Meta CEO Zuckerberg Dismisses Workers Making Over Six Figures For Taking Advantage Of Company Food Delivery Service

Mark Zuckerberg’s tech giant Meta recently dismissed 24 employees from its Los Angeles office for exploiting the company’s $25 meal voucher system to buy nonfood items such as toothpaste, laundry detergent and even wine glasses, according to employees’ posts on the anonymous workplace chat app Blind.

The vouchers, intended for food deliveries when working at the office, had been misused for ordering household items, an issue Meta addressed swiftly by terminating those involved.

Don’t Miss:

Meta, valued at $1.5 trillion, is known for its lavish perks, including free meals at its larger offices, a strategy designed to entice employees back into the workplace amid the rise of remote work. In smaller offices where on-site dining options aren’t available, employees are provided with meal credits for delivery services like Grubhub. This benefit, however, appears to have been stretched beyond its intended purpose by some staff.

According to The Financial Times, the misuse of meal vouchers had been happening for a while, with some employees regularly ordering cosmetics and groceries. Despite initial warnings, the situation persisted, leading to the recent terminations. Surprisingly, these sackings also involved some high-earning engineers with six-figure salaries.

Trending: This Adobe-backed AI marketing startup went from a $5 to $85 million valuation working with brands like L’Oréal, Hasbro, and Sweetgreen in just three years – here’s how there’s an opportunity to invest at $1,000 for only $0.50/share today.

While the staff involved had been given prior warnings, their continued misuse ultimately resulted in their dismissals.

This news comes as Meta makes broader cuts across several divisions, including WhatsApp, Instagram and its virtual reality unit. The company cited restructuring efforts aimed at realigning resources with long-term strategic goals.

Meta spokespersons have not directly commented on the meal voucher scandal but reiterated that restructuring involves shifting teams and roles to more critical business areas.

See Also: Maker of the $60,000 foldable home has 3 factory buildings, 600+ houses built, and big plans to solve housing — you can become an investor for $0.80 per share today.

“Today, a few teams at Meta are making changes to ensure resources are aligned with their long-term strategic goals and location strategy,” said Meta spokesperson David Arnold in a statement. “This includes moving some teams to different locations and reallocating employees into new roles. In cases where a role is eliminated, we work hard to find new opportunities within the company.”

‘You could at least kiss me’: Lawsuit reveals decades of employee texts sent to billionaire Marc Lasry in blackmail scheme

Billionaire chief executive and chairman Marc Lasry is suing ex-employee Gina Strum, alleging she carried on a decade-long campaign of harassment, lies, and blackmail and is now trying to illicitly siphon millions from Lasry and his firm.

The suit—filed jointly with his sister Sonia Gardner and the firm they cofounded together, Avenue Capital—lists a litany of alleged grievances against Strum, including obsessive and inappropriate texts to Lasry that he repeatedly rebuffed, even as they tried to placate her with phone calls, meetings, and emails. Lasry and Gardner alleged they suffered through it because they feared Strum would carry out her threats to take down both Lasry and the $12 billion global investment firm he built for 30 years alongside his sibling, the complaint states. For years, Strum allegedly alternated between praising the firm when she felt she was on the receiving end of attention and money, and then menacing them when that stopped.

The complaint alleges that Strum recently escalated her threats, saying she would make it “really, really ugly” for Lasry and Avenue Capital unless she was paid $50 million, and would destroy Lasry’s reputation personally. The suit also includes alleged lines from text messages and emails Strum sent to Lasry over the years that the complaint described as “personal, obsessive, and simply inappropriate.” The suit alleges Strum also sent photos and videos of herself to Lasry in low-cut tops, seeking his response.

For instance, Strum allegedly wrote: “U wonder why I love you so much.” And then, “Did you forget about me? My life doesn’t really work without you. Stop punishing me.” Plus, “You are a lovebug to me.” Also: “And one more thought- if I had to go through therapy and all this shit just to talk to you. You could at least kiss me. We would know everything then.”

The complaint alleges Strum would compliment Lasry’s appearance, including a black turtleneck that caused her to start “sweating.” She also allegedly told him he looked “cute,” and allegedly updated him when she went to be checked out for “Girly bits.”

Another alleges Strum wrote she was “def lonely and flirting with you.” The complaint states that Lasry apologized to Strum for being lonely, and said he could be a friend to her, “but it can never be more than that.”

The suit says Strum was employed by Avenue Capital from 2009 to 2013 but worked as a consultant on occasion in the years that followed. Strum’s LinkedIn lists her employment with Avenue Capital as managing director from 2009 to 2017. Avenue Capital’s specialty is distressed assets, which includes investing in real estate debt. Lasry has an estimated net worth of almost $2 billion, per Forbes. Unrelatedly, he’s a longtime democratic donor, according to campaign finance data from the Federal Election Commission.

Alkermes's Earnings: A Preview

Alkermes ALKS is gearing up to announce its quarterly earnings on Thursday, 2024-10-24. Here’s a quick overview of what investors should know before the release.

Analysts are estimating that Alkermes will report an earnings per share (EPS) of $0.74.

Anticipation surrounds Alkermes’s announcement, with investors hoping to hear about both surpassing estimates and receiving positive guidance for the next quarter.

New investors should understand that while earnings performance is important, market reactions are often driven by guidance.

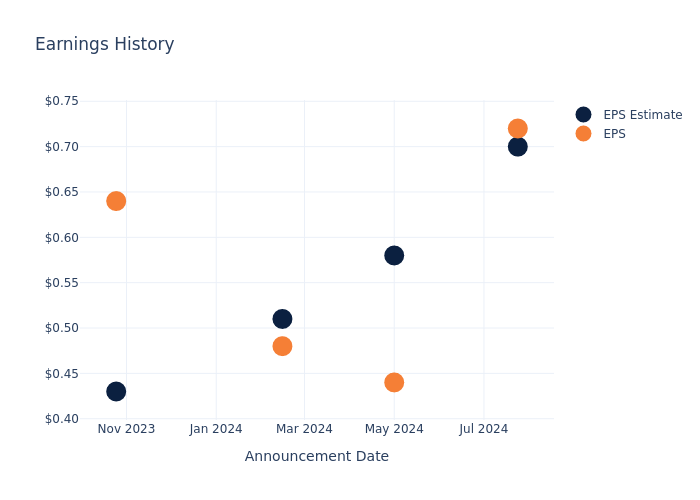

Overview of Past Earnings

The company’s EPS beat by $0.02 in the last quarter, leading to a 5.77% increase in the share price on the following day.

Here’s a look at Alkermes’s past performance and the resulting price change:

| Quarter | Q2 2024 | Q1 2024 | Q4 2023 | Q3 2023 |

|---|---|---|---|---|

| EPS Estimate | 0.70 | 0.58 | 0.51 | 0.43 |

| EPS Actual | 0.72 | 0.44 | 0.48 | 0.64 |

| Price Change % | 6.0% | -1.0% | -1.0% | 5.0% |

Performance of Alkermes Shares

Shares of Alkermes were trading at $28.1 as of October 22. Over the last 52-week period, shares are up 22.14%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

Analysts’ Perspectives on Alkermes

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Alkermes.

Analysts have provided Alkermes with 7 ratings, resulting in a consensus rating of Outperform. The average one-year price target stands at $41.14, suggesting a potential 46.41% upside.

Analyzing Analyst Ratings Among Peers

The following analysis focuses on the analyst ratings and average 1-year price targets of Ultragenyx Pharmaceutical, TG Therapeutics and Blueprint Medicines, three prominent industry players, providing insights into their relative performance expectations and market positioning.

- The consensus outlook from analysts is an Outperform trajectory for Ultragenyx Pharmaceutical, with an average 1-year price target of $91.64, indicating a potential 226.12% upside.

- The prevailing sentiment among analysts is an Buy trajectory for TG Therapeutics, with an average 1-year price target of $38.0, implying a potential 35.23% upside.

- Analysts currently favor an Buy trajectory for Blueprint Medicines, with an average 1-year price target of $126.6, suggesting a potential 350.53% upside.

Peer Metrics Summary

Within the peer analysis summary, vital metrics for Ultragenyx Pharmaceutical, TG Therapeutics and Blueprint Medicines are presented, shedding light on their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Alkermes | Outperform | -35.35% | $337.66M | 7.20% |

| Ultragenyx Pharmaceutical | Outperform | 35.75% | $125.75M | -45.96% |

| TG Therapeutics | Buy | 357.05% | $65.16M | 4.07% |

| Blueprint Medicines | Buy | 139.98% | $130.56M | -15.85% |

Key Takeaway:

Alkermes ranks at the bottom for Revenue Growth and Gross Profit, while it is in the middle for Return on Equity.

About Alkermes

Alkermes PLC is a fully integrated biotechnology company that applies its proprietary technologies to research, develop, and commercialize pharmaceutical products designed for unmet medical needs in therapeutic areas. The company utilizes several to develop and commercialize products and, in so doing, access technological, financial, marketing, manufacturing, and other resources. Alkermes either purchases active drug products from third parties or receives them from its third-party licensees to formulate products using its technologies. It operates in U.S., which derives maximum revenue, Ireland and Rest of the world.

Breaking Down Alkermes’s Financial Performance

Market Capitalization: With restricted market capitalization, the company is positioned below industry averages. This reflects a smaller scale relative to peers.

Negative Revenue Trend: Examining Alkermes’s financials over 3 months reveals challenges. As of 30 June, 2024, the company experienced a decline of approximately -35.35% in revenue growth, reflecting a decrease in top-line earnings. In comparison to its industry peers, the company trails behind with a growth rate lower than the average among peers in the Health Care sector.

Net Margin: Alkermes’s net margin surpasses industry standards, highlighting the company’s exceptional financial performance. With an impressive 22.89% net margin, the company effectively manages costs and achieves strong profitability.

Return on Equity (ROE): The company’s ROE is a standout performer, exceeding industry averages. With an impressive ROE of 7.2%, the company showcases effective utilization of equity capital.

Return on Assets (ROA): Alkermes’s financial strength is reflected in its exceptional ROA, which exceeds industry averages. With a remarkable ROA of 4.22%, the company showcases efficient use of assets and strong financial health.

Debt Management: Alkermes’s debt-to-equity ratio is below the industry average at 0.29, reflecting a lower dependency on debt financing and a more conservative financial approach.

To track all earnings releases for Alkermes visit their earnings calendar on our site.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Dean Graziosi and Mastermind.com Introduce the Upgraded Mastermind Business System: a Complete Solution for Business Owners to Scale with Information Products

Scottsdale, AZ October 23, 2024 –(PR.com)– Dean Graziosi, renowned entrepreneur and Co-Founder of Mastermind.com, has launched the newly upgraded Mastermind Business System, an all-in-one platform designed to help business owners transform their knowledge into profitable digital products. This innovative system combines expert education, personalized support, and easy-to-use tools, making it a comprehensive solution for scaling digital ventures.

Dean Graziosi, a multiple New York Times best-selling author, created the Mastermind Business System to offer a streamlined approach for business owners of all backgrounds—whether they are seasoned entrepreneurs or new to digital products. With this enhanced version, business owners can access proven tools, strategies, and real-time support that pave the way for sustainable success.

For more details about the Mastermind Business System, visit joinmbs.com.

“With the rapid changes in today’s business landscape, the potential to turn knowledge into income has never been greater,” Graziosi said. “The revamped Mastermind Business System delivers everything business owners need to create, launch, and scale digital products, moving from their first sale to consistent growth.”

The Mastermind Business System provides a clear, step-by-step roadmap, helping users achieve results faster and more efficiently. It’s a holistic approach designed to drive real outcomes, ensuring business owners can easily adapt and excel in the evolving digital economy.

Key features of the Mastermind Business System include:

Personalized Roadmap: Users start with a pre-course assessment that identifies strengths, learning preferences, and goals, resulting in a tailored learning path.

Mastermind Business System Course: Comprehensive training modules that guide users from initial sales to consistent growth.

Hotseat With GG, Your 24/7 AI Business Guide: On-demand coaching that provides actionable insights, offering the feel of having Dean as a personal mentor.

All-In-One Business Hub: A fully integrated suite of tools that streamlines the entire sales and marketing process, eliminating the need for multiple software platforms.

Pre-Loaded Industry Templates: Ready-made templates designed for specific industries to help users get started quickly.

Live Mentoring with Dean Graziosi: Monthly sessions focused on driving momentum, marketing strategies, and business breakthroughs.

24/7 Live Support: Real-time assistance to ensure users never feel stuck.

Bonus VIP Ticket to the Business Breakthrough Workshop: A 3-day, immersive event on December 12-14, 2024, dedicated to scaling businesses through hands-on learning.

Unlike traditional programs that overwhelm users with scattered content, the Mastermind Business System offers a streamlined, results-oriented approach. It combines hands-on learning, continuous support, and practical tools, making it easier for business owners to achieve consistent growth and long-term success.

“Whether you’re taking your first step into the knowledge economy or looking to scale your existing digital product, the Mastermind Business System is designed to empower you at every stage,” Graziosi added.

Thousands of business owners have already experienced success with the Mastermind Business System, creating new revenue streams, maximizing impact, and gaining more freedom in their businesses. It’s more than just a system—it’s a pathway to redefining what’s possible in today’s digital landscape.

For more information or to explore the Mastermind Business System, visit joinmbs.com.

About Dean Graziosi

Dean Graziosi is a multiple New York Times best-selling author, seasoned business coach, and serial entrepreneur. With over 30 years of experience in transforming businesses and lives, Dean has helped thousands of entrepreneurs achieve breakthrough results. As Co-Founder of Mastermind.com, he continues to revolutionize the knowledge industry by delivering innovative tools and strategies for business growth.

Contact Information:

Mastermind.com

Tanner Sheldon

757-645-5957

Contact via Email

Read the full story here: https://www.pr.com/press-release/923730

Press Release Distributed by PR.com

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Why AT&T Stock Is Jumping Today

AT&T (NYSE: T) stock is climbing in Wednesday’s trading session following the telecom giant’s third-quarter report. The share price was up by about 4% as of 1:45 p.m. ET.

AT&T reported its Q3 results before the market opened Wednesday morning, posting non-GAAP (adjusted) earnings of $0.60 per share, which beat the average estimate of Wall Street analysts for $0.57 per share. But its sales of $30.2 billion fell short of expectations for sales of $30.45 billion. However, margins were strong, and the company gave encouraging guidance along some key lines.

In the quarter, the company added 403,000 postpaid phone subscriptions, and mobility services sales climbed 4% compared to the prior-year period. Meanwhile, it added 226,000 new AT&T Fiber subscriptions, making Q3 the 19th straight quarter with net additions above 200,000. Total consumer broadband sales were up 6.4% year over year.

Despite strong performances from its wireless and broadband segments, continued declines in the business wireline segment continued to weigh on the top line. Total sales in the period were down 0.5% from the $30.4 billion posted in the prior-year period, and adjusted earnings per share declined roughly 6%.

Even with annual declines in sales and earnings in Q3, AT&T’s core growth drivers served up encouraging results — and profitability came in better than anticipated. Strategy execution appears to be on track.

Management also reiterated its full-year guidance. The company continues to expect annual wireless services and broadband revenue to grow by roughly 3% and more than 7%, respectively. Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) are projected to increase by 3%. Management also said that the company is on track to reach its goal of hitting a net-debt-to-adjusted-EBITDA ratio of 2.5 in the first half of next year.

Before you buy stock in AT&T, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and AT&T wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $879,935!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

Philip Morris' Q3 Driven By Smoke-Free Products Amid Rising Market Share In Key Regions: Analyst Forecasts Growth Across IQOS And ZYN Brands

Stifel analyst Matthew E. Smith reiterated a Buy rating on Philip Morris International Inc PM, raising the price forecast to $145 from $138.

Yesterday, the Marlboro maker reported third-quarter revenue of $9.91 billion, up 8.4% year over year, beating the consensus of $9.69 billion.

Smith writes that growth in smoke-free products is driving both organic revenue growth and margin expansion.

Net revenues increased by 11.6% on an organic basis, mainly reflecting a favorable pricing variance, primarily due to higher combustible tobacco pricing, and a favorable volume/mix, mainly driven by higher smoke-free product volume.

Per Smith, there is a strong argument for owning the stock, thanks to the impressive and accelerating growth of IQOS and ZYN brands, which supports robust long-term business expansion.

The analyst highlighted that market share is growing steadily in important regions like Japan and Europe, with Europe’s share hitting 9.5% this quarter.

Most of the flavor bans in Europe are now in place, and Smith adds that the rebound in in-market sales (IMS) and market share shows promising growth potential for IQOS in the region.

Philip Morris has raised the low end of its U.S. ZYN volume outlook for 2024, now expecting 570 to 580 million cans, which is an increase of 10 million at the low end. The analyst estimates a total of 579 million cans, reflecting over 50% growth.

For 2025, the analyst estimates 9.5% EPS growth, driven by 8% organic revenue growth and margin expansion from smoke-free products.

This includes a 10% increase in organic operating profit, supported by volume growth and over 7 percentage points from price/mix contributions.

Price Action: PM shares are trading lower by 0.36% to $130.94 at last check Wednesday.

Photo by nawamin on Shutterstock

Read Next:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Stock market today: Nasdaq leads stocks lower as Wall Street braces for Tesla earnings

Sales of existing homes fell in September as house hunters remained on the fence about buying a home despite mortgage rates easing during the month.

Existing home sales slipped 1.0% from August’s tally to a seasonally adjusted annual rate of 3.84 million, the National Association of Realtors said Wednesday. That marked the lowest rate since October 2010. Economists polled by Bloomberg expected a pace of 3.88 million in September.

On a yearly basis, sales of previously owned homes were 3.5% lower in September. The median home price rose 3.0% from last September to $404,500, marking the 15th consecutive month of annual price increases.

“Home sales have been essentially stuck at around a 4 million-unit pace for the past 12 months,” NAR chief economist Lawrence Yun said in a press release.

There have been significant challenges that have weighed on sales activity, including a lack of inventory, escalating prices, and elevated mortgage rates. Last month, however, those factors turned around.

The Federal Reserve cut its benchmark rate by half a percentage point in September. While the central bank doesn’t set mortgage rates, its actions influence their direction of movement.

Mortgage rates hit the lowest level since February 2023 ahead of the Fed decision to ease, while listing inventory picked up.

But overall, that hasn’t been enough to entice buyers.

“Some consumers are hesitating about moving forward with a major expenditure like purchasing a home before the upcoming election,” Yun said.