Cryogenic Ethylene Market Share Expand at a CAGR of 9.2%, Reaching US$ 13,760.3 Million by 2034 | Fact.MR Report

Rockville, MD , Oct. 21, 2024 (GLOBE NEWSWIRE) — According to Fact.MR, a market research and competitive intelligence provider, the Global Cryogenic Ethylene Market is estimated to reach a valuation of US$ 5,706.9 million in 2024 and is expected to grow at a CAGR of 9.2% during the forecast period of (2024 to 2034).

The cryogenic ethylene market is a dynamic and ever-evolving industry that is driven by several causes. First and foremost, the driving force affects to the increase in demand for polyethylene. It is a multi-application plastic used across packaging, building, and construction, and consumer goods. Technological advancement has also been a key determinant in the market.

Innovations in cryogenic storage and transportation have so far enabled ethylene to be efficiently and safely handled, thus making it more accessible to industries worldwide. More stress is being laid on research and development, too, in finding new applications for cryogenic ethylene in the manufacture of speciality chemicals and materials.

As would be expected from the established chemical companies and special gases suppliers, the competitive landscape of cryogenic ethylene is shared between just a few big names. Competition among the companies exists concerning product quality, pricing, distribution networks, and many other aspects. There is even variation within products on the basis of their capabilities to deliver supplies of cryogenic ethylene credibly and regularly.

For More Insights into the Market, Request a Sample of this Report: https://www.factmr.com/connectus/sample?flag=S&rep_id=7232

.png")

Key Takeaways from Market Study:

- The global Cryogenic Ethylene market is projected to grow at 2% CAGR and reach US$ 13,760.3 million by 2034

- The market created an opportunity of US$ 8,053.4 million between 2024 to 2034

- North America is a prominent region that is estimated to hold a market share of 5 % in 2024

- Polymer production under application segment is estimated to grow at a CAGR of 2% creating an absolute $ opportunity of US$ 8,053.4 million between 2024 and 2034

- North America and East Asia are expected to create an absolute $ opportunity of US$ 4,633.0 million collectively

“The cryogenic ethylene market is poised for continued growth, driven by increasing demand for polyethylene, advancements in cryogenic technology, and expanding industrial applications. However, challenges such as volatility in raw material prices and regulatory pressures could impact market dynamics.” says a Fact.MR analyst.

Leading Players Driving Innovation in the Cryogenic Ethylene Market:

Air Liquide ; Borealis; Chevron Philips; DOW; Eastman; Exxon Mobil; Indorama; Lotte; LyondellBasell; BASF; Reliance Industries Limited; Shell Global; SABIC; INEOS Group AG; Other Prominent Players.

Market Development:

Recent innovations include, LanzaTech partnered with Danone to concentrate on monoethylene glycol-a main feedstock for polyethylene terephthalate applied to resins, fibers, and bottles in May 2022.

In March 2024, New Energy Blue reached another critical milestone in its Decarbonizing America initiative by forming New Energy Chemicals, a game-changing biochemical subsidiary. The subsidiary will focus on producing, during this first phase of the project, bio-based ethylene that is sourced and manufactured in the US.

In Dec 2023, EFC Gases & Advanced Materials introduced an innovative neon gas cycling system designed to provide consistent and stable pricing for neon to end users over the long term.

Cryogenic Ethylene Industry News:

- In December 2021, Butler Gas received formal recognition as the designated industrial gas supplier for the Pittsburgh Penguins. This partnership involves Butler Gas supplying propane for the Zambonis and industrial forklifts used at the Penguins’ facilities, namely PPG Arena and UPMC Lemieux.

- In May 2022, LanzaTech partnered with Danone to concentrate on monoethylene glycol-a main feedstock for polyethylene terephthalate applied to resins, fibers, and bottles.

Get Customization on this Report for Specific Research Solutions: https://www.factmr.com/connectus/sample?flag=S&rep_id=7232

More Valuable Insights on Offer:

Fact.MR, in its new offering, presents an unbiased analysis of the global Cryogenic Ethylene market, presenting historical data for 2019 to 2023 and forecast statistics for 2024 to 2034.

The study reveals essential insights based on Grade (Polymer Grade, Chemical Grade), Application (Chemical Production, Polymer Production, Alkylation and Refining, Solvent and Specialty Chemicals, Automotive, Construction, Medical and Pharmaceuticals, Textile and Fiber Production), Transport Mode (Tank Cars (Rail Cars), Cargo Tanks (Tank Trucks), ISO Containers, High-Pressure Cylinders), across major regions of the world (North America, Latin America, Western Europe, Eastern Europe, East Asia, South Asia, and Pacific, Middle East & Africa).

Segmentation of Cryogenic Ethylene Industry Research:

- By Grade :

- Polymer Grade

- Chemical Grade

- By Application :

- Chemical Production

- Ethylene Oxide (EO)

- Ethylene Glycol (EG)

- Ethylene Benzene (EB)

- Polymer Production

- Polyethylene (PE)

- Low-Density Polyethylene (LDPE)

- High-Density Polyethylene (HDPE)

- Linear Low-Density Polyethylene (LLDPE)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Polyethylene (PE)

- Solvent and Specialty Chemicals

- Agricultural Intermediates

- Polyethylene Wax

- Refrigerant

- LNG Liquifaction

- Coolant Systems

- Other Applications

- Chemical Production

- By Transport Mode :

- Tank Cars (Rail Cars)

- Cargo Tanks (Tank Trucks)

- ISO Containers

- High-Pressure Cylinders

Checkout More Related Studies Published by Fact.MR Research:

The global high purity boron market is valued at US$ 1.21 billion in 2024 and is forecasted to expand at a CAGR of 8.5% to reach US$ 2.72 billion by the end of the assessment period in 2034.

The global EVA foam market is approximated to touch a valuation of US$ 18.99 billion in 2024. The market has been forecasted to increase at 5.4% CAGR to achieve a value of US$ 32.2 billion by the end of 2034.

Revenue from the global seismic rubber bearing and isolator market is estimated to reach US$ 461.91 million in 2024. The market is analyzed to rise at a CAGR of 3.2% to reach US$ 630.69 million by the end of 2034.

The global electroplating chemicals market is currently valued at around US$ 49.23 billion in 2024 and is forecasted to expand at a CAGR of 6.8% to reach US$ 94.69 billion by 2034.

The global container glass coating market is estimated to reach a valuation of US$ 3.91 billion in 2024 and further expand at a CAGR of 5.6% to end up at US$ 6.77 billion by the year 2034.

About Us:

Fact.MR is a distinguished market research company renowned for its comprehensive market reports and invaluable business insights. As a prominent player in business intelligence, we deliver deep analysis, uncovering market trends, growth paths, and competitive landscapes. Renowned for its commitment to accuracy and reliability, we empower businesses with crucial data and strategic recommendations, facilitating informed decision-making and enhancing market positioning.

With its unwavering dedication to providing reliable market intelligence, FACT.MR continues to assist companies in navigating dynamic market challenges with confidence and achieving long-term success. With a global presence and a team of experienced analysts, FACT.MR ensures its clients receive actionable insights to capitalize on emerging opportunities and stay ahead in the competitive landscape.

Contact:

US Sales Office:

11140 Rockville Pike

Suite 400

Rockville, MD 20852

United States

Tel: +1 (628) 251-1583

Sales Team: sales@factmr.com

Follow Us: LinkedIn | Twitter | Blog

![]()

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Nearly Half of Americans Are Absolutely Wrong About This All-Important Social Security Rule

Social Security is the foundation for many Americans’ retirement plans. However, not everyone knows all of the details of how the government program works. There are a few foundational rules everyone should know, but many Americans’ knowledge falls short for even the most basic and important rules governing the program.

If you don’t know the basics of how Social Security works, making an informed decision about when to claim your retirement benefits becomes impossible. Applying for benefits too early (or too late) can have serious long-term ramifications on your retirement goals. Unfortunately, almost half of Americans maintain an incorrect belief about how claiming benefits early will impact their monthly benefit, according to a recent survey from Nationwide.

A costly mistaken belief

In the survey, 48% of Americans incorrectly identified the following statement as true: “If I claim benefits early, my benefits will go up automatically when reaching full retirement age.”

Most readers will reach full retirement age at 67 despite becoming eligible to claim Social Security benefits at age 62. But there’s no free lunch when it comes to these benefits. The truth is claiming your benefits before you reach full retirement age will permanently reduce your monthly benefit.

The following table shows just how much less you can expect to receive relative to your full retirement age if you claim early.

Claiming Age% of Full Benefit6270%6375%6480%6586.7%6693.3%67100%

For Americans with a full retirement age of 67 (born in 1960 or later).

Table source: Author. Data source: Social Security Administration.

Why is this misunderstanding so prevalent?

There’s a reason why many people may maintain the mistaken belief that you’ll see a bump in benefits upon reaching full retirement age. That’s because sometimes you actually do. But that’s only due to another commonly misunderstood rule: the Social Security earnings test.

The Social Security earnings test says if you earn over a certain amount while collecting retirement benefits before your full retirement age, the Social Security Administration will withhold some of your monthly benefits. The amount withheld is factored back into your monthly benefit once you reach full retirement age. At that point, the earnings test no longer applies, and the SSA no longer withholds any of your benefit.

In this context, the ultimate size of your check is primarily determined by the age at which you initially apply for Social Security. If you never exceed the earnings test threshold in a given year, you’ll never see a change in the amount you collect besides the annual COLA.

Many Americans are unaware of how the Social Security earnings test works as well. Just 56% of survey respondents correctly answered a question about it in Nationwide’s survey.

The earnings test is the exception to the rule, not the rule itself. It’s important to make that distinction to avoid confusion when making a decision about when to claim benefits.

It pays to delay

All things being equal, it’s typically beneficial to wait to claim your benefits, possibly even beyond your full retirement age.

If you opt to wait to claim your benefits, the Social Security Administration will increase your monthly benefit by 2/3 of a percentage point for each month you delay beyond full retirement age. Those delayed retirement credits max out at age 70, which means someone with a full retirement age of 67 can receive a 24% boost to their monthly checks.

A 2019 study from United Income found the majority of seniors (57%) would be better off by waiting until age 70 to claim their retirement benefits. Just 8% would benefit from claiming before age 65.

There are plenty of good reasons to claim early, though.

For one, if the quality of your life with the supplemental income is significantly higher than without, then it probably makes sense to claim it when you need it. There are steps you can take later if your situation improves to mitigate the impact of claiming early.

Another situation is when you have a reasonable expectation that you’ll pass away earlier than your peers. Social Security is designed to pay out roughly the same amount in lifetime benefits for someone living an average life expectancy regardless of when they claim. But if you suffer from a condition that curbs your life expectancy, it might make sense to claim your benefits earlier.

No matter when you decide to claim, be sure you do it with a complete understanding of how your claiming age impacts your monthly benefit and whether or not you should actually expect your benefit to increase in the future.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

View the “Social Security secrets” »

The Motley Fool has a disclosure policy.

Nearly Half of Americans Are Absolutely Wrong About This All-Important Social Security Rule was originally published by The Motley Fool

The Rise of Metaverse Market: A $1,303.4 billion Industry Dominated by Microsoft, Sony, Meta, HTC | MarketsandMarkets™

Delray Beach, FL, Oct. 21, 2024 (GLOBE NEWSWIRE) — The global Metaverse Market size is expected to grow from USD 83.9 Billion in 2023 to USD 1,303.4 Billion by 2030 at a CAGR of 48.0% during the forecast period, according to new research report by MarketsandMarkets™

Browse in-depth TOC on “Metaverse Market”

291 – Tables

67 – Figures

359 – Pages

Download Report Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=166893905

Metaverse Market Dynamics:

Drivers

- Increase in demand from entertainment and gaming industries

- Emerging opportunities from adjacent markets

- Virtualization in fashion, art, and retail industries

Restraints

- High installation and maintenance costs of high-end metaverse components

- Regulations pertaining to cybersecurity, privacy, and usage standards

Opportunities

- Incorporation of metaverse and adjacent technologies in aerospace & defense sector

- Continuous developments in 5G technology

- Emergence of virtual experiences in corporate and hospitality sectors

List of Key Players in Metaverse Market:

- Microsoft (US)

- Sony (Japan)

- Meta (US)

- HTC (Taiwan)

- Google (US)

- Apple (US)

- Qualcomm (US)

- Samsung (South Korea)

- Activision Blizzard (US)

- NetEase (China)

- Electronic Arts (US)

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=166893905

Metaverse is an online experience of shared 3D virtual worlds created by combining physical and digital worlds. These virtual worlds are created by leveraging AR, VR, real-time 3D, and interactive video. The Metaverse has gained wide popularity in social networking, online video gaming, and live entertainment. With investments towering up for real-time 3D technology development, the market players from the social media industry, online gaming market space, and other technology fields are already foreseeing a vast potential in the metaverse market. Online game makers, such as Activision Blizzard (US), Electronic Arts (US), Microsoft (US), NetEase (China), Nexon (Japan), Roblox (US), Take-Two (US), and Tencent (China), support the metaverse market growth through the in-game 3D virtual worlds. The opportunities in adjacent markets, such as VR, AR, extended reality, cloud gaming, AI in social media, and AR/VR hardware and peripherals, open new revenue prospects for the metaverse market.

The software segment holds the largest market size during the forecast period. The software includes gaming engines, 3D modeling & reconstruction tools, volumetric video tools, geospatial mapping software, metaverse platforms, and financial platforms. A game engine is a software framework or platform that developers use to create and develop video games. It provides a set of tools, libraries, and systems for various aspects of game development, such as rendering graphics, handling physics, managing game assets, and implementing gameplay logic. Game engines help streamline the game development process and enable developers to focus on creating the actual content and gameplay rather than building the underlying technology from scratch.

Game engines play a significant role in the development of the metaverse, which is a virtual, interconnected, and immersive digital universe where users can interact, socialize, work, and play. The few usage of game engine in metaverse are, creating virtual worlds, increasing user interaction, avatar creation and animation, multiplayer networking and many more. In 2023, the software segment held the highest share in the metaverse market during the forecast period as it helps to o create and design the virtual worlds and environments within the metaverse. This includes 3D modeling software, world-building tools, and terrain generation software, it enable users to navigate, interact, and control their experience within the metaverse. This includes menus, HUDs (Heads-Up Displays), and gesture recognition interfaces, it helps to implement networking protocols and multiplayer functionality to enable users to interact with each other in real-time within the metaverse. This would support market growth in the coming years.

Inquire Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=166893905

The geographic analysis of the metaverse market includes five regions: North America, Asia Pacific, Europe, Middle East & Africa, and Latin America. As a technology adopter, North America holds the largest market size during the forecast period. Being technologically advanced and developed, North America is the leading market in developing cutting-edge display technology. Further, the rising expenditure of companies and individuals on digital solutions and advanced technologies also boosts market growth. North America has emerged as the largest market for metaverse technology. It accounted for a significant share of the global market in 2023. The use of AR technology in consumer electronics propels the growth of the AR market in the region. Industries such as aerospace and defense, healthcare, consumer, and commercial applications for education and training also use AR. Several global companies providing AR devices and solutions have their presence in the US, including Microsoft, Apple, Meta, and Google. Additionally, enterprises’ increased acceptance of metaverse technologies to market their products in a modern way has been the key factor driving the growth of the metaverse market in North America.

VR and AR technologies are crucial for creating immersive metaverse experiences. VR provides fully immersive digital environments, while AR overlays digital content onto the real world, blending the physical and digital realms. Advances in hardware have made VR and AR more accessible and compelling; this includes better headsets, more powerful GPUs, and more affordable components, making the technology available to a broader range of consumers and industries. The availability of engaging content boosts AR and VR growth. As more developers and creators produce high-quality VR and AR experiences, it encourages user adoption. This content spans from games and entertainment to educational and professional applications. The gaming industry has been a significant driver for VR adoption. Games like “Beat Saber,” “Half-Life: Alyx,” and “Superhot VR” have demonstrated the potential for immersive gaming experiences.

Additionally, businesses use AR for interactive marketing campaigns and location-based entertainment, like the success of Pokémon GO. MR is finding significant traction in the enterprise and industrial sectors. Businesses are adopting MR for remote assistance, training, maintenance and repair, 3D modeling, and data visualization; MR helps improve efficiency, reduce errors, and enhance collaboration in these industries.

Get access to the latest updates on Metaverse Companies and Metaverse Industry

About MarketsandMarkets™ MarketsandMarkets™ has been recognized as one of America's best management consulting firms by Forbes, as per their recent report. MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients. Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes. The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing. Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry. To find out more, visit www.MarketsandMarkets™.com or follow us on Twitter, LinkedIn and Facebook. Contact: Mr. Rohan Salgarkar MarketsandMarkets Inc. 1615 South Congress Ave. Suite 103, Delray Beach, FL 33445 USA : 1-888-600-6441 UK +44-800-368-9399 Email: sales@marketsandmarkets.com Visit Our Website: https://www.marketsandmarkets.com/

![]()

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Is It Wise to Convert 15% of My 401(k) Into a Roth IRA Each Year to Avoid Taxes and RMDs?

SmartAsset and Yahoo Finance LLC may earn commission or revenue through links in the content below.

Converting retirement funds from a 401(k) into a Roth IRA offers the opportunity for tax-free growth and tax-free withdrawals in retirement, while also avoiding Required Minimum Distribution (RMD) rules. However, Roth conversion requires paying a significant tax bill up front. Often, this initial tax bill can be partially mitigated by gradually converting the 401(k) over time to keep yourself in lower tax brackets. However, the dynamics of a shifting portfolio and income over time, as well as a five-year withdrawal limitation on conversions, may make a Roth conversion inappropriate in some circumstances. When a Roth conversion does look like a winner, converting a fixed percentage each year may or may not be the best approach either. Before embarking on a Roth conversion plan, consider talking it over with a financial advisor to determine if it makes sense for you.

Roth Conversion Strategies

Retirement funds in a 401(k) account are subject to federal income tax when withdrawn, and oftentimes state and local taxes, too. And because of RMD rules, savers with funds in tax-deferred retirement accounts such as 401(k) plans must begin withdrawing from the accounts once they reach age 73. That can create a tax burden for some retirees.

Those disadvantages prompt many retirement savers to consider Roth conversions, which roll over funds from 401(k) accounts to Roth IRAs. Once in the Roth account, investment earnings and qualified withdrawals are both tax-free. Roth accounts are also not subject to RMD rules, which gives retirees better control over their retirement funds.

However, the upfront tax bill for a Roth conversion can be steep. Converted funds are taxed as ordinary income, so converting a sizable 401(k) into a Roth IRA can put even a middle-income earner temporarily into the top 37% federal tax bracket and result in an enormous tax bill. For example, consider a single $100,000 earner in the 22% tax bracket for 2024 who ordinarily pays about $14,000 in federal income tax. If in one year they convert a $500,000 401(k) to a Roth IRA, the one-time tax bill would be an estimated $177,000, an increase of about $163,000.

Gradual conversions can help manage the tax consequences. The single $100,000 earner could convert up to $91,950 in a year and move up to the 24% bracket, incurring a one-time tax bill of approximately $36,000, adding about $22,000 to their tax bill that year. If it takes seven years of this to empty the account, accounting for average investing returns on the unconverted balance in the interim, the total cumulative federal tax bill would add up to approximately $153,000, a savings of about $10,000 compared to making the conversion all at once. Additionally, the amount of money converted to the Roth IRA would be higher than it would have been if converting all at once, thanks to theoretical portfolio growth during the staggered conversion period.

As was done in this example, conversion strategies often get better results when based on dollar amounts and the effect on tax brackets rather than percentages of the 401(k) balance. In addition, conversion plans often incorporate flexibility, which allows savers to convert larger amounts, for instance, in years when their income is lower. In any case, conversion strategies are best tailored to individual savers’ unique circumstances. Consider matching with a financial advisor to discuss your strategy.

Roth Conversion Limitations

Roth conversions aren’t always the best move. For example, they hold less attraction for retirees who will be in a lower tax bracket after retirement. These retirees’ overall tax bills may be lower if they leave money in a 401(k) and pay taxes on withdrawals in retirement.

The conversion math also may not add up for savers who are near retirement and will need Roth funds to pay retirement expenses. That’s because converted funds can’t be withdrawn tax-free for five years after conversion. A financial advisor can help you weigh the pros and cons of doing Roth conversions based on your personal goals and circumstances.

Finally, Roth conversions may make less sense for someone who plans to donate or leave money to charity. That’s because charitable gifts and bequests from a 401(k) can escape taxation, removing one of the lures of conversion

Bottom Line

Convert 15% of a 401(k) in a Roth IRA each year could be an effective way to manage taxes and avoid RMDs. However, much depends on individual circumstances and that strategy may not be the most efficient for many savers. Well-designed conversion strategies focus on dollar amounts and income tax brackets more than strict percentages. And Roth conversions may not make financial sense for people who are close to retirement, expect to be in lower tax brackets after retirement or plan to leave sizable legacies to charitable organizations from their 401(k) plans.

Tips

-

Before starting to convert funds from a 401(k) to a Roth, talk the plan over with a financial advisor who can help you construct what-if scenarios and models to examine the likely outcomes of various approaches. Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three financial advisors in your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

-

SmartAsset’s RMD Calculator allows you to quickly and easily project the size of future mandatory withdrawals from tax-deferred retirement accounts.

-

Keep an emergency fund on hand in case you run into unexpected expenses. An emergency fund should be liquid — in an account that isn’t at risk of significant fluctuation like the stock market. The tradeoff is that the value of liquid cash can be eroded by inflation. But a high-interest account allows you to earn compound interest. Compare savings accounts from these banks.

-

Are you a financial advisor looking to grow your business? SmartAsset AMP helps advisors connect with leads and offers marketing automation solutions so you can spend more time making conversions. Learn more about SmartAsset AMP.

Photo credit: ©iStock.com/Dragos Condrea, ©iStock.com/busracavus

The post Is It Wise to Convert 15% of My 401(k) Into a Roth IRA Each Year to Avoid Taxes and RMDs? appeared first on SmartReads by SmartAsset.

Live Oak Ventures Participates in Financing of Synply, Inc.

WILMINGTON, N.C., Oct. 21, 2024 (GLOBE NEWSWIRE) — Live Oak Ventures, the investment arm of Live Oak Bancshares, Inc., has announced an investment in Synply Inc., a cloud-based technology company dedicated to transforming the loan syndication process for banks.

“Live Oak’s entrepreneurial environment is fertile ground for new and exciting companies like Synply to enter the fintech landscape,” said Stephanie Mann, Live Oak Bank Chief Strategy Officer. “After incubating the Synply platform at Live Oak, we are excited to see the company level the playing field for all banks to compete in the syndicated loan space.”

Synply offers banks a simplified tool to centralize the entire process of syndicated lending and portfolio management.

“We built Synply because we saw a critical need for a modern and intuitive platform specifically designed for the loan syndication process,” said Corbin Penland, CEO of Synply and former managing director of loan syndications at Live Oak Bank. “Our team of experienced bankers understands the pain points associated with current tools and workflows. Synply empowers banks to focus on building relationships and growing their business, not managing cumbersome processes.”

The Synply platform offers end-to-end efficiency by allowing all banks participating in a loan to manage the entire loan syndication process, from origination to servicing, all within one platform.

About Live Oak Ventures

Live Oak Ventures, a wholly owned subsidiary of Live Oak Bancshares LOB, is a fintech-focused investor that aims to bring innovation and performance excellence to the forefront of the banking industry. By investing in companies that accelerate the delivery of open digital solutions to the market, Live Oak Ventures intends to change the landscape of financial services and small business banking.

About Synply

Synply is a cloud-based technology company dedicated to transforming the loan syndication process for banks. Developed by experienced bankers and incubated within Live Oak Bank, a leading industry player, Synply offers a comprehensive and user-friendly platform that empowers banks to easily navigate the complexities of loan syndication.

Contact:

Claire Parker

Live Oak Bank, SVP Corporate Communications

910.597.1592

claire.parker@liveoak.bank

![]()

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Billionaire Israel Englander Sold 59% of Millennium's Stake in Palantir and Has Opted to Pile Into a Stock Consumers Absolutely Adore

Last week, Wall Street kicked off earnings season. This marks a roughly six-week stretch where most S&P 500 companies will lift their proverbial hoods and report their quarterly operating results from the most recent quarter. While these reports help to paint a picture regarding the health of the U.S. economy and stocks, in general, there’s another group of data releases that are, arguably, even more important.

Every quarter, institutional investors with at least $100 million in assets under management (AUM) are required to file Form 13F with the Securities and Exchange Commission. A 13F allows investors an over-the-shoulder look to see what Wall Street’s smartest money managers bought and sold in the latest quarter. August 14 marked the filing deadline for second-quarter trading activity, and is potentially the most important data release in recent months.

While Berkshire Hathaway CEO Warren Buffett is easily the most-watched of all asset managers, other billionaire investors have garnered quite the following. One highly successful billionaire money maanger that professional and everyday investors tend to closely monitor is Israel Englander of Millennium Management.

Englander and his team run a very active hedge fund, with thousands of positions and close to $216 billion in AUM, as of the midpoint of 2024. Among the many trades undertaken by Englander and his crew during the June-ended quarter, the one that stands out most is the decisive selling activity in ultra-popular artificial intelligence (AI) stock Palantir Technologies (NYSE: PLTR).

Englander’s Millennium dumped more than half its stake in Palantir over three months

Palantir has been a continuous holding in Millennium Management’s mammoth portfolio since it became a public company in September 2020. But during the second quarter, Englander oversaw the sale of 7,074,815 shares of Palantir, which reduced Millennium’s stake by 59% to 4,973,308 shares.

As of the second quarter, Palantir’s stock had more than doubled from an extensive base that kept shares more or less pegged between $6 and $10 from May 2022 through April 2023. With Millennium holding its top-20 positions by market value for an average of only 11 quarters (i.e., less than three years), profit-taking is certainly a viable reason for this more than 7-million-share reduction. But it’s probably not the only reason for this aggressive selling.

To be perfectly blunt, Palantir’s valuation has become an eyesore. In one respect, the company absolutely deserves some level of valuation premium given that its services are irreplaceable at scale. These “services” include its AI-driven Gotham platform, which aids mission planning for federal governments, as well as its enterprise-focused Foundry platform that helps businesses streamline their operations by making sense of their data.

Then again, Palantir’s is approaching a forward price-to-earnings (P/E) ratio of almost 100, and tipped the scales at roughly 30 times forward-year sales last week. With the company’s annual sales growth expected to dip to 21% in 2025, maintaining a nearly triple-digit forward P/E ratio probably isn’t sustainable.

Palantir is also contending with a natural growth ceiling for its Gotham platform. Though Gotham is responsible for making Palantir profitable on a recurring basis, and has helped the company land lucrative multiyear contracts from the U.S. government, there are only so many government entities that can use Gotham (e.g., Palantir won’t allow China or Russia to access its services).

With limited potential for expansion from Gotham, Palantir is going to have to rely on Foundry for its long-term growth. Although Foundry’s future is bright, this is still a relatively nascent operating segment for the company.

But while Israel Englander and his team were busy showing more than half of their Palantir shares to the door, they were avid buyers of a company that’s near and dear to the hearts of consumers worldwide.

Englander piles into the world’s most-chosen consumer goods brand

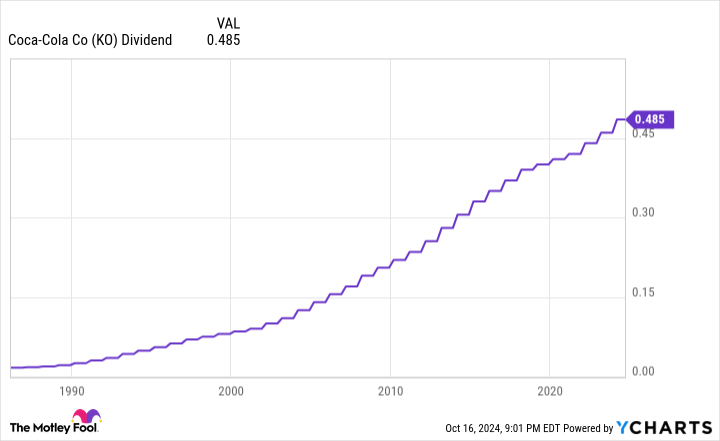

Despite adding to more than 2,100 existing positions in the June-ended quarter, the purchase Englander made for Millennium Management that really stands out is consumer staples goliath Coca-Cola (NYSE: KO).

Millennium’s 13F shows that 5,444,678 shares of Coca-Cola were purchased by the fund’s brightest investment minds, including Englander. This lifted Millennium’s stake in the beverage leader by 347% in a three-month period to 7,009,050 shares.

The beautiful thing about consumer staples stocks is that they perform well in pretty much any economic climate. Coca-Cola sells beverages, which are a basic necessity no matter how well or poorly the U.S. or global economy are performing. The predictability of cash flow consumer staples leaders bring to the table is what makes them such popular investments.

But there’s more to like about Coca-Cola than simply its ability to deliver predictable operating cash flow. For instance, it offers almost unrivaled geographic diversity. It has more than two dozen brands generating at least $1 billion in annual sales, with operations in all but three countries around the globe (North Korea, Cuba, and Russia). This leads to steady cash flow in developed markets and provides needle-moving organic growth in emerging markets.

Coca-Cola is also the world’s top brand among consumers. In May, Kantar released its annual “Brand Footprint” report which, for the 12th consecutive year, was topped by Coca-Cola. Kantar’s report notes that the percentage of households purchasing Coke products grew by 2.6% in 2023 from the prior year, with the brand chosen by consumers close to 8.3 billion times.

Being a highly recognized brand is a reflection of Coca-Cola’s marketing efforts paying off. It has more than a century of history and well-known brand ambassadors to lean on in order to connect with mature consumers. Meanwhile, the company’s marketing team is relying on AI and digital media channels to engage with a younger audience.

Let’s not forget that Coca-Cola has one of the most impressive capital-return programs, too. While the company’s board does, occasionally, authorize share buybacks, it’s the dividend that does the talking. In February, the company’s base annual payout increased for a 62nd consecutive year, which firmly establishes Coca-Cola as a Dividend King. You’ll only need the fingers on two hands to count how many public companies currently have a longer streak of continuous payout increases.

The final piece of the puzzle for Millennium’s investment team was, likely, Coca-Cola’s valuation. Although its forward P/E is currently in-line with its trailing-five-year average, shares were trading at a notable discount to this average during the second quarter.

While Coca-Cola isn’t going to knock investor’s socks off in the growth department, its well-defined competitive advantages and superior dividend continue to deliver for patient shareholders.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,285!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,456!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $411,959!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 14, 2024

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway and Palantir Technologies. The Motley Fool has a disclosure policy.

Billionaire Israel Englander Sold 59% of Millennium’s Stake in Palantir and Has Opted to Pile Into a Stock Consumers Absolutely Adore was originally published by The Motley Fool

2 Ultra-High-Yield Dividend Stocks to Buy Now for a Lifetime of Passive Income

A buoyant stock market that keeps reaching new heights is making it tougher to find high-yield dividend payers. The S&P 500 reached a new all-time high on Oct 18. At recent prices, the average dividend-paying stock in the benchmark index offers an uninspiring 1.3% dividend yield.

The average dividend payer in the S&P 500 index might be unappealing, but there are underappreciated businesses with ultra high dividend yields waiting for income-seeking investors to scoop them up. Ares Capital (NASDAQ: ARCC), and EPR Properties (NYSE: EPR) offer yields above 8% at recent prices.

1. Ares Capital

Ares Capital is the world’s largest publicly traded business development company, or BDC. These specialty financiers fill the gap left by U.S. banks that have been dialing back their direct lending operations for decades. They are also popular with income-seeking investors because they can legally avoid paying income taxes by distributing nearly all their profits to shareholders as dividends.

This BDC’s quarterly dividend payment hasn’t risen in a straight line, but it is up by 26% over the past 10 years. At recent prices, it offers an 8.9% yield and confidence that comes with plenty of diversification.

At the end of June, there were 525 companies in Ares Capital’s portfolio. The company it’s most exposed to is responsible for just 1.8% of the total portfolio. Diversification and an enviable track record earned the BDC an investment-grade credit rating that recently allowed it to sell $850 million worth of five-year notes with a low 5.95% coupon.

The midsize businesses Ares lends to are willing to borrow at higher rates than you might expect. The average yield it received from the debt securities in its portfolio was 12.2% in the second quarter. This is even more encouraging when you consider half of its assets are first-lien senior secured loans, which are first to be repaid if there’s a bankruptcy.

Ares Capital has so much room to grow that buying shares now and never letting go looks like the right move. Its portfolio has swelled to nearly $25 billion but management estimates the current demand for mid-market capital at about $5.4 trillion.

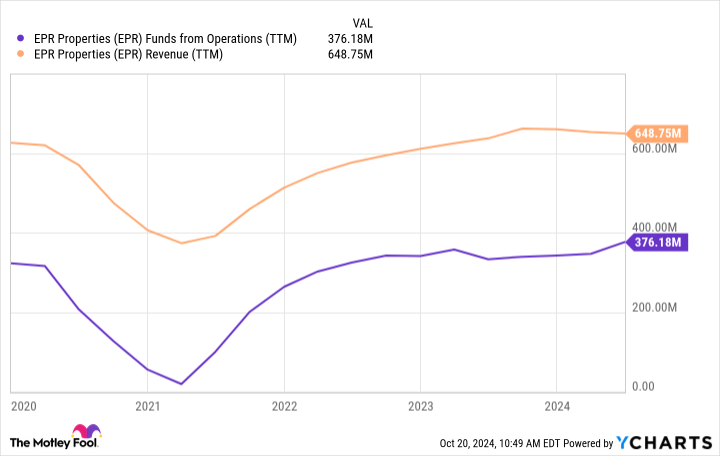

2. EPR Properties

EPR Properties is a real estate investment trust (REIT) that offers a big 9.3% dividend yield at recent prices. The stock has been under pressure because it looks like its recent recovery is losing steam.

This REIT specializes in properties that bring people together in large groups. The stock price has been under pressure because underperforming theaters made up 37% of its total portfolio at the end of June. Investors considering EPR Properties will be glad to know that the theater segment was responsible for just 0.3% of total investment spending during the first six months of 2024.

Increasingly popular eat-and-play facilities like Top Golf make up a large and growing share of EPR’s portfolio. While total revenue has declined slightly, a portfolio leaning further toward non-theater tenants is pushing up profits.

EPR Properties abruptly stopped paying dividends in the spring of 2020 while the COVID-19 pandemic kept us from joining together in large groups. It restarted its monthly dividend program at a reduced level in July 2021.

Since restarting payments in 2021, EPR Properties has raised its dividend by 14% and it’s in a position to raise it a lot further. Funds from operations (FFO) is a proxy for earnings used to evaluate REITs like EPR properties. This year, management expects adjusted FFO to land in a range between $4.76 and $4.96 per share, which is more than enough to support and raise a payout currently set at an annualized $3.42 per share.

The pandemic taught investors that nobody should put too many eggs in EPR’s basket, but its ability to survive the worst of the challenge suggests it can survive all kinds of unforeseen issues. Adding some beaten-down shares to a diverse portfolio now could be a great way to pump up your passive income stream over the long run.

Should you invest $1,000 in Ares Capital right now?

Before you buy stock in Ares Capital, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Ares Capital wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $845,679!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 14, 2024

Cory Renauer has positions in Ares Capital. The Motley Fool recommends EPR Properties. The Motley Fool has a disclosure policy.

2 Ultra-High-Yield Dividend Stocks to Buy Now for a Lifetime of Passive Income was originally published by The Motley Fool

‘God works in mysterious ways’: I became a Nvidia millionaire playing ‘World of Warcraft.’ Am I smart — or just lucky?

Dear Quentin,

In 2010, I was working for a company that was going under, but I didn’t know that. My evil manager was a jerk and manipulated me into quitting by severely and publicly bullying and humiliating me every day. I was too naive at the time to understand this type of manipulation. I decided to quit my job like a boss, but after finding out how I got played, I was devastated. I had no job and no unemployment benefits.

I spent the next year unemployed, at home playing “World of Warcraft.” That’s when I discovered how great Nvidia graphics cards were. One day I got a surprise pension check from the company for over $4,000. I sat on the money for a while, not sure what to do with it. Eventually, I decided to put it all in Nvidia stock. Why not? I thought. It’s just a few thousand dollars, and I like their cards.

Most Read from MarketWatch

It was literally the first stock I ever bought. Those Nvidia stocks are now worth $2 million. Yes, I became a multimillionaire by quitting my job and playing videogames all day. I’m not really religious, but even I have to think, ‘God works in mysterious ways.’ And that’s my funny story about how Nvidia made me a multimillionaire. What do you think? Did I deserve this windfall? Should I feel guilty or smart or did I just get lucky?

Mr. Lucky or Mr. Smart?

Dear Mr. Smart,

In 2010 you were in a funk, and by investing in this stock you were investing in something far more ephemeral — hope.

You saw something others didn’t. There’s a fine line between a stroke of genius and a stroke of luck. And you, my friend, walked it. In 2018, Nvidia made a ride-or-die push to upgrade those graphics cards by revamping the graphics processing units that helped fuel its artificial-intelligence ambitions. Speaking at a conference in Los Angeles last year, Nvidia NVDA CEO Jensen Huang said that he had a “bet-the-company moment.” As TechCrunch reported, Huang said: “It required that we reinvent the hardware, the software, the algorithms and, while we were reinventing CG with AI, we were reinventing the GPU for AI.”

The awesome truth: Your good fortune is due to both your gut instinct and an educated guess as a gamer that this company displayed foresight — and pursued excellence. In 2018, Ryan Shrout, the founder and lead analyst at Shrout Research, wrote on MarketWatch about Nvidia’s next-generation graphics architecture. Despite competition from bigger rivals, Shrout wrote, “Nvidia continues to ship products with leadership performance and penetration. Even Google GOOG GOOGL is using Nvidia graphics chips for its cloud-based AI inference systems, proving that Nvidia is doing while most others are simply trying to.”

Honest retail investors who made successful once-in-a-lifetime bets in the other six members of the “Magnificent Seven” group of stocks — Apple, Microsoft MSFT, Alphabet, Amazon AMZN, Meta META and Tesla TSLA — will tell you what you told me: They bought the stock on a hunch or because they noticed something special about the company’s products or philosophy. Of course, you’re more likely to get lucky with a long-term investment: 14 hours or days may be a long time in politics, but 14 years is a short time for many investors in the stock market.

The upshot: Instinct is a powerful tool — especially when you’re proved right. You’re not the first person to buy a company’s stock because you like one of their products. Have you ever used a BlackBerry BB? I did not find them to be an easy or intuitive device to use, and I never understood their appeal. Mine stayed in the box. It was subsequently upstaged by a new device called the iPhone AAPL. So yes, not liking a company’s products may be one reason to avoid the stock — or vice versa. As obvious as it may seem, it can also be useful to look at a company’s financials and price-earnings ratio before committing your hard-earned cash.

You took a bet on one stock and, while you went against all the rules of diversification, you had perhaps once-in-lifetime luck with the explosion of artificial intelligence. But you also had an inkling that this company was doing something special, even if you did not foresee the exact nature of the stock’s meteoric rise — or that, in the words of DataTrek cofounder Nick Colas, Nvidia would “become, quite literally, the single most important company in the world to global equity investors.”

Financial advisers, for better or for worse, have all sorts of methods for choosing stocks — such as fundamental analysis or technical analysis — but there are no guarantees, even for the most forensic stock picker. And history is littered with bad calls. “Fundamental analysis attempts to identify stocks offering strong growth potential at a good price,” says Charles Schwab SCHW. “Investors have traditionally used fundamental analysis for longer-term trades, relying on metrics like earnings per share (EPS), price-to-earnings (P/E) ratio, P/E growth, and dividend yield.”

Schwab continues: “Technical analysis, on the other hand, bypasses the underlying company’s fundamentals and instead looks for statistical patterns on stock charts that might foretell future price moves. The idea here is that stock prices already reflect all the publicly available information about a particular company, so there’s nothing to be gained from poring over a balance sheet, income statement, or other financial information. Given the focus on price and volume moves, traders have traditionally used technical analysis for shorter-term trades.”

What were your objectives in buying this stock? Long-term growth? Capitalizing on a hot trend? Making a quick buck? Or did you merely want a foothold in the stock market with a $4,000 investment in your future and a shot at something less tangible — something that was in short supply after the traumatic experience with your former manager — a chance at a better future? Buying low is only the beginning: Riding the stock’s volatility, and resisting cashing out as the price slowly climbed before finally exploding. That takes chutzpah, nerves of steel and self-restraint, so give yourself credit for that.

You put your life savings in one stock, a risky move, but it paid off. God works in mysterious ways and, sometimes, so does the S&P 500 SPX.

Related: ‘I’m convinced the U.S. will be drawn into World War III’: How do I prepare my finances?