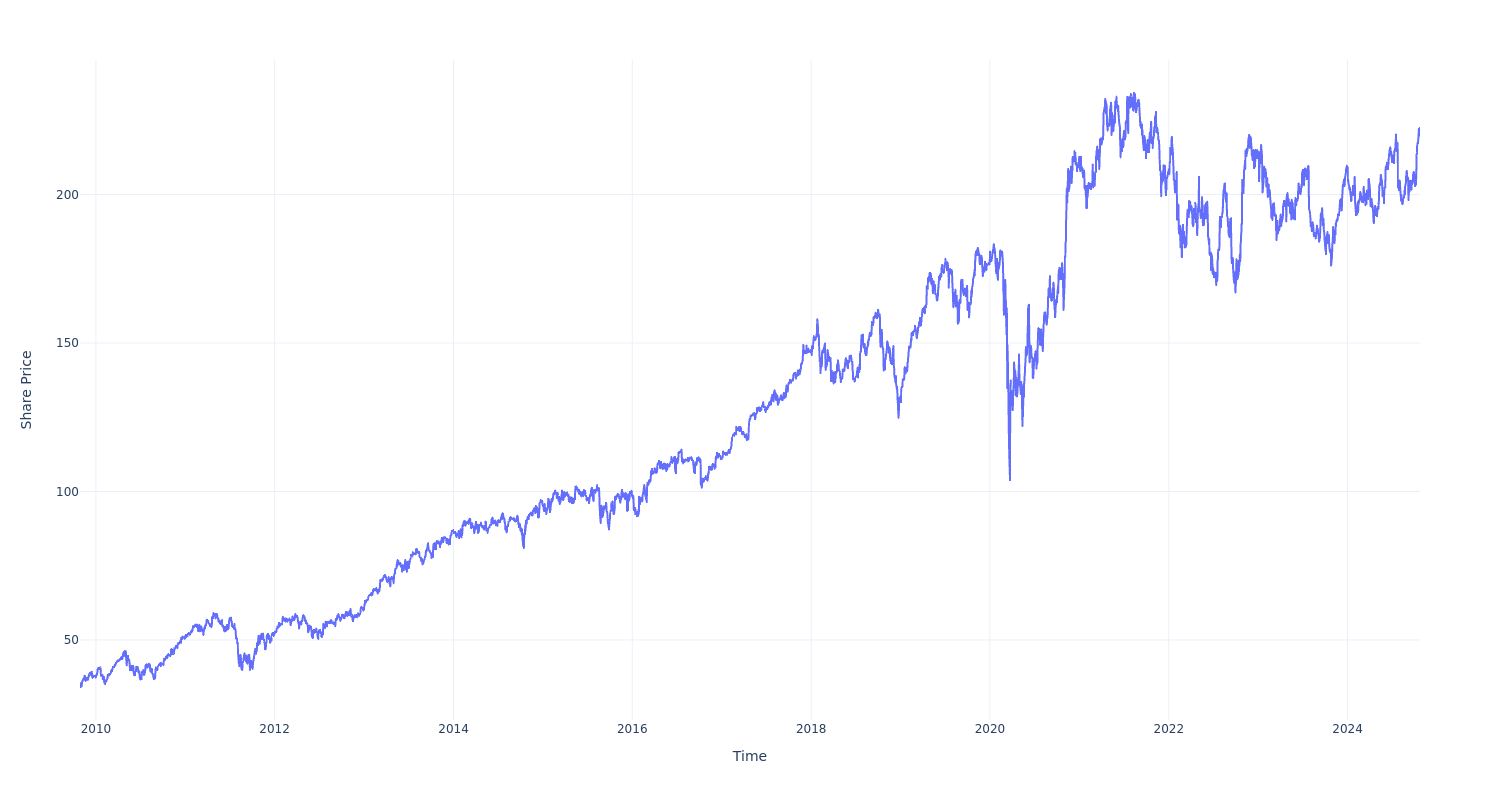

If You Invested $100 In This Stock 15 Years Ago, You Would Have $600 Today

Honeywell Intl HON has outperformed the market over the past 15 years by 1.04% on an annualized basis producing an average annual return of 12.94%. Currently, Honeywell Intl has a market capitalization of $142.77 billion.

Buying $100 In HON: If an investor had bought $100 of HON stock 15 years ago, it would be worth $630.77 today based on a price of $219.75 for HON at the time of writing.

Honeywell Intl’s Performance Over Last 15 Years

Finally — what’s the point of all this? The key insight to take from this article is to note how much of a difference compounded returns can make in your cash growth over a period of time.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Summerwell Sunterra Now Offering Tours

Opening marks Greystar’s first build for rent project in the Houston area

KATY, Texas, Oct. 22, 2024 /PRNewswire/ — Greystar, a global leader in the investment, development, and management of real estate, including rental housing, logistics and life sciences, announced today that its latest Summerwell-branded community, Summerwell Sunterra, is now offering tours and welcoming move-ins.

Summerwell is Greystar’s dedicated build for rent brand focused on developing purpose-built, single-family rental communities across the United States. This approach to build for rent adds single-family housing supply while striving to deliver efficient and scalable communities in target markets that need this product most.

“We’re excited to open our doors at Summerwell Sunterra to renters looking for the privacy and comfort of a single family home without the hassles of ownership,” Brian Herwald, Managing Director of development for Greystar said. “Residents also have the added benefit of living within the master planned Sunterra community with access to The Retreat Amenity Village and so much more. Whether floating along the lazy river, grabbing a game of pickleball or hosting a barbecue in their private backyard, our residents will get the feeling of getting away from it all on a daily basis.”

The amenities in the Retreat Amenity Village, which is a across the street, include:

- Resort-style pool

- Lazy river

- Kids splash zone

- Boardwalk

- Event lawn

- Pickleball courts

- Horseshoe pits

- Yoga lawn

- Dog park

- Resident lounge

Residents also have access to Sunterra’s nearby 3.5-acre Crystal Lagoon. The lagoon features a beach-like area with sand, cabanas and a floating dock that allows kayaks and paddleboards to launch. The Crystal Lagoon is slated to open in May 2025.

Summerwell Sunterra consists of 156 townhomes and detached single-family rental homes in three- and four-bedroom layouts that range from 1,500 sq. ft. to 1,800 sq. ft. Each home features a two-car garage, beautiful landscaping and fully fenced-in private backyard.

Homes will also include:

- 20′ deep driveways

- Open concept floor plans bathed in natural light

- Granite countertops

- Hardwood-style floors available in two options

- Oversized primary closets

- SmartRent smart home features with electronic locks, thermostats and hub

- Ceiling fans

- Stainless steel appliances

- Washer and dryer

- Storage space

To schedule a tour, please visit www.summerwellsunterra.com.

About Greystar

Greystar is a leading, fully integrated global real estate company offering expertise in property management, investment management, development, and construction services in institutional-quality rental housing, logistics, and life sciences sectors. Headquartered in Charleston, South Carolina, Greystar manages and operates more than $320 billion of real estate in approximately 250 markets globally with offices throughout North America, Europe, South America, and the Asia-Pacific region. Greystar is the largest operator of apartments in the United States, manages nearly 997,000 units/beds globally, and has a robust institutional investment management platform comprised of over $78 billion of assets under management, including $36 billion of development assets. Greystar was founded by Bob Faith in 1993 to become a provider of world-class service in the rental residential real estate business. To learn more, visit www.greystar.com

![]()

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/summerwell-sunterra-now-offering-tours-302283676.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/summerwell-sunterra-now-offering-tours-302283676.html

SOURCE Greystar

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Hemostatic Agents Market Size to Achieve USD 4.5 Billion by 2031 with 6.2% CAGR, Supporting Hemostasis for Effective Bleeding Control| Transparency Market Research, Inc.

Wilmington, Delaware, United States, Transparency Market Research, Inc. , Oct. 22, 2024 (GLOBE NEWSWIRE) — The hemostatic agents industry (Industrie für blutstillende Mittel) was worth US$ 2.6 billion in 2022. A CAGR of 6.2% is expected from 2023 to 2031, and the market will reach US$ 4.5 billion in this period. Globally, the prevalence of chronic illnesses like cancer, liver disease, and cardiovascular ailments is rising. Surgical interventions are often necessary for the diagnosis, treatment, or management of several of these disorders.

Patients with chronic illnesses frequently have complicated medical histories when they first arrive, which puts them at risk for hemorrhage during surgery. Hemostatic medications are, therefore, in greater demand to control intraoperative and postoperative bleeding in this patient population.

As minimally invasive surgical techniques become more popular, trauma is reduced, recovery is sped up, and complications are reduced. However, effective hemostatic drugs are still required for these surgeries to halt the bleeding at the surgical site. The need for hemostatic agents appropriates for minimally invasive procedures is expected to rise due to the growing popularity of these treatments across various medical specialties, driving the market’s expansion.

Download sample PDF copy of report: https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=52779

Key Findings of the Market Report

- Based on product type, active agents are anticipated to drive demand for hemostatic agents in the future.

- The hemostatic agents market in North America held the largest share in 2022.

- As transplantation rates rise, hemostatic agents will become more prevalent on the market.

- In terms of distribution channels, large hospitals (500 +beds) are a major driver of hemostatic agent sales.

Global Hemostatic Agents Market: Competitive Landscape

Hemostatic agents are mainly used to treat excessive blood flow during severe injuries and surgeries, and most major players focus on providing various options. The company is introducing cutting-edge hemostatic agents that are more precise, effective, and accessible, forming strategic alliances, and expanding globally.

Key Market Players

- Baxter

- Ethicon Inc.

- BD

- B. Braun SE

- Pfizer Inc.

- Teleflex Incorporated

- CryoLife, Inc.

- Integra LifeSciences

- Advanced Medical Solutions Group plc

- GELITA AG

Key Developments

- In July 2023, Baxter International Inc., the leading global provider of surgical innovation, announced the introduction of PERCLOT absorbable hemostatic powder in the U.S. The PERCLOT hemostatic powder, which is passive and absorbable, is designed to treat mild bleeding in patients with intact coagulation.

- In August 2023, Teleflex Incorporated, a global leader in medical technology, announced the FDA’s approval of its QuikClot Control+ Hemostatic Device in cardiac surgery procedures and bone surface bleeding following sternotomies, according to the U.S. Food and Drug Administration (FDA). By doing this, clinicians can control all bleeding during cardiac surgery using the QuikClot Control+ Device.

Global Hemostatic Agents Market: Growth Drivers

· The number of surgical procedures performed across the globe is steadily on the rise. The frequency of chronic conditions requiring surgical intervention, improvements in medical technology, and easier access to healthcare facilities are some of the causes contributing to the rise. As a result, the need for hemostatic medicines to control bleeding during different surgical operations is rising concurrently.

· Populations worldwide are aging, with a greater proportion of elderly individuals. The proportion of the older population with health issues requiring surgery is often higher. In addition, physiological changes associated with aging may increase the risk of bleeding during surgery. As a result, there is an increased need for hemostatic drugs to meet the specific requirements of this group.

· Hemostatic agent innovation has resulted in the creation of cutting-edge products with enhanced safety and efficacy characteristics. Manufacturers invest in research and development to develop hemostatic treatments that promote quick hemostasis, reduce tissue injury, and improve biocompatibility. As healthcare practitioners seek better ways to handle bleeding during surgery, these technical developments are causing the market to grow.

Unlock Growth Potential in Your Industry! Download PDF Brochure: https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=52779

Global Hemostatic Agents Market: Regional Landscape

- North America has a highly developed and modern healthcare system. This infrastructure makes a variety of medical supplies, such as hemostatic agents, more easily accessible and encourages the use of cutting-edge surgical methods. The strong healthcare system in the area fuels demand for superior hemostatic agents that adhere to strict regulations and provide the best possible results for patients.

- With large investments in healthcare delivery, innovation, and research, North America has some of the highest healthcare spending in the world. Healthcare facilities can purchase sophisticated hemostatic agents and other medical supplies required for surgical procedures because of the significant spending on healthcare. Affordability of reimbursement rules in the region further encourages using hemostatic drugs in surgical settings.

- Chronic illnesses, including diabetes, cancer, and cardiovascular problems, are common in North America and place a significant strain on the healthcare system. Hemostatic medicines are in greater demand due to the need to manage bleeding issues during surgeries. As the population ages and chronic diseases become more prevalent, the need for efficient hemostatic agents will increase.

Global Hemostatic Agents Market: Segmentation

Product Type

- Active Agents

- Passive Agents

- Combination

Specialty/Therapeutic Area

- Cardiology

- Cath Lab

- Trauma

- General Surgery

- ObGyn

- Transplant

- Oncology

- Neurology

- Orthopedic

- Plastic Surgery

- Dental

- Others (Urological Surgeries, Pulmonary Surgeries)

Distribution Channel

- Large Hospital (500+ Beds)

- Medium Hospital (250-499 Beds)

- Small Hospitals (Less than 250 Beds)

Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Buy this Premium Research Report @ https://www.transparencymarketresearch.com/checkout.php?rep_id=52779<ype=S

More Trending Reports by Transparency Market Research –

- Hybrid Operating Room Market – The market was valued at US$ 876.9 Mn in 2021 and it is estimated to grow at a CAGR of 7.7 % from 2022 to 2031 and reach US$ 1.8 Bn by the end of 2031

- Dental Putty Market – The industry was valued at US$ 64.3 Mn in 2021 and it is estimated to advance at a CAGR of 6.5 % from 2022 to 2031 and reach US$ 119.9 Mn by the end of 2031

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

Email: sales@transparencymarketresearch.com

Follow Us: LinkedIn| Twitter| Blog | YouTube

![]()

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Seeking at Least 8% Dividend Yield? Raymond James Suggests 2 Dividend Stocks to Buy

We’ve been seeing a bullish market in recent months, and investors, as always, are looking to maximize their returns. The analysts at Raymond James are recommending dividend stocks, encouraging investors to capitalize on both share growth and reliable dividend income.

Discussing the market landscape, Raymond James’ CIO, Larry Adam, states: “The sun continues to shine on the U.S. economy. Some of the traditional metrics that we follow (e.g., ISM manufacturing, the Fed’s aggressive tightening cycle, and leading indicators) suggest that the economy should have succumbed to a recession by now. However, growth has proven more resilient than expected. Just like the GPS ‘recalculates’ when a road trip takes an unexpected detour, our growth forecasts have had to ‘recalculate’ as the economy has proven more resilient than expected. The reasons: healthy job growth, government stimulus, travel spending, fiscal support (IRA, CHIPS, Infrastructure Act) and AI investments.”

Adam’s conclusion is clear: recession is unlikely under current conditions. He summarizes, “The important point: slowing, but still positive job growth, healthy levels of business capex, and unspent fiscal stimulus should keep the economy on a path to a soft landing.”

In this environment, the dividend stocks recommended by Raymond James offer a sound opportunity, providing substantial dividend yields – some exceeding 8% – in addition to share price appreciation. Leveraging TipRanks’ data, we’ve examined two of Raymond James’ top picks in detail.

CTO Realty Growth (CTO)

The first stock we’ll look at is CTO Realty Growth, a REIT, or real estate investment trust. These companies are known for their frequent high dividend yields, a product of regulatory requirements that they return a specified portion of their profits directly to their investors; dividends are the frequent method of choice.

CTO owns and operates a portfolio of 19 high-end retail properties in some of the highest growth markets of the US. The company’s properties include primarily commercial parks and upscale shopping malls, with locations in North Carolina, Florida, Georgia, Texas, and Arizona. In addition, CTO acts as the external manager of – and maintains a ‘meaningful’ ownership interest in – another REIT, Alpine Income Property Trust.

CTO has built its investment strategy on future income potential, seeing room for growth as more important than current income generation. The company’s geographic position reflects this; the sun-belt states of Florida, Texas, and Arizona are among the highest growth regions in the US, and Georgia and North Carolina are close behind.

Ipsen delivers strong sales momentum in the first nine months of 2024 and increases its full-year guidance

PARIS, FRANCE, 23 October 2024 – Ipsen (IPNIPSEY, a global specialty-care biopharmaceutical company, today presents its performance for the year to date and the third quarter of 2024.

| |

YTD 2024 | YTD 2023 | % change | Q3 2024 |

Q3 2023 |

% change | ||

| €m | €m | Actual | CER1 | €m | €m | Actual | CER1 | |

| Oncology | 1 829,8 | 1 744,1 | 4,9% | 5,8% | 604,0 | 574,5 | 5,1% | 5,6% |

| Neuroscience | 536,4 | 489,0 | 9,7% | 11,8% | 181,9 | 164,8 | 10,4% | 10,1% |

| Rare Disease | 129,7 | 76,0 | 70,7% | 71,3% | 50,8 | 33,2 | 53,1% | 54,4% |

| Total Sales | 2 495,9 | 2 309,1 | 8,1% | 9,2% | 836,6 | 772,4 | 8,3% | 8,6% |

Highlights

- Total-sales growth in the year to date of 9.2% at CER1, or 8.1% as reported, with notable performances from Dysport® (abobotulinumtoxinA), Cabometyx® (cabozantinib) and Bylvay® (odevixibat), with robust Somatuline® (lanreotide) sales, as well as the increasing contribution from the launches of Iqirvo® (elafibranor) in 2L PBC2 and Onivyde® (irinotecan) in 1L mPDAC3

- Regulatory approvals in the E.U. of Iqirvo and Kayfanda® (odevixibat)

- Increased 2024 financial guidance: total-sales growth greater than 8.0% at CER1 (prior guidance: greater than 7.0% at CER1); core operating margin greater than 31.0% of total sales (prior guidance: greater than 30.0%)

“Since the launch of our strategy in 2020, we have enjoyed uninterrupted growth. This quarter was no exception and was accompanied by further progress in the pipeline”, commented David Loew, Chief Executive Officer. “We have also continued to launch across several indications and lines of therapy, including the recent rollouts of Iqirvo and Onivyde, which are progressing well. Supported by the performance so far this year, we are further increasing our 2024 sales and margin guidance.”

“We have built a track record of delivery, grounded in a strong foundation of external innovation, commercial excellence and our ongoing mission to offer more choices for patients.”

Full-year 2024 guidance

Based on the strong performance in the third quarter, Ipsen has further increased its financial guidance for 2024:

- Total-sales growth greater than 8.0%, at constant currency (prior guidance of greater than 7.0%). Based on the average level of exchange rates in September 2024, an adverse impact on total sales of around 1.5% from currencies is expected

- Core operating margin greater than 31.0% of total sales (prior guidance of greater than 30.0%)

Pipeline update

In September 2024, the European Commission conditionally approved Iqirvo 80mg tablets for the treatment of PBC in combination with ursodeoxycholic acid (UDCA) in adults with an inadequate response to UDCA, or as a monotherapy in patients unable to tolerate UDCA. Iqirvo was approved in the same setting by the U.S. FDA in June 2024.

In September 2024, the European Commission also approved Kayfanda as a treatment for pruritus in children from as young as six months of age who have Alagille syndrome (ALGS). Odevixibat, under the brand name Bylvay, is already marketed in the E.U. for the treatment of progressive familial intrahepatic cholestasis (PFIC), and in the U.S. and E.U. for PFIC, and in the U.S. for ALGS.

In the same month, final results from the CABINET Phase III trial were presented at the 2024 European Society for Medical Oncology Congress and were published in the New England Journal of Medicine, reinforcing the efficacy benefits of Cabometyx in advanced neuroendocrine tumors. It was announced at that time that Ipsen had submitted an extension of indication Marketing Authorization to the European Medicines Agency.

Business development

In August 2024, Ipsen entered into an agreement to sell its rare pediatric disease Priority Review Voucher. As part of the agreement, Ipsen received a cash payment of $158m in the third quarter.

In October 2024, Eton Pharmaceuticals entered into an agreement with Ipsen to acquire Increlex® (mecasermin injection). The transaction is expected to close before the end of 2024.

Arbitration proceedings with Galderma

As of 30 September 2024, two arbitration proceedings initiated by Galderma against Ipsen at the International Chamber of Commerce (ICC) were ongoing. The first dispute, initiated by Galderma in 2021, pertains to the territorial scope of the commercial partnership related to Azzalure® (abobotulinumtoxinA) and Dysport under an agreement signed in 2007 in the E.U., in certain Eastern European countries, and in Central Asia. The Tribunal of the ICC Internal Court of Arbitration issued a final award, in October 2024, dismissing most, if not all, of Galderma’s claims in this first arbitration and ordered that Galderma bear the majority of the legal fees and arbitration costs incurred by Ipsen.

A second dispute was initiated by Galderma in November 2023, related to the validity of Ipsen’s 2023 termination of a joint R&D collaboration agreement entered into in 2014 under the parties’ respective early-stage neurotoxin programs, including the development of IPN10200. At this stage, Ipsen cannot reasonably predict any potential financial impact from this final remaining arbitration process, for which it intends to fully defend and vindicate its rights.

Conference call

A conference call and webcast for investors and analysts will begin today at 2pm CET. Participants can access the call and its details by registering here; webcast details can be found here.

Calendar

Ipsen intends to publish its full-year and fourth-quarter results on 13 February 2025.

Notes

All financial figures are in € millions (€m). The performance shown in this announcement covers the nine-month period to 30 September 2024 (YTD 2024) and the three-month period to 30 September 2024

(Q3 2024), compared to the nine-month period to 30 September 2023 (YTD 2023) and the three-month period to 30 September 2023 (Q3 2023), respectively. Commentary is based on the performance in

YTD 2024, unless stated otherwise.

About Ipsen

Ipsen is a global biopharmaceutical company with a focus on bringing transformative medicines to patients in three therapeutic areas: Oncology, Rare Disease and Neuroscience. Our pipeline is fuelled by external innovation and supported by nearly 100 years of development experience and global hubs in the U.S., France and the U.K. Our teams in more than 40 countries and our partnerships around the world enable us to bring medicines to patients in more than 100 countries.

Ipsen is listed in Paris IPN and in the U.S. through a Sponsored Level I American Depositary Receipt program IPSEY. For more information, visit ipsen.com.

Ipsen contacts

Investors

- Craig Marks +44 (0)7584 349 193

- Nicolas Bogler +33 6 52 19 98 92

Media

- Jennifer Smith-Parker +44 (0) 7843 137 764

- Anne Liontas +33 7 67 34 72 96

1 At constant exchange rates (CER), which excludes any foreign-exchange impact by recalculating the performance for the relevant period by applying the exchange rates used for the prior period.

2 Second-line primary biliary cholangitis.

3 First-line metastatic pancreatic ductal adenocarcinoma.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trump Vows To 'Make Interest On Car Loans Fully Tax-Deductible' For Made In America Vehicles

Former President Donald Trump has proposed making the interest on car loans tax-deductible for vehicles manufactured in the United States. This move is seen as an attempt to bolster the American auto industry and attract voters.

What Happened: Trump made this announcement on Tuesday during a rally in North Carolina. He stated that if elected, he would make the interest on car loans fully tax-deductible for vehicles produced in the U.S., reported Reuters.

“I will make interest on car loans fully tax-deductible,” Trump said. “I am only going to do it if they build that particular product – namely an automobile – in the United States.”

With the presidential election just two weeks away, Trump’s proposal is seen as a strategic move to win over voters.

Why It Matters: Trump’s proposal comes amid a tight race between him and Democratic Vice President Kamala Harris. Both candidates have been making economic pledges to appeal to voters.

This is not the first time Trump has proposed economic incentives to boost the American auto industry. Earlier in September, he pledged to impose 100% tariffs on cars made in Mexico if elected. He also suggested that car assembly work in the U.S. is simple, drawing criticism from labor advocates and Democratic officials.

However, economists have warned that Trump’s economic policies could lead to higher inflation and deficits compared to Harris’ policies, as per a survey.

Read Next:

Image Via Flickr

This story was generated using Benzinga Neuro and edited by Kaustubh Bagalkote

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

It's Getting Harder to Qualify for Social Security Benefits in Retirement. Here's the Reason Why

One of the biggest Social Security myths out there is that everyone is entitled to a monthly benefit once they reach a certain age. But that’s not how the program works.

Generally speaking, the way to get Social Security benefits in retirement is to earn them by working and paying into the program. There can be exceptions for people who don’t work but are eligible for spousal benefits or survivors benefits. But if you want to guarantee yourself those benefits for your retirement, then it’s important to make sure you’ve earned enough work credits in your lifetime.

Specifically, Social Security requires a total of 40 work credits to be eligible for benefits. But the tricky thing is that you’re only allowed to earn up to four work credits per year. This means that you basically have to work in some capacity for at least 10 years to qualify for Social Security.

Meanwhile, the value of a work credit can change from one year to the next — and that’s precisely what’s happening in 2025.

On Oct. 10, the Social Security Administration announced a number of key changes to the program that are set to take effect in 2025. One major change is a 2.5% cost-of-living adjustment. Another is a higher wage cap for Social Security tax purposes — $176,100, up from $168,600 in 2024.

An additional big change that’s coming in 2025 is the value of a single work credit. Currently, it takes $1,730 in earnings to earn one work credit. Next year, it will take $1,810. That’s something to keep in mind if you work part-time but want to make sure you’re able to get Social Security down the line.

However, you should know that if you work full-time, this change shouldn’t really affect you, even if you only earn minimum wage. If that’s the case, if you earn the minimum wage for 40 hours a week over 50 working weeks, that’s more than enough income to secure your four work credits for 2025.

Even though Social Security has been around for a long time, the program tends to undergo changes on a yearly basis. It pays to keep tabs on those, regardless of your age.

You might assume you don’t need to bother reading up on Social Security if you’re nowhere close to retirement. But if you don’t understand what it takes to get benefits, you might end up missing out on that key income source once you’re no longer able to work at all.

Of course, if you’re someone who works so part-time that you’re unable to accumulate 40 work credits in your lifetime, it may be that you have somebody else’s income to fall back on, like a spouse’s. You may be eligible for some type of Social Security benefit down the line based on their earnings record. But it’s best to know the rules so you know what to expect once you get older.

Taylor Morrison Reports Third Quarter 2024 Results

SCOTTSDALE, Ariz., Oct. 23, 2024 /PRNewswire/ — Taylor Morrison Home Corporation TMHC, a leading national land developer and homebuilder, announced results for the third quarter ended September 30, 2024. Reported third quarter net income was $251 million, or $2.37 per diluted share, as compared to $171 million, or $1.54 per diluted share, in the prior-year quarter.

![]()

Third quarter 2024 highlights included the following, as compared to the third quarter of 2023:

- Diluted EPS increased 54% to $2.37

- Net sales orders increased 9% to 2,830

- Home closings revenue of $2.0 billion, driven by 3,394 closings at an average price of $598,000

- Home closings gross margin of 24.8%, up from 23.1% a year ago

- 83,579 homebuilding lots owned and controlled, of which a record 58% was controlled off balance sheet

- Share repurchases totaled $61 million during the quarter and $258 million year to date

- Total liquidity of $1.2 billion; no senior debt maturities until 2027

“In the third quarter, our team delivered better-than-expected results, which clearly demonstrated the benefits of our diversified consumer and geographic strategy, as well as our team’s impressive execution in the face of continued interest rate volatility, economic uncertainty and hurricane-related disruptions,” said Sheryl Palmer, Taylor Morrison CEO and Chairman. “Led by strong top-line growth and improved margins, our results generated over-50% year-over-year growth in our earnings per diluted share to $2.37 and a 15% year-over-year increase in our book value per share to approximately $54.”

Palmer continued, “By meeting the needs of well-qualified homebuyers with appropriate product offerings in prime community locations, we continue to benefit from healthy demand and pricing resiliency across our portfolio. On the sales front, our net orders increased 9% year over year, driven by a monthly absorption pace of 2.8 per community. As I shared on our second quarter call, we had begun to see traffic recover in June and July, which translated into improving order volume throughout the third quarter, with sales activity ending on a high note in September. While still early in October, demand has generally been healthy and consistent with seasonal trends, even with the impact of yet another hurricane in Florida.”

“Since expanding our company’s scale and refining our operational capabilities over the last many years, we believe that our ability to generate accretive growth and attractive returns has been permanently strengthened. This is reflected in the long-term targets that we introduced earlier this year, each of which are meaningfully stronger than our historic norms. These targets include: 10% annual home closings growth, an annualized low-three absorption pace, low-to-mid 20% home closings gross margins, and mid-to-high teens returns on equity.”

“This year, with just over two months to go, we expect to meet or exceed each of these metrics with anticipated double-digit closings growth to approximately 12,725 homes at a home closings gross margin of around 24.3% as 2024 has shaped up to be another milestone year for our company. As we head into 2025, we are confident that our long-standing emphasis on capital-efficient growth will yield another year of strong performance, supported by tailwinds driving the need for new construction and our favorable positioning as a diversified homebuilder,” said Palmer.

Business Highlights (All comparisons are of the current quarter to the prior-year quarter, unless indicated.)

Homebuilding

- Home closings revenue increased 26% to $2.0 billion, driven by a 29% increase in closings to 3,394 homes, which was partially offset by a 2% decrease in the average price to $598,000.

- The home closings gross margin was 24.8%, which was up 170 basis points from 23.1% in the prior-year quarter.

- Net sales orders increased 9% to 2,830, driven by a 5% increase in ending community count to 340 outlets and a 4% increase in the monthly absorption pace to 2.8 per community.

- SG&A as a percentage of home closings revenue decreased to 9.8% from 10.4% a year ago.

- Cancellations equaled 9.3% of gross orders, down from 11.4% a year ago.

- Backlog at quarter end was 5,692 homes with a sales value of $3.8 billion. Backlog customer deposits averaged approximately $54,000 per home.

Land Portfolio

- Homebuilding land acquisition and development spend totaled $593 million, up from $552 million a year ago. Development-related spend accounted for 46% of the total versus 42% a year ago.

- Homebuilding lot supply was 83,579 homesites, of which a record 58% was controlled off balance sheet.

- Based on trailing twelve-month home closings, total homebuilding lots represented 6.6 years of supply, of which 2.7 years was owned.

Financial Services

- The mortgage capture rate was 88%, unchanged from a year ago.

- Borrowers had an average credit score of 754 and average debt-to-income ratio of 40%.

Balance Sheet

- At quarter end, total liquidity was approximately $1.2 billion, including $946 million of total capacity on the Company’s revolving credit facility, which was undrawn outside of normal letters of credit.

- The gross homebuilding debt to capital ratio was 25.1%. Including $256 million of unrestricted cash on hand, the net homebuilding debt-to-capital ratio was 22.5%.

- The Company repurchased 1.0 million shares for $61 million, bringing the year-to-date total to 4.2 million shares for $258 million. At quarter end, the remaining share repurchase authorization was $237 million. Subsequent to quarter end, our Board of Directors authorized an expanded share repurchase authorization of up to $1 billion, effective through December 31, 2026.

Business Outlook

Fourth Quarter 2024

- Home closings are expected to be approximately 3,400

- Average closing price is expected to be approximately $610,000

- Home closings gross margin is expected to be around 24.5%

- Ending active community count is expected to be between 330 to 340

- Effective tax rate is expected to be approximately 25%

- Diluted share count is expected to be approximately 106 million

Full Year 2024

- Home closings are now expected to be approximately 12,725

- Average closing price is now expected to be approximately $600,000

- Home closings gross margin is now expected to be approximately 24.3%

- Ending active community count is expected to be between 330 to 340

- SG&A as a percentage of home closings revenue is expected to be in the high-9% range

- Effective tax rate is now expected to be between 24.5% to 25.0%

- Diluted share count is expected to be approximately 107 million

- Land and development spend is now expected to be around $2.5 billion

- Share repurchases are expected to total approximately $300 million

Quarterly Financial Comparison

|

(Dollars in thousands) |

Q3 2024 |

Q3 2023 |

Q3 2024 vs. Q3 2023 |

||

|

Total Revenue |

$ 2,120,842 |

$ 1,675,545 |

26.6 % |

||

|

Home Closings Revenue |

$ 2,029,134 |

$ 1,611,883 |

25.9 % |

||

|

Home Closings Gross Margin |

$ 503,309 |

$ 372,884 |

35.0 % |

||

|

24.8 % |

23.1 % |

170 bps increase |

|||

|

SG&A |

$ 199,341 |

$ 167,791 |

18.8 % |

||

|

% of Home Closings Revenue |

9.8 % |

10.4 % |

60 bps decrease |

Earnings Conference Call Webcast

A public webcast to discuss the Company’s earnings will be held later today at 8:30 a.m. ET. Call participants are asked to register for the event here to receive a unique passcode and dial-in information. The call will be recorded and available for replay on Taylor Morrison’s website at www.taylormorrison.com on the Investor Relations portion of the site under the Events & Presentations tab.

About Taylor Morrison

Headquartered in Scottsdale, Arizona, Taylor Morrison is one of the nation’s leading homebuilders and developers. We serve a wide array of consumers from coast to coast, including first-time, move-up, luxury and resort lifestyle homebuyers and renters under our family of brands—including Taylor Morrison, Esplanade and Yardly. From 2016-2024, Taylor Morrison has been recognized as America’s Most Trusted® Builder by Lifestory Research. Our long-standing commitment to sustainable operations is highlighted in our annual Sustainability and Belonging Report.

For more information about Taylor Morrison, please visit www.taylormorrison.com.

Forward-Looking Statements

This earnings summary includes “forward-looking statements.” These statements are subject to a number of risks, uncertainties and other factors that could cause our actual results, performance, prospects or opportunities, as well as those of the markets we serve or intend to serve, to differ materially from those expressed in, or implied by, these statements. You can identify these statements by the fact that they do not relate to matters of a strictly factual or historical nature and generally discuss or relate to forecasts, estimates or other expectations regarding future events. Generally, the words “”anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “may,” “will,” “can,” “could,” “might,” “should” and similar expressions identify forward-looking statements, including statements related to expected financial, operating and performance results, planned transactions, planned objectives of management, future developments or conditions in the industries in which we participate and other trends, developments and uncertainties that may affect our business in the future.

Such risks, uncertainties and other factors include, among other things: inflation or deflation; changes in general and local economic conditions; slowdowns or severe downturns in the housing market; homebuyers’ ability to obtain suitable financing; increases in interest rates, taxes or government fees; shortages in, disruptions of and cost of labor; higher cancellation rates of existing agreements of sale; competition in our industry; any increase in unemployment or underemployment; the seasonality of our business; the physical impacts of climate change and the increased focus by third-parties on sustainability issues; our ability to obtain additional performance, payment and completion surety bonds and letters of credit; significant home warranty and construction defect claims; our reliance on subcontractors; failure to manage land acquisitions, inventory and development and construction processes; availability of land and lots at competitive prices; decreases in the market value of our land inventory; new or changing government regulations and legal challenges; our compliance with environmental laws and regulations regarding climate change; our ability to sell mortgages we originate and claims on loans sold to third parties; governmental regulation applicable to our financial services and title services business; the loss of any of our important commercial lender relationships; our ability to use deferred tax assets; raw materials and building supply shortages and price fluctuations; our concentration of significant operations in certain geographic areas; risks associated with our unconsolidated joint venture arrangements; information technology failures and data security breaches; costs to engage in and the success of future growth or expansion of our operations or acquisitions or disposals of businesses; costs associated with our defined benefit and defined contribution pension schemes; damages associated with any major health and safety incident; our ownership, leasing or occupation of land and the use of hazardous materials; existing or future litigation, arbitration or other claims; negative publicity or poor relations with the residents of our communities; failure to recruit, retain and develop highly skilled, competent people; utility and resource shortages or rate fluctuations; constriction of the capital markets; risks related to instability in the banking system; risks associated with civil unrest, acts of terrorism, threats to national security, the conflicts in Eastern Europe and the Middle East and other geopolitical events; the scale and scope of current and future public health events, including pandemics and epidemics; any failure of lawmakers to agree on a budget or appropriation legislation to fund the federal government’s operations (also known as a government shutdown), and financial markets’ and businesses’ reactions to any such failure; risks related to our substantial debt and the agreements governing such debt, including restrictive covenants contained in such agreements; our ability to access the capital markets; the risks associated with maintaining effective internal controls over financial reporting; provisions in our charter and bylaws that may delay or prevent an acquisition by a third party; and our ability to effectively manage our expanded operations.

In addition, other such risks and uncertainties may be found in our most recent annual report on Form 10-K and our subsequent quarterly reports filed with the Securities and Exchange Commission (SEC) as such factors may be updated from time to time in our periodic filings with the SEC. We undertake no duty to update any forward-looking statement, whether as a result of new information, future events or changes in our expectations, except as required by applicable law.

|

Taylor Morrison Home Corporation Condensed Consolidated Statements of Operations (In thousands, except per share amounts, unaudited) |

|||||||

|

Three Months Ended |

Nine Months Ended |

||||||

|

2024 |

2023 |

2024 |

2023 |

||||

|

Home closings revenue, net |

$ 2,029,134 |

$ 1,611,883 |

$ 5,585,516 |

$ 5,221,225 |

|||

|

Land closings revenue |

27,820 |

14,291 |

48,279 |

31,439 |

|||

|

Financial services revenue |

49,654 |

40,045 |

145,529 |

117,108 |

|||

|

Amenity and other revenue |

14,234 |

9,326 |

32,323 |

28,194 |

|||

|

Total revenue |

2,120,842 |

1,675,545 |

5,811,647 |

5,397,966 |

|||

|

Cost of home closings |

1,525,825 |

1,238,999 |

4,231,740 |

3,980,749 |

|||

|

Cost of land closings |

27,010 |

13,572 |

50,915 |

30,620 |

|||

|

Financial services expenses |

27,304 |

23,128 |

80,553 |

70,618 |

|||

|

Amenity and other expenses |

9,634 |

8,128 |

28,237 |

25,010 |

|||

|

Total cost of revenue |

1,589,773 |

1,283,827 |

4,391,445 |

4,106,997 |

|||

|

Gross margin |

531,069 |

391,718 |

1,420,202 |

1,290,969 |

|||

|

Sales, commissions and other marketing costs |

117,714 |

98,797 |

334,270 |

304,591 |

|||

|

General and administrative expenses |

81,627 |

68,994 |

231,970 |

205,904 |

|||

|

Net income from unconsolidated entities |

(707) |

(1,934) |

(6,086) |

(7,049) |

|||

|

Interest expense/(income), net |

3,379 |

(5,782) |

7,423 |

(12,013) |

|||

|

Other (income)/expense, net |

(3,635) |

2,968 |

3,837 |

6,683 |

|||

|

Loss on extinguishment of debt, net |

— |

269 |

— |

269 |

|||

|

Income before income taxes |

332,691 |

228,406 |

848,788 |

792,584 |

|||

|

Income tax provision |

81,219 |

57,960 |

206,241 |

196,005 |

|||

|

Net income before allocation to non-controlling interests |

251,472 |

170,446 |

642,547 |

596,579 |

|||

|

Net (income)/loss attributable to non-controlling interests |

(346) |

245 |

(1,691) |

(235) |

|||

|

Net income |

$ 251,126 |

$ 170,691 |

$ 640,856 |

$ 596,344 |

|||

|

Earnings per common share: |

|||||||

|

Basic |

$ 2.41 |

$ 1.57 |

$ 6.08 |

$ 5.48 |

|||

|

Diluted |

$ 2.37 |

$ 1.54 |

$ 5.97 |

$ 5.40 |

|||

|

Weighted average number of shares of common stock: |

|||||||

|

Basic |

104,132 |

108,837 |

105,359 |

108,827 |

|||

|

Diluted |

106,089 |

110,622 |

107,361 |

110,536 |

|||

|

Taylor Morrison Home Corporation Condensed Consolidated Balance Sheets (In thousands, unaudited) |

|||

|

September 30, |

December 31, |

||

|

Assets |

|||

|

Cash and cash equivalents |

$ 256,447 |

$ 798,568 |

|

|

Restricted cash |

846 |

8,531 |

|

|

Total cash |

257,293 |

807,099 |

|

|

Owned inventory |

6,265,280 |

5,473,828 |

|

|

Consolidated real estate not owned |

175,245 |

71,618 |

|

|

Total real estate inventory |

6,440,525 |

5,545,446 |

|

|

Land deposits |

273,967 |

203,217 |

|

|

Mortgage loans held for sale |

265,356 |

193,344 |

|

|

Lease right of use assets |

69,083 |

75,203 |

|

|

Prepaid expenses and other assets, net |

336,051 |

290,925 |

|

|

Other receivables, net |

207,595 |

184,518 |

|

|

Investments in unconsolidated entities |

397,061 |

346,192 |

|

|

Deferred tax assets, net |

67,825 |

67,825 |

|

|

Property and equipment, net |

322,483 |

295,121 |

|

|

Goodwill |

663,197 |

663,197 |

|

|

Total assets |

$ 9,300,436 |

$ 8,672,087 |

|

|

Liabilities |

|||

|

Accounts payable |

$ 269,300 |

$ 263,481 |

|

|

Accrued expenses and other liabilities |

577,501 |

549,074 |

|

|

Lease liabilities |

79,426 |

84,999 |

|

|

Income taxes payable |

5,528 |

— |

|

|

Customer deposits |

307,510 |

326,087 |

|

|

Estimated development liabilities |

19,241 |

27,440 |

|

|

Senior notes, net |

1,470,014 |

1,468,695 |

|

|

Loans payable and other borrowings |

439,878 |

394,943 |

|

|

Revolving credit facility borrowings |

— |

— |

|

|

Mortgage warehouse borrowings |

233,331 |

153,464 |

|

|

Liabilities attributable to consolidated real estate not owned |

175,245 |

71,618 |

|

|

Total liabilities |

$ 3,576,974 |

$ 3,339,801 |

|

|

Stockholders’ equity |

|||

|

Total stockholders’ equity |

5,723,462 |

5,332,286 |

|

|

Total liabilities and stockholders’ equity |

$ 9,300,436 |

$ 8,672,087 |

|

|

Homes Closed and Home Closings Revenue, Net: |

|||||||||||||||||

|

Three Months Ended September 30, |

|||||||||||||||||

|

Homes Closed |

Home Closings Revenue, Net |

Average Selling Price |

|||||||||||||||

|

(Dollars in thousands) |

2024 |

2023 |

Change |

2024 |

2023 |

Change |

2024 |

2023 |

Change |

||||||||

|

East |

1,320 |

996 |

32.5 % |

$ 758,179 |

$ 572,971 |

32.3 % |

$ 574 |

$ 575 |

(0.2 %) |

||||||||

|

Central |

932 |

709 |

31.5 % |

515,643 |

423,396 |

21.8 % |

553 |

597 |

(7.4) % |

||||||||

|

West |

1,142 |

934 |

22.3 % |

755,312 |

615,516 |

22.7 % |

661 |

659 |

0.3 % |

||||||||

|

Total |

3,394 |

2,639 |

28.6 % |

$ 2,029,134 |

$ 1,611,883 |

25.9 % |

$ 598 |

$ 611 |

(2.1) % |

||||||||

|

Nine Months Ended September 30, |

|||||||||||||||||

|

Homes Closed |

Home Closings Revenue, Net |

Average Selling Price |

|||||||||||||||

|

(Dollars in thousands) |

2024 |

2023 |

Change |

2024 |

2023 |

Change |

2024 |

2023 |

Change |

||||||||

|

East |

3,490 |

3,228 |

8.1 % |

$ 1,991,038 |

$ 1,906,862 |

4.4 % |

$ 570 |

$ 591 |

(3.6 %) |

||||||||

|

Central |

2,628 |

2,376 |

10.6 % |

1,468,197 |

1,499,420 |

(2.1) % |

559 |

631 |

(11.4 %) |

||||||||

|

West |

3,207 |

2,701 |

18.7 % |

2,126,281 |

1,814,943 |

17.2 % |

663 |

672 |

(1.3) % |

||||||||

|

Total |

9,325 |

8,305 |

12.3 % |

$ 5,585,516 |

$ 5,221,225 |

7.0 % |

$ 599 |

$ 629 |

(4.8) % |

||||||||

|

Net Sales Orders: |

|||||||||||||||||

|

Three Months Ended September 30, |

|||||||||||||||||

|

Net Sales Orders |

Sales Value |

Average Selling Price |

|||||||||||||||

|

(Dollars in thousands) |

2024 |

2023 |

Change |

2024 |

2023 |

Change |

2024 |

2023 |

Change |

||||||||

|

East |

1,140 |

940 |

21.3 % |

$ 610,892 |

$ 559,524 |

9.2 % |

$ 536 |

$ 595 |

(9.9 %) |

||||||||

|

Central |

747 |

641 |

16.5 % |

398,587 |

374,224 |

6.5 % |

534 |

584 |

(8.6) % |

||||||||

|

West |

943 |

1,011 |

(6.7 %) |

651,841 |

680,666 |

(4.2 %) |

691 |

673 |

2.7 % |

||||||||

|

Total |

2,830 |

2,592 |

9.2 % |

$ 1,661,320 |

$ 1,614,414 |

2.9 % |

$ 587 |

$ 623 |

(5.8 %) |

||||||||

|

Nine Months Ended September 30, |

|||||||||||||||||

|

Net Sales Orders |

Sales Value |

Average Selling Price |

|||||||||||||||

|

(Dollars in thousands) |

2024 |

2023 |

Change |

2024 |

2023 |

Change |

2024 |

2023 |

Change |

||||||||

|

East |

3,595 |

3,066 |

17.3 % |

$ 2,004,598 |

$ 1,786,988 |

12.2 % |

$ 558 |

$ 583 |

(4.3) % |

||||||||

|

Central |

2,466 |

2,123 |

16.2 % |

1,362,042 |

1,248,196 |

9.1 % |

552 |

588 |

(6.1) % |

||||||||

|

West |

3,566 |

3,280 |

8.7 % |

2,404,249 |

2,219,056 |

8.3 % |

674 |

677 |

(0.4) % |

||||||||

|

Total |

9,627 |

8,469 |

13.7 % |

$ 5,770,889 |

$ 5,254,240 |

9.8 % |

$ 599 |

$ 620 |

(3.4) % |

||||||||

|

Sales Order Backlog: |

|||||||||||||||||

|

As of September 30, |

|||||||||||||||||

|

Sold Homes in Backlog |

Sales Value |

Average Selling Price |

|||||||||||||||

|

(Dollars in thousands) |

2024 |

2023 |

Change |

2024 |

2023 |

Change |

2024 |

2023 |

Change |

||||||||

|

East |

2,176 |

2,421 |

(10.1) % |

$ 1,493,828 |

$ 1,613,188 |

(7.4) % |

$ 687 |

$ 666 |

3.2 % |

||||||||

|

Central |

1,238 |

1,464 |

(15.4) % |

758,008 |

960,269 |

(21.1) % |

612 |

656 |

(6.7) % |

||||||||

|

West |

2,278 |

2,233 |

2.0 % |

1,578,168 |

1,523,545 |

3.6 % |

693 |

682 |

1.6 % |

||||||||

|

Total |

5,692 |

6,118 |

(7.0) % |

$ 3,830,004 |

$ 4,097,002 |

(6.5) % |

$ 673 |

$ 670 |

0.4 % |

||||||||

|

Ending Active Selling Communities: |

|||||

|

As of |

Change |

||||

|

September 30, 2024 |

September 30, 2023 |

||||

|

East |

120 |

107 |

12.1 % |

||

|

Central |

106 |

94 |

12.8 % |

||

|

West |

114 |

124 |

(8.1 %) |

||

|

Total |

340 |

325 |

4.6 % |

||

Reconciliation of Non-GAAP Financial Measures

In addition to the results reported in accordance with accounting principles generally accepted in the United States (“GAAP”), we provide our investors with supplemental information relating to: (i) adjusted net income and adjusted earnings per common share, (ii) adjusted income before income taxes and related margin, (iii) adjusted home closings gross margin, (iv) EBITDA and adjusted EBITDA and (v) net homebuilding debt to capitalization ratio.

Adjusted net income, adjusted earnings per common share and adjusted income before income taxes and related margin are non-GAAP financial measures that reflect the net income/(loss) available to the Company excluding, to the extent applicable in a given period, the impact of inventory or land impairment charges, impairment of investment in unconsolidated entities, pre-acquisition abandonment charges, gains/losses on land transfers to joint ventures, extinguishment of debt, net, and legal reserves or settlements that the Company deems not to be in the ordinary course of business and in the case of adjusted net income and adjusted earnings per common share, the tax impact due to such items. Adjusted home closings gross margin is a non-GAAP financial measure calculated on GAAP home closings gross margin (which is inclusive of capitalized interest), excluding inventory impairment charges. EBITDA and Adjusted EBITDA are non-GAAP financial measures that measure performance by adjusting net income before allocation to non-controlling interests to exclude, as applicable, interest expense/(income), net, amortization of capitalized interest, income taxes, depreciation and amortization (EBITDA), non-cash compensation expense, if any, inventory or land impairment charges, impairment of investment in unconsolidated entities, pre-acquisition abandonment charges, gains/losses on land transfers to joint ventures, extinguishment of debt, net and legal reserves or settlements that the Company deems not to be in the ordinary course of business, in each case, as applicable in a given period. Net homebuilding debt to capitalization ratio is a non-GAAP financial measure we calculate by dividing (i) total debt, plus unamortized debt issuance cost/(premium), net, and less mortgage warehouse borrowings, net of unrestricted cash and cash equivalents (“net homebuilding debt”), by (ii) total capitalization (the sum of net homebuilding debt and total stockholders’ equity).

Management uses these non-GAAP financial measures to evaluate our performance on a consolidated basis, as well as the performance of our regions, and to set targets for performance-based compensation. We also use the ratio of net homebuilding debt to total capitalization as an indicator of overall leverage and to evaluate our performance against other companies in the homebuilding industry. In the future, we may include additional adjustments in the above-described non-GAAP financial measures to the extent we deem them appropriate and useful to management and investors.

We believe that adjusted net income, adjusted earnings per common share, adjusted income before income taxes and related margin, as well as EBITDA and adjusted EBITDA, are useful for investors in order to allow them to evaluate our operations without the effects of various items we do not believe are characteristic of our ongoing operations or performance and also because such metrics assist both investors and management in analyzing and benchmarking the performance and value of our business. Adjusted EBITDA also provides an indicator of general economic performance that is not affected by fluctuations in interest rates or effective tax rates, levels of depreciation or amortization, or unusual items. Because we use the ratio of net homebuilding debt to total capitalization to evaluate our performance against other companies in the homebuilding industry, we believe this measure is also relevant and useful to investors for that reason. We believe that adjusted home closings gross margin is useful to investors because it allows investors to evaluate the performance of our homebuilding operations without the varying effects of items or transactions we do not believe are characteristic of our ongoing operations or performance.

These non-GAAP financial measures should be considered in addition to, rather than as a substitute for, the comparable U.S. GAAP financial measures of our operating performance or liquidity. Although other companies in the homebuilding industry may report similar information, their definitions may differ. We urge investors to understand the methods used by other companies to calculate similarly-titled non-GAAP financial measures before comparing their measures to ours.

A reconciliation of (i) adjusted net income and adjusted earnings per common share, (ii) adjusted income before income taxes and related margin, (iii) adjusted home closings gross margin, (iv) EBITDA and adjusted EBITDA and (v) net homebuilding debt to capitalization ratio to the comparable GAAP measures is presented below.

|

Adjusted Net Income and Adjusted Earnings Per Common Share |

|||

|

Three Months Ended September 30, |

|||

|

(Dollars in thousands, except per share data) |

2024 |

2023 |

|

|

Net income |

$ 251,126 |

$ 170,691 |

|

|

Inventory impairment charges (1) |

— |

11,791 |

|

|

Loss on extinguishment of debt, net |

— |

269 |

|

|

Tax impact due to above non-GAAP reconciling items |

— |

(3,060) |

|

|

Adjusted net income |

$ 251,126 |

$ 179,691 |

|

|

Basic weighted average number of shares |

104,132 |

108,837 |

|

|

Adjusted earnings per common share – Basic |

$ 2.41 |

$ 1.65 |

|

|

Diluted weighted average number of shares |

106,089 |

110,622 |

|

|

Adjusted earnings per common share – Diluted |

$ 2.37 |

$ 1.62 |

|

|

Adjusted Income Before Income Taxes and Related Margin |

|||

|

Three Months Ended September 30, |

|||

|

(Dollars in thousands) |

2024 |

2023 |

|

|

Income before income taxes |

332,691 |

228,406 |

|

|

Inventory impairment charges (1) |

— |

11,791 |

|

|

Loss on extinguishment of debt, net |

— |

269 |

|

|

Adjusted income before income taxes |

$ 332,691 |

$ 240,466 |

|

|

Total revenue |

2,120,842 |

1,675,545 |

|

|

Income before income taxes margin |

15.7 % |

13.6 % |

|

|

Adjusted income before income taxes margin |

15.7 % |

14.4 % |

|

|

Adjusted Home Closings Gross Margin |

|||

|

Three Months Ended September 30, |

|||

|

(Dollars in thousands) |

2024 |

2023 |

|

|

Home closings revenue |

$ 2,029,134 |

$ 1,611,883 |

|

|

Cost of home closings |

1,525,825 |

1,238,999 |

|

|

Home closings gross margin |

$ 503,309 |

$ 372,884 |

|

|

Inventory impairment charges (1) |

— |

11,791 |

|

|

Adjusted home closings gross margin |

$ 503,309 |

$ 384,675 |

|

|

Home closings gross margin as a percentage of home closings revenue |

24.8 % |

23.1 % |

|

|

Adjusted home closings gross margin as a percentage of home closings revenue |

24.8 % |

23.9 % |

|

|

EBITDA and Adjusted EBITDA Reconciliation |

|||

|

Three Months Ended |

|||

|

(Dollars in thousands) |

2024 |

2023 |

|

|

Net income before allocation to non-controlling interests |

$ 251,472 |

$ 170,446 |

|

|

Interest expense/(income), net |

3,379 |

(5,782) |

|

|

Amortization of capitalized interest |

30,064 |

32,377 |

|

|

Income tax provision |

81,219 |

57,960 |

|

|

Depreciation and amortization |

2,668 |

2,728 |

|

|

EBITDA |

$ 368,802 |

$ 257,729 |

|

|

Non-cash compensation expense |

5,461 |

5,702 |

|

|

Inventory impairment charges (1) |

— |

11,791 |

|

|

Loss on extinguishment of debt, net |

— |

269 |

|

|

Adjusted EBITDA |

$ 374,263 |

$ 275,491 |

|

|

Total revenue |

$ 2,120,842 |

$ 1,675,545 |

|

|

Net income before allocation to non-controlling interests as a percentage of total revenue |

11.9 % |

10.2 % |

|

|

EBITDA as a percentage of total revenue |

17.4 % |

15.4 % |

|

|

Adjusted EBITDA as a percentage of total revenue |

17.6 % |

16.4 % |

|

|

(1) |

Included in Cost of home closings on the Condensed consolidated statement of operations |

|

Debt to Capitalization Ratios Reconciliation |

|||||

|

(Dollars in thousands) |

As of |

As of |

As of |

||

|

Total debt |

$ 2,143,223 |

$ 2,150,021 |

$ 1,992,077 |

||

|

Plus: unamortized debt issuance cost, net |

7,056 |

7,496 |

8,815 |

||

|

Less: mortgage warehouse borrowings |

(233,331) |

(276,205) |

(191,645) |

||

|

Total homebuilding debt |

$ 1,916,948 |

$ 1,881,312 |

$ 1,809,247 |

||

|

Total equity |

5,723,462 |

5,526,542 |

5,175,110 |

||

|

Total capitalization |

$ 7,640,410 |

$ 7,407,854 |

$ 6,984,357 |

||

|

Total homebuilding debt to capitalization ratio |

25.1 % |

25.4 % |

25.9 % |

||

|

Total homebuilding debt |

$ 1,916,948 |

$ 1,881,312 |

$ 1,809,247 |

||

|

Less: cash and cash equivalents |

(256,447) |

(246,845) |

(613,811) |

||

|

Net homebuilding debt |

$ 1,660,501 |

$ 1,634,467 |

$ 1,195,436 |

||

|

Total equity |

5,723,462 |

5,526,542 |

5,175,110 |

||

|

Total capitalization |

$ 7,383,963 |

$ 7,161,009 |

$ 6,370,546 |

||

|

Net homebuilding debt to capitalization ratio |

22.5 % |

22.8 % |

18.8 % |

||

CONTACT:

Mackenzie Aron, VP Investor Relations

(480) 734-2060

investor@taylormorrison.com

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/taylor-morrison-reports-third-quarter-2024-results-302283720.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/taylor-morrison-reports-third-quarter-2024-results-302283720.html

SOURCE Taylor Morrison

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.