Quiet Bitcoin Whales, Sitting On A Windfall, Spring Back To Activity — Price Retrace Imminent?

Bitcoin BTC/USD investors were suddenly waking up after years of dormancy to move around their stash as the leading cryptocurrency gathers upward momentum toward all-time highs.

What Happened: On-chain analytics firm Whale Alert reported that a Bitcoin address, dormant for roughly 11 years, transferred 21.87 BTC to another address Sunday overnight.

The stash was worth $16,252 when it last moved in 2013, Whale Alert added. As of this writing, the total value of the holdings was around $1.5 million, indicating a massive 9159% return.

Similarly, a Satoshi-era whale transferred 20 BTCs to another wallet a little earlier in the day, which at the time of the transfer netted 411596% in return.

“Satoshi Era” is a popular term in cryptocurrency parlance, referring to the phase from 2009 to 2011, when Nakamoto was actively working and promoting the project.

Why It Matters: The movement of such old Bitcoins has picked up pace this month. It wasn’t immediately clear whether the transfer was meant to sell and lock in profits.

The movements of Bitcoin whales, especially those from the Satoshi era, are closely watched by the cryptocurrency community. These whales hold a significant amount of Bitcoin, and their transactions can potentially impact the market.

According to blockchain research firm CryptoQuant, whale inflows to exchanges lifted significantly last week, sparling fears of sell-offs.

Bitcoin, the world’s largest cryptocurrency, surged above $69,000 late Sunday evening, the first occurrence since early June. The coin gained over 7% in the last week, with top cryptocurrency analysts projecting a swift return to its all-time highs.

Price Action: At the time of writing, Bitcoin was exchanging hands at 68,773.18, up 0.73% in the last 24 hours, according to data from Benzinga Pro.

Read Next:

Disclaimer: This content was partially produced with the help of Benzinga Neuro and was reviewed and published by Benzinga editors.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Tylenol, Listerine Maker Kenvue Under Activist Spotlight With Starboard Value Stake — Overhaul Ahead For The Johnson & Johnson Spinoff?

Starboard Value, an activist investor, has reportedly acquired a substantial stake in Kenvue Inc KVUE, the company behind popular consumer products like Tylenol and Listerine.

What Happened: Starboard Value is pushing for changes at Kenvue, which was spun off from Johnson & Johnson JNJ last year and has a market value of over $40 billion, reported The Wall Street Journal, citing people familiar with the matter.

Despite having some of the best consumer brands in the industry, Kenvue’s stock has underperformed its peers and the broader market since its debut over a year ago.

The exact size of Starboard’s position in Kenvue and its specific ideas for the company are not known. Starboard’s founder and CEO, Jeff Smith, is expected to present the firm’s thesis on Kenvue at an activist investing conference in New York on Tuesday.

Kenvue’s other brands include Aveeno, Band-Aid, Zyrtec, Neosporin, and Neutrogena. The company, led by CEO Thibaut Mongon, recorded over $15 billion in net sales in 2023.

Kenvue and Starboard Value did not immediately respond to Benzinga‘s request for comment.

Why It Matters: Kenvue’s stock price has remained relatively unchanged this year, in contrast to the S&P 500 index’s 23% increase. The company’s biggest competitors include Haleon, the parent company of Advil, Procter & Gamble, the owner of Pepto-Bismol, and Unilever, the maker of Axe deodorant.

Starboard’s recent investment in Kenvue follows its move to acquire a roughly $1 billion stake in Pfizer Inc., where it is seeking various changes to improve the drugmaker’s performance. This includes the appointment of former Pfizer executives Ian Read and Frank D’Amelio, who have pledged their support for current Pfizer CEO Albert Bourla.

Starboard is known for its active involvement in various sectors, including technology, where it has recently made efforts at companies like Salesforce, Autodesk, and Match Group.

Price Action: Kenvue Inc.’s stock closed at $21.72 on Friday, up 1.26% with a gain of $0.27. Year to date, the stock has risen by 0.70%, according to data from Benzinga Pro.

Read Next:

Image Via Shutterstock

This story was generated using Benzinga Neuro and edited by Kaustubh Bagalkote

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

If You Invested $10,000 In Apple Stock 10 Years Ago, How Much Would You Have Now?

Benzinga and Yahoo Finance LLC may earn commission or revenue on some items through the links below.

Apple Inc. (NASDAQ:AAPL) designs, manufactures, and markets smartphones, personal computers, tablets, wearables, and accessories worldwide. It is the largest company in the world with a market cap of $3.51 trillion.

It is set to report its Q4 2024 earnings on October 31. Wall Street analysts expect the tech giant to post an EPS of $1.60, up from $1.46 in the year-ago period. According to Benzinga Pro, quarterly revenue is expected to reach $94.41 billion up from $89.50 billion in the previous year.

Don’t Miss:

If You Bought Apple Stock 10 Years Ago

The company’s stock traded at approximately $24.69 per share 10 years ago. If you had invested $10,000, you could have bought roughly 405 shares. Currently, shares trade at $231.30, meaning your investment’s value could have surged to $93,682 from stock price appreciation alone. However, Apple also consistently paid dividends during the past 10 years.

Apple’s dividend yield is currently 0.43%. Over the last 10 years, it has paid about $19.13 in dividends per share, which means you could have made $7,748 from dividends alone.

Summing up $93,682 and $7,748, we end up with the final value of your investment, which is $101,430. This is how much you could have made if you had invested $10,000 in Apple stock 10 years ago. This means a total return of 914.3%. In comparison, S&P 500 total return for the same period is 257.58%.

Trending: This billion-dollar fund has invested in the next big real estate boom, here’s how you can join for $10.

This is a paid advertisement. Carefully consider the investment objectives, risks, charges and expenses of the Fundrise Flagship Fund before investing. This and other information can be found in the Fund’s prospectus. Read them carefully before investing.

What Could The Next 20 Years Bring?

Apple has a consensus rating of “Buy” and a price target of $243.34 based on the ratings of 30 analysts. The price target implies more than a 5% potential upside from the current stock price.

On Aug. 1, the company reported its Q3 2024 earnings, posting an EPS of $1.40 compared to the consensus estimate of $1.35 and revenues of $85.80 billion compared to the consensus of $84.531 billion, as reported by Benzinga.

The company set a new sales record for its iPhone during the quarter, coinciding with a broader recovery in the global smartphone market. Overall, the global smartphone market experienced a 5% year-over-year growth in Q3 2024, marking the fourth consecutive quarter of expansion.

Two reasons to jump on Apple stock now and one reason to think twice. Check out this article by Benzinga to learn more.

Given the historical stock price appreciation and expected upside potential, growth-focused investors may find Apple stock attractive. In addition, they can benefit from the company’s modest dividend yield of 0.43% and consistent hikes. Apple has raised its dividend consecutively for the last 12 years.

Wondering if your investments can get you to a $5,000,000 nest egg? Speak to a financial advisor today. SmartAsset’s free tool matches you up with up to three vetted financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you.

Keep Reading:

This article If You Invested $10,000 In Apple Stock 10 Years Ago, How Much Would You Have Now? originally appeared on Benzinga.com

3 Must-Watch Tech Earnings Reports Coming Up

Three major players—Microsoft, IBM, and Amazon—are set to release their quarterly earnings reports, and all eyes will be on these updates to assess their growth, resilience, and ability to drive future trends.

These earnings reports are particularly important as they will reveal how these tech leaders are leveraging advancements in artificial intelligence, expanding cloud computing services, and navigating macroeconomic challenges such as changing consumer habits, monetary policy, and geopolitical uncertainties.

Investors will also be watching closely to see whether these companies can help sustain the rally in the U.S. stock market. Last week, the S&P 500 reached a new all-time high, marking a 23% year-to-date gain, while the Dow Jones closed above the 43,000 mark for the first time, signaling continued optimism about market growth.

According to Bank of America, as earnings season kicked off, 30 companies in the S&P 500 surpassed earnings expectations by an average of 5%, up from 3% at the start of the last quarter. An additional 41 S&P 500 companies reported results last week. However, with the S&P 500 currently trading at around 21.8 times forward earnings—well above its long-term average of 15.7—some analysts caution that stock valuations may be stretched. Any disappointment in these reports could trigger a market correction as investors reassess valuations.

As we look ahead to big tech’s upcoming releases, here’s what to watch for:

1# Will Microsoft’s Azure Unit Miss Expectations Again?

Microsoft delivered stronger-than-expected earnings and revenue for its fiscal fourth quarter, with total revenue rising 15% year-over-year. Net income climbed to $22.04 billion, up from $20.08 billion in the same quarter last year, translating to $2.69 per share.

While these results were solid, investor attention was focused on Azure’s performance, which fell below expectations for the first time since 2022. Azure and other cloud services posted 29% revenue growth, but this missed consensus estimates, sparking concerns about whether Microsoft’s cloud unit is losing momentum in an increasingly competitive market.

Despite the Azure miss, Microsoft’s management remains optimistic about future growth, suggesting potential acceleration in the coming quarters. However, investors remain cautious, as Azure’s performance is now a critical driver of Microsoft’s overall growth, especially as cloud computing continues to gain importance across industries.

As Microsoft prepares to release its fiscal Q1 2025 earnings on Tuesday, Oct. 22, after market close, all eyes will be on Azure once again. Analysts are forecasting a profit of $3.10 per share, with total revenue expected to dip slightly from $64.73 billion to $64.54 billion.

So far this year, Microsoft shares are up 12.75%, hovering around $418.

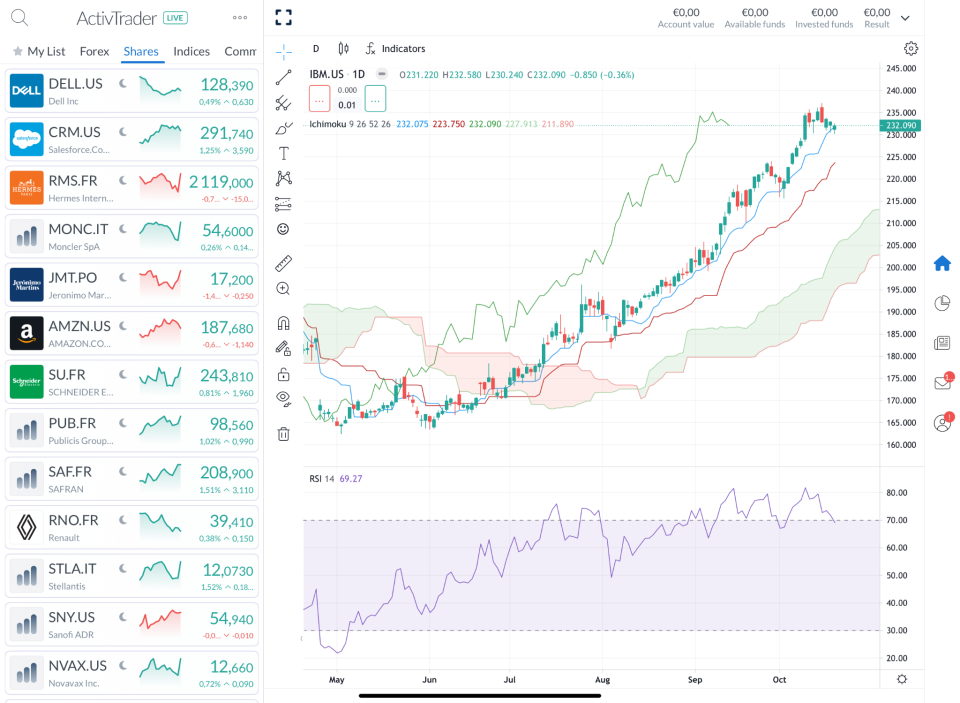

2# Can IBM’s Share Price Hit New Highs with a Strong Earnings Surprise?

IBM has made notable progress in its business, particularly with its focus on generative artificial intelligence, which played a key role in its strong performance last quarter. In its second-quarter earnings report from July, IBM exceeded analysts’ expectations, reporting a 1.9% revenue increase to $15.48 billion compared to the previous year. Net income also rose significantly to $1.83 billion, or $1.96 per share, up from $1.58 billion, or $1.72 per share, a year earlier.

Despite these gains, IBM faces several macroeconomic challenges, including higher interest rates, inflation, and geopolitical uncertainties, which may impact its growth. Still, the company remains confident in its tech-driven approach, particularly in AI and cloud computing, which it believes will fuel future success.

As IBM prepares to release its Q3 2024 earnings on Wednesday, Oct. 23, investors are eager to see if the company can once again exceed expectations. Analysts forecast a slower profit of $2.22 per share, down from $2.43 in the previous quarter, and a slight revenue dip from $15.77 billion to $15.06 billion. If IBM delivers a strong performance—boosted by AI adoption or robust hybrid cloud growth—it could reignite investor confidence and push the share price to new highs.

So far this year, IBM shares are up 43.78%, hovering around $232.

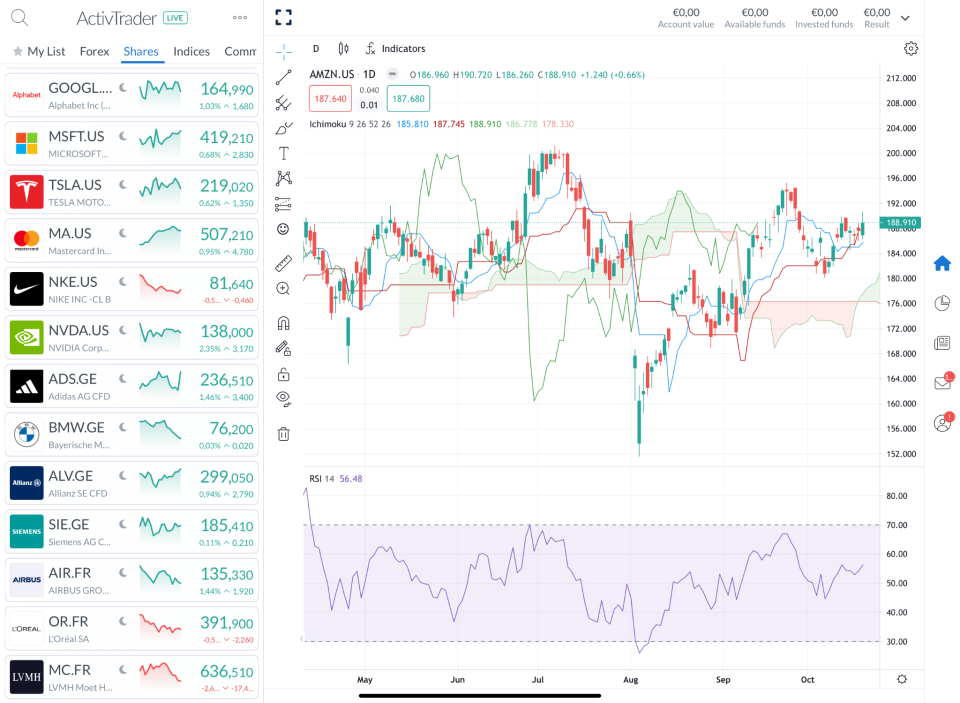

3# Is Amazon Still Losing Ground to Its Peers?

Amazon reported softer-than-expected revenue for the second quarter, alongside a disappointing forecast for the third quarter. Net sales grew 10% year-over-year to $148.0 billion, up from $134.4 billion in the same period last year, but fell short of the $148.56 billion projected by analysts at LSEG. Despite the revenue miss, Amazon saw a significant boost in profitability, with net income climbing to $13.5 billion, or $1.26 per diluted share, compared to $6.7 billion, or $0.65 per diluted share, a year ago.

The underwhelming revenue performance is largely attributed to sluggish growth in Amazon’s core retail business, where competition from discount platforms like Temu and Shein has intensified. These rivals, which allow Chinese merchants to sell low-cost products to U.S. consumers, are eating into Amazon’s market share. Sales in Amazon’s online stores segment grew just 5% year-over-year, reflecting consumers opting for cheaper products and leading to a decline in the company’s average selling price (ASP).

On the cloud front, Amazon Web Services (AWS) performed well, growing 19% year-over-year and generating $26.3 billion in revenue, surpassing estimates of $26 billion. However, AWS is expanding at a slower pace compared to its major competitors, Microsoft and Google, whose cloud divisions are growing more rapidly.

As Amazon looks ahead, the company faces the challenge of balancing slow retail growth with rising competition in both e-commerce and cloud computing, adding pressure to innovate and find new growth opportunities in the next quarter.

So far this year, Amazon shares are up 26.05%, hovering around $188.

Disclaimer

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. Between 66% and 83% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

ActivTrades Corp is authorised and regulated by The Securities Commission of the Bahamas. ActivTrades Corp is an international business company registered in the Commonwealth of the Bahamas, registration number 199667 B.

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk.

This article was originally posted on FX Empire

More From FXEMPIRE:

Nearfield Instruments Receives Purchase Order for QUADRA High-Throughput Metrology System from Leading Semiconductor Manufacturer in East Asia

ROTTERDAM, The Netherlands, Oct. 20, 2024 (GLOBE NEWSWIRE) — Nearfield Instruments, a leading innovator in advanced process control metrology solutions, is proud to announce the receipt of a purchase order for its flagship QUADRA High-Throughput Process Control Metrology product. The order, secured after an intensive supplier selection process, was placed by a prominent semiconductor manufacturer in East Asia, further strengthening Nearfield Instruments’ presence in this technologically advanced region.

The QUADRA system was selected following a competitive evaluation process, where it outperformed alternative metrology solutions in several key areas critical to advanced semiconductor manufacturing. The decision was driven by the following decisive factors:

- Direct Correlation to Device Yield: Extensive testing of QUADRA demonstrated a direct correlation between its measurement results and device yield (via E-test), a critical consideration for the customer’s high-performance semiconductor fabrication processes.

- Non-Destructive Measurement Capability: The QUADRA system stood out for its ability to conduct accurate, non-destructive measurements. After rigorous testing, QUADRA proved its reliability, showing no impact on the integrity of sensitive semiconductor components even under the most demanding conditions.

- Superior Throughput with Stability and Accuracy: QUADRA’s ability to deliver high throughput without compromising on accuracy and stability was a significant differentiator. The system’s superior speed, paired with precision, enables manufacturers to maintain peak production efficiency while ensuring stringent quality control.

- Outstanding Customer Support and Responsiveness: Nearfield Instruments’ reputation for exceptional customer support and responsiveness was a major contributing factor in the customer’s decision. The company’s commitment to providing continuous support throughout the evaluation and decision-making process was highly valued by the customer.

This strategic win marks a significant step in Nearfield Instruments’ ongoing expansion in East Asia. It reflects the growing recognition of QUADRA’s industry-leading capabilities in process control metrology, reinforcing the system’s role in driving mass production yield and quality for advanced semiconductor manufacturing.

“We are pleased to receive this important order from yet another highly respected semiconductor manufacturer in East Asia,” said Hamed Sadeghian, CEO of Nearfield Instruments. “It underscores the confidence our customers have in the QUADRA system’s ability to meet the demands of next-generation semiconductor fabrication, as well as the strength of our customer service and support. As semiconductor production processes become increasingly complex, Nearfield Instruments remains committed to delivering cutting-edge metrology systems that address the evolving challenges faced by manufacturers worldwide.”

About Nearfield Instruments

Nearfield Instruments is bridging the semiconductor industry’s metrology and inspection challenges with in-line, non-destructive process control nanometrology solutions for advanced 3D memory and logic devices. Their groundbreaking technology combines high-resolution with high-throughput, essential for the production of advanced semiconductor nodes. Nearfield is headquartered in Rotterdam with offices in Eindhoven, The Netherlands and Pyeongtaek, South Korea.

For more information, visit www.nearfieldinstruments.com

Media Contact

Roland van Vliet

Chief Partnership Officer

Nearfield Instruments B.V.

e-mail: roland.vanvliet@nearfieldinstruments.com

Telephone: +31620369741

![]()

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Don’t be grumpy about taking RMDs — you’ve got lots of options

Dear Paul,

I recently had to start taking money out of my investment accounts to satisfy my RMD (required minimum distribution). What’s the best thing to do with this money? I’d like it to continue to grow.

Still Want Growth

Most Read from MarketWatch

Dear Still,

Some people grouse when they have to take RMDs and grumble at the requirement to pay taxes on the money they withdraw. But if you can avoid that attitude, you can appreciate your good fortune in having this “problem.”

In years past, you essentially made a deal with the government:

· The U.S. Treasury agreed that you wouldn’t pay taxes right away on some of the money you earned if you put it into a tax-sheltered investment account like an IRA or a 401(k). That meant this money could work for you instead of the government.

· You agreed that when you reached a certain age (currently 73), you would start withdrawing that money and pay taxes on the withdrawals.

· And now, as a result, you almost certainly have more money than you would if it weren’t for this deal.

What you should do with the RMDs depends mostly on your eventual plans for that money.

Read: Are you taking an RMD? 10 smart things you can use it for right now.

If you think you will use or need it later in your life, you will probably want to balance growth (stock funds) with some measure of stability (bond funds) with more emphasis on the latter when you are within spitting distance of its use.

However, if you expect to leave these investments to your heirs, you should consider investing with their financial needs and risk tolerance in mind. That might mean investing mostly, if not entirely, in equities.

In either case I think the U.S. four-fund portfolio should offer good equity returns with less volatility than the S&P 500 SPX. The four funds could be AVUS AVUS (large cap blend), RPV RPV (large cap value), IJR IJR (small cap blend), and AVUV AVUV (U.S. small cap value).

You can see the long-term impact of these four equity asset classes in a colorful table that our team produced to show how this combination did, compared with its components, in every individual year from 1928 through 2023.

Quite aside from all that, there’s another important question you should ask yourself: Could some of this not-needed-now money improve your life in some significant way? My guess is the answer is yes.

Read: I have my RMD all figured out, except for one thing: Which investments should I take it from?

By age 73, you should be thinking about how to give yourself an extra reward for your years of working, saving and investing.

With some percentage of your RMD each year, you could do extra travel. You could donate to a charity that’s doing work you like. You could make gifts (up to $17,000 a year) to some of your heirs so you can experience their (you hope) appreciation and (you also hope) good sense in putting unexpected money (you also hope) to constructive use.

Whatever you choose, I think you can — and should — pat yourself on the back for the solid financial situation you are in.

Dear Paul,

Now that I’m 58 and approaching retirement, what is the most appropriate asset allocation and “glide path” for preretirement and then in retirement? I know the answer might be “It depends,” but for someone without a pension coming, and a mix of taxable and retirement accounts, what is the right mix of funds?

Gliding to Retirement

Dear Gliding,

You are right that the correct answer is “it depends.” To keep my answer simple (yet still sufficient), I’ll focus on two factors.

First, Wall Street’s collective wisdom. Second, your comfort level.

Big bucks are paid to the men and women who manage trillions of dollars in target-date funds (TDFs) at large mutual-fund companies. Every dollar is managed to combine an appropriate mix of growth (equity funds) and stability (bond funds) for investors in a given age range.

If you’re 58, you’re a good candidate for a fund such as Vanguard’s Target Retirement 2030 Fund (VTHRX). This fund’s glide path is managed assuming you’ll retire at age 65. If you intend to keep working longer, you could choose a fund with a later target date, say 2035.

These funds gradually change the mix of equities and bonds in their portfolios to become more conservative as their shareholders age.

There’s nothing wrong with this approach, and its sheer simplicity is a bonus.

However, you may want to be more conservative or more aggressive, depending on your risk tolerance and the amount of money you have in relation to what you will need to maintain an acceptable standard of living.

If you want to be more conservative, you could hold 10% to 15% of your money in bond funds and the rest in a target-date fund.

On the other hand, you may want to add a little extra firepower in order to increase the amount you are likely to have for spending in retirement and to leave to your heirs.

My suggestion in that case is to add something that target-date fund portfolios have very little of: small-cap value stocks. (You can also check out a recent podcast I recorded on this asset class; and for a much deeper dive, here’s a recent article.)

Our studies show that holding 80% in a target-date fund and the other 20% in small-cap value stocks could increase your annual return by 1% and increase your safe withdrawal rate by 0.5% (for example from 4% of your portfolio’s value each year to 4.5%).

That last detail may sound small, but in fact it represents a 12.5% increase in your retirement income all by itself.

For more on this idea, check out this excellent video with Chris Pedersen, director of research at the Merriman Financial Education Foundation.

.

Richard Buck contributed to this article.

.

Most Read from MarketWatch

CoolMOS IC Market to Reach $4.1 Billion, Globally, by 2032 at 5.3% CAGR: Allied Market Research

Wilmington, Delaware , Oct. 20, 2024 (GLOBE NEWSWIRE) — Allied Market Research published a report, titled, “CoolMOS IC Market by Type (Through-hole and Surface-mount), End User (Automotive, Industrial, Consumer Electronics, Telecommunication, Medical and Others): Global Opportunity Analysis and Industry Forecast, 2024-2032″. According to the report, the coolmos ic market was valued at $2.6 billion in 2023, and is estimated to reach $4.1 billion by 2032, growing at a CAGR of 5.3% from 2024 to 2032.

Download Research Report Sample & TOC: https://www.alliedmarketresearch.com/request-sample/A324259

(We are providing report as per your research requirement, including the Latest Industry Insight’s Evolution, and Potential)

Prime determinants of growth

The significant impacting factors of the CoolMOS IC market include surge in adoption of switch-mode power supplies, and rise in power electronics applications such as electric vehicles, renewable energy systems, and data centers. However, high initial cost is expected to hinder the market growth. Conversely, technological innovations are projected to offer remunerative opportunities to the CoolMOS IC industry.

Report coverage & details:

| Report Coverage | Details |

| Forecast Period | 2024–2032 |

| Base Year | 2023 |

| Market Size in 2023 | $2.6 billion |

| Market Size in 2032 | $4.1 billion |

| CAGR | 5.3% |

| No. of Pages in Report | 250 |

| Segments Covered | Type, End user, and Region. |

| Drivers | Increase in global emphasis on energy efficiency Growth in adoption of switch-mode power supplies Rise in power electronics applications such as electric vehicles, renewable energy systems, and data centers |

| Opportunities | Technological innovations |

| Restraint | High costs associated with CoolMOS ICs |

Segment Highlights

By type, the surface-mount segment held the highest market share in 2023 due to its smaller size, lighter weight, and suitability for automated manufacturing, leading to higher production efficiency and cost-effectiveness. Its prevalent use in compact, high-density applications, such as consumer electronics and telecommunications, drives its dominance in the market.

By end user, the consumer electronics segment held the highest market share in 2022, accounting for nearly half of the CoolMOS IC market share. The increase in demand for energy-efficient devices, like smartphones, laptops, and smart home appliances, fuels the adoption of CoolMOS ICs. Their superior performance in reducing power loss and enhancing device reliability significantly contributes to their extensive use in this sector.

Get Customized Reports with your Requirements: https://www.alliedmarketresearch.com/request-for-customization/A324259

Regional Market Outlook

On the basis of region, the CoolMOS IC market is analyzed across North America, Europe, Asia-Pacific, and LAMEA. Asia-Pacific accounted for the largest market share and is projected to grow at a fastest CAGR during the forecast period owing to the presence of major electronics manufacturers, rapid industrialization, and growing demand for advanced consumer electronics. Moreover, countries like China, Japan, and South Korea, with their robust semiconductor industries and extensive manufacturing capabilities, play a pivotal role in this regional dominance.

Players: -

- Infineon Technologies AG

- ON Semiconductor Corporation

- Vishay Intertechnology, Inc

- Mitsubishi Electric Corporation.

The report provides a detailed analysis of these key players in the global CoolMOS IC market. These players have adopted different strategies such as new product launches, collaborations, expansion, joint ventures, agreements, and others to increase their market share and maintain dominant shares in different regions. The report is valuable in highlighting business performance, operating segments, product portfolio, and strategic moves of market players to showcase the competitive scenario.

Inquiry before Buying: https://www.alliedmarketresearch.com/purchase-enquiry/A324259

Recent Development:

- In December 2023, Infineon Technologies AG launches its new CoolMOS S7T product family with an integrated temperature sensor to improve the accuracy of junction temperature sensing. The integration of these products has a positive impact on the durability, safety, and efficiency of many electronic applications. The CoolMOS S7T is best suited for solid-state relay (SSR) applications for enhanced performance and reliability due to its superior RDS (on) and the highly accurate, embedded sensor.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current CoolMOS IC market trends, estimations, and dynamics of the CoolMOS IC market. In the CoolMOS IC market forecast analysis is from 2024 to 2032 to identify the prevailing CoolMOS IC market opportunities. The CoolMOS IC market value is in the $ billion in the report.

- The market research is offered along with information related to key CoolMOS IC growth drivers, restraints, and opportunities.

- Porter’s five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth CoolMOS IC market analysis of the market segmentation assists to determine the prevailing CoolMOS IC market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market analysis. CoolMOS IC market size by country and CoolMOS IC market insights by each country covered in the report.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players. In the report leading CoolMOS IC company list along with CoolMOS IC market share by companies is also covered.

- The report includes the analysis of the regional as well as global CoolMOS IC market trends, key players, market segments, application areas, and CoolMOS IC market growth strategies.

Procure Complete Report (250 Pages PDF with Insights, Charts, Tables, and Figures) @ https://bit.ly/3YevzZY

CoolMOS IC Market Key Segments:

By Type

By End User

By Region

- North America (U.S., Canada, Mexico)

- Europe (France, Germany, Italy, UK, Rest of Europe)

- Asia-Pacific (China, Japan, India, South Korea, Rest of Asia-Pacific)

- LAMEA (Latin America, Middle East, Africa)

Access AVENUE – A Subscription-Based Library (Premium On-Demand, Subscription-Based Pricing Model) @ https://www.alliedmarketresearch.com/library-access

Avenue is a user-based library of global market report database, provides comprehensive reports pertaining to the world’s largest emerging markets. It further offers e-access to all the available industry reports just in a jiffy. By offering core business insights on the varied industries, economies, and end users worldwide, Avenue ensures that the registered members get an easy as well as single gateway to their all-inclusive requirements.

Avenue Library Subscription | Request For 14 Days Free Trial of Before Buying: https://www.alliedmarketresearch.com/avenueTrial

Trending Reports in Semiconductor and Electronics Industry:

Non-volatile memory (NVM) market valued at $41 billion in 2022, and is projected to reach $96.1 billion by 2032

3D NAND Flash Memory Market valued at $12.38 billion in 2020, and is projected to reach $78.42 billion by 2030

Automotive battery thermal management system market valued at $4.6 billion in 2022, and is projected to reach $18.7 billion by 2032

About Us:

Allied Market Research (AMR) is a full-service market research and business-consulting wing of Allied Analytics LLP based in Wilmington, Delaware. Allied Market Research provides global enterprises as well as medium and small businesses with unmatched quality of “Market Research Reports Insights” and “Business Intelligence Solutions.” AMR has a targeted view to provide business insights and consulting to assist its clients to make strategic business decisions and achieve sustainable growth in their respective market domain.

We are in professional corporate relations with various companies, and this helps us in digging out market data that helps us generate accurate research data tables and confirms utmost accuracy in our market forecasting. Allied Market Research CEO Pawan Kumar is instrumental in inspiring and encouraging everyone associated with the company to maintain high quality of data and help clients in every way possible to achieve success. Each and every data presented in the reports published by us is extracted through primary interviews with top officials from leading companies of domain concerned. Our secondary data procurement methodology includes deep online and offline research and discussion with knowledgeable professionals and analysts in the industry.

Contact:

David Correa

1209 Orange Street,

Corporation Trust Center,

Wilmington, New Castle,

Delaware 19801 USA.

Int’l: +1-503-894-6022

Toll Free: +1-800-792-5285

UK: +44-845-528-1300

India (Pune): +91-20-66346060

Fax: +1-800-792-5285

help@alliedmarketresearch.com

![]()

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Morning Bid: China rate cuts looming, US booming

By Jamie McGeever

(Reuters) – A look at the day ahead in Asian markets.

The trading week in Asia opens against an increasingly bullish global backdrop fueled by continued strength in U.S. stocks, but with local sentiment more circumspect due to the uncertainty surrounding China’s deep-rooted economic problems.

The People’s Bank of China is expected to cut its loan prime rates on Monday, Beijing’s latest move in a series of monetary, fiscal and liquidity support measures to shore up the imploding property sector, revive growth and fight off deflation.

PBOC Governor Pan Gongsheng told a financial forum in Beijing on Friday that the LPR will be reduced by 20 to 25 basis points on Monday, the official Xinhua news agency quoted Pan as saying.

The PBOC also on Friday unveiled new measures to inject more than $100 billion into the country’s stock market, which helped lift Shanghai’s blue chip equity index by 3.6%, while the MSCI Asia ex-Japan index rose 1.6% for its best day since Sept. 26.

China’s economic “data dump” on Friday wasn’t as bad as many feared it could have been, and annual GDP growth in the third quarter was slightly above consensus at 4.6%.

But as economist Phil Suttle notes, the past two quarters have been unusually weak, delivering 2.75% growth on a seasonally-adjusted annualized basis, “the weakest two-quarter growth rate in modern times” outside of COVID-related shutdowns.

Little wonder Beijing has sprung into action.

Stocks have responded positively, but bond yields are sliding again. They initially spiked higher on hopes the support measures, which include substantial bond issuance, will reflate the economy but 10-year yield is once again within sight of 2.00%.

U.S.-Sino trade wars have been pushed to the forefront of investors’ minds again after Republican presidential candidate Donald Trump said he would impose additional tariffs “at 150% to 200%” on China if China were to “go into Taiwan,” the Wall Street Journal reported on Friday.

The U.S. juggernaut, meanwhile, keeps rolling on – economic data are beating expectations, GDP growth is tracking well over 3%, incoming earnings are strong, and Wall Street is hitting new highs.

But perhaps the optimism is overdone. Analysts at Raymond James note that short-term options and technical indicators are getting skewed, suggesting the market may be “ripe for a period of consolidation or vulnerable to a near-term pullback.”

Financial conditions are easing around the world, as central banks cut rates and stocks march higher. On that score, investors in Asia will keep close tabs on the dollar, which has recovered recently and is at a three-month high.

Friday’s Morning Bid Asia newsletter incorrectly stated that Malaysia would announce GDP data later in the day. The preliminary GDP will be released on Monday, Oct. 21.

Here are key developments that could provide more direction to markets on Monday:

– China loan prime rate decision

– Malaysia GDP (Q3)

– Reserve Bank of Australia deputy governor Andrew Hauser speaks

(Reporting by Jamie McGeever)