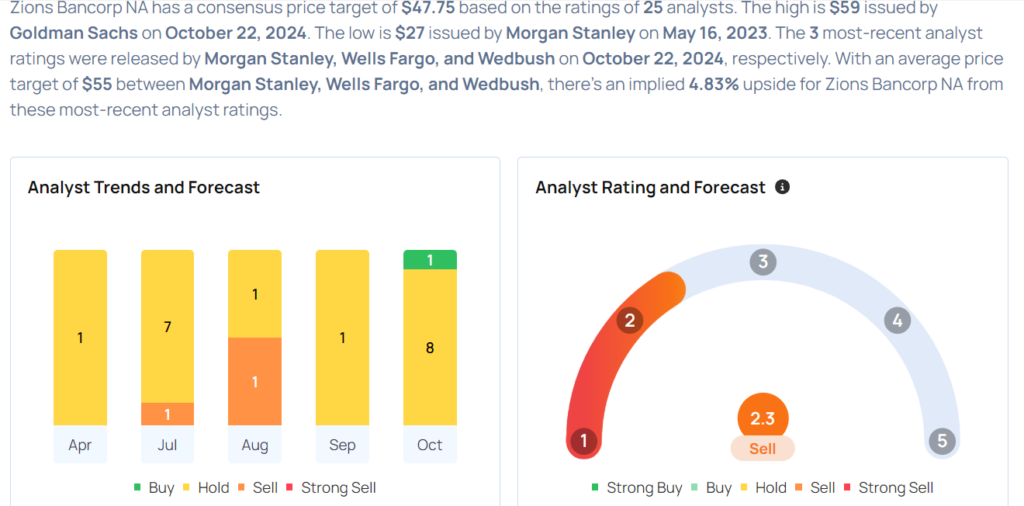

Zions Bancorp Analysts Boost Their Forecasts After Better-Than-Expected Earnings

Zions Bancorporation ZION reported better-than-expected third-quarter financial results on Monday.

Zions Bancorp reported quarterly earnings of $1.37 per share which beat the analyst consensus estimate of $1.17 per share. The company reported quarterly sales of $798.000 million which beat the analyst consensus estimate of $778.857 million.

Harris H. Simmons, Chairman and CEO of Zions Bancorporation, commented, “We’re pleased with the continued improvement in our financial performance, reflected in the 21% increase in earnings per share over the same period last year. The net interest margin strengthened to 3.03% from 2.93% a year ago, and operating costs increased a modest 1%. Average noninterest-bearing demand deposits decreased 1.7% relative to the prior quarter of this year, but were flat to last quarter’s ending balance, suggesting continued stabilization of this important source of low-cost funding. Tangible common equity has grown 28% over the past year, and 8% over the past quarter.”

Zions Bancorporation shares gained 6.4% to trade at $52.58 on Tuesday.

These analysts made changes to their price targets on Zions Bancorporation following earnings announcement.

- Baird analyst David George maintained Zions Bancorp with a Neutral and raised the price target from $52 to $55.

- RBC Capital analyst Jon Arfstrom maintained the stock with a Sector Perform and raised the price target from $55 to $57.

- Stephens & Co. analyst Terry McEvoy maintained the stock with an Equal-Weight and increased the price target from $53 to $55.

- Goldman Sachs analyst Ryan Nash maintained Zions Bancorp with a Neutral and raised the price target from $52 to $59.

- Keefe, Bruyette & Woods analyst Christopher Mcgratty maintained Zions Bancorp with a Market Perform and raised the price target from $53 to $56.

- Wedbush analyst David Chiaverini maintained Zions Bancorp with a Neutral and raised the price target from $52 to $55.

- Wells Fargo analyst Mike Mayo maintained the stock with an Equal-Weight and raised the price target from $50 to $54.

- Morgan Stanley analyst Ken Zerbe maintained Zions Bancorp with an Equal-Weight and raised the price target from $54 to $56.

Considering buying ZION stock? Here’s what analysts think:

Read Next:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

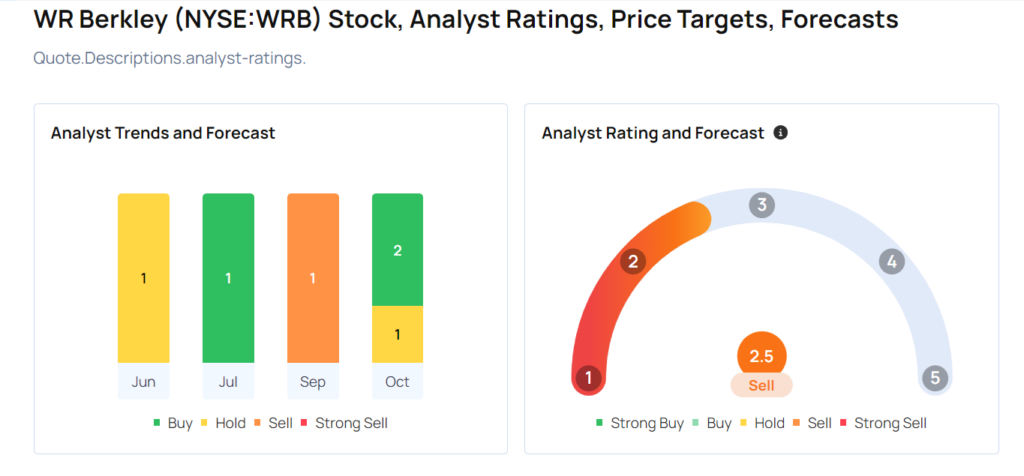

These Analysts Increase Their Forecasts On WR Berkley After Q3 Results

W. R. Berkley Corporation WRB reported better-than-expected earnings for its third quarter on Monday.

The company posted quarterly earnings of 93 cents per share which beat the analyst consensus estimate of 92 cents per share. The company reported quarterly sales of $3.400 billion which missed the analyst consensus estimate of $3.444 billion.

WR Berkley shares fell 4.7% to trade at $58.14 on Tuesday.

These analysts made changes to their price targets on WR Berkley following earnings announcement.

- Evercore ISI Group analyst David Motemaden maintained WR Berkley with an In-Line and raised the price target from $57 to $60.

- Keefe, Bruyette & Woods analyst Meyer Shields maintained the stock with a Market Perform and lowered the price target from $59 to $58.

- RBC Capital analyst Scott Heleniak maintained WR Berkley with a Sector Perform and raised the price target from $57 to $63.

- UBS analyst Brian Meredith maintained the stock with a Buy and raised the price target from $67 to $69.

- Wells Fargo analyst Elyse Greenspan maintained WR Berkley with an Overweight and raised the price target from $63 to $68.

- B of A Securities analyst Joshua Shanker maintained WR Berkley with a Buy and boosted the price target from $73 to $76.

Considering buying WRB stock? Here’s what analysts think:

Read More:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

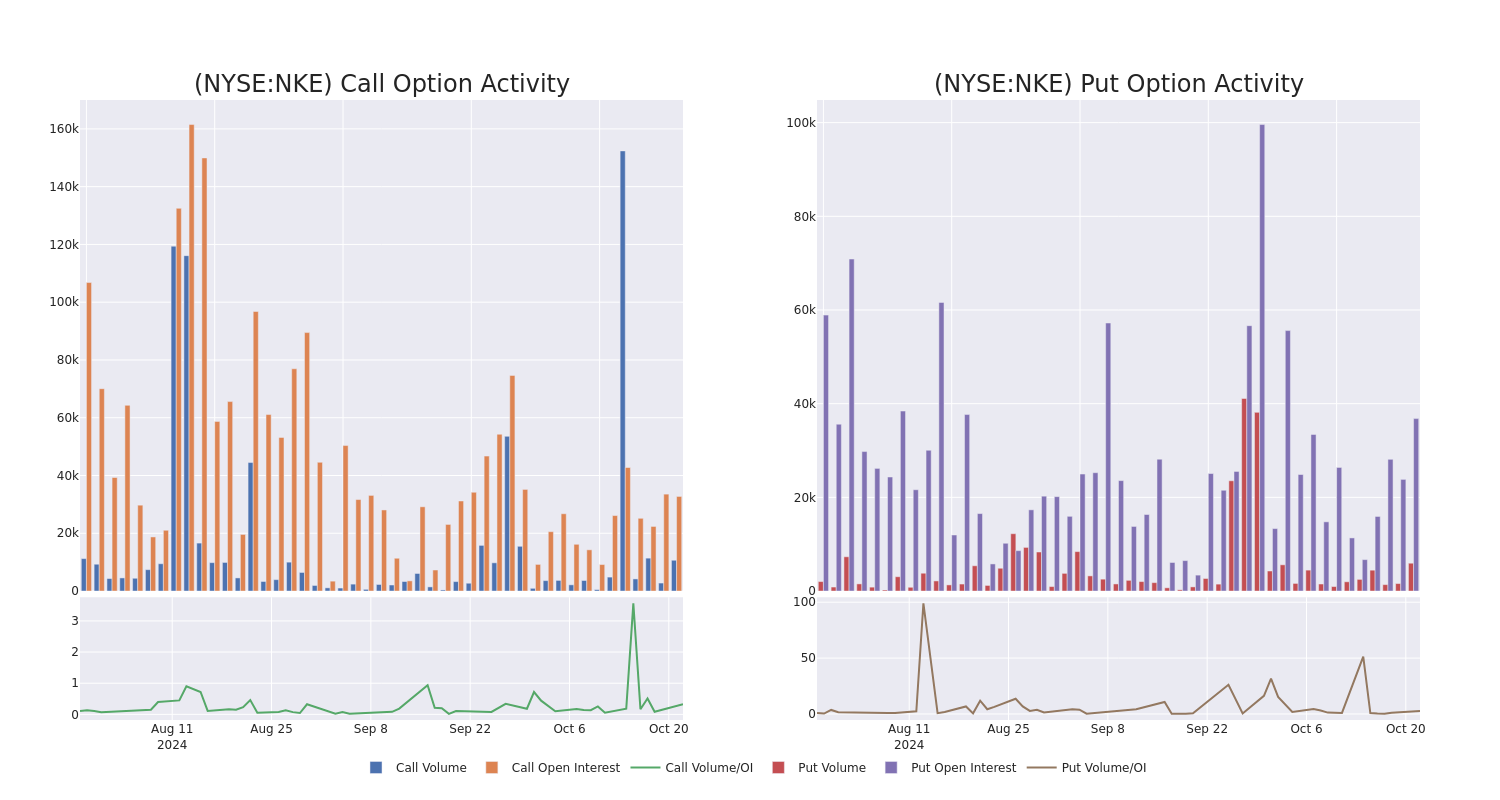

Behind the Scenes of Nike's Latest Options Trends

Financial giants have made a conspicuous bullish move on Nike. Our analysis of options history for Nike NKE revealed 26 unusual trades.

Delving into the details, we found 57% of traders were bullish, while 34% showed bearish tendencies. Out of all the trades we spotted, 15 were puts, with a value of $1,019,899, and 11 were calls, valued at $727,876.

Projected Price Targets

Taking into account the Volume and Open Interest on these contracts, it appears that whales have been targeting a price range from $75.0 to $130.0 for Nike over the last 3 months.

Volume & Open Interest Trends

Looking at the volume and open interest is a powerful move while trading options. This data can help you track the liquidity and interest for Nike’s options for a given strike price. Below, we can observe the evolution of the volume and open interest of calls and puts, respectively, for all of Nike’s whale trades within a strike price range from $75.0 to $130.0 in the last 30 days.

Nike 30-Day Option Volume & Interest Snapshot

Significant Options Trades Detected:

| Symbol | PUT/CALL | Trade Type | Sentiment | Exp. Date | Ask | Bid | Price | Strike Price | Total Trade Price | Open Interest | Volume |

|---|---|---|---|---|---|---|---|---|---|---|---|

| NKE | PUT | SWEEP | BULLISH | 12/20/24 | $1.43 | $1.37 | $1.37 | $75.00 | $205.7K | 13.7K | 1.6K |

| NKE | CALL | SWEEP | BEARISH | 01/17/25 | $9.0 | $8.9 | $9.0 | $75.00 | $162.0K | 7.0K | 495 |

| NKE | PUT | TRADE | BEARISH | 01/17/25 | $3.7 | $3.6 | $3.7 | $80.00 | $128.3K | 10.5K | 455 |

| NKE | CALL | SWEEP | BEARISH | 01/17/25 | $1.05 | $0.96 | $0.96 | $95.00 | $99.9K | 5.3K | 3.5K |

| NKE | PUT | SWEEP | BULLISH | 12/20/24 | $3.05 | $2.93 | $2.93 | $80.00 | $97.2K | 6.7K | 454 |

About Nike

Nike is the largest athletic footwear and apparel brand in the world. Key categories include basketball, running, and football (soccer). Footwear generates about two thirds of its sales. Its brands include Nike, Jordan (premium athletic footwear and clothing), and Converse (casual footwear). Nike sells products worldwide through company-owned stores, franchised stores, and third-party retailers. The firm also operates e-commerce platforms in more than 40 countries. Nearly all its production is outsourced to contract manufacturers in more than 30 countries. Nike was founded in 1964 and is based in Beaverton, Oregon.

Having examined the options trading patterns of Nike, our attention now turns directly to the company. This shift allows us to delve into its present market position and performance

Present Market Standing of Nike

- With a volume of 3,285,197, the price of NKE is down -0.28% at $81.25.

- RSI indicators hint that the underlying stock may be approaching oversold.

- Next earnings are expected to be released in 58 days.

Professional Analyst Ratings for Nike

In the last month, 5 experts released ratings on this stock with an average target price of $87.2.

Turn $1000 into $1270 in just 20 days?

20-year pro options trader reveals his one-line chart technique that shows when to buy and sell. Copy his trades, which have had averaged a 27% profit every 20 days. Click here for access.

* An analyst from Truist Securities has decided to maintain their Hold rating on Nike, which currently sits at a price target of $83.

* An analyst from B of A Securities downgraded its action to Buy with a price target of $104.

* Consistent in their evaluation, an analyst from Morgan Stanley keeps a Equal-Weight rating on Nike with a target price of $82.

* Consistent in their evaluation, an analyst from Jefferies keeps a Hold rating on Nike with a target price of $85.

* Maintaining their stance, an analyst from UBS continues to hold a Neutral rating for Nike, targeting a price of $82.

Trading options involves greater risks but also offers the potential for higher profits. Savvy traders mitigate these risks through ongoing education, strategic trade adjustments, utilizing various indicators, and staying attuned to market dynamics. Keep up with the latest options trades for Nike with Benzinga Pro for real-time alerts.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Preview: Univest Financial's Earnings

Univest Financial UVSP is gearing up to announce its quarterly earnings on Wednesday, 2024-10-23. Here’s a quick overview of what investors should know before the release.

Analysts are estimating that Univest Financial will report an earnings per share (EPS) of $0.55.

Investors in Univest Financial are eagerly awaiting the company’s announcement, hoping for news of surpassing estimates and positive guidance for the next quarter.

It’s worth noting for new investors that stock prices can be heavily influenced by future projections rather than just past performance.

Performance in Previous Earnings

The company’s EPS beat by $0.10 in the last quarter, leading to a 2.66% increase in the share price on the following day.

Here’s a look at Univest Financial’s past performance and the resulting price change:

| Quarter | Q2 2024 | Q1 2024 | Q4 2023 | Q3 2023 |

|---|---|---|---|---|

| EPS Estimate | 0.51 | 0.51 | 0.47 | 0.54 |

| EPS Actual | 0.61 | 0.60 | 0.55 | 0.58 |

| Price Change % | 3.0% | 3.0% | 2.0% | 2.0% |

Univest Financial Share Price Analysis

Shares of Univest Financial were trading at $27.08 as of October 21. Over the last 52-week period, shares are up 60.92%. Given that these returns are generally positive, long-term shareholders should be satisfied going into this earnings release.

To track all earnings releases for Univest Financial visit their earnings calendar on our site.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Constellium Shares Are Falling Behind Competitors As Europe Copes With Aluminum Supply Restraints

As every investor knows — a stock is cheap, and in decline, for a reason.

Over the last 12 months, the NYSE-listed shares of global aluminum giant Constellium CSTM are down 12%, while rivals like Alcoa Corporation AA, Kaiser Aluminum Corporation KALU and Century Aluminum Company CENX are all up. Alcoa is up 55%. CENX is like crypto aluminum, up 155.8% in a year.

Its price-to-earnings ratio is not bad at 12x, and it has a new $65 million investment in a new aluminum plant being built in Alabama, though that is not expected to be operational until the second half of 2026.

What’s the problem?

As some in Washington might say – it’s Russia’s fault.

That’s sort of true. Constellium makes aluminum products that it casts from aluminum sheets, some of which it imports from Russian-based aluminum company Rusal. Prior to the war in Ukraine, the Europeans loved Russian aluminum – especially Rusal aluminum – because a lot of it is made in factories powered by a hydroelectric dam. This means it is deemed low-carbon friendly aluminum. But Rusal aluminum is facing restrictions and that means Constellium is now paying more for primary aluminum than a year ago and is focusing more on European and U.S. production. European producers are in worse shape as they have reduced primary aluminum production by about 30% over the last five years, likely due to environmental regulations.

Constellation: A Victim of Geopolitics

In April, the U.S. Government imposed a 200% tariff on aluminum products if they contained aluminum sourced from Russia, even if the finished product was made elsewhere. Since March 10, 2023, Washington already had increased tariffs on Russian aluminum products up from the Sectio to 200%, up from the roughly 25% in the Section 232 aluminum tariffs imposed globally by then-president Trump in 2018. The supply of Russian aluminum to the United States is currently zero.

U.S. importers have turned to the Middle East for alternatives, increasing prices by an additional $200 per ton from those sources due to U.S. demand.

Europe is thinking of doing the same. This weighs heavily on Constellium shares for the near term, at least until the European Commission decides on what to do about Russian aluminum imports.

A March 4 article by Reuters put it this way: “The loss of Russian metal would leave Europe with a shortfall of around 500,000 tons. Middle Eastern suppliers will not be able to fully substitute Europe’s shortfall quickly.”

A small group of EU countries keep pushing for tougher measures against Russia, led by Poland and the Baltic states. They want U.S.-style restrictions on aluminum imports. Some EU economies are blocking this move, most likely Germany and France, which rely on imports at least in part to manufacture cars and aircraft.

Restrictions on aluminum could pose a threat to domestic industries, which are already losing out in competitiveness to Asia, according to Chris Weafer, the Chief Executive of Macro-Advisory , an investment research firm and consultancy focused on emerging markets with offices in Washington DC. The EU relies on imports for over 90% of its aluminum needs, with 8-9% coming from Russia.

“The EU is walking a tightrope between the need to increase the sanctions pressure on Russia while at the same time…keeping its own economy and domestic enterprises afloat,” Weafer wrote in an op-ed published by Euro News on Oct. 17.

If there are new sanctions, Weafer said in a report to clients last month, there will be some further Russian imports this year because of residual contracts. But after that, Russian imports “eventually fall to zero for the foreseeable future,” he wrote. If there are no sanctions – which is still possible if big industry in Western Europe get their way – then Weafer thinks Russian imports will fall gradually as more European companies will either choose domestic production or be pressured to import from elsewhere.

Earnings Call To Reveal More This Week

Constellium will have their earnings call on Wednesday, Oct. 23 before the market opens.

Investors are likely to wait and see what Europe does about Russia. Constellium’s long-term prospects, meanwhile, seem okay.

The company’s stock survived the Section 232 steel and aluminum tariffs imposed by the Trump administration in March 2018. Constellium’s share price ended the month at $10.85 per share and hit $12.15 per share in May 2018 despite the higher prices associated at the time with the tariff. Constellium today trades closer to $15.

Alcoa stocks rose last week after an earnings beat. JP Morgan raised its price target from $36 to $39. That call is too late for investors now. Alcoa has already surpassed that target and was trading over $41 on Friday.

Constellium could see similar fortunes.

Aluminum is one of the metals required for the energy grid and for new EVs and solar. Global demand is set to reach 85 million tons in 2030, up from 66 million tons in 2020. Given tariffs as they are now, it is clear the U.S. sees aluminum as a critical sector worth protecting, so Constellium’s Alabama project should find plenty of demand locally. Longer-term buyers may be rewarded. For now, out of the four big aluminum companies – AA, KALU and CENX – CSTM is the worst performer. Still, it has a better profit margin than Alcoa at 2.35% versus negative 5.14% for Alcoa and Alcoa just got an upgrade.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Exploring Constellium's Earnings Expectations

Constellium CSTM is preparing to release its quarterly earnings on Wednesday, 2024-10-23. Here’s a brief overview of what investors should keep in mind before the announcement.

Analysts expect Constellium to report an earnings per share (EPS) of $0.50.

The announcement from Constellium is eagerly anticipated, with investors seeking news of surpassing estimates and favorable guidance for the next quarter.

It’s worth noting for new investors that guidance can be a key determinant of stock price movements.

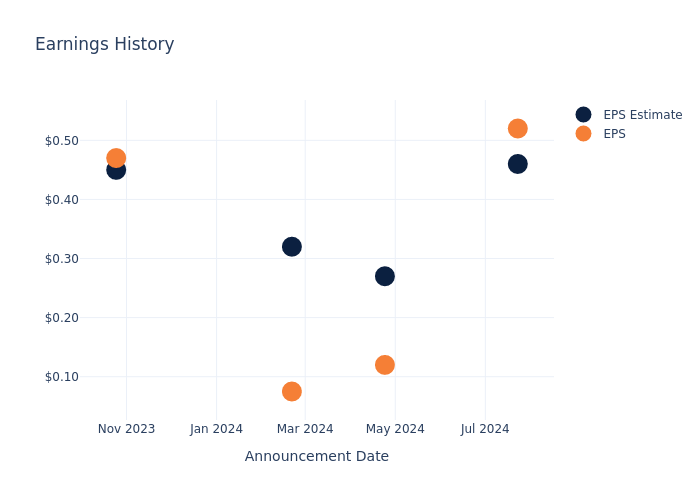

Earnings History Snapshot

In the previous earnings release, the company beat EPS by $0.06, leading to a 2.79% drop in the share price the following trading session.

Here’s a look at Constellium’s past performance and the resulting price change:

| Quarter | Q2 2024 | Q1 2024 | Q4 2023 | Q3 2023 |

|---|---|---|---|---|

| EPS Estimate | 0.46 | 0.27 | 0.320 | 0.45 |

| EPS Actual | 0.52 | 0.12 | 0.075 | 0.47 |

| Price Change % | -3.0% | 2.0% | 1.0% | 4.0% |

Stock Performance

Shares of Constellium were trading at $14.14 as of October 21. Over the last 52-week period, shares are down 1.17%. Given that these returns are generally negative, long-term shareholders are likely a little upset going into this earnings release.

To track all earnings releases for Constellium visit their earnings calendar on our site.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Alexandria Real Estate Equities, Inc. Reports: 3Q24 and YTD 3Q24 Net Income per Share – Diluted of $0.96 and $2.18, respectively; and 3Q24 and YTD 3Q24 FFO per Share – Diluted, as Adjusted, of $2.37 and $7.08, respectively

![]()

PASADENA, Calif., Oct. 21, 2024 /PRNewswire/ — Alexandria Real Estate Equities, Inc. ARE announced financial and operating results for the third quarter ended September 30, 2024.

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

|

Key highlights |

||||||||

|

YTD |

||||||||

|

Operating results |

3Q24 |

3Q23 |

3Q24 |

3Q23 |

||||

|

Total revenues: |

||||||||

|

In millions |

$ 791.6 |

$ 713.8 |

$ 2,327.4 |

$ 2,128.5 |

||||

|

Growth |

10.9 % |

9.3 % |

||||||

|

Net income attributable to Alexandria’s common stockholders – diluted: |

||||||||

|

In millions |

$ 164.7 |

$ 21.9 |

$ 374.5 |

$ 184.4 |

||||

|

Per share |

$ 0.96 |

$ 0.13 |

$ 2.18 |

$ 1.08 |

||||

|

Funds from operations attributable to Alexandria’s common stockholders – diluted, as adjusted: |

||||||||

|

In millions |

$ 407.9 |

$ 386.4 |

$ 1,217.3 |

$ 1,142.5 |

||||

|

Per share |

$ 2.37 |

$ 2.26 |

$ 7.08 |

$ 6.69 |

||||

An industry-leading REIT with a high-quality, diverse tenant base and strong margins

|

(As of September 30, 2024, unless stated otherwise) |

||||

|

Occupancy of operating properties in North America |

94.7 % |

|||

|

Percentage of annual rental revenue in effect from mega campuses |

76 % |

|||

|

Percentage of annual rental revenue in effect from investment-grade or publicly |

53 % |

|||

|

Operating margin |

71 % |

|||

|

Adjusted EBITDA margin |

70 % |

|||

|

Percentage of leases containing annual rent escalations |

96 % |

|||

|

Weighted-average remaining lease term: |

||||

|

Top 20 tenants |

9.5 |

years |

||

|

All tenants |

7.5 |

years |

||

|

Sustained strength in tenant collections: |

||||

|

Tenant receivables as a percentage of 3Q24 rental revenues |

0.9 % |

|||

|

October 2024 tenant rents and receivables collected as of October 21, 2024 |

99.6 % |

|||

|

3Q24 tenant rents and receivables collected as of October 21, 2024 |

99.9 % |

Strong and flexible balance sheet with significant liquidity; top 10% credit rating ranking among all publicly traded U.S. REITs

- Net debt and preferred stock to Adjusted EBITDA of 5.5x and fixed-charge coverage ratio of 4.4x for 3Q24 annualized (targets for 4Q24 annualized of ≤5.1x and ≥4.5x, respectively).

- Significant liquidity of $5.4 billion.

- 31% of our total debt matures in 2049 and beyond.

- 12.6 years weighted-average remaining term of debt.

- Since 2020, an average of 97.7% of our debt has been fixed rate.

- Total debt and preferred stock to gross assets of 29%.

- $1.0 billion of capital contribution commitments from existing consolidated real estate joint venture partners to fund construction from 4Q24 through 2027.

Strong leasing volume and solid rental rate changes

- Strong leasing volume aggregating 1.5 million RSF during 3Q24, up 48% compared to our previous four-quarter average of 1.0 million RSF.

- Rental rate changes on lease renewals and re-leasing of space were 5.1% and 1.5% (cash basis) for 3Q24 and 16.4% and 8.9% (cash basis) for YTD 3Q24.

- 80% of our leasing activity during the last twelve months was generated from our existing tenant base.

|

3Q24 |

YTD 3Q24 |

||||||||

|

Total leasing activity – RSF |

1,486,097 |

3,742,955 |

|||||||

|

Leasing of development and redevelopment space – RSF |

39,121 |

480,342 |

|||||||

|

Lease renewals and re-leasing of space: |

|||||||||

|

RSF (included in total leasing activity above) |

1,278,857 |

2,863,277 |

|||||||

|

Rental rate changes |

5.1 % |

(1) |

16.4 % |

||||||

|

Rental rate changes (cash basis) |

1.5 % |

(1) |

8.9 % |

||||||

|

(1) |

Includes a five-year lease extension to an investment-grade rated technology tenant aggregating 357,136 RSF of recently acquired tech R&D space in our Texas market that was renewed with rental rate changes of (33.6)% and (4.8)% (cash basis). These spaces were originally targeted for a future change in use at acquisition, but we instead renewed them with a lower capital investment while we continue to evaluate options to convert these spaces in the future, subject to market conditions. Excluding this lease, rental rate changes for renewed/re-leased space for 3Q24 were 13.0% and 2.3% (cash basis). |

Attractive dividend strategy to share net cash flows from operating activities with stockholders while retaining a significant portion for reinvestment

- Common stock dividend declared for 3Q24 of $1.30 per common share aggregating $5.14 per common share for the twelve months ended September 30, 2024, up 24 cents, or 5%, over the twelve months ended September 30, 2023.

- Dividend yield of 4.4% as of September 30, 2024.

- Dividend payout ratio of 55% for the three months ended September 30, 2024.

- Average annual dividend per-share growth of 5.4% from 2020 through 3Q24 annualized.

- Significant net cash flows from operating activities after dividends retained for reinvestment aggregating $2.1 billion for the years ended December 31, 2020 through 2023 and including the midpoint of our 2024 guidance range for net cash provided by operating activities after dividends.

Ongoing successful execution of Alexandria’s 2024 capital strategy

We expect to continue pursuing our strategy to fund a significant portion of our capital requirements for the year ending December 31, 2024 with dispositions primarily focused on sales of properties and land parcels not integral to our mega campus strategy. Refer to “Dispositions” in the Earnings Press Release for additional details.

|

(in millions) |

||

|

Completed dispositions of 100% interest in properties |

$ 319 |

|

|

Pending dispositions subject to non-refundable deposits |

577 |

|

|

Pending dispositions subject to executed letters of intent and/or purchase and sale agreements |

603 |

|

|

Forward equity sales agreements |

28 |

|

|

Total |

$ 1,527 |

|

|

2024 guidance midpoint for dispositions and common equity |

$ 1,550 |

Ongoing successful execution of Alexandria’s 2024 capital strategy (continued)

- In September 2024, we completed the following transactions with our longstanding tenant, Fred Hutchinson Cancer Center (“Fred Hutch“), in the Lake Union submarket:

- Sale of 1165 Eastlake Avenue East, a fully leased 100,086 RSF single-tenant Class A+ life science facility that was developed in 2021. We sold the property for $150.0 million, or $1,499 per RSF, at strong capitalization rates of 4.7% and 4.9% (cash basis). Upon completion of the sale, we recognized a gain on sale of real estate aggregating $21.5 million.

- Fred Hutch executed early renewals aggregating 117,479 RSF at our 1201 and 1208 Eastlake Avenue East properties, including a 15-year lease extension at 1201 Eastlake Avenue East.

- Our prior joint venture partner sold their partial interest ownership in each of 1201 and 1208 Eastlake Avenue East to Fred Hutch. Our ownership interest in both properties remains unchanged at 30.0%. This sale, lease extensions, and new joint venture affirm Fred Hutch’s commitment to South Lake Union.

Alexandria’s development and redevelopment pipeline delivered incremental annual net operating income of $21 million commencing during 3Q24 and is expected to deliver incremental annual net operating income aggregating $510 million primarily by 1Q28

- During 3Q24, we placed into service development and redevelopment projects aggregating 316,691 RSF that are 100% leased across multiple submarkets and delivered incremental annual net operating income of $21 million. 3Q24 deliveries included 250,000 RSF at 9820 Darnestown Road on the Alexandria Center® for Life Science – Shady Grove mega campus in our Rockville submarket.

- Annual net operating income (cash basis) is expected to increase by $57 million upon the burn-off of initial free rent, with a weighted-average burn-off period of approximately six months, from recently delivered projects.

- 69% of the RSF in our total development and redevelopment pipeline is within our mega campuses.

|

Development and Redevelopment Projects |

Incremental Annual Net |

RSF |

Leased/ Percentage |

|||||||

|

(dollars in millions) |

||||||||||

|

Placed into service: |

||||||||||

|

1H24 |

$ 42 |

628,427 |

100 % |

|||||||

|

3Q24 |

21 |

316,691 |

100 |

|||||||

|

Placed into service in YTD 3Q24 |

$ 63 |

945,118 |

100 % |

|||||||

|

Expected to be placed into service(1): |

||||||||||

|

4Q24 through 4Q25 |

$ 158 |

(2) |

5,467,897 |

55 % |

||||||

|

1Q26 through 1Q28 |

352 |

(3) |

||||||||

|

$ 510 |

||||||||||

|

(1) |

Represents expected incremental annual net operating income to be placed into service from deliveries of |

||||

|

(2) |

Includes (i) 1.0 million RSF that is expected to stabilize through 2025 and is 92% leased/negotiating and |

||||

|

(3) |

70% of the leased RSF of our development and redevelopment projects was generated from our existing |

Continued solid net operating income and internal growth

- Net operating income (cash basis) of $2.0 billion for 3Q24 annualized, up $274.2 million, or 15.5%, compared to 3Q23 annualized.

- Same property net operating income growth of 1.5% and 6.5% (cash basis) for 3Q24 over 3Q23 and 1.6% and 4.6% (cash basis) for YTD 3Q24 over YTD 3Q23.

- 96% of our leases contain contractual annual rent escalations approximating 3%.

Strong balance sheet management

Key metrics as of or for the three months ended September 30, 2024

- $33.1 billion in total market capitalization.

- $20.5 billion in total equity capitalization, which ranks in the top 10% among all publicly traded U.S. REITs.

|

3Q24 |

Target |

|||||

|

Quarter |

Trailing 12 Months |

4Q24 Annualized |

||||

|

Net debt and preferred stock to |

5.5x |

5.6x |

Less than or equal to 5.1x |

|||

|

Fixed-charge coverage ratio |

4.4x |

4.5x |

Greater than or equal to 4.5x |

|||

Key capital events

- In September 2024, we amended and restated our unsecured senior line of credit to, among other changes, extend the maturity date from January 22, 2028 to January 22, 2030, including extension options that we control.

- During 3Q24, we had no activity under our ATM program. As of October 21, 2024, the remaining aggregate amount available for future sales of common stock was $1.47 billion.

Investments

- As of September 30, 2024:

- Our non-real estate investments aggregated $1.5 billion.

- Unrealized gains presented in our consolidated balance sheet were $166.2 million, comprising gross unrealized gains and losses aggregating $284.4 million and $118.2 million, respectively.

- Investment income of $15.2 million for 3Q24 presented in our consolidated statement of operations consisted of $23.0 million of realized gains and $2.6 million of unrealized gains, partially offset by $10.3 million of impairment charges.

Other key highlights

|

Key items included in net income attributable to Alexandria’s common stockholders: |

||||||||||||||||

|

YTD |

||||||||||||||||

|

3Q24 |

3Q23 |

3Q24 |

3Q23 |

3Q24 |

3Q23 |

3Q24 |

3Q23 |

|||||||||

|

(in millions, except per share |

Amount |

Per Share – |

Amount |

Per Share – |

||||||||||||

|

Unrealized gains (losses) on |

$ 2.6 |

$ (77.2) |

$ 0.02 |

$ (0.45) |

$ (32.5) |

$ (221.0) |

$ (0.19) |

$ (1.29) |

||||||||

|

Gain on sales of real estate |

27.1 |

— |

0.16 |

— |

27.5 |

214.8 |

0.16 |

1.26 |

||||||||

|

Impairment of non-real estate |

(10.3) |

(28.5) |

(0.06) |

(0.17) |

(37.8) |

(51.5) |

(0.22) |

(0.30) |

||||||||

|

Impairment of real estate |

(5.7) |

(20.6) |

(0.03) |

(0.12) |

(36.5) |

(189.2) |

(0.22) |

(1.11) |

||||||||

|

Acceleration of stock |

— |

(1.9) |

— |

(0.01) |

— |

(1.9) |

— |

(0.01) |

||||||||

|

Total |

$ 13.7 |

$ (128.2) |

$ 0.09 |

$ (0.75) |

$ (79.3) |

$ (248.8) |

$ (0.47) |

$ (1.45) |

||||||||

|

Refer to “Funds from operations and funds from operations per share” in the Earnings Press Release for additional |

||||||||||||||||

Subsequent events

- In October 2024, we agreed to sell four properties located in our Greater Boston market for a sales price of $369.4 million to the current tenant of the properties with whom we have a long-established relationship. The sales price represents capitalization rates of 8.5% and 6.3% (cash basis) based upon net operating income and net operating income (cash basis), respectively, for 3Q24 annualized. These properties, acquired primarily during 2020–2021, are currently 100% leased with a weighted-average remaining lease term of 18 years. In October 2024, we recognized an impairment charge aggregating $40.9 million to reduce the carrying amounts of these properties by approximately 10% to the expected sales price less costs to sell. Our decision to dispose of these properties is based on their non-strategic location and the significant capital that the expected sales proceeds provide for immediate reinvestment into our development and redevelopment pipeline.

- In October 2024, we agreed to sell five operating properties aggregating 203,223 RSF and land parcels aggregating 1.5 million SF in our Sorrento Mesa and University Town Center submarkets to buyers that are expected to develop residential properties on these sites for an aggregate sales price of approximately $314.0 million. In October 2024, we recognized impairment charges aggregating $65.9 million to reduce the carrying amounts of these properties to the expected aggregate sales price less costs to sell. Our decision to dispose of these assets, which are not integral to our mega campus strategy, is primarily based on the substantial capital that the sales proceeds will provide for immediate reinvestment into our development and redevelopment pipeline.

Industry and corporate responsibility leadership: catalyzing and leading the way for positive change to benefit human health and society

- In September 2024, Alexandria was named one of the World’s Most Trustworthy Companies by Newsweek. This significant distinction builds on the Company’s recognition by the publication as one of America’s Most Trustworthy Companies in 2023 and 2024. Alexandria is one of only three S&P 500 REITs recognized in the real estate and housing category.

- In September 2024, Alexandria and its executive chairman and founder, Joel S. Marcus, were honored with the inaugural Bisnow Life Sciences Icon & Influencer Award. This prestigious award highlights Mr. Marcus and the Company’s significant long-term contributions to and lasting impact on the life science real estate sector and broader life science industry. Mr. Marcus accepted the award on his own behalf and that of Alexandria at Bisnow’s International Life Sciences & Biotech Conference, where he was also the keynote speaker.

- Alexandria continued to receive broad recognition for our operational excellence in asset management, design, development, and sustainability, including the following recent awards:

- In our Greater Boston market, the atrium at 325 Binney Street, located on the Alexandria Center® at One Kendall Square mega campus, is a light-filled collaboration space with a terraced garden and communal staircase that was celebrated for design excellence in the Science & Research – Small (under 50,000 SF) category of the 2024 International Interior Design Association New England (IIDA NE) Design Awards and also received the award program’s top honor, Best in Show.

- In our Maryland market, we were awarded three 2024 NAIOP DC|MD Awards of Excellence for developments and enhancements on the Alexandria Center® for Life Science – Shady Grove mega campus: 9810 and 9820 Darnestown Road for Best Life Science Facility, 9800 Medical Center Drive for Best Amenity Space, and 9950 Medical Center Drive for Best Industrial/Flex.

- We received a 2024 Nareit Sustainable Design Impact Award for our groundbreaking approach to utilizing alternative energy sources such as geothermal energy and wastewater heat recovery systems to reduce operational greenhouse gas emissions in Labspace® development projects in our Greater Boston and Seattle markets.

- Alexandria GradLabs® at 9880 Campus Point Drive, located on the Campus Point by Alexandria mega campus in our San Diego market, earned a 2024 International Institute for Sustainable Laboratories (I2SL) Lab Buildings and Projects Award for Excellence in Energy Efficiency. The state-of-the-art building was designed to operate as a highly energy-efficient research facility. In 2023, the LEED Platinum certified facility earned an I2SL Labs2Zero pilot Energy Score of 96 out of 100, indicating its operational energy performance is better than 96% of similar facilities.

About Alexandria Real Estate Equities, Inc.

Alexandria Real Estate Equities, Inc. ARE, an S&P 500® company, is a best-in-class, mission-driven life science REIT making a positive and lasting impact on the world. As the pioneer of the life science real estate niche with our founding in 1994, Alexandria is the preeminent and longest-tenured owner, operator, and developer of collaborative mega campuses in AAA life science innovation cluster locations, including Greater Boston, the San Francisco Bay Area, San Diego, Seattle, Maryland, Research Triangle, and New York City. As of September 30, 2024, Alexandria has a total market capitalization of $33.1 billion and an asset base in North America that includes 41.8 million RSF of operating properties, 5.3 million RSF of Class A/A+ properties undergoing construction, and one committed near-term project expected to commence construction in the next two years. Alexandria has a longstanding and proven track record of developing Class A/A+ properties clustered in mega campuses that provide our innovative tenants with highly dynamic and collaborative environments that enhance their ability to successfully recruit and retain world-class talent and inspire productivity, efficiency, creativity, and success. Alexandria also provides strategic capital to transformative life science companies through our venture capital platform. We believe our unique business model and diligent underwriting ensure a high-quality and diverse tenant base that results in higher occupancy levels, longer lease terms, higher rental income, higher returns, and greater long-term asset value. For more information on Alexandria, please visit www.are.com.

|

Guidance |

|

The following guidance for 2024 has been updated to reflect our current view of existing market conditions and assumptions for the year ending December 31, 2024. There can be no assurance that |

|

2024 Guidance Midpoint |

||||||||||

|

Summary of Key Changes in Guidance |

As of 10/21/24 |

As of 7/22/24 |

Summary of Key Changes in Sources and Uses of Capital |

As of 10/21/24 |

As of 7/22/24 |

|||||

|

EPS, FFO per share, and FFO per share, as adjusted |

See updates below |

Cash expected to be held at December 31, 2024 |

$150 |

$— |

||||||

|

Straight-line rent revenue |

$147 to $162 |

$169 to $184 |

||||||||

|

General and administrative expenses |

$176 to $186 |

$181 to $191 |

||||||||

|

Key Credit Metric Targets(1) |

||

|

Net debt and preferred stock to Adjusted EBITDA – 4Q24 annualized |

Less than or equal to 5.1x |

|

|

Fixed-charge coverage ratio – 4Q24 annualized |

Greater than or equal to 4.5x |

|

Projected 2024 Earnings per Share and Funds From Operations per Share Attributable to |

|||||||||

|

As of 10/21/24 |

As of 7/22/24 |

||||||||

|

Earnings per share(2) |

$2.60 to $2.64 |

$2.98 to $3.10 |

|||||||

|

Depreciation and amortization of real estate assets |

6.05 |

5.95 |

|||||||

|

Gain on sales of real estate(3) |

(0.38) |

— |

|||||||

|

Impairment of real estate – rental properties and land(4) |

0.67 |

0.01 |

|||||||

|

Allocation to unvested restricted stock awards |

(0.06) |

(0.05) |

|||||||

|

Funds from operations per share(1) |

$8.88 to $8.92 |

$8.89 to $9.01 |

|||||||

|

Unrealized losses on non-real estate investments |

0.19 |

0.20 |

|||||||

|

Impairment of non-real estate investments |

0.22 |

0.16 |

|||||||

|

Impairment of real estate |

0.17 |

0.17 |

|||||||

|

Allocation to unvested restricted stock awards |

(0.01) |

(0.01) |

|||||||

|

Funds from operations per share, as adjusted(1) |

$9.45 to $9.49 |

$9.41 to $9.53 |

|||||||

|

Midpoint |

$9.47 |

$9.47 |

|||||||

|

Certain |

|||||||||

|

Key Sources and Uses of Capital |

Range |

Midpoint |

|||||||

|

Sources of capital: |

|||||||||

|

Incremental debt |

$ 885 |

$ 1,185 |

$ 1,035 |

See below |

|||||

|

Net cash provided by operating activities after |

400 |

500 |

450 |

||||||

|

Dispositions and common equity(5) |

1,050 |

2,050 |

1,550 |

(5) |

|||||

|

Total sources of capital |

$ 2,335 |

$ 3,735 |

$ 3,035 |

||||||

|

Uses of capital: |

|||||||||

|

Construction |

$ 1,950 |

$ 2,550 |

$ 2,250 |

||||||

|

Acquisitions |

250 |

750 |

500 |

$ 249 |

|||||

|

Ground lease prepayment(6) |

135 |

135 |

135 |

||||||

|

Cash expected to be held at December 31, 2024(7) |

— |

300 |

150 |

||||||

|

Total uses of capital |

$ 2,335 |

$ 3,735 |

$ 3,035 |

||||||

|

Incremental debt (included above): |

|||||||||

|

Issuance of unsecured senior notes payable(8) |

$ 1,000 |

$ 1,000 |

$ 1,000 |

$ 1,000 |

(8) |

||||

|

Unsecured senior line of credit, commercial paper, |

(115) |

185 |

35 |

||||||

|

Net incremental debt |

$ 885 |

$ 1,185 |

$ 1,035 |

||||||

|

Key Assumptions |

Low |

High |

|||

|

Occupancy percentage in North America as of December 31, 2024 |

94.6 % |

95.6 % |

|||

|

Lease renewals and re-leasing of space: |

|||||

|

Rental rate changes |

11.0 % |

19.0 % |

|||

|

Rental rate changes (cash basis) |

5.0 % |

13.0 % |

|||

|

Same property performance: |

|||||

|

Net operating income changes |

0.5 % |

2.5 % |

|||

|

Net operating income changes (cash basis) |

3.0 % |

5.0 % |

|||

|

Straight-line rent revenue(9) |

$ 147 |

$ 162 |

|||

|

General and administrative expenses(10) |

$ 176 |

$ 186 |

|||

|

Capitalization of interest |

$ 325 |

$ 355 |

|||

|

Interest expense |

$ 154 |

$ 184 |

|||

|

Realized gains on non-real estate investments(11) |

$ 95 |

$ 125 |

|

(1) |

Refer to “Definitions and reconciliations” in the Supplemental Information for additional details. |

|

(2) |

Excludes unrealized gains or losses on non-real estate investments after September 30, 2024 that are required to be recognized in earnings and are excluded from funds from operations per share, as adjusted. |

|

(3) |

Includes $37.1 million of gain on sales of real estate recognized in October 2024. Refer to “Dispositions” in the Earnings Press Release for additional details. |

|

(4) |

Includes $106.8 million of real estate impairments recognized in October 2024. Refer to “Subsequent Events” in the Earnings Press Release for additional details. |

|

(5) |

We expect to fund our remaining capital requirements for the year ending December 31, 2024 with real estate dispositions. As of October 21, 2024, we completed real estate dispositions aggregating $319.2 million, have additional pending transactions subject to (i) non-refundable deposits aggregating $577.2 million and (ii) executed letters of intent and/or purchase and sale agreements aggregating $602.5 million and forward equity sales agreements aggregating $28 million, which in aggregate, represents 98% of the $1.55 billion midpoint of our guidance range. We do not expect to issue additional equity in 2024 beyond the existing forward equity sales agreements outstanding. |

|

(6) |

In July 2024, we executed an amendment to our existing ground lease agreement at the Alexandria Technology Square® mega campus in our Cambridge submarket, which requires that we prepay our entire rent obligation for the extended lease term aggregating $270.0 million in two equal installments during the fourth quarter of 2024 and the first quarter of 2025. |

|

(7) |

The increase in cash expected to be held at December 31, 2024 is primarily due to changes in the mix and timing of pending dispositions that are subject to non-refundable deposits or subject to executed letters of intent and/or purchase and sale agreements that are expected to close in 4Q24. This cash is expected to reduce our 2025 debt capital needs. |

|

(8) |

Represents $1.0 billion of unsecured senior notes payable issued in February 2024. Subject to market conditions, we may seek additional opportunities in 2024 to fund all or a portion of the proceeds necessary for the repayment of our $600.0 million of 3.45% unsecured senior notes payable due on April 30, 2025 through the issuance of additional unsecured senior notes payable that is not assumed in our current 2024 guidance. |

|

(9) |

Reduction in the midpoint of our guidance range for straight-line rent revenue by $22 million is primarily attributable to (i) the write-off of a deferred rent receivable of $9 million related to the lease termination and a payment of $10 million from a tenant at 409 Illinois Street in our Mission Bay submarket, a 234,249 RSF property owned by our consolidated real estate joint venture for which we have an ownership interest of 25%, and (ii) a change in the expected stabilization date from 4Q24 to 1Q25 at our fully leased development project at 230 Harriet Tubman Way in our South San Francisco submarket as reported in our 2Q24 Earnings Press Release and Supplemental Information. |

|

(10) |

Reduction in the midpoint of our guidance range for general and administrative expense by $5 million is primarily attributable to the realization of savings associated with overall efficiencies, including enhanced cost control measures, incremental use of technology, streamlined processes, and optimization of execution in connection with the sale of non-core assets not integral to our mega campus strategy. |

|

(11) |

Represents realized gains and losses included in funds from operations per share – diluted, as adjusted, and excludes significant impairments realized on non-real estate investments, if any. Refer to “Investments” in the Supplemental Information for additional details. |

|

Acquisitions |

|||||||||||||||||

|

Property |

Submarket/Market |

Date of Purchase |

Number of |

Operating Occupancy |

Square Footage |

Purchase Price |

|||||||||||

|

Future |

Operating With |

||||||||||||||||

|

Completed in 1H24: |

|||||||||||||||||

|

285, 299, 307, and 345 Dorchester Avenue (60% |

Seaport Innovation District/Greater |

1/30/24 |

— |

N/A |

1,040,000 |

— |

$ |

155,321 |

|||||||||

|

Other |

46,490 |

||||||||||||||||

|

201,811 |

|||||||||||||||||

|

Completed in October 2024: |

|||||||||||||||||

|

428 Westlake Avenue North |

Lake Union/Seattle |

10/1/24 |

1 |

100 % |

— |

88,514 |

47,600 |

||||||||||

|

$ |

249,411 |

||||||||||||||||

|

2024 guidance range for acquisitions |

$250,000 – $750,000 |

||||||||||||||||

|

(1) |

We expect to provide total estimated costs and related yields for development and significant redevelopment projects in the future, subsequent to the commencement of construction. |

|

Dispositions |

|||||||||||||||||||

|

Property |

Submarket/Market |

Date of |

Interest |

RSF |

Capitalization |

Capitalization (Cash Basis) |

Sales Price |

Sales Price |

|||||||||||

|

Completed in 1H24 |

$ 17,213 |

||||||||||||||||||

|

Completed in 3Q24: |

|||||||||||||||||||

|

Sale to longstanding tenant |

|||||||||||||||||||

|

1165 Eastlake Avenue East |

Lake Union/Seattle |

9/12/24 |

100 % |

100,086 |

4.7 % |

4.9 % |

149,985 |

(1) |

$ 1,499 |

||||||||||

|

Dispositions of properties not integral to our mega campus |

|||||||||||||||||||

|

219 East 42nd Street |

New York City/New York City |

7/9/24 |

100 % |

349,947 |

N/A |

N/A |

60,000 |

(2) |

N/A |

||||||||||

|

Other |

11,511 |

||||||||||||||||||

|

221,496 |

(3) |

||||||||||||||||||

|

Dispositions completed in YTD 3Q24 |

238,709 |

||||||||||||||||||

|

Completed in October 2024: |

|||||||||||||||||||

|

Dispositions of properties not integral to our mega campus |

|||||||||||||||||||

|

14225 Newbrook Drive |

Northern Virginia/Maryland |

10/15/24 |

100 % |

248,186 |

7.6 % |

7.4 % |

80,500 |

(4) |

$ 324 |

||||||||||

|

319,209 |

|||||||||||||||||||

|

Pending 4Q24 dispositions subsequent to October 21, 2024: |

|||||||||||||||||||

|

Subject to non-refundable deposits |

|||||||||||||||||||

|

Sale to longstanding tenant |

Greater Boston |

4Q24 |

100 % |

8.5 % |

6.3 % |

369,439 |

(5) |

||||||||||||

|

Other |

207,713 |

||||||||||||||||||

|

577,152 |

|||||||||||||||||||

|

Subject to executed letters of intent and/or purchase and sale |

602,500 |

(5) |

|||||||||||||||||

|

1,179,652 |

(6) |

||||||||||||||||||

|

$ 1,498,861 |

|||||||||||||||||||

|

2024 guidance range for dispositions and common equity |

$1,050,000 – $2,050,000 |

||||||||||||||||||

|

(1) |

Upon completion of the sale, we recognized a gain on sale of real estate aggregating $21.5 million. |

|

(2) |

The property was leased to a single tenant with a July 2024 lease expiration and had annual net operating income of $18.6 million based on 2Q24 annualized. This property was previously considered to be a potential development project upon expiration of the in-place non-laboratory space lease. |

|

(3) |

Dispositions completed during the three months ended September 30, 2024 had annual net operating income of $26.5 million (based on 2Q24 annualized) with a weighted-average disposition date of July 28, 2024 (weighted by net operating income for 2Q24 annualized). |

|

(4) |

Demonstrating the long-term enduring value of our laboratory facilities, Alexandria successfully operated our only asset in the Northern Virginia submarket from its acquisition in 1997 (prior to our IPO) through its sale in October 2024. Upon completion of the sale, we recognized a gain on sale of real estate aggregating $37.1 million. |

|

(5) |

Refer to “Subsequent events” in the Earnings Press Release for additional details. |

|

(6) |

Pending dispositions subsequent to October 21, 2024 have estimated annual net operating income of approximately $95.8 million (based on 3Q24 annualized) with a weighted-average non-core estimated stand-alone disposition date of December 5, 2024 (weighted by net operating income for 3Q24 annualized). Approximately half of our pending dispositions are non-core stabilized stand-alone properties with weighted-average capitalization rates of 8.5% and 7.0% (cash basis), and the remaining half are land and non-stabilized properties that have vacancy or significant near-term lease expirations that will require capital to re-tenant, including one building with approximately 72% of non-laboratory space. |

Earnings Call Information and About the Company

September 30, 2024

We will host a conference call on Tuesday, October 22, 2024, at 3:00 p.m. Eastern Time (“ET”)/noon Pacific Time (“PT”), which is open to the general public, to discuss our financial and operating results for the third quarter ended September 30, 2024. To participate in this conference call, dial (833) 366-1125 or (412) 902-6738 shortly before 3:00 p.m. ET/noon PT and ask the operator to join the call for Alexandria Real Estate Equities, Inc. The audio webcast can be accessed at www.are.com in the “For Investors” section. A replay of the call will be available for a limited time from 5:00 p.m. ET/2:00 p.m. PT on Tuesday, October 22, 2024. The replay number is (877) 344-7529 or (412) 317-0088, and the access code is 1168152.

Additionally, a copy of this Earnings Press Release and Supplemental Information for the third quarter ended September 30, 2024 is available in the “For Investors” section of our website at www.are.com or by following this link: https://www.are.com/fs/2024q3.pdf.

For any questions, please contact corporateinformation@are.com; Joel S. Marcus, executive chairman and founder; Peter M. Moglia, chief executive officer and chief investment officer; Marc E. Binda, chief financial officer and treasurer; Paula Schwartz, managing director of Rx Communications Group, at (917) 633-7790; or Sara M. Kabakoff, senior vice president – chief content officer.

About the Company

Alexandria Real Estate Equities, Inc. ARE, an S&P 500® company, is a best-in-class, mission-driven life science REIT making a positive and lasting impact on the world. As the pioneer of the life science real estate niche with our founding in 1994, Alexandria is the preeminent and longest-tenured owner, operator, and developer of collaborative mega campuses in AAA life science innovation cluster locations, including Greater Boston, the San Francisco Bay Area, San Diego, Seattle, Maryland, Research Triangle, and New York City. As of September 30, 2024, Alexandria has a total market capitalization of $33.1 billion and an asset base in North America that includes 41.8 million RSF of operating properties, 5.3 million RSF of Class A/A+ properties undergoing construction, and one committed near-term project expected to commence construction in the next two years. Alexandria has a longstanding and proven track record of developing Class A/A+ properties clustered in mega campuses that provide our innovative tenants with highly dynamic and collaborative environments that enhance their ability to successfully recruit and retain world-class talent and inspire productivity, efficiency, creativity, and success. Alexandria also provides strategic capital to transformative life science companies through our venture capital platform. We believe our unique business model and diligent underwriting ensure a high-quality and diverse tenant base that results in higher occupancy levels, longer lease terms, higher rental income, higher returns, and greater long-term asset value. For more information on Alexandria, please visit www.are.com.

Forward-Looking Statements

This document includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such forward-looking statements include, without limitation, statements regarding our 2024 earnings per share, 2024 funds from operations per share, 2024 funds from operations per share, as adjusted, net operating income, and our projected sources and uses of capital. You can identify the forward-looking statements by their use of forward-looking words, such as “forecast,” “guidance,” “goals,” “projects,” “estimates,” “anticipates,” “believes,” “expects,” “intends,” “may,” “plans,” “seeks,” “should,” “targets,” or “will,” or the negative of those words or similar words. These forward-looking statements are based on our current expectations, beliefs, projections, future plans and strategies, anticipated events or trends, and similar expressions concerning matters that are not historical facts, as well as a number of assumptions concerning future events. There can be no assurance that actual results will not be materially higher or lower than these expectations. These statements are subject to risks, uncertainties, assumptions, and other important factors that could cause actual results to differ materially from the results discussed in the forward-looking statements. Factors that might cause such a difference include, without limitation, our failure to obtain capital (debt, construction financing, and/or equity) or refinance debt maturities, lower than expected yields, increased interest rates and operating costs, adverse economic or real estate developments in our markets, our failure to successfully place into service and lease any properties undergoing development or redevelopment and our existing space held for future development or redevelopment (including new properties acquired for that purpose), our failure to successfully operate or lease acquired properties, decreased rental rates, increased vacancy rates or failure to renew or replace expiring leases, defaults on or non-renewal of leases by tenants, adverse general and local economic conditions, an unfavorable capital market environment, decreased leasing activity or lease renewals, failure to obtain LEED and other healthy building certifications and efficiencies, and other risks and uncertainties detailed in our filings with the Securities and Exchange Commission (“SEC”). Accordingly, you are cautioned not to place undue reliance on such forward-looking statements. All forward-looking statements are made as of the date of this Earnings Press Release and Supplemental Information, and unless otherwise stated, we assume no obligation to update this information and expressly disclaim any obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. For more discussion relating to risks and uncertainties that could cause actual results to differ materially from those anticipated in our forward-looking statements, and risks to our business in general, please refer to our SEC filings, including our most recent annual report on Form 10-K and any subsequent quarterly reports on Form 10-Q.

This document is not an offer to sell or a solicitation to buy securities of Alexandria Real Estate Equities, Inc. Any offers to sell or solicitations to buy our securities shall be made only by means of a prospectus approved for that purpose. Unless otherwise indicated, the “Company,” “Alexandria,” “ARE,” “we,” “us,” and “our” refer to Alexandria Real Estate Equities, Inc. and our consolidated subsidiaries. Alexandria®, Lighthouse Design® logo, Building the Future of Life-Changing Innovation®, That’s What’s in Our DNA®, Labspace®, At the Vanguard and Heart of the Life Science Ecosystem™, Alexandria Center®, Alexandria Technology Square®, Alexandria Technology Center®, and Alexandria Innovation Center® are copyrights and trademarks of Alexandria Real Estate Equities, Inc. All other company names, trademarks, and logos referenced herein are the property of their respective owners.

|

Consolidated Statements of Operations |

||||||||||||||

|

Three Months Ended |

Nine Months Ended |

|||||||||||||

|

9/30/24 |

6/30/24 |

3/31/24 |

12/31/23 |

9/30/23 |

9/30/24 |

9/30/23 |

||||||||

|

Revenues: |

||||||||||||||

|

Income from rentals |

$ 775,744 |

$ 755,162 |

$ 755,551 |

$ 742,637 |

$ 707,531 |

$ 2,286,457 |

$ 2,099,819 |

|||||||

|

Other income |

15,863 |

11,572 |

13,557 |

14,579 |

6,257 |

40,992 |

28,664 |

|||||||

|

Total revenues |

791,607 |

766,734 |

769,108 |

757,216 |

713,788 |

2,327,449 |

2,128,483 |

|||||||

|

Expenses: |

||||||||||||||

|

Rental operations |

233,265 |

217,254 |

218,314 |

222,726 |

217,687 |

668,833 |

636,454 |

|||||||

|

General and administrative |

43,945 |

44,629 |

47,055 |

59,289 |

45,987 |

135,629 |

140,065 |

|||||||

|

Interest |

43,550 |

45,789 |

40,840 |

31,967 |

11,411 |

130,179 |

42,237 |

|||||||

|

Depreciation and amortization |

293,998 |

290,720 |

287,554 |

285,246 |

269,370 |

872,272 |

808,227 |

|||||||

|

Impairment of real estate |

5,741 |

30,763 |

— |

271,890 |

20,649 |

36,504 |

189,224 |

|||||||

|

Total expenses |

620,499 |

629,155 |

593,763 |

871,118 |

565,104 |

1,843,417 |

1,816,207 |

|||||||

|

Equity in earnings of unconsolidated real estate joint ventures |

139 |

130 |

155 |

363 |

242 |

424 |

617 |

|||||||

|

Investment income (loss) |

15,242 |

(43,660) |

43,284 |

8,654 |

(80,672) |

14,866 |

(204,051) |

|||||||

|

Gain on sales of real estate |

27,114 |

— |

392 |

62,227 |

— |

27,506 |

214,810 |

|||||||

|

Net income (loss) |

213,603 |

94,049 |

219,176 |

(42,658) |

68,254 |

526,828 |

323,652 |

|||||||

|

Net income attributable to noncontrolling interests |

(45,656) |

(47,347) |

(48,631) |

(45,771) |

(43,985) |

(141,634) |

(131,584) |

|||||||

|

Net income (loss) attributable to Alexandria Real Estate Equities, Inc.’s |

167,947 |

46,702 |

170,545 |

(88,429) |

24,269 |

385,194 |

192,068 |

|||||||

|

Net income attributable to unvested restricted stock awards |

(3,273) |

(3,785) |

(3,659) |

(3,498) |

(2,414) |

(10,717) |

(7,697) |

|||||||

|

Net income (loss) attributable to Alexandria Real Estate Equities, Inc.’s |

$ 164,674 |

$ 42,917 |

$ 166,886 |

$ (91,927) |

$ 21,855 |

$ 374,477 |

$ 184,371 |

|||||||

|

Net income (loss) per share attributable to Alexandria Real Estate Equities, |

||||||||||||||

|

Basic |

$ 0.96 |

$ 0.25 |

$ 0.97 |

$ (0.54) |

$ 0.13 |

$ 2.18 |

$ 1.08 |

|||||||

|

Diluted |

$ 0.96 |

$ 0.25 |

$ 0.97 |

$ (0.54) |

$ 0.13 |

$ 2.18 |

$ 1.08 |

|||||||

|

Weighted-average shares of common stock outstanding: |

||||||||||||||

|

Basic |

172,058 |

172,013 |

171,949 |

171,096 |

170,890 |

172,007 |

170,846 |

|||||||

|

Diluted |

172,058 |

172,013 |

171,949 |

171,096 |

170,890 |

172,007 |

170,846 |

|||||||

|

Dividends declared per share of common stock |

$ 1.30 |

$ 1.30 |

$ 1.27 |

$ 1.27 |

$ 1.24 |

$ 3.87 |

$ 3.69 |

|||||||

|

Consolidated Balance Sheets |

||||||||||

|

9/30/24 |

6/30/24 |

3/31/24 |

12/31/23 |

9/30/23 |

||||||

|

Assets |

||||||||||

|

Investments in real estate |

$ 32,951,777 |

$ 32,673,839 |

$ 32,323,138 |

$ 31,633,511 |

$ 31,712,731 |

|||||

|

Investments in unconsolidated real estate joint ventures |

40,170 |

40,535 |

40,636 |

37,780 |

37,695 |

|||||

|

Cash and cash equivalents |

562,606 |

561,021 |

722,176 |

618,190 |

532,390 |

|||||

|

Restricted cash |

17,031 |

4,832 |

9,519 |

42,581 |

35,321 |

|||||

|

Tenant receivables |

6,980 |

6,822 |

7,469 |

8,211 |

6,897 |

|||||

|

Deferred rent |

1,216,176 |

1,190,336 |

1,138,936 |

1,050,319 |

1,012,666 |

|||||

|

Deferred leasing costs |

516,872 |

519,629 |

520,616 |

509,398 |

512,216 |

|||||

|

Investments |

1,519,327 |

1,494,348 |

1,511,588 |

1,449,518 |

1,431,766 |

|||||

|

Other assets |

1,657,189 |

1,356,503 |

1,424,968 |

1,421,894 |

1,501,611 |

|||||

|

Total assets |

$ 38,488,128 |

$ 37,847,865 |

$ 37,699,046 |

$ 36,771,402 |

$ 36,783,293 |

|||||

|

Liabilities, Noncontrolling Interests, and Equity |

||||||||||

|

Secured notes payable |

$ 145,000 |

$ 134,942 |

$ 130,050 |

$ 119,662 |

$ 109,110 |

|||||

|

Unsecured senior notes payable |

12,092,012 |

12,089,561 |

12,087,113 |

11,096,028 |

11,093,725 |

|||||

|

Unsecured senior line of credit and commercial paper |

454,589 |

199,552 |

— |

99,952 |

— |

|||||

|

Accounts payable, accrued expenses, and other liabilities |

2,865,886 |

2,529,535 |

2,503,831 |

2,610,943 |

2,653,126 |

|||||

|

Dividends payable |

227,191 |

227,408 |

222,134 |

221,824 |

214,450 |

|||||

|

Total liabilities |

15,784,678 |

15,180,998 |

14,943,128 |

14,148,409 |

14,070,411 |

|||||

|

Commitments and contingencies |

||||||||||

|

Redeemable noncontrolling interests |

16,510 |

16,440 |

16,620 |

16,480 |

51,658 |

|||||

|

Alexandria Real Estate Equities, Inc.’s stockholders’ equity: |

||||||||||

|

Common stock |

1,722 |

1,720 |

1,720 |

1,719 |

1,710 |

|||||

|

Additional paid-in capital |

18,238,438 |

18,284,611 |

18,434,690 |

18,485,352 |

18,651,185 |

|||||

|

Accumulated other comprehensive loss |

(22,529) |

(27,710) |

(23,815) |

(15,896) |

(24,984) |

|||||

|

Alexandria Real Estate Equities, Inc.’s stockholders’ equity |

18,217,631 |

18,258,621 |

18,412,595 |

18,471,175 |

18,627,911 |

|||||

|

Noncontrolling interests |

4,469,309 |

4,391,806 |

4,326,703 |

4,135,338 |

4,033,313 |

|||||

|

Total equity |

22,686,940 |

22,650,427 |

22,739,298 |

22,606,513 |

22,661,224 |

|||||

|

Total liabilities, noncontrolling interests, and equity |

$ 38,488,128 |

$ 37,847,865 |

$ 37,699,046 |

$ 36,771,402 |

$ 36,783,293 |

|||||

|

Funds From Operations and Funds From Operations per Share |

|

The following table presents a reconciliation of net income (loss) attributable to Alexandria’s common stockholders, the most directly comparable financial measure presented in |

|

Three Months Ended |

Nine Months Ended |

|||||||||||||

|

9/30/24 |

6/30/24 |

3/31/24 |

12/31/23 |

9/30/23 |

9/30/24 |

9/30/23 |

||||||||

|

Net income (loss) attributable to Alexandria’s common stockholders – basic |

$ 164,674 |

$ 42,917 |

$ 166,886 |

$ (91,927) |

$ 21,855 |

$ 374,477 |

$ 184,371 |

|||||||

|

Depreciation and amortization of real estate assets |

291,258 |

288,118 |

284,950 |

281,939 |

266,440 |

864,326 |

798,590 |

|||||||

|

Noncontrolling share of depreciation and amortization from consolidated real |

(32,457) |

(31,364) |

(30,904) |

(30,137) |

(28,814) |

(94,725) |

(85,212) |

|||||||

|

Our share of depreciation and amortization from unconsolidated real estate JVs |

1,075 |

1,068 |

1,034 |

965 |

910 |

3,177 |

2,624 |

|||||||

|

Gain on sales of real estate |

(27,114) |

— |

(392) |

(62,227) |

— |

(27,506) |

(214,810) |

|||||||

|

Impairment of real estate – rental properties and land |

5,741 |

(1) |

2,182 |

— |

263,982 |

19,844 |

7,923 |

186,446 |

||||||

|

Allocation to unvested restricted stock awards |

(2,908) |

(1,305) |

(3,469) |

(2,268) |

(838) |

(7,657) |

(3,050) |

|||||||

|

Funds from operations attributable to Alexandria’s common stockholders – |

400,269 |

301,616 |

418,105 |

360,327 |

279,397 |

1,120,015 |

868,959 |

|||||||

|

Unrealized (gains) losses on non-real estate investments |

(2,610) |

64,238 |

(29,158) |

(19,479) |

77,202 |

32,470 |

220,954 |

|||||||

|

Impairment of non-real estate investments |

10,338 |

(3) |

12,788 |

14,698 |

23,094 |

28,503 |

37,824 |

51,456 |

||||||

|

Impairment of real estate |

— |

28,581 |

— |

7,908 |

805 |

28,581 |

2,778 |

|||||||

|

Acceleration of stock compensation expense due to executive officer resignations |

— |

— |

— |

18,436 |

1,859 |

— |

1,859 |

|||||||

|

Allocation to unvested restricted stock awards |

(125) |

(1,738) |

247 |

(472) |

(1,330) |

(1,640) |

(3,503) |

|||||||

|

Funds from operations attributable to Alexandria’s common stockholders – |

$ 407,872 |

$ 405,485 |

$ 403,892 |

$ 389,814 |

$ 386,436 |

$ 1,217,250 |

$ 1,142,503 |

|||||||

|

Refer to “Definitions and reconciliations” in the Supplemental Information for additional details. |

|

|

(1) |

Primarily to reduce the carrying amount of one property in Canada that continued to meet the held-for-sale classification to the sales price under negotiation with a potential buyer less costs to sell. |

|

(2) |

Calculated in accordance with standards established by the Nareit Board of Governors. |

|

(3) |

Primarily related to two non-real estate investments in privately held entities that do not report NAV. |

|

Funds From Operations and Funds From Operations per Share (continued) |

|

The following table presents a reconciliation of net income (loss) per share attributable to Alexandria’s common stockholders, the most directly comparable financial measure presented in |

|

Three Months Ended |

Nine Months Ended |

|||||||||||||

|

9/30/24 |

6/30/24 |

3/31/24 |

12/31/23 |

9/30/23 |

9/30/24 |

9/30/23 |

||||||||

|

Net income (loss) per share attributable to Alexandria’s common stockholders – |

$ 0.96 |

$ 0.25 |

$ 0.97 |

$ (0.54) |

$ 0.13 |

$ 2.18 |

$ 1.08 |

|||||||

|

Depreciation and amortization of real estate assets |

1.51 |

1.50 |

1.48 |

1.48 |

1.40 |

4.49 |

4.19 |

|||||||

|

Gain on sales of real estate |

(0.16) |

— |

— |

(0.36) |

— |

(0.16) |

(1.26) |

|||||||

|

Impairment of real estate – rental properties and land |

0.03 |

0.01 |

— |

1.54 |

0.12 |

0.05 |

1.09 |

|||||||

|

Allocation to unvested restricted stock awards |

(0.01) |

(0.01) |

(0.02) |

(0.01) |

(0.01) |

(0.05) |

(0.01) |

|||||||

|

Funds from operations per share attributable to Alexandria’s common |

2.33 |

1.75 |

2.43 |

2.11 |

1.64 |

6.51 |

5.09 |

|||||||

|

Unrealized (gains) losses on non-real estate investments |

(0.02) |

0.37 |

(0.17) |

(0.11) |

0.45 |

0.19 |

1.29 |

|||||||

|

Impairment of non-real estate investments |

0.06 |

0.08 |

0.09 |

0.13 |

0.17 |

0.22 |

0.30 |

|||||||

|

Impairment of real estate |

— |

0.17 |

— |

0.05 |

— |

0.17 |

0.02 |

|||||||

|

Acceleration of stock compensation expense due to executive officer resignations |

— |

— |

— |

0.11 |

0.01 |

— |

0.01 |

|||||||

|

Allocation to unvested restricted stock awards |

— |

(0.01) |

— |

(0.01) |

(0.01) |

(0.01) |

(0.02) |

|||||||

|

Funds from operations per share attributable to Alexandria’s common |

$ 2.37 |

$ 2.36 |

$ 2.35 |

$ 2.28 |

$ 2.26 |

$ 7.08 |

$ 6.69 |

|||||||

|

Weighted-average shares of common stock outstanding – diluted |

172,058 |

172,013 |

171,949 |

171,096 |

170,890 |

172,007 |

170,846 |

|||||||

|

Refer to “Definitions and reconciliations” in the Supplemental Information for additional details. |

||||||||||||||

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/alexandria-real-estate-equities-inc-reports-3q24-and-ytd-3q24-net-income-per-share–diluted-of-0-96-and-2-18–respectively-and-3q24-and-ytd-3q24-ffo-per-share–diluted-as-adjusted-of-2-37-and-7-08–respectively-302282138.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/alexandria-real-estate-equities-inc-reports-3q24-and-ytd-3q24-net-income-per-share–diluted-of-0-96-and-2-18–respectively-and-3q24-and-ytd-3q24-ffo-per-share–diluted-as-adjusted-of-2-37-and-7-08–respectively-302282138.html

SOURCE Alexandria Real Estate Equities, Inc.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.