial Average (DJIA) showed a similar downward trend earlier in the day, only partially recovering.

This widespread decline points to a broader economic shift, with investors adopting a more cautious approach amid market volatility.

The performance of these major indices often reflects investor sentiment across sectors, and the impact on cannabis stocks highlights their sensitivity to these broader economic movements.

Cannabis Stocks Hit Hard

Several prominent cannabis stocks saw significant drops today. Tilray Brands Inc. TLRY fell by 2.8%, Aurora Cannabis Inc. ACB dropped by 4.14% and Canopy Growth Corporation CGC saw a 6.67% decline. Other companies, like SNDL Inc. SNDL and Cronos Group Inc. CRON, also recorded losses. The downward trend isn’t limited to individual companies; cannabis ETFs, such as the AdvisorShares Pure US Cannabis ETF MSOS and Amplify Alternative Harvest ETF MJ, experienced losses as well. This widespread impact underscores the challenges cannabis stocks face in a volatile market.

Cannabis Stocks Watchlist In Benzinga Pro. Movements recorder prior to the writing of this article.

Election Uncertainty Adds Pressure

Political factors may also be contributing to the pressure on cannabis stocks.

With the upcoming U.S. elections, rising support for Donald Trump could signal potential GOP control of Congress. Historically, a Republican-led Congress has been less supportive of cannabis reform, raising concerns about policy stagnation for the industry. Investors might be factoring in this possibility, creating additional headwinds for cannabis-related equities in an already challenging market environment.

COVER: AI-generated image

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Click on the image for more info.

Cannabis rescheduling seems to be right around the corner

Want to understand what this means for the future of the industry?

Hear directly for top executives, investors and policymakers at the Benzinga Cannabis Capital Conference, coming to Chicago this Oct. 8-9.

Get your tickets now before prices surge by following this link.

Intel CEO calls TSMC an 'awesome' company, says the company is still waiting for CHIPS Act money

Another kitchen sink type of earnings day from chip giant Intel (INTC).

Intel shares rose nearly 7% in after-market trading on Thursday as the struggling US icon managed to serve up better than expected fourth quarter guidance.

“This was a critical quarter for us and I think gives optimism for what is to come,” Intel CEO Pat Gelsinger told Yahoo Finance moments after the company’s earnings call ended (video above).

But the initial market reaction may be a tad overdone when digging into the quarterly results.

Intel revealed $15.9 billion in total non-cash charges related to inventory write-downs and lower performance expectations for certain businesses, such as autonomous driving firm Mobileye (MBLY), where it owns a majority stake. The company reported a $5.8 billion operating loss at Intel Foundry — Intel’s upstart chipmaking business — on $4.4 billion in sales.

Intel took a cautious stance on the health of the foundry business in 2025. On the earnings call, management promised to continue executing on a $10 billion cost-cutting plan, as well as exploring alternative sources of funding to support chipmaking ambitions.

Gelsinger told Yahoo Finance no deal is imminent in terms of external funding.

He reiterated that Intel will push forward opening chipmaking plants in states like Ohio and Arizona despite not receiving billions of dollars in funding yet from the CHIPS Act.

The Biden administration has earmarked $8.5 billion in direct funding to Intel for its projects, but the company is still awaiting the cash as government officials iron out milestones that it must hit.

“Overall, we are seeing the CHIPS Act as a critical thing that we’ve invested a lot of time and energy into, and as we said on our earnings call, we’re disappointed by the time that it’s taken to get done,” Gelsinger said.

“It’s well over two years since the CHIPS Act passed. And over that period, I’ve invested $30 billion in US manufacturing and we’ve seen $0 from the CHIPS Act. This has taken too long, we need to get it finished.”

To be sure, Wall Street still sees a bumpy road ahead for Intel.

Intel faces an “uphill battle” to turn itself around and compete with the likes of Nvidia (NVDA), AMD (AMD), and Taiwan’s TSMC (TSM), Goldman Sachs analyst Toshiya Hari recently told Yahoo Finance.

He adds the company will need some time to get its technology — notably AI chips — on par with its rivals, if they can do it at all.

And BofA analyst Vivek Arya struck a cautious tone on Intel in a new episode of the Opening Bid podcast (listen in here).