Meow! Dogecoin, Shiba Inu Leapfrogged By Cat Coins Gaining: It's 'Cat Season Once Again,' Says Trader

Cat-themed cryptocurrencies Popcat POPCAT/USD and cat in a dogs world MEW/USD have emerged as top gainers in the overall crypto market.

What Happened: According to Coingecko, cat coins are nearing a $5 billion market cap, with a 7.7% gain in the last 24 hours. Popcat flipped Bonk BONK/USD to become the second-largest meme coin on the Solana SOL/USD network, trailing only Dogwifhat WIF/USD.

Mew reached a significant milestone, crossing the $1 billion valuation—an impressive feat for a Solana-based meme coin.

Meme coin favorites like Dogecoin DOGE/USD and Shiba Inu SHIB/USD have lagged, unable to match the recent gains of these cat coins.

| Cryptocurrency | Price | Market cap | 24-hour trend | 7-day trend |

| Dogecoin DOGE/USD | $0.1399 | $20.5B | +2.9% | +15.2% |

| Shiba Inu SHIB/USD | $0.00001781 | $10.5B | +2.7% | +0.7% |

| Popcat POPCAT/USD | $1.59 | $1.56B | +12.2% | +22% |

| cat in a dogs world MEW/USD | $0.1116 | $992M | +23.4% | +35.7% |

Also Read: Trader Shares 3-Point Strategy To Win With Meme Coins—Here’s Where Dogecoin, Shiba Inu Come In

Trader Notes: Popular trader Altcoin Sherpa highlighted on X (formerly Twitter) that “cat season” is back, with Popcat leading the charge and Mew showing strong potential. He emphasized that outside of AI-related memes, the most promising sector right now is cat-themed tokens.

Another trader, Bluntz, predicts a major breakout for Popcat, pointing to its resilience during market pullbacks and a bullish 1-2 setup pattern. He suggests that assets demonstrating strength during market declines tend to outperform in bullish markets

Meanwhile, Crypto General noted that MEW has been on a steady uptrend since its launch, recently breaking its all-time high. He expects a parabolic move in the coming days, potentially driving the price to $0.045.

Crypto trader Curbo even compared MEW to Shiba Inu, hinting that it could be the next big meme coin of this cycle.

Read Next:

Image: Shutterstock

This content was partially produced with the help of AI tools and was reviewed and published by Benzinga editors.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Lam Research Positioned For Growth Amid NAND Recovery And Advanced Packaging Strength, Analysts Highlight China Risks

BofA Securities analyst Vivek Arya reiterated the Buy rating on Lam Research LRCX, raising the price forecast to $92 from $88.

Arya expresses confidence in Lam Research’s leverage to key tech trends, its strong exposure to a NAND recovery, and solid free cash flow generation.

However, the analyst notes that while China is expected to normalize to 30% of the mix in December, ongoing risks from export controls remain, and gains in gross and operating margins appear limited.

The analyst raises the earnings estimates for 2025 and 2026 by 4% and 7%, respectively.

The analyst writes that the company’s unique portfolio will help it outperform its competitors in 2025, despite concerns about ASML Holding N.V outlook.

Also Read: ASML Stock Plunges Further On Lower 2025 Sales Outlook: Analysts Break Down Semiconductor Challenges

Arya notes that recent high shipments of lithography tools to China might lead to a bigger correction there, but Lam Research is less affected by this due to its strengths in advanced technologies like NAND and packaging.

Overall, Lam Research has several growth opportunities in 2025, even with potential challenges in China and delays from Intel and Samsung.

Meanwhile, Goldman Sachs analyst Toshiya Hari reiterated the Buy rating on Lam Research, lowering the price forecast to $96 from $102.50).

The analyst highlights that advancements in NAND, leading-edge foundry/logic, and DRAM will increase demand for etching and deposition, helping Lam gain market share in wafer fabrication equipment (WFE) in 2025 and beyond.

The analyst notes that while ASML lowered its 2025 revenue guidance due to weak demand in leading-edge foundry and potential declines in Chinese spending, Lam Research maintained its forecast of a mid-$90 billion WFE market for 2024.

In fact, Lam Research expects WFE spending to grow in 2025, driven by changes in NAND technology and ongoing strength in DRAM, HBM, and leading-edge foundry sectors, the analyst adds.

Hari notes, Advanced Packaging, essential for AI technology, will boost Lam Research’s performance.

Additionally, in the Systems business, China’s share of total revenue decreased to 37% in the September quarter from 42% in the March quarter and 39% in the June quarter.

Per Hari, the market will perceive the guided decline in China contribution positively, given the tendency for the market to pay a below-average multiple for revenue streams generated in China.

According to Hari, the market is likely to view the expected decline in China’s contribution positively, as it typically assigns a “below-average” multiple to revenue generated in China.

Price Action: LRCX shares are trading higher by 4.87% to $76.41 at last check Thursday.

Photo via Shutterstock

Read Next:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Nasdaq Edges Higher; Honeywell Shares Fall After Q3 Results

U.S. stocks traded mixed midway through trading, with the Nasdaq Composite gaining around 0.3% on Thursday.

The Dow traded down 0.72% to 42,206.88 while the NASDAQ rose 0.26% to 18,323.75. The S&P 500 also fell, dropping, 0.16% to 5,788.23.

Check This Out: Top 3 Tech Stocks You’ll Regret Missing In Q4

Leading and Lagging Sectors

Consumer discretionary shares rose by 2.6% on Thursday.

In trading on Thursday, materials shares fell by 1.1%.

Top Headline

Shares of Honeywell International Inc. HON fell around 4% on Thursday after the company reported third-quarter results and updated FY24 guidance.

Revenue grew 6% year-over-year (organic: +3%) to $9.728 billion, missing the consensus of $9.901 billion. Adjusted EPS was $2.58 (+8% Y/Y), beating the consensus of $2.50.

For FY24, the company lowered sales guidance to $38.6 billion – $38.8 billion (from $39.1 billion – $39.7 billion prior) versus the consensus of $39.20 billion. Honeywell tightened adjusted EPS guidance to $10.15 – $10.25 (from $10.05 – $10.25) versus the estimate of $10.13.

Equities Trading UP

- Nxu, Inc. NXU shares shot up 216% to $0.7930. Nxu and Verde Bioresins reported a proposed merger.

- Shares of QuantumScape Corporation QS got a boost, surging 25% to $6.49 after the company said it has begun producing low volumes of its first B-sample cells and has begun shipping cells for automotive customer testing.

- Molina Healthcare, Inc. MOH shares were also up, gaining 22% to $336.39 after the company reported better-than-expected third-quarter financial results.

Equities Trading DOWN

- Beyond, Inc. BYON shares dropped 26% to $7.03 after the company reported worse-than-expected third-quarter adjusted EPS and sales.

- Shares of Marinus Pharmaceuticals, Inc. MRNS were down 80% to $0.3413 after the company announced its Phase 3 TrustTSC trial of Oral Ganaxolone did not meet its primary endpoint.

- Community Health Systems, Inc. CYH was down, falling 23% to $4.2550 following third-quarter earnings.

Commodities

In commodity news, oil traded down 0.7% to $70.29 while gold traded up 0.4% at $2,741.10.

Silver traded down 0.1% to $33.790 on Thursday, while copper fell 0.1% to $4.3350.

Euro zone

European shares were higher today. The eurozone’s STOXX 600 gained 0.25%, Germany’s DAX gained 0.54% and France’s CAC 40 rose 0.27%. Spain’s IBEX 35 Index rose 0.12%, while London’s FTSE 100 rose 0.28%.

The S&P Global UK composite PMI declined to 51.7 in October from 52.6 in September, while Eurozone composite edged higher rose to 49.7 in October versus 49.6 in the previous month.

The HCOB Germany composite PMI increased to 48.4 in October versus 47.5 in September, while French composite PMI slipped to 47.3 in October from 48.6 in September.

Asia Pacific Markets

Asian markets closed mostly lower on Thursday, with Japan’s Nikkei 225 gaining 0.10%, Hong Kong’s Hang Seng Index falling 1.30%, China’s Shanghai Composite Index falling 0.68% and India’s BSE Sensex falling 0.02%.

The HSBC India composite PMI rose to 58.6 in October from 58.3 in the prior month. The au Jibun Bank Flash Japan composite PMI declined to 49.4 in October compared to a final reading of 52.0 in September.

Economics

- The Chicago Fed National Activity Index fell to a reading of -0.28 in September compared to a revised level of -0.01 in August.

- U.S. initial jobless claims declined by 15,000 from the prior week to 227,000 during the period ending Oct. 19, compared to market estimates of 242,000.

- U.S. building permits declined by 3.1% to an annual rate of 1.425 million in September.

- The S&P Global flash manufacturing PMI rose to 47.8 in October versus a 15-month low level of 47.3 in September.

- The S&P Global services PMI increased to 55.3 in October from 55.2 in the prior month.

- Sales of new single-family homes in the U.S. surged 4.1% to an annual rate of 738,000 in September.

Now Read This:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

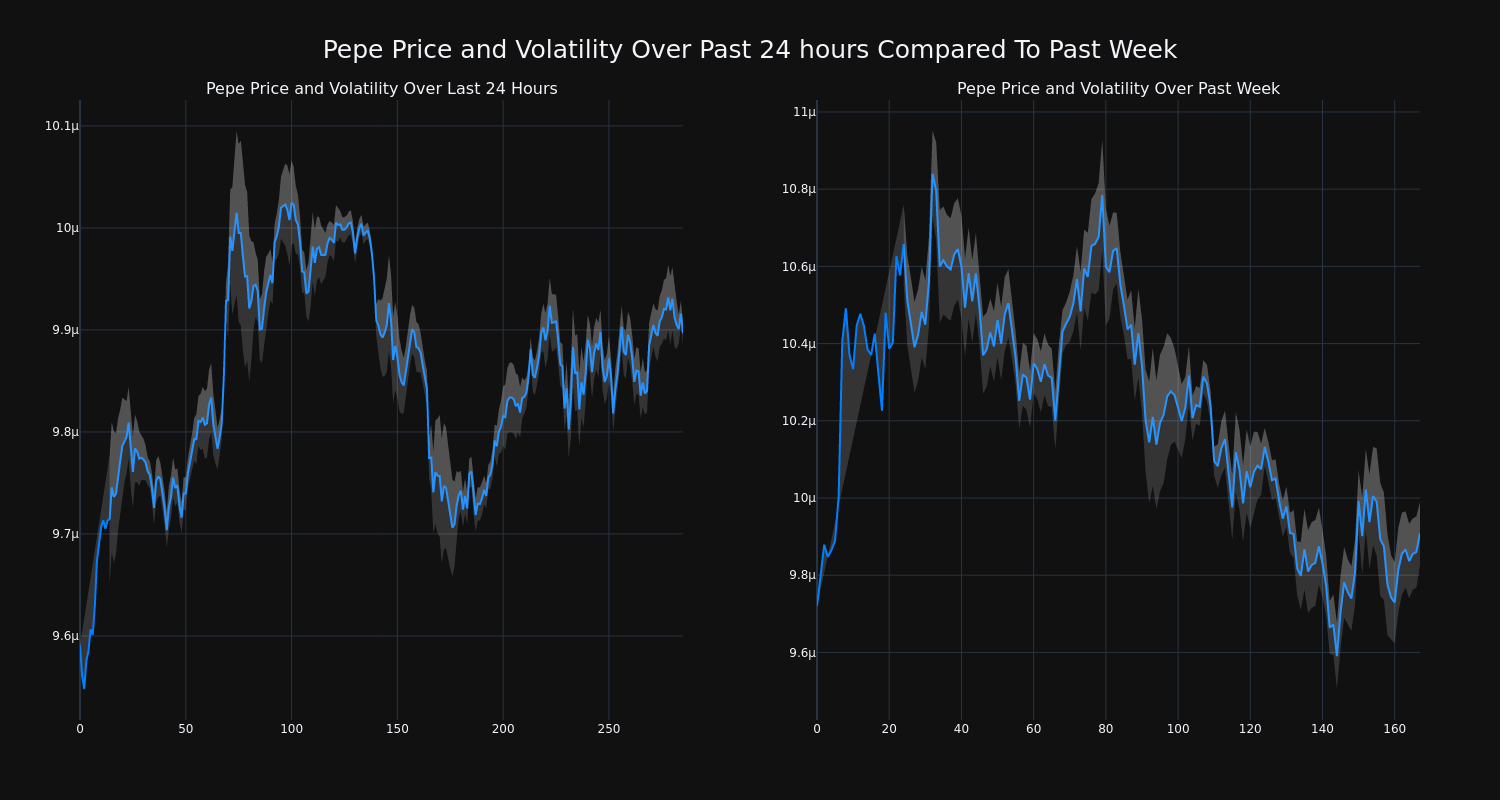

Cryptocurrency Pepe Up More Than 3% In 24 hours

Over the past 24 hours, Pepe’s PEPE/USD price has risen 3.31% to $0.000010. This continues its positive trend over the past week where it has experienced a 2.0% gain, moving from $0.000010 to its current price.

The chart below compares the price movement and volatility for Pepe over the past 24 hours (left) to its price movement over the past week (right). The gray bands are Bollinger Bands, measuring the volatility for both the daily and weekly price movements. The wider the bands are, or the larger the gray area is at any given moment, the larger the volatility.

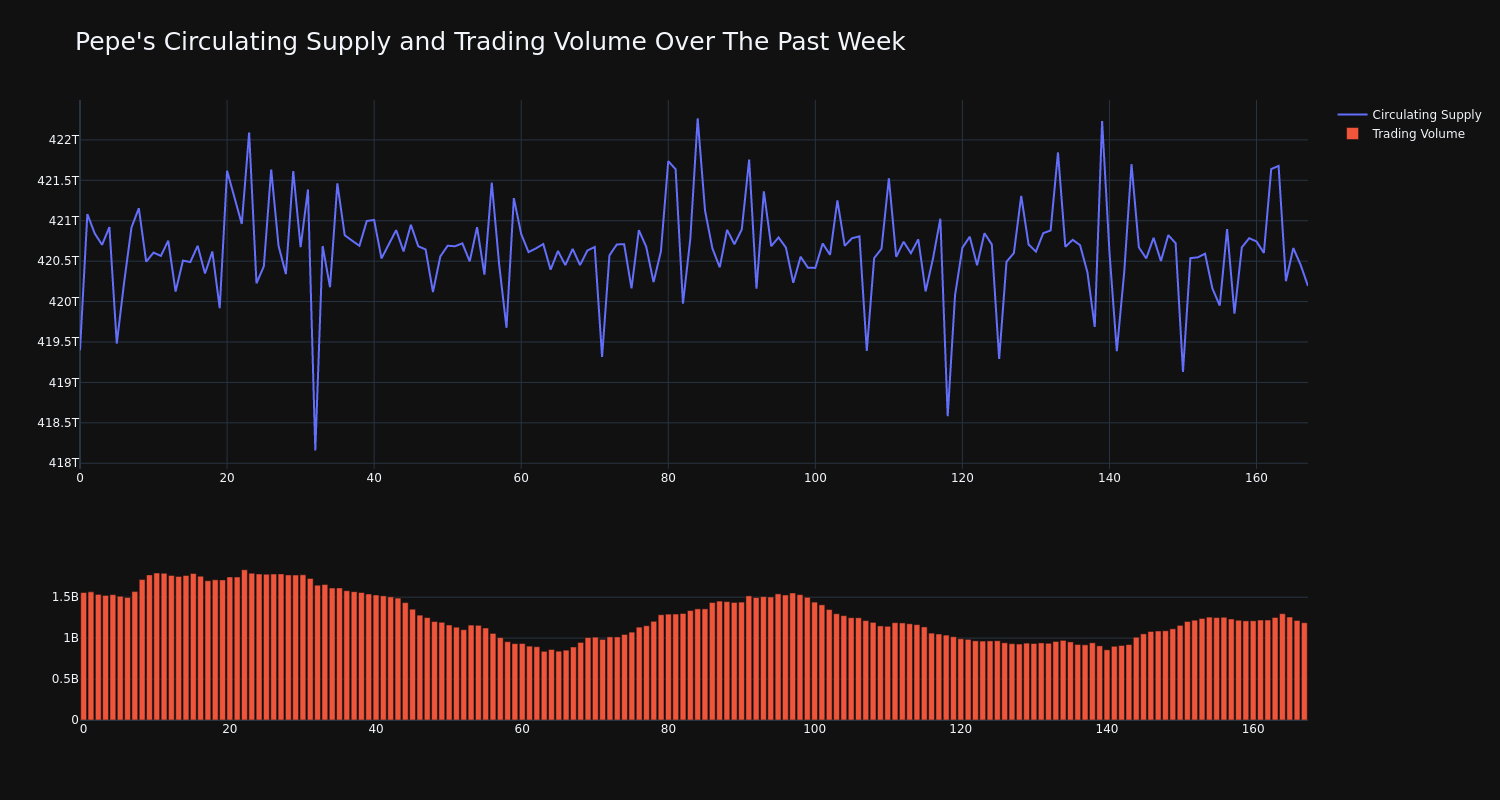

The trading volume for the coin has decreased 24.0% over the past week, while the overall circulating supply of the coin has increased 0.19% to over 420.69 trillion. This puts its current circulating supply at an estimated 100.0% of its max supply, which is 420.69 trillion. The current market cap ranking for PEPE is #29 at $4.16 billion.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Price Over Earnings Overview: Axon Enterprise

In the current session, the stock is trading at $443.51, after a 0.19% increase. Over the past month, Axon Enterprise Inc. AXON stock increased by 12.78%, and in the past year, by 120.92%. With performance like this, long-term shareholders are optimistic but others are more likely to look into the price-to-earnings ratio to see if the stock might be overvalued.

Axon Enterprise P/E Ratio Analysis in Relation to Industry Peers

The P/E ratio measures the current share price to the company’s EPS. It is used by long-term investors to analyze the company’s current performance against it’s past earnings, historical data and aggregate market data for the industry or the indices, such as S&P 500. A higher P/E indicates that investors expect the company to perform better in the future, and the stock is probably overvalued, but not necessarily. It also could indicate that investors are willing to pay a higher share price currently, because they expect the company to perform better in the upcoming quarters. This leads investors to also remain optimistic about rising dividends in the future.

Compared to the aggregate P/E ratio of 81.81 in the Aerospace & Defense industry, Axon Enterprise Inc. has a higher P/E ratio of 116.8. Shareholders might be inclined to think that Axon Enterprise Inc. might perform better than its industry group. It’s also possible that the stock is overvalued.

In summary, while the price-to-earnings ratio is a valuable tool for investors to evaluate a company’s market performance, it should be used with caution. A low P/E ratio can be an indication of undervaluation, but it can also suggest weak growth prospects or financial instability. Moreover, the P/E ratio is just one of many metrics that investors should consider when making investment decisions, and it should be evaluated alongside other financial ratios, industry trends, and qualitative factors. By taking a comprehensive approach to analyzing a company’s financial health, investors can make well-informed decisions that are more likely to lead to successful outcomes.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Penns Woods Bancorp, Inc. Reports Third Quarter 2024 Earnings

WILLIAMSPORT, Pa., Oct. 24, 2024 (GLOBE NEWSWIRE) — Penns Woods Bancorp, Inc. PWOD

Penns Woods Bancorp, Inc. achieved net income of $14.0 million for the nine months ended September 30, 2024, resulting in basic and diluted earnings per share of $1.86.

Highlights

- Net income, as reported under generally accepted accounting principles (GAAP), for the three and nine months ended September 30, 2024 was $4.8 million and $14.0 million, respectively, compared to $2.2 million and $11.1 million for the same periods of 2023. Results for the three and nine months ended September 30, 2024 compared to 2023 were impacted by an increase in net interest income of $1.7 million and $2.3 million, respectively, as the cost of funds has stabilized. The disposal of assets related to two former branch properties resulted in a one time after-tax loss of $261,000 for the nine month period ended September 30, 2024.

- The allowance for credit losses was impacted for the three and nine months ended September 30, 2024 by a provision for credit losses of $740,000 and a negative provision of $299,000, respectively, compared to provisions for credit losses of $1.4 million and $263,000 for the 2023 periods. The recognition of a negative provision for credit losses for the nine months ended September 30, 2024 is due primarily to recoveries during the second quarter of 2024 on a commercial loan. In addition, a minimal level of loan charge-offs of $312,000 contributed to the recognition of the negative provision for credit losses for the nine months ended September 30, 2024.

- Basic and diluted earnings per share for the three and nine months ended September 30, 2024 were $0.64 and $1.86, respectively, compared to basic and diluted earnings per share of $0.31 and $1.56 basic and $1.53 diluted for the three and nine month periods ended September 30, 2023.

- Annualized return on average assets was 0.86% for the three months ended September 30, 2024, compared to 0.41% for the corresponding period of 2023. Annualized return on average assets was 0.84% for the nine months ended September 30, 2024, compared to 0.70% for the corresponding period of 2023.

- Annualized return on average equity was 9.60% for the three months ended September 30, 2024, compared to 5.06% for the corresponding period of 2023. Annualized return on average equity was 9.74% for the nine months ended September 30, 2024, compared to 8.58% for the corresponding period of 2023.

Net Income

Net income from core operations (“core earnings”), which is a non-GAAP measure of net income excluding net securities gains or losses, was $4.8 million and $14.0 million, respectively, for the three and nine months ended September 30, 2024 compared to $2.3 million and $11.2 million for the same periods of 2023. Basic and diluted core earnings per share (non-GAAP) for the three and nine months ended September 30, 2024 were $0.63 and $1.86, respectively, while basic and diluted core earnings per share for the three month period of 2023 were $0.32 and for the nine month period of 2023 were $1.58 basic and $1.55 diluted. Annualized core return on average assets and core return on average equity (non-GAAP) were 0.85% and 9.54%, respectively, for the three months ended September 30, 2024, compared to 0.42% and 5.20% for the corresponding period of 2023. Annualized core return on average assets and core return on average equity (non-GAAP) were 0.84% and 9.75%, respectively, for the nine months ended September 30, 2024, compared to 0.71% and 8.67% for the corresponding period of 2023. A reconciliation of the non-GAAP financial measures of core earnings, core return on assets, core return on equity, core earnings per share and tangible book value per share to the comparable GAAP financial measures is included at the end of this press release.

Net Interest Margin

The net interest margin for the three and nine months ended September 30, 2024 was 2.88% and 2.79% respectively, compared to 2.65% and 2.82% for the corresponding periods of 2023. The increase in the net interest margin for the three month period was driven by an increase in the rate paid on interest-earning assets of 64 basis points (“bps”), while the decrease in the net interest margin for the nine month period was driven by a 96 bps increase in the rate paid on interest-bearing liabilities. The overall increase in interest rates over the periods resulted in increases to both the yield on the earnings asset portfolio and the rate paid on interest bearing liabilities. Driving the increase in the yield and interest income on the earning assets portfolio was the repricing of legacy assets coupled with portfolio growth. The average loan portfolio balance increased $76.0 million and $127.0 million, respectively, for the three and nine month periods ended September 30, 2024 compared to the same periods of 2023 as the average yield on the portfolio increased 65 bps and 72 bps, resulting in an increase in taxable equivalent interest income of $3.9 million and $14.5 million, for the periods. The three and nine month periods ended September 30, 2024 were impacted by an increase of 55 bps and 70 bps in the yield earned on the securities portfolio as legacy securities matured with the funds reinvested at higher rates, which resulted in an increase in taxable equivalent interest income of $343,000 and $1.2 million, respectively. Short-term borrowings decreased in volume, which offset the impact of an increase in rate paid, resulting in a decrease of $1.5 million and $2.1 million in expense for the three and nine month periods ended September 30, 2024 compared to the same periods of 2023. The rate paid on interest-bearing deposits increased 76 bps and 116 bps, respectively, or $3.1 million and $11.8 million in expense, for the three and nine month periods ended September 30, 2024 compared to the corresponding periods of 2023 due to the rate environment, an increase in competition for deposits, and a migration of deposit balances from core deposits to higher rate time deposits. The rates paid on time deposits significantly contributed to the increase in funding costs as rates paid for the three and nine month periods ended September 30, 2024 compared to the same periods of 2023 increased 70 bps and 114 bps, respectively, or $2.2 million and $8.2 million in expense, as deposit gathering campaigns continued to focus on time deposits with a maturity of five months. In addition, brokered deposits have been utilized to assist with funding the loan portfolio growth and contributed to the increase in time deposit funding costs, while lowering the reliance on higher cost short-term borrowings.

Assets

Total assets increased to $2.3 billion at September 30, 2024, an increase of $82.8 million compared to September 30, 2023. Net loans increased $58.0 million to $1.9 billion at September 30, 2024 compared to September 30, 2023, as continued emphasis was placed on commercial loan growth and indirect auto lending. The investment portfolio increased $8.8 million from September 30, 2023 to September 30, 2024. Investment debt securities increased $12.8 million from September 30, 2023 to September 30, 2024 as fixed rate instruments with maturities of approximately ten years were added to the portfolio to lock in yields.

Non-performing Loans

The ratio of non-performing loans to total loans ratio increased to 0.42% at September 30, 2024 from 0.20% at September 30, 2023, as non-performing loans increased to $7.9 million at September 30, 2024 from $3.7 million at September 30, 2023. The majority of non-performing loans involve loans that are either in a secured position and have sureties with a strong underlying financial position or have been classified as individually evaluated loans that have a specific allocation recorded within the allowance for credit losses. Net loan charge offs of $328,000 and $312,000 for the three and nine months ended September 30, 2024, respectively, impacted the allowance for credit losses, which was 0.62% of total loans at September 30, 2024 compared to 0.71% at September 30, 2023. Exposure to non-owner occupied office space is minimal at $13.9 million at September 30, 2024 with none of these loans being delinquent.

Deposits

Deposits increased $133.1 million to $1.7 billion at September 30, 2024 compared to September 30, 2023. Noninterest-bearing deposits decreased $18.6 million to $452.9 million at September 30, 2024 compared to September 30, 2023. Core deposits declined $6.6 million as deposits migrated from core deposit accounts into time deposits as market rates and competition for deposits increased. Core deposit gathering efforts remained focused on increasing the utilization of electronic (internet and mobile) deposit banking by our customers. Core deposits have remained stable at $1.2 billion over the past five quarters. Interest-bearing deposits increased $151.6 million from September 30, 2023 to September 30, 2024 due to growth in the time deposit portfolio of $78.7 million as customers sought a higher rate of interest. Brokered deposit balances increased $61.0 million to $167.7 million at September 30, 2024 as this funding source was utilized to supplement funding loan portfolio growth, while reducing the need to draw upon available borrowing lines. A campaign to attract time deposits with a maturity of five to twenty-four months commenced during the latter part of 2022 and has continued throughout 2023 and 2024 with current efforts centered on five months.

Shareholders’ Equity

Shareholders’ equity increased $29.2 million to $203.7 million at September 30, 2024 compared to September 30, 2023 due in part to a registered at-the-market offering that generated $7.5 million in capital during the fourth quarter of 2023. During the three and nine months ended September 30, 2024 there were no shares issued as part of the registered at-the-market offering. A total of 9,074 and 31,050 shares for net proceeds of $205,000 and $632,000 were issued as part of the Dividend Reinvestment Plan during the three and nine months ended September 30 2024. Accumulated other comprehensive loss of $5.3 million at September 30, 2024 decreased from a loss of $14.9 million at September 30, 2023 as a result of a decrease in net unrealized loss on available for sale securities to $2.6 million at September 30, 2024 from a net unrealized loss of $10.9 million at September 30, 2023, coupled with a decrease in loss of $1.3 million in the defined benefit plan obligation. The current level of shareholders’ equity equates to a book value per share of $26.96 at September 30, 2024 compared to $24.55 at September 30, 2023, and an equity to asset ratio of 9.02% at September 30, 2024 and 8.02% at September 30, 2023. Tangible book value per share (a non-GAAP measure) increased to $24.77 at September 30, 2024 compared to $22.20 at September 30, 2023. Dividends declared for the three and nine months ended September 30, 2024 and 2023 were $0.32 and $0.96 per share.

Penns Woods Bancorp, Inc. is the parent company of Jersey Shore State Bank, which operates sixteen branch offices providing financial services in Lycoming, Clinton, Centre, Montour, Union, and Blair Counties, and Luzerne Bank, which operates eight branch offices providing financial services in Luzerne County, and United Insurance Solutions, LLC, which offers insurance products. Investment and insurance products are offered through Jersey Shore State Bank’s subsidiary, The M Group, Inc. D/B/A The Comprehensive Financial Group.

NOTE: This press release contains financial information determined by methods other than in accordance with U.S. Generally Accepted Accounting Principles (“GAAP”). Management uses the non-GAAP measure of net income from core operations in its analysis of the company’s performance. This measure, as used by the Company, adjusts net income determined in accordance with GAAP to exclude the effects of special items, including significant gains or losses that are unusual in nature such as net securities gains and losses. Because these certain items and their impact on the Company’s performance are difficult to predict, management believes presentation of financial measures excluding the impact of such items provides useful supplemental information in evaluating the operating results of the Company’s core businesses. These disclosures should not be viewed as a substitute for net income determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies.

This press release may contain certain “forward-looking statements” including statements concerning plans, objectives, future events or performance and assumptions and other statements, which are statements other than statements of historical fact. The Company cautions readers that the following important factors, among others, may have affected and could in the future affect actual results and could cause actual results for subsequent periods to differ materially from those expressed in any forward-looking statement made by or on behalf of the Company herein: (i) the effect of changes in laws and regulations, including federal and state banking laws and regulations, and the associated costs of compliance with such laws and regulations either currently or in the future as applicable; (ii) the effect of changes in accounting policies and practices, as may be adopted by the regulatory agencies as well as by the Financial Accounting Standards Board, or of changes in the Company’s organization, compensation and benefit plans; (iii) the effect on the Company’s competitive position within its market area of the increasing consolidation within the banking and financial services industries, including the increased competition from larger regional and out-of-state banking organizations as well as non-bank providers of various financial services; (iv) the effect of changes in interest rates; (v) the effects of health emergencies, including the spread of infectious diseases or pandemics; or (vi) the effect of changes in the business cycle and downturns in the local, regional or national economies. For a list of other factors which could affect the Company’s results, see the Company’s filings with the Securities and Exchange Commission, including “Item 1A. Risk Factors,” set forth in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023.

You should not place undue reliance on any forward-looking statements. These statements speak only as of the date of this press release, even if subsequently made available by the Company on its website or otherwise. The Company undertakes no obligation to update or revise these statements to reflect events or circumstances occurring after the date of this press release.

Previous press releases and additional information can be obtained from the Company’s website at www.pwod.com.

| Contact: | Richard A. Grafmyre, Chief Executive Officer | |

| 110 Reynolds Street | ||

| Williamsport, PA 17702 | ||

| 570-322-1111 | e-mail: pwod@pwod.com | |

| PENNS WOODS BANCORP, INC. CONSOLIDATED BALANCE SHEET (UNAUDITED) |

|||||||||||

| (In Thousands, Except Share and Per Share Data) | September 30, | ||||||||||

| 2024 | 2023 | % Change | |||||||||

| ASSETS: | |||||||||||

| Noninterest-bearing balances | $ | 28,805 | $ | 26,651 | 8.08 | % | |||||

| Interest-bearing balances in other financial institutions | 10,889 | 8,939 | 21.81 | % | |||||||

| Total cash and cash equivalents | 39,694 | 35,590 | 11.53 | % | |||||||

| Investment debt securities, available for sale, at fair value | 197,466 | 184,667 | 6.93 | % | |||||||

| Investment equity securities, at fair value | 1,145 | 1,072 | 6.81 | % | |||||||

| Restricted investment in bank stock | 21,227 | 25,289 | (16.06)% | ||||||||

| Loans held for sale | 8,967 | 4,083 | 119.62 | % | |||||||

| Loans | 1,875,174 | 1,818,461 | 3.12 | % | |||||||

| Allowance for credit losses | (11,588 | ) | (12,890 | ) | (10.10)% | ||||||

| Loans, net | 1,863,586 | 1,805,571 | 3.21 | % | |||||||

| Premises and equipment, net | 27,975 | 30,746 | (9.01)% | ||||||||

| Accrued interest receivable | 11,433 | 10,500 | 8.89 | % | |||||||

| Bank-owned life insurance | 45,378 | 33,695 | 34.67 | % | |||||||

| Investment in limited partnerships | 6,966 | 8,275 | (15.82)% | ||||||||

| Goodwill | 16,450 | 16,450 | — | % | |||||||

| Intangibles | 133 | 235 | (43.40)% | ||||||||

| Operating lease right of use asset | 2,861 | 2,562 | 11.67 | % | |||||||

| Deferred tax asset | 3,034 | 6,961 | (56.41)% | ||||||||

| Other assets | 12,935 | 10,772 | 20.08 | % | |||||||

| TOTAL ASSETS | $ | 2,259,250 | $ | 2,176,468 | 3.80 | % | |||||

| LIABILITIES: | |||||||||||

| Interest-bearing deposits | $ | 1,247,399 | $ | 1,095,760 | 13.84 | % | |||||

| Noninterest-bearing deposits | 452,922 | 471,507 | (3.94)% | ||||||||

| Total deposits | 1,700,321 | 1,567,267 | 8.49 | % | |||||||

| Short-term borrowings | 78,305 | 193,746 | (59.58)% | ||||||||

| Long-term borrowings | 252,508 | 217,645 | 16.02 | % | |||||||

| Accrued interest payable | 5,509 | 2,716 | 102.84 | % | |||||||

| Operating lease liability | 2,936 | 2,619 | 12.10 | % | |||||||

| Other liabilities | 15,977 | 17,935 | (10.92)% | ||||||||

| TOTAL LIABILITIES | 2,055,556 | 2,001,928 | 2.68 | % | |||||||

| SHAREHOLDERS’ EQUITY: | |||||||||||

| Preferred stock, no par value, 3,000,000 shares authorized; no shares issued | — | — | n/a | ||||||||

| Common stock, par value $5.55, 22,500,000 shares authorized; 8,064,713 and 7,620,250 shares issued; 7,554,488 and 7,110,025 shares outstanding | 44,802 | 42,335 | 5.83 | % | |||||||

| Additional paid-in capital | 62,989 | 55,890 | 12.70 | % | |||||||

| Retained earnings | 114,008 | 104,067 | 9.55 | % | |||||||

| Accumulated other comprehensive loss: | |||||||||||

| Net unrealized loss on available for sale securities | (2,571 | ) | (10,886 | ) | 76.38 | % | |||||

| Defined benefit plan | (2,719 | ) | (4,051 | ) | 32.88 | % | |||||

| Treasury stock at cost, 510,225 shares | (12,815 | ) | (12,815 | ) | — | % | |||||

| TOTAL SHAREHOLDERS’ EQUITY | 203,694 | 174,540 | 16.70 | % | |||||||

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | $ | 2,259,250 | $ | 2,176,468 | 3.80 | % | |||||

| PENNS WOODS BANCORP, INC. CONSOLIDATED STATEMENT OF INCOME (UNAUDITED) |

||||||||||||||||||||||

| (In Thousands, Except Share and Per Share Data) | Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||

| 2024 | 2023 | % Change | 2024 | 2023 | % Change | |||||||||||||||||

| INTEREST AND DIVIDEND INCOME: | ||||||||||||||||||||||

| Loans including fees | $ | 25,632 | $ | 21,720 | 18.01 | % | $ | 74,021 | $ | 59,571 | 24.26 | % | ||||||||||

| Investment securities: | ||||||||||||||||||||||

| Taxable | 1,874 | 1,365 | 37.29 | % | 5,213 | 3,870 | 34.70 | % | ||||||||||||||

| Tax-exempt | 61 | 114 | (46.49)% | 233 | 410 | (43.17)% | ||||||||||||||||

| Dividend and other interest income | 621 | 722 | (13.99)% | 1,980 | 1,827 | 8.37 | % | |||||||||||||||

| TOTAL INTEREST AND DIVIDEND INCOME | 28,188 | 23,921 | 17.84 | % | 81,447 | 65,678 | 24.01 | % | ||||||||||||||

| INTEREST EXPENSE: | ||||||||||||||||||||||

| Deposits | 9,599 | 6,463 | 48.52 | % | 26,439 | 14,686 | 80.03 | % | ||||||||||||||

| Short-term borrowings | 932 | 2,412 | (61.36)% | 4,024 | 6,084 | (33.86)% | ||||||||||||||||

| Long-term borrowings | 2,601 | 1,714 | 51.75 | % | 7,667 | 3,892 | 96.99 | % | ||||||||||||||

| TOTAL INTEREST EXPENSE | 13,132 | 10,589 | 24.02 | % | 38,130 | 24,662 | 54.61 | % | ||||||||||||||

| NET INTEREST INCOME | 15,056 | 13,332 | 12.93 | % | 43,317 | 41,016 | 5.61 | % | ||||||||||||||

| PROVISION (RECOVERY) FOR CREDIT LOSSES | 740 | 1,372 | (46.06)% | (299 | ) | 263 | (213.69)% | |||||||||||||||

| NET INTEREST INCOME AFTER PROVISION (RECOVERY) OF CREDIT LOSSES | 14,316 | 11,960 | 19.70 | % | 43,616 | 40,753 | 7.03 | % | ||||||||||||||

| NON-INTEREST INCOME: | ||||||||||||||||||||||

| Service charges | 537 | 545 | (1.47)% | 1,551 | 1,557 | (0.39)% | ||||||||||||||||

| Net debt securities losses, available for sale | (5 | ) | (45 | ) | 88.89 | % | (40 | ) | (125 | ) | 68.00 | % | ||||||||||

| Net equity securities gains (losses) | 41 | (36 | ) | 213.89 | % | 24 | (35 | ) | 168.57 | % | ||||||||||||

| Bank-owned life insurance | 206 | 170 | 21.18 | % | 856 | 892 | (4.04)% | |||||||||||||||

| Gain on sale of loans | 416 | 257 | 61.87 | % | . | 1,021 | 732 | 39.48 | % | |||||||||||||

| Insurance commissions | 145 | 136 | 6.62 | % | 425 | 416 | 2.16 | % | ||||||||||||||

| Brokerage commissions | 164 | 142 | 15.49 | % | 521 | 448 | 16.29 | % | ||||||||||||||

| Loan broker income | 351 | 241 | 45.64 | % | 841 | 728 | 15.52 | % | ||||||||||||||

| Debit card income | 355 | 320 | 10.94 | % | 1,052 | 995 | 5.73 | % | ||||||||||||||

| Other | 211 | 145 | 45.52 | % | 657 | 546 | 20.33 | % | ||||||||||||||

| TOTAL NON-INTEREST INCOME | 2,421 | 1,875 | 29.12 | % | 6,908 | 6,154 | 12.25 | % | ||||||||||||||

| NON-INTEREST EXPENSE: | ||||||||||||||||||||||

| Salaries and employee benefits | 6,402 | 6,290 | 1.78 | % | 19,224 | 18,778 | 2.38 | % | ||||||||||||||

| Occupancy | 731 | 784 | (6.76)% | 2,394 | 2,422 | (1.16)% | ||||||||||||||||

| Furniture and equipment | 731 | 867 | (15.69)% | 2,436 | 2,503 | (2.68)% | ||||||||||||||||

| Software amortization | 245 | 237 | 3.38 | % | 657 | 593 | 10.79 | % | ||||||||||||||

| Pennsylvania shares tax | 351 | 280 | 25.36 | % | 1,022 | 807 | 26.64 | % | ||||||||||||||

| Professional fees | 530 | 719 | (26.29)% | 1,654 | 2,313 | (28.49)% | ||||||||||||||||

| Federal Deposit Insurance Corporation deposit insurance | 399 | 425 | (6.12)% | 1,179 | 1,122 | 5.08 | % | |||||||||||||||

| Marketing | 60 | 167 | (64.07)% | 209 | 594 | (64.81)% | ||||||||||||||||

| Intangible amortization | 26 | 25 | 4.00 | % | 77 | 92 | (16.30)% | |||||||||||||||

| Other | 1,409 | 1,378 | 2.25 | % | 4,652 | 4,275 | 8.82 | % | ||||||||||||||

| TOTAL NON-INTEREST EXPENSE | 10,884 | 11,172 | (2.58)% | 33,504 | 33,499 | 0.01 | % | |||||||||||||||

| INCOME BEFORE INCOME TAX PROVISION | 5,853 | 2,663 | 119.79 | % | 17,020 | 13,408 | 26.94 | % | ||||||||||||||

| INCOME TAX PROVISION | 1,052 | 439 | 139.64 | % | 3,022 | 2,355 | 28.32 | % | ||||||||||||||

| NET INCOME AVAILABLE TO COMMON SHAREHOLDERS’ | $ | 4,801 | $ | 2,224 | 115.87 | % | $ | 13,998 | $ | 11,053 | 26.64 | % | ||||||||||

| EARNINGS PER SHARE – BASIC | $ | 0.64 | $ | 0.31 | 106.45 | % | $ | 1.86 | $ | 1.56 | 19.23 | % | ||||||||||

| EARNINGS PER SHARE – DILUTED | $ | 0.64 | $ | 0.31 | 106.45 | % | $ | 1.86 | $ | 1.53 | 21.57 | % | ||||||||||

| WEIGHTED AVERAGE SHARES OUTSTANDING – BASIC | 7,544,344 | 7,072,440 | 6.67 | % | 7,528,758 | 7,064,336 | 6.57 | % | ||||||||||||||

| WEIGHTED AVERAGE SHARES OUTSTANDING – DILUTED | 7,544,344 | 7,228,940 | 4.36 | % | 7,528,758 | 7,220,836 | 4.26 | % | ||||||||||||||

| PENNS WOODS BANCORP, INC. AVERAGE BALANCES AND INTEREST RATES (UNAUDITED) |

||||||||||||||||||

| Three Months Ended | ||||||||||||||||||

| (Dollars in Thousands) | September 30, 2024 | September 30, 2023 | ||||||||||||||||

| Average Balance (1) |

Interest | Average Rate |

Average Balance (1) |

Interest | Average Rate |

|||||||||||||

| ASSETS: | ||||||||||||||||||

| Tax-exempt loans (3) | $ | 69,831 | $ | 534 | 3.04 | % | $ | 68,243 | $ | 462 | 2.69 | % | ||||||

| All other loans | 1,805,097 | 25,210 | 5.56 | % | 1,730,669 | 21,355 | 4.90 | % | ||||||||||

| Total loans (2) | 1,874,928 | 25,744 | 5.46 | % | 1,798,912 | 21,817 | 4.81 | % | ||||||||||

| Taxable securities | 207,888 | 2,355 | 4.61 | % | 193,019 | 1,945 | 4.09 | % | ||||||||||

| Tax-exempt securities (3) | 11,475 | 77 | 2.73 | % | 20,777 | 144 | 2.81 | % | ||||||||||

| Total securities | 219,363 | 2,432 | 4.51 | % | 213,796 | 2,089 | 3.96 | % | ||||||||||

| Interest-bearing balances in other financial institutions | 10,167 | 140 | 5.48 | % | 11,868 | 142 | 4.75 | % | ||||||||||

| Total interest-earning assets | 2,104,458 | 28,316 | 5.36 | % | 2,024,576 | 24,048 | 4.72 | % | ||||||||||

| Other assets | 132,244 | 131,451 | ||||||||||||||||

| TOTAL ASSETS | $ | 2,236,702 | $ | 2,156,027 | ||||||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY: | ||||||||||||||||||

| Savings | $ | 214,050 | 282 | 0.52 | % | $ | 225,357 | 181 | 0.32 | % | ||||||||

| Super Now deposits | 220,825 | 1,133 | 2.04 | % | 244,387 | 1,174 | 1.91 | % | ||||||||||

| Money market deposits | 320,908 | 2,781 | 3.45 | % | 294,006 | 1,862 | 2.51 | % | ||||||||||

| Time deposits | 482,335 | 5,403 | 4.46 | % | 342,450 | 3,246 | 3.76 | % | ||||||||||

| Total interest-bearing deposits | 1,238,118 | 9,599 | 3.08 | % | 1,106,200 | 6,463 | 2.32 | % | ||||||||||

| Short-term borrowings | 66,795 | 932 | 5.54 | % | 173,364 | 2,412 | 5.52 | % | ||||||||||

| Long-term borrowings | 250,938 | 2,601 | 4.12 | % | 204,901 | 1,714 | 3.32 | % | ||||||||||

| Total borrowings | 317,733 | 3,533 | 4.42 | % | 378,265 | 4,126 | 4.33 | % | ||||||||||

| Total interest-bearing liabilities | 1,555,851 | 13,132 | 3.35 | % | 1,484,465 | 10,589 | 2.83 | % | ||||||||||

| Demand deposits | 453,169 | 471,494 | ||||||||||||||||

| Other liabilities | 27,558 | 24,193 | ||||||||||||||||

| Shareholders’ equity | 200,124 | 175,875 | ||||||||||||||||

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | $ | 2,236,702 | $ | 2,156,027 | ||||||||||||||

| Interest rate spread (3) | 2.01 | % | 1.89 | % | ||||||||||||||

| Net interest income/margin (3) | $ | 15,184 | 2.88 | % | $ | 13,459 | 2.65 | % | ||||||||||

1. Information on this table has been calculated using average daily balance sheets to obtain average balances.

2. Non-accrual loans have been included with loans for the purpose of analyzing net interest earnings.

3. Income and rates on fully taxable equivalent basis include an adjustment for the difference between annual income

from tax-exempt obligations and the taxable equivalent of such income at the standard tax rate of 21%

| Three Months Ended September 30, | ||||||

| 2024 | 2023 | |||||

| Total interest income | $ | 28,188 | $ | 23,921 | ||

| Total interest expense | 13,132 | 10,589 | ||||

| Net interest income (GAAP) | 15,056 | 13,332 | ||||

| Tax equivalent adjustment | 128 | 127 | ||||

| Net interest income (fully taxable equivalent) (non-GAAP) | $ | 15,184 | $ | 13,459 | ||

| PENNS WOODS BANCORP, INC. AVERAGE BALANCES AND INTEREST RATES (UNAUDITED) |

||||||||||||||||||

| Nine Months Ended | ||||||||||||||||||

| September 30, 2024 | September 30, 2023 | |||||||||||||||||

| (Dollars in Thousands) | Average Balance (1) |

Interest | Average Rate |

Average Balance (1) |

Interest | Average Rate |

||||||||||||

| ASSETS: | ||||||||||||||||||

| Tax-exempt loans (3) | $ | 69,455 | $ | 1,490 | 2.87 | % | $ | 66,372 | $ | 1,371 | 2.76 | % | ||||||

| All other loans | 1,792,518 | 72,844 | 5.43 | % | 1,668,596 | 58,488 | 4.69 | % | ||||||||||

| Total loans (2) | 1,861,973 | 74,334 | 5.33 | % | 1,734,968 | 59,859 | 4.61 | % | ||||||||||

| Taxable securities | 203,964 | 6,795 | 4.45 | % | 188,477 | 5,331 | 3.78 | % | ||||||||||

| Tax-exempt securities (3) | 13,625 | 295 | 2.89 | % | 25,837 | 519 | 2.69 | % | ||||||||||

| Total securities | 217,589 | 7,090 | 4.35 | % | 214,314 | 5,850 | 3.65 | % | ||||||||||

| Interest-bearing balances in other financial institutions | 10,382 | 398 | 5.12 | % | 10,619 | 366 | 4.61 | % | ||||||||||

| Total interest-earning assets | 2,089,944 | 81,822 | 5.24 | % | 1,959,901 | 66,075 | 4.41 | % | ||||||||||

| Other assets | 131,000 | 132,133 | ||||||||||||||||

| TOTAL ASSETS | $ | 2,220,944 | $ | 2,092,034 | ||||||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY: | ||||||||||||||||||

| Savings | $ | 217,056 | 811 | 0.50 | % | $ | 233,784 | 456 | 0.26 | % | ||||||||

| Super Now deposits | 218,307 | 3,303 | 2.02 | % | 293,636 | 3,026 | 1.38 | % | ||||||||||

| Money market deposits | 308,027 | 7,734 | 3.35 | % | 292,490 | 4,807 | 2.20 | % | ||||||||||

| Time deposits | 446,158 | 14,591 | 4.37 | % | 264,855 | 6,397 | 3.23 | % | ||||||||||

| Total interest-bearing deposits | 1,189,548 | 26,439 | 2.97 | % | 1,084,765 | 14,686 | 1.81 | % | ||||||||||

| Short-term borrowings | 96,669 | 4,024 | 5.60 | % | 155,136 | 6,084 | 5.26 | % | ||||||||||

| Long-term borrowings | 256,960 | 7,667 | 3.99 | % | 169,276 | 3,892 | 3.07 | % | ||||||||||

| Total borrowings | 353,629 | 11,691 | 4.43 | % | 324,412 | 9,976 | 4.12 | % | ||||||||||

| Total interest-bearing liabilities | 1,543,177 | 38,130 | 3.30 | % | 1,409,177 | 24,662 | 2.34 | % | ||||||||||

| Demand deposits | 454,967 | 484,662 | ||||||||||||||||

| Other liabilities | 31,133 | 26,334 | ||||||||||||||||

| Shareholders’ equity | 191,667 | 171,861 | ||||||||||||||||

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | $ | 2,220,944 | $ | 2,092,034 | ||||||||||||||

| Interest rate spread (3) | 1.94 | % | 2.07 | % | ||||||||||||||

| Net interest income/margin (3) | $ | 43,692 | 2.79 | % | $ | 41,413 | 2.82 | % | ||||||||||

1. Information on this table has been calculated using average daily balance sheets to obtain average balances.

2. Non-accrual loans have been included with loans for the purpose of analyzing net interest earnings.

3. Income and rates on fully taxable equivalent basis include an adjustment for the difference between annual income

from tax-exempt obligations and the taxable equivalent of such income at the standard tax rate of 21%

| Nine months ended September 30, | ||||||

| 2024 | 2023 | |||||

| Total interest income | $ | 81,447 | $ | 65,678 | ||

| Total interest expense | 38,130 | 24,662 | ||||

| Net interest income (GAAP) | 43,317 | 41,016 | ||||

| Tax equivalent adjustment | 375 | 397 | ||||

| Net interest income (fully taxable equivalent) (non-GAAP) | $ | 43,692 | $ | 41,413 | ||

| (Dollars in Thousands, Except Per Share Data, Unaudited) | Quarter Ended | |||||||||||||||||||

| 9/30/2024 | 6/30/2024 | 3/31/2024 | 12/31/2023 | 9/30/2023 | ||||||||||||||||

| Operating Data | ||||||||||||||||||||

| Net income | $ | 4,801 | $ | 5,390 | $ | 3,808 | $ | 5,555 | $ | 2,224 | ||||||||||

| Net interest income | 15,056 | 14,515 | 13,746 | 13,948 | 13,332 | |||||||||||||||

| Provision (recovery) for credit losses | 740 | (1,177 | ) | 138 | (1,742 | ) | 1,372 | |||||||||||||

| Net security gains (losses) | 36 | (19 | ) | (33 | ) | (18 | ) | (81 | ) | |||||||||||

| Non-interest income, excluding net security gains (losses) | 2,385 | 2,044 | 2,495 | 2,239 | 1,956 | |||||||||||||||

| Non-interest expense | 10,884 | 10,996 | 11,623 | 10,997 | 11,172 | |||||||||||||||

| Performance Statistics | ||||||||||||||||||||

| Net interest margin | 2.88 | % | 2.83 | % | 2.69 | % | 2.73 | % | 2.65 | % | ||||||||||

| Annualized cost of total deposits | 2.27 | % | 2.14 | % | 2.01 | % | 1.89 | % | 1.64 | % | ||||||||||

| Annualized non-interest income to average assets | 0.43 | % | 0.37 | % | 0.45 | % | 0.41 | % | 0.35 | % | ||||||||||

| Annualized non-interest expense to average assets | 1.95 | % | 1.98 | % | 2.10 | % | 2.02 | % | 2.07 | % | ||||||||||

| Annualized return on average assets | 0.86 | % | 0.97 | % | 0.69 | % | 1.02 | % | 0.41 | % | ||||||||||

| Annualized return on average equity | 9.60 | % | 11.12 | % | 8.03 | % | 12.60 | % | 5.06 | % | ||||||||||

| Annualized net loan charge-offs (recoveries) to average loans | 0.07 | % | (0.09)% | 0.08 | % | (0.05)% | 0.01 | % | ||||||||||||

| Net charge-offs (recoveries) | 328 | (396 | ) | 380 | (209 | ) | 33 | |||||||||||||

| Efficiency ratio | 62.26 | % | 66.25 | % | 71.41 | % | 67.78 | % | 72.76 | % | ||||||||||

| Per Share Data | ||||||||||||||||||||

| Basic earnings per share | $ | 0.64 | $ | 0.72 | $ | 0.51 | $ | 0.77 | $ | 0.31 | ||||||||||

| Diluted earnings per share | 0.64 | 0.72 | 0.51 | 0.77 | 0.31 | |||||||||||||||

| Dividend declared per share | 0.32 | 0.32 | 0.32 | 0.32 | 0.32 | |||||||||||||||

| Book value | 26.96 | 26.13 | 25.72 | 25.51 | 24.55 | |||||||||||||||

| Tangible book value (Non-GAAP) | 24.77 | 23.93 | 23.50 | 23.29 | 22.20 | |||||||||||||||

| Common stock price: | ||||||||||||||||||||

| High | 23.98 | 21.08 | 22.64 | 23.64 | 27.17 | |||||||||||||||

| Low | 19.29 | 17.17 | 18.44 | 20.05 | 20.70 | |||||||||||||||

| Close | 23.79 | 20.55 | 19.41 | 22.51 | 21.08 | |||||||||||||||

| Weighted average common shares: | ||||||||||||||||||||

| Basic | 7,544 | 7,529 | 7,513 | 7,255 | 7,072 | |||||||||||||||

| Fully Diluted | 7,544 | 7,529 | 7,513 | 7,255 | 7,229 | |||||||||||||||

| End-of-period common shares: | ||||||||||||||||||||

| Issued | 8,065 | 8,052 | 8,036 | 8,019 | 7,620 | |||||||||||||||

| Treasury | (510 | ) | (510 | ) | (510 | ) | (510 | ) | (510 | ) | ||||||||||

| (Dollars in Thousands, Unaudited) | Quarter Ended | |||||||||||||||||||

| 9/30/2024 | 6/30/2024 | 3/31/2024 | 12/31/2023 | 9/30/2023 | ||||||||||||||||

| Financial Condition Data: | ||||||||||||||||||||

| General | ||||||||||||||||||||

| Total assets | $ | 2,259,250 | $ | 2,234,617 | $ | 2,210,116 | $ | 2,204,809 | $ | 2,176,468 | ||||||||||

| Loans, net | 1,863,586 | 1,855,054 | 1,843,805 | 1,828,318 | 1,805,571 | |||||||||||||||

| Goodwill | 16,450 | 16,450 | 16,450 | 16,450 | 16,450 | |||||||||||||||

| Intangibles | 133 | 158 | 184 | 210 | 235 | |||||||||||||||

| Total deposits | 1,700,321 | 1,648,093 | 1,618,562 | 1,589,493 | 1,567,267 | |||||||||||||||

| Noninterest-bearing | 452,922 | 461,092 | 471,451 | 471,173 | 471,507 | |||||||||||||||

| Savings | 211,560 | 218,354 | 220,932 | 219,287 | 226,897 | |||||||||||||||

| NOW | 218,279 | 209,906 | 208,073 | 214,888 | 220,730 | |||||||||||||||

| Money Market | 321,614 | 320,101 | 299,916 | 299,353 | 291,889 | |||||||||||||||

| Time Deposits | 328,294 | 310,187 | 292,372 | 260,067 | 249,550 | |||||||||||||||

| Brokered Deposits | 167,652 | 128,453 | 125,818 | 124,725 | 106,694 | |||||||||||||||

| Total interest-bearing deposits | 1,247,399 | 1,187,001 | 1,147,111 | 1,118,320 | 1,095,760 | |||||||||||||||

| Core deposits* | 1,204,375 | 1,209,453 | 1,200,372 | 1,204,701 | 1,211,023 | |||||||||||||||

| Shareholders’ equity | 203,694 | 197,087 | 193,517 | 191,556 | 174,540 | |||||||||||||||

| Asset Quality | ||||||||||||||||||||

| Non-performing loans | $ | 7,940 | $ | 6,784 | $ | 7,958 | $ | 3,148 | $ | 3,683 | ||||||||||

| Non-performing loans to total assets | 0.35 | % | 0.30 | % | 0.36 | % | 0.14 | % | 0.17 | % | ||||||||||

| Allowance for credit losses on loans | 11,588 | 11,234 | 11,542 | 11,446 | 12,890 | |||||||||||||||

| Allowance for credit losses on loans to total loans | 0.62 | % | 0.60 | % | 0.62 | % | 0.62 | % | 0.71 | % | ||||||||||

| Allowance for credit losses on loans to non-performing loans | 145.94 | % | 165.60 | % | 145.04 | % | 363.60 | % | 349.99 | % | ||||||||||

| Non-performing loans to total loans | 0.42 | % | 0.36 | % | 0.43 | % | 0.17 | % | 0.20 | % | ||||||||||

| Capitalization | ||||||||||||||||||||

| Shareholders’ equity to total assets | 9.02 | % | 8.82 | % | 8.76 | % | 8.69 | % | 8.02 | % | ||||||||||

* Core deposits are defined as total deposits less time deposits and brokered deposits.

| Reconciliation of GAAP and Non-GAAP Financial Measures (UNAUDITED) |

||||||||||||||||

| (Dollars in Thousands, Except Per Share Data, Unaudited) | Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| GAAP net income | $ | 4,801 | $ | 2,224 | $ | 13,998 | $ | 11,053 | ||||||||

| Net securities (gains) losses, net of tax | (28 | ) | 64 | 13 | 126 | |||||||||||

| Non-GAAP core earnings | $ | 4,773 | $ | 2,288 | $ | 14,011 | $ | 11,179 | ||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Return on average assets (ROA) | 0.86 | % | 0.41 | % | 0.84 | % | 0.70 | % | ||||||||

| Net securities (gains) losses, net of tax | (0.01)% | 0.01 | % | — | % | 0.01 | % | |||||||||

| Non-GAAP core ROA | 0.85 | % | 0.42 | % | 0.84 | % | 0.71 | % | ||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Return on average equity (ROE) | 9.60 | % | 5.06 | % | 9.74 | % | 8.58 | % | ||||||||

| Net securities (gains) losses, net of tax | (0.06)% | 0.14 | % | 0.01 | % | 0.09 | % | |||||||||

| Non-GAAP core ROE | 9.54 | % | 5.20 | % | 9.75 | % | 8.67 | % | ||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Basic earnings per share (EPS) | $ | 0.64 | $ | 0.31 | $ | 1.86 | $ | 1.56 | ||||||||

| Net securities (gains) losses, net of tax | (0.01 | ) | 0.01 | — | 0.02 | |||||||||||

| Non-GAAP basic core EPS | $ | 0.63 | $ | 0.32 | $ | 1.86 | $ | 1.58 | ||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Diluted EPS | $ | 0.64 | $ | 0.31 | $ | 1.86 | $ | 1.53 | ||||||||

| Net securities (gains) losses, net of tax | (0.01 | ) | 0.01 | — | 0.02 | |||||||||||

| Non-GAAP diluted core EPS | $ | 0.63 | $ | 0.32 | $ | 1.86 | $ | 1.55 | ||||||||

| (Dollars in Thousands, Except Share and Per Share Data, Unaudited) | Quarter Ended | |||||||||||||||||||

| 9/30/2024 | 6/30/2024 | 3/31/2024 | 12/31/2023 | 9/30/2023 | ||||||||||||||||

| Total shareholders’ equity | $ | 203,694 | $ | 197,087 | $ | 193,517 | $ | 191,556 | $ | 174,540 | ||||||||||

| Goodwill | (16,450 | ) | (16,450 | ) | (16,450 | ) | (16,450 | ) | (16,450 | ) | ||||||||||

| Intangibles | (133 | ) | (158 | ) | (184 | ) | (210 | ) | (235 | ) | ||||||||||

| Tangible shareholders’ equity | $ | 187,111 | $ | 180,479 | $ | 176,883 | $ | 174,896 | $ | 157,855 | ||||||||||

| Shares outstanding | 7,554,488 | 7,541,474 | 7,525,372 | 7,508,994 | 7,110,025 | |||||||||||||||

| Book value per share | $ | 26.96 | $ | 26.13 | $ | 25.72 | $ | 25.51 | $ | 24.55 | ||||||||||

| Tangible book value per share (Non-GAAP) | $ | 24.77 | $ | 23.93 | $ | 23.50 | $ | 23.29 | $ | 22.20 | ||||||||||

![]()

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Analyst Report: Comerica, Inc.

Summary

Based in Dallas, Comerica has 430 bank locations in Texas, California, Michigan, Arizona, and Florida, with some select business lines in several other states, as well as in Canada and Mexico. The company organizes its business int

Upgrade to begin using premium research reports and get so much more.

Exclusive reports, detailed company profiles, and best-in-class trade insights to take your portfolio to the next level

Chitosan Market to Surpass Value of $62.76 Billion by 2031: SkyQuest Technology

Westford, US, Oct. 24, 2024 (GLOBE NEWSWIRE) — SkyQuest projects that the global chitosan market size will reach a value of USD 62.76 Billion by 2031, with a CAGR of 21.3% during the forecast period (2024-2031). Global market is predicted to witness explosive growth due to the ever-growing demand among consumers for organic and natural products. Chitosan fits the green and eco-friendly choices that consumers are increasingly opting for The demand for chitosan is also being driven by the growing pharmaceutical sector and growing health consciousness attributed to its excellent properties in tissue engineering, drug delivery systems, and wound healing.

Request Sample of the Report- https://www.skyquestt.com/sample-request/chitosan-market

Asia-Pacific Dominance Due to Its Large Customer Base

The global chitosan market share was dominated by Asia-Pacific. The success of the region is owed to a number of factors. Among such factors are the strong presence of significant manufacturers, easy access to raw materials, and the strong food and pharmaceutical industries, which use significant quantities of chitosan in various applications. With more than 4.5 billion people living in its territory and growing sectors of industry fast, Asia-Pacific is one significant source of a considerable customer base and a lucrative market for chitosan products.

On the contrary, the North America chitosan market is anticipated to grow at the fastest rate. This growth is driven by growing awareness of the diverse benefits Chitosan could offer in most medical, cosmetic, and agricultural applications. In addition, robust legislation on green innovation combined with overwhelming demand for green and organic products has also contributed to better observance of chitosan application in North America.

Chitosan Market Report Overview:

| Report Coverage | Details |

| Market Revenue in 2023 | USD 13.39 Billion |

| Estimated Value by 2031 | USD 62.76 Billion |

| Growth Rate | Poised to grow at a CAGR of 21.3 % |

| Forecast Period | 2024–2031 |

| Forecast Units | Value (USD Billion) |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Trends |

| Segments Covered | Source, Application, Region |

| Geographies Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa |

| Report Highlights | Chitosan and its Rising Demand |

| Key Market Opportunities | Emerging Applications of Chitosan |

| Key Market Drivers | Advancements in Extraction and Processing Technologies |

Get Customized Reports with your Requirements, Free – https://www.skyquestt.com/speak-with-analyst/chitosan-market

Shrimp-Based Chitosan and its Prevalence Due to the Seafood Industry’s Waste

The shrimp-based chitosan segment held the largest market share and also the biggest category in terms of source. The wide prevalence of chitosan derived from shrimp can be traced to the sheer amount of waste from shrimp produced by the seafood processing industry. Increased demand for shrimp, which is increasingly becoming a popular seafood product, has increased the market for shrimp-based chitosan. Shrimp shells are full of chitin. Moreover, high-quality and pure chitosan produced from shrimp is highly in demand by different end-use industries such as cosmetics, agriculture, and pharmaceuticals.

Rapid Growth of Chitosan in Biomedical & Pharmaceuticals Industry Due to Its Antibacterial Properties

The biomedical & pharmaceuticals segment is the fastest-growing category in the Chitosan market. Due to its outstanding antibacterial, biodegradable, and biocompatibility properties, chitosan is a great material for various medicinal applications. It is now gaining high application in tissue engineering, drug delivery systems, wound healing, and other fields of medicinal practice. The biomedical & pharmaceuticals industry is increasingly growing due to factors such as the increasing frequency of chronic illnesses, advanced drug delivery technologies, and demand for regenerative medicine.

Is this report aligned with your requirements? Purchase Inquiry- https://www.skyquestt.com/buy-now/chitosan-market

Chitosan Market Drivers

- Advancements in Extraction and Processing Technologies

- Agricultural Applications

- Growing Demand for Biodegradable Products

Chitosan Market Restraints

- High Production Costs

- Variability in Quality

- Regulatory Challenges

Chitosan Market Key Players

- Koyo World

- Primex Iceland

- Primex EHF

- KitoZyme SA

- CarboMer Inc.

- United Chitotechnologies Inc.

- Biophrame Technologies

- Primex

- G.T.C. Bio Corporation

- Golden-Shell Pharmaceutical Co., Ltd.

Key Questions Covered in the Chitosan Market Report

- What are the factors driving the growth of the global chitosan market?

- Which is the dominant region within the market?

- What are the major players operating within the market?

This report provides the following insights:

Analysis of key drivers (advancements in extraction & processing technologies, growing demand for biodegradable products), restraints (high production costs, regulatory challenges), opportunities (emerging applications, R&D), and challenges (sustainability of raw materials, competition from synthetic alternatives) influencing the growth of the chitosan market.

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the market.

- Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product launches in the market.

- Market Development: Comprehensive information on lucrative emerging regions.

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the market.

- Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players.

Related Report:

Biochar Market: Global Opportunity Analysis and Forecast, 2024-2031

Green Ammonia Market: Global Opportunity Analysis and Forecast, 2024-2031

Activated Carbon Market: Global Opportunity Analysis and Forecast, 2024-2031

Specialty Chemicals Market: Global Opportunity Analysis and Forecast, 2024-2031

Lubricants Market: Global Opportunity Analysis and Forecast, 2024-2031

About Us:

SkyQuest is an IP focused Research and Investment Bank and Accelerator of Technology and assets. We provide access to technologies, markets and finance across sectors viz. Life Sciences, CleanTech, AgriTech, NanoTech and Information & Communication Technology.

We work closely with innovators, inventors, innovation seekers, entrepreneurs, companies and investors alike in leveraging external sources of R&D. Moreover, we help them in optimizing the economic potential of their intellectual assets. Our experiences with innovation management and commercialization have expanded our reach across North America, Europe, ASEAN and Asia Pacific.

Contact:

Mr. Jagraj Singh

SkyQuest Technology

1 Apache Way,

Westford,

Massachusetts 01886

USA (+1) 351-333-4748

Email: sales@skyquestt.com

Visit Our Website: https://www.skyquestt.com/

![]()

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.