Cigna revives merger talks with Humana, Bloomberg reports

Cigna (CI) has refreshed efforts to combine with Humana (HUM) after merger discussions fell apart late last year, Bloomberg’s Michelle Davis and John Tozzi report, citing people familiar with the matter. The companies have held informal talks lately about a possible deal, though such discussions are in early stages, the authors note. Shares of Humana are up about 4% in after-hours trading, while Cigna shares are 1.2% lower.

Published first on TheFly – the ultimate source for real-time, market-moving breaking financial news. Try Now>>

See Insiders’ Hot Stocks on TipRanks >>

Read More on CI:

We heard from 1,000 older Americans: Here are some of their biggest regrets

-

More than 1,000 older Americans shared their biggest regrets in life with Business Insider.

-

These included not saving enough for retirement and taking Social Security benefits too early.

-

Most older Americans are unable to absorb a financial shock, while millions can’t afford daily needs.

Over 1,000 Americans between the ages of 48 and 90 told Business Insider their biggest regrets in life. Those insights show how perplexing retirement and planning for it can be.

Responses to an opt-in Business Insider reader survey, along with interviews with 20 respondents, show that preparing for retirement while juggling life’s many obstacles is often a trial-and-error process. Many said they couldn’t crack the code on balancing how much to save, where to invest, when to retire, and how to be fiscally responsible when raising a family. Others said they took Social Security too early or didn’t pursue career opportunities that may have led to higher pay.

Janis Carroll, 79, said she was in the middle class for much of her life and made decent wages, but she is now struggling to live comfortably on about $25,000 in Social Security each year and $35,000 in savings.

Though she retired over a decade ago with enough to get by, she said not being more savvy with investing, moving too frequently, and draining an IRA account to buy a home she lost $50,000 on have contributed to her fears about the future. She’s considered returning to work, but she’s worried it would be too physically and mentally taxing.

“I don’t have the money to go to the movies or go anywhere,” said Carroll, who lives in Eugene, Oregon. “I have no idea what’s going to happen to me if I’m going to have an emergency.”

The median 55-year-old has less than $50,000 in retirement savings, according to a Prudential survey — which was conducted by Brunswick Group between April and May and interviewed 905 Americans ages 55, 65, and 75. According to the National Council on Aging and the LeadingAge LTSS Center, which analyzed the data of 11,874 households from the Health and Retirement Study, nearly 50% of Americans 60 or older say they have household incomes below what’s necessary for meeting their basic needs.

To be sure, three in four retired Americans say they have enough money to live comfortably compared to less than half of non-retirees, according to a Gallup poll conducted in April which surveyed 1,001 people and was published in August.

Many respondents’ regrets are partially out of their control, from a cancer diagnosis disrupting financial stability to an unexpected divorce or layoff.

BI analyzed over 1,000 responses to a callout in previous stories asking about older Americans’ life regrets, in addition to dozens of emails reporters received, to determine four of the main regrets they have about their lives.

We want to hear from you. Are you an older American with any life regrets that you would be comfortable sharing with a reporter? Please fill out this quick form.

1. Not saving enough for retirement

After navigating various job losses and undergoing cancer treatments, Jan Hoggatt, 69, is unsure she can ever retire and works part-time.

“I wish I hadn’t assumed I’d be able to work into my 70s,” said Hoggatt, who lives in the St. Louis suburbs and receives about $1,800 monthly in Social Security.

She regrets not better preparing financially for an emergency, adding that she never knew exactly how to go about saving for retirement or what resources were available.

Dozens, like Hoggatt, remarked that their parents, employers, or professors never taught them investing basics, adding that there weren’t many accessible resources for financial planning in their early careers. Some described saving for retirement as a trial-and-error process, noting that they wished they had worked with a financial advisor or taken courses on growing their wealth.

Meanwhile, nearly every respondent wished they had saved more for retirement. Many said they lived too much in the moment and didn’t consider putting money into retirement accounts or investments throughout their lives.

Respondents also commonly thought they would be able to survive on Social Security once they retired and wouldn’t need hefty savings. Well over a quarter said they have little savings and receive between $1,000 and $2,000 monthly in Social Security, forcing some to work part-time jobs or move into low-income housing.

“The benefits that we’re providing for people as they age are not keeping up with the cost of living,” Jessica Johnston, senior director for the Center of Economic Wellbeing at the National Council on Aging, told BI. She added that the asset limit people can have to receive Supplemental Security Income, which is $2,000 for individuals and $3,000 for couples, hasn’t changed since 1989.

To be sure, dozens said they rarely had enough money to set aside each week for retirement savings. A few dozen said they were single parents working two or three jobs to put food on the table. Others went on disability earlier in life and had only enough income to pay rent.

2. Making mistakes during the retirement process

Hundreds wrote that they were lost on how much to save, what to invest in, when to retire, and what to do financially during retirement. A few dozen wished they had more guidance on what pitfalls to avoid, how to live comfortably after working for decades, and what to do when a spouse dies.

Steve Watkins and his wife both worked for 50 years at their respective employers and retired with enough to live comfortably. Then his wife died in January.

Watkins, 74, receives about $3,100 a month in Social Security and has more than $1 million in savings. However, Social Security rules dictate that he cannot collect his wife’s $1,300 monthly benefits because her amount is lower than his. That lack of income worries him, as he doesn’t know how long his savings will finance his remaining years.

“You either have to go get another job to make up for it or suffer by losing that amount of money,” said Watkins, who lives outside Los Angeles.

Over two dozen respondents said they claimed Social Security too early and received less money each month than if they had waited until their full retirement age to collect more. Some had to collect Social Security early because they needed the money, though others didn’t realize how much more they could get if they waited.

Americans can collect Social Security as early as age 62, though benefits are reduced until reaching the full retirement age of either 66 or 67, depending on your birth year. People can delay taking their benefits until 70, which increases the amount.

Similarly, dozens regretted retiring too early without an insufficient nest egg. Then, they needed part-time work to supplement their Social Security payments. A handful noted that even though they waited until 65 to retire, they wished they had delayed retirement until 70 to pad their accounts and feel more financially secure.

3. Not making the right career choices

Along with not saving enough, hundreds of respondents said they should have been more aggressive during their careers to secure higher-paying roles.

Dozens said they stayed too long in dead-end jobs and avoided developing marketable skills. More than 100 respondents said they wished they had gone into higher-paying sectors or applied for more prestigious positions where they could have made more money.

Those in corporate positions wished they had tried harder to get promoted instead of settling. Over two dozen wished they had networked more outside their companies in case of job loss; many said they’re now facing unemployment in their 50s and 60s.

At least a dozen said they should have stayed more up-to-date on the skills necessary for securing new positions, such as new coding languages or online tools.

Alternatively, some wished they had been less ambitious. A few dozen regretted leaving stable careers to start businesses, some of which failed and put their founders in the red. Michael R., 70, told BI he lost over $650,000 in savings and had to declare bankruptcy after his New York-based business crashed during the 2008 recession. He asked to use partial anonymity due to privacy concerns.

4. Not prioritizing education enough

Hundreds of respondents wrote they should have pursued education more. Though a few dozen said they lacked the money to attend higher education institutions — or were not told about the benefits of college — those with the means wished they had gotten an associate’s or bachelor’s degree to better prepare for the workforce.

However, respondents were divided over student loans. Over two dozen said they regretted not attending college and taking out loans to pursue higher education, as it may have opened more doors for them. Another dozen wished they took out fewer loans or worked throughout college to fund their tuition. These people are still paying off loans from 50 years ago.

To be sure, at least a dozen said they regretted attending college and not going into the workforce immediately. They said college didn’t prepare them well for more advanced careers.

A few said they went to college later in life, which opened more doors for them professionally, though they said it was difficult attending classes while juggling a job and raising children. Still, many said this decision was fulfilling for advancing their careers.

Carol Brownfield, 48, is going back to community college to become a therapist counselor. The Washington resident said she has lots of experience, from running a casino and resort, though she wanted to “better myself and do what I want to do.”

“Going back to school is for a career that pays better and just matches with my morals,” Brownfield said. “My daughter sees that. She says, ‘I’m right behind you, Mom,’ and she wants to do it too.”

Are you an older American with any life regrets that you would be comfortable sharing with a reporter? Please fill out this quick form or email nsheidlower@businessinsider.com.

Read the original article on Business Insider

Reality bites: Is Generation X in denial about its own impending retirement?

Is Generation X in denial about its own impending retirement?

Gen X, born between 1965 and 1980, will be next to retire after the baby boom. It’s a generation largely defined by financial uncertainty: Generation X was the first to cope without ubiquitous workplace pensions, relying instead on a new savings tool called the 401(k). The Great Recession of 2008 stands as the generation’s defining economic event.

Now, with the oldest Gen Xers pushing 60, the cohort may not be ready for its next life stage.

A Wealth Watch survey from insurer New York Life is one of several recent reports that portray much of Generation X as woefully unprepared for their looming retirement.

Fewer than half of Generation X, or 46%, are “actively planning for retirement,” New York Life found, even as they approach the milestone.

Most of Generation X, or 70%, think they will retire “later than expected,” the survey found, “or not at all.” Only one-quarter of Gen-Xers believe they will retire on time. The survey, released in September, reached 2,230 adults.

‘They’re basically going to be working forever’

“There are a whole lot of Gen Xers who are finding themselves resigned to the fact that they’re basically going to be working forever,” said Matt Schulz, chief credit analyst at LendingTree, the personal finance site.

Generation X’s retirement fears are not unwarranted.

Gen Xers ages 45 to 54 had a median net worth of about $247,000 in 2022, according to the federal Survey of Consumer Finances.

That’s less money than baby boomers had at the same age. Boomers in the 45-54 age group had a median net worth of about $265,000 in 2007, after adjusting for inflation.

The contrast suggests Generation X has struggled more than other age groups to recover from the Great Recession of 2008.

“I think there’s this cumulative wear and tear of different circumstances Gen X has had throughout their lives,” said KC Boas, head of retirement thought leadership and marketing at BlackRock, the global investment firm.

First the dot-com bubble, then the Great Recession

Many in Generation X entered the workforce around the time of the dot-com bubble, the tech-stock boom that went bust in 2000, sending the stock market tumbling.

Several years later, many Gen Xers were in their prime earning years when the Great Recession hit. Every generation suffered in 2008, but economic research suggests Gen X suffered more than most.

“Older generations were hit much harder, in some ways, because they had more to lose,” said Catherine Collinson, CEO of the nonprofit Transamerica Center for Retirement Studies.

Late baby boomers, born between 1960 and 1965, were also in their top earning years when the Great Recession descended. Today, the “Beatlemania boomers” have much less retirement savings than Americans born in the 1950s or earlier. They and Gen X suffered a similar fate.

Millennials, born between 1981 and 1996, have fared better. The millennial generation is in a stronger financial position now than Gen X was at the same age, according to a new LendingTree analysis.

As of 2022, millennials had a median net worth of $84,941, LendingTree reports. Generation X had a lower net worth at the same age: $78,333, after adjusting for inflation.

Millennials are also better-off financially than boomers were at the same age. But boomers are much more likely than Gen X or millennials to have workplace pensions, a guaranteed source of retirement income.

Gen X entered the workforce as pensions were fading

Generation X entered the workforce as workplace pensions were fading, leaving most workers to build their own retirement savings with 401(k) plans and Individual Retirement Accounts.

But 401(k) plans were few and far between in the early years. Partly for that reason, many Gen Xers got a late start in retirement saving.

“This all happened without access to education and guidance,” said Jessica Ruggles, corporate vice president of financial wellness at New York Life. “It wasn’t until much later that we did things like auto-enrollment and auto-contribution,” innovations that encourage higher rates of retirement saving.

Schulz, of LendingTree, is 52: a quintessential Gen Xer. He got his first real job around 1995, in his early 20s.

“I didn’t even really think of retirement, or anything like that, at that age,” he said.

The typical Gen Xer began saving for retirement at age 30, half a decade later than millennials, according to the Transamerica Center. Today, the median Gen X household has $93,000 in retirement savings: Not nearly enough, in the eyes of many retirement planners.

As a result, Transamerica found, most Gen Xers plan to keep working in retirement.

Those figures come from the 2024 Transamerica Retirement Survey of Workers, which reached 5,730 workers.

Gen X faces a singular struggle in preparing for retirement

Other retirement surveys concur that Generation X faces a unique struggle in preparing for retirement.

Only 60% of Gen Xers feel “on track” for retirement, the lowest share of any generation, according to the 2024 BlackRock Read on Retirement report.

Three-fifths of Gen Xers worry they will outlive their retirement savings, BlackRock found. Only two-fifths of Gen Xers use a financial adviser, the lowest rate of any generation.

Generation X also seems to have a credit card problem. More than one Gen X cardholder in four, or 27%, have maxed out their credit, Bankrate reported on Thursday.

Gen-Xers are more likely than millennials or boomers to have exhausted their credit, the survey found.

The finding is worrisome, retirement experts say, because consumers should be paying down their debt as they approach retirement, not charging it up. The Bankrate survey covered 3,576 adults.

Meet the ‘Beatlemania boomers.’ They face a looming retirement crisis

Gen X remains hopeful for the future

But here’s some good news, at least from a retirement perspective: Generation X is spending less on discretionary purchases in 2024, Bank of America reports.

“Discretionary” is a category that covers non-essentials. And discretionary spending among Gen Xers is down 2% in the year ended August, according to internal Bank of America card data, the biggest drop of any generation.

At the same time, Gen X is investing a larger share of its paycheck than other generations, according to a September report from Bank of America Institute.

“Bottom line, they’re spending less and they’re investing more,” said Joe Wadford, an economist at the Bank of America Institute. “It’s certainly a sign that Gen X is hopeful for the future. They think they will retire, and they think that in the future, those investments are going to pay off.”

This article originally appeared on USA TODAY: Gen X is next up for retirement. Are they in denial?

Peter Schiff Criticizes Trump's Tariff Strategy, Oil Prices Drop Following Netanyahu's Statement, Kamala Harris Pledges To Remove Unnecessary Degree Requirements And More: Top Political Updates This Week

The past week was a hotbed of activity, with political debates and economic strategies taking center stage. From tariff discussions to election battles, the week saw a flurry of statements and counterarguments from prominent figures. Here’s a quick recap of the top stories that made headlines over the weekend.

Peter Schiff Criticizes Trump’s Tariff Strategy

Noted economist and financial commentator Peter Schiff voiced his opinion on former President Donald Trump’s tariff strategy. Schiff, in a recent social media post, argued that Trump’s tariffs were not imposed on China but on Americans purchasing Chinese products. Read the full article here.

Barry Diller Criticizes Billionaire Trump Supporters

Barry Diller, the chair of IAC Inc and a supporter of Vice President Kamala Harris, expressed his disapproval of wealthy business figures backing Donald Trump in the 2024 election. Diller, a longtime Democratic Party supporter, shared his views in recent interviews. Read the full article here.

Kamala Harris Pledges To Remove Unnecessary Degree Requirements

Vice President and Democratic presidential nominee Kamala Harris reiterated her commitment to eliminating degree prerequisites for certain federal jobs. She also urged the private sector to follow suit, stating that a college degree isn’t the only measure of a qualified worker. Read the full article here.

Oil Prices Drop Following Netanyahu’s Statement

Crude oil prices saw a significant drop after Israeli Prime Minister Benjamin Netanyahu stated his willingness to strike military targets in Iran instead of oil or nuclear facilities. This statement was made during a call with President Joe Biden last Wednesday. Read the full article here.

Mark Cuban And Kevin O’Leary Clash Over China Tariffs

“Shark Tank” co-stars Mark Cuban and Kevin O’Leary engaged in a public disagreement over tariffs on China. O’Leary called for a massive 400% increase in tariffs, citing unfair business practices by China. However, Cuban expressed his concerns over this approach. Read the full article here.

Image via Wikimedia Commons

This story was generated using Benzinga Neuro and edited by Anan Ashraf.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Backyard Treehouse Gets So Much Attention On Airbnb, Owner Doesn't Have To Work Anymore: 'I'm Booked For Months'

A DIYer once dreamt of constructing a treehouse on his land before his own house was even built. Now, with multiple accommodations on the property, the treehouse has become a reality, and a legitimate source of income.

Getting Off The Ground: Will Sutherland built a treehouse in his backyard in six months’ time. It’s super popular on Airbnb Inc ABNB, bringing in an average of $30,000 per year on the platform, according to a Business Insider report.

He saved money on the build by doing all the work himself and sourcing a lot of the material from a friend who was in the process of building a house at the same time.

There’s a queen bed with a loft area above it, so it can accommodate a family. It doesn’t have running water, but there’s a five-gallon tank, so guests can brush their teeth or wash their hands. The treehouse also has a window unit air conditioner and an electric heater.

See Also: This DIYer Built A $17K Tiny Home That Generates $50K A Year — Now He Works Just 2 Hours A Week

Despite the lack of amenities, the house in the trees doesn’t have any trouble attracting guests, and let’s be real, if you are interested in staying the night in a treehouse, you probably aren’t expecting a whole lot.

Depending on the time of year, Sutherland lists it on Airbnb for anywhere from $160 to $250 a night.

“The treehouse gets thousands of views per month on Airbnb, and I’m booked for months out,” he said.

The treehouse alone brings in $30,000 a year in income, but Sutherland also has a renovated school bus on his property that he rents out to guests and a bathhouse for anyone staying on the land.

Combined, the two unique Airbnb listings generate enough annual income that he was able to quit his job and spend his time working on other projects.

“We basically live in a little miniature community here, flanked by our bus guests and treehouse guests all the time,” Sutherland said.

The Airbnb income is rewarding in more ways than one. Sutherland now works from home, which has freed up more time that he can spend with friends and family. He also feels fulfilled seeing his guests create memories in a treehouse he built himself.

Read Next:

This story is part of a new series of features on the subject of success, Benzinga Inspire. Some elements of this story were previously reported by Benzinga and it has been updated.

This illustration was generated using artificial intelligence via MidJourney.

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

1 Reason to Buy Eli Lilly Stock Hand Over Fist Right Now

Pharmaceutical powerhouse Eli Lilly (NYSE: LLY) is having a terrific 2024. Shares have gained 58% so far this year, handily outperforming both the S&P 500 and Nasdaq Composite indexes.

Much of the share price appreciation can be attributed to Lilly’s success in the diabetes and obesity care markets thanks to its blockbuster glucagon-like peptide-1 (GLP-1) agonists, Mounjaro and Zepbound. Moreover, Lilly made headlines back in July as the company’s Alzheimer’s drug, donanemab, received approval from the Food and Drug Administration (FDA).

About a month ago, Lilly secured another big win that I think is being overshadowed by the company’s success in other areas of the healthcare realm. Below, I’m going to break down Lilly’s latest milestone and explain why I see now as a great opportunity to scoop up shares.

Lilly’s latest win

Back in September, Lilly received FDA approval for its atopic dermatitis medication Ebglyss. Atopic dermatitis is more commonly referred to as eczema.

Eczema is generally treated with topical medications such as creams, ointments, or gels. For some patients, topical solutions are suboptimal as symptoms such as dry skin and itchiness continue lingering.

Ebglyss differs from topical ointments because it is an injectable. The medication is specifically marketed for patients with moderate-to-severe eczema who are not able to fully treat their symptoms with topical prescriptions.

A $31 billion opportunity

According to Lilly’s announcement regarding Ebglyss, there are 16.5 million adults with eczema just in the U.S. Moreover, roughly 40% of this cohort experiences “moderate-to-severe symptoms like itchiness, dry and scaly skin, discoloration and rashes, which can lead to more scratching that may cause skin to crack and bleed”.

To put some numbers on the eczema treatment opportunity, Precedence Research estimates that the global total addressable market (TAM) will reach $31.4 billion by 2034 — up from $14.7 billion today. Additionally, Precedence’s report suggests that North America is the largest market for eczema and could reach $8.1 billion by the middle of next decade.

Is Eli Lilly a good stock to buy right now?

The chart below illustrates the price-to-earnings (P/E) ratio for Eli Lilly over the last six months.

Right off the bat, I’ll admit that a P/E multiple of 113 is not cheap.

However, there are some trends from the chart above that I think are worth calling out and studying a bit further. Notice that Lilly’s P/E ratio began to fall between July and August.

At a company-specific level, some of the sell-off can be traced to rising fears that Lilly’s dominance in weight loss will begin to decelerate should new products from competitors come to market. Additionally, some in the political arena have also taken issue with Lilly’s pricing protocols for Mounjaro and Zepbound.

From a wider standpoint, the markets in general experienced some brutal selling activity over the summer, and Lilly’s price action was impacted by these moves as well.

And yet over the last month or so, Lilly’s P/E has rebounded back to where it was about six months ago. I find this dynamic peculiar because Lilly is a much different enterprise today than just several months back.

The company now has opportunities across Alzheimer’s disease, eczema, and even artificial intelligence (AI). So, while Lilly stock isn’t trading at a steal by any means, I think the stock is potentially underpriced considering the massive opportunities outside of weight management that the company has.

Lilly’s eczema approval looks like yet another stepping stone as it continues to build one of the most prolific pharmaceutical operations on the market. I see the stock as a compelling buy for long-term investors and believe that Lilly’s growth is just getting started.

Should you invest $1,000 in Eli Lilly right now?

Before you buy stock in Eli Lilly, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Eli Lilly wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $845,679!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 14, 2024

Adam Spatacco has positions in Eli Lilly. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

1 Reason to Buy Eli Lilly Stock Hand Over Fist Right Now was originally published by The Motley Fool

2 Surefire Chip Stocks to Buy and Hold for the Next Decade

The chip industry has been growing for decades, and the investment in artificial intelligence (AI) technology could keep the industry growing for years to come.

While the semiconductor industry can experience cyclical demand, the increasing quantity of chips used in consumer devices, cars, and data centers bodes well for the industry’s long-term prospects. Statista projects the industry will grow 10% per year through 2029 to reach $980 billion.

To profit off this opportunity, here are two outstanding chip companies to hold for the next 10 years.

1. Taiwan Semiconductor Manufacturing

Taiwan Semiconductor Manufacturing (NYSE: TSM) is close to joining the $1 trillion club. The share price has doubled since 2022, bringing its market cap to about $971 billion. TSMC is in a lucrative position as the leading semiconductor foundry, which refers to its business of making chips for other companies, including Nvidia, Broadcom, Advanced Micro Devices, and Intel, among others.

The company has delivered market-beating returns for years, and it continues to show strong growth. Analysts expect revenue to be up 26% this year before increasing 24% in 2025, according to YCharts.

Investing in Taiwan Semiconductor is making a bet on the long-term advances in chip technology and increasing chip quantities in smartphones, data centers, and cars. Because its chips are used in a variety of end markets, TSMC is a relatively safe way to invest in the growth of the chip industry.

TSMC is in a great position to benefit from growing demand for chips used for AI workloads. The company’s revenue from high-performance chips makes up half of the business, and TSMC controls 61% of the global foundry market. Its long-standing customer relationships, advanced manufacturing processes, and large capacity to meet demand are advantages that position the company to deliver profitable growth for shareholders.

The stock offers excellent return prospects in the near term, too, as it trades at a very attractive price-to-earnings ratio relative to forward earnings estimates. Analysts expect the company’s earnings to grow at an annualized rate of 26%. Assuming TSMC meets those estimates, the stock could double within three years if it’s still trading at the same price-to-earnings multiple.

2. Arm Holdings

Arm Holdings (NASDAQ: ARM) potentially has even greater long-term upside than TSMC. It currently has a market cap of about $159 billion, but could join the $1 trillion club one day. It is gaining share in several markets where its chips are used, including cloud computing, networking equipment, consumer electronics, automotive, and the Internet of Things.

Arm’s revenue grew 39% year over year in the most recent quarter, but it’s important to know that Arm doesn’t make money by manufacturing chips. Instead, Arm focuses on chip design, and then it licenses those designs to other semiconductor companies and manufacturers. It earns a royalty on nearly all processors shipped using its products, which allows Arm to earn very high margins.

Arm-based processors are in high demand because they deliver exceptional performance with lower energy consumption. The latter is becoming increasingly important, since more powerful chips run hotter and drive up energy costs. For large data centers, this can be a problem, but Arm is offering solutions that address this challenge. For example, U.K.-based Avantek has developed an Arm-based server that consumes up to 90% less electricity.

Arm-based products play such an important role in the industry that Nvidia tried to acquire it four years ago, which ultimately failed to gain the approval of regulators. But Nvidia’s Grace processor included in its upcoming Blackwell platform for AI workloads is based on Arm. This positions the chip designer to benefit from the growing demand for AI chips in data centers.

Arm stock has been volatile, but patient investors should do well. Analysts expect the company’s earnings to grow at an annualized rate of 27% over the next several years. The company should continue to grow faster than the chip industry and deliver excellent returns to investors over the next decade.

Should you invest $1,000 in Taiwan Semiconductor Manufacturing right now?

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $845,679!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 14, 2024

John Ballard has positions in Advanced Micro Devices and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and Intel and recommends the following options: short November 2024 $24 calls on Intel. The Motley Fool has a disclosure policy.

2 Surefire Chip Stocks to Buy and Hold for the Next Decade was originally published by The Motley Fool

A $295 Billion Opportunity Is Hiding In Plain Sight. 2 Stocks That Should Help You Plug Into It.

Last month, utility company Constellation Energy unveiled plans to restart one of the two now-mothballed nuclear reactors at Pennsylvania’s Three Mile Island power facility.

On the surface it doesn’t mean much. The world needs more electricity right now. Nuclear is a quickly accessible low-cost option.

There was a curious detail within Constellation’s press release, however. That is, although it will connect to the national power grid, the electricity it will generate is largely meant to power AI data centers managed by software giant Microsoft. The news underscores the fact that data centers are power-hungry, and increasingly so the bigger the business gets. Goldman Sachs believes data centers’ power consumption will grow 160% between now and 2030, yet will still just be getting started then.

The restart of Three Mile Island’s 800-megawatt reactor, however, is only a stopgap measure. The future of nuclear power is likely to be defined by so-called small modular reactors, which are precisely what they sound like … nuclear power plants that are easy to build and cost-effective to manage. Perhaps most notably, they can be put into action much close to where the electricity they generate is used, rather than delivering their electricity through the power grid.

Two particular companies stand ready to capitalize on this quickly gelling opportunity.

Small modular reactors are the real deal

This isn’t merely theoretical thinking either. Just within the past week Alphabet as well as Amazon announced intentions to purchase electricity generated by small modular reactors (or SMRs) to power their AI data centers. Industry research outfit Wood Mackenzie estimates the SMRs already under construction will eventually be able to produce over 22 gigawatts of electricity. That’s enough to power over 16 million homes or, presumably, at least a whole bunch of data centers.

Even before the first of these power plants becomes operational, though, more are apt to be lined up in anticipation of their success. IDTechEx reports the annual SMR market will be worth over $72 billion per year by 2033, en route to $295 billion in 2043. That’s an annualized growth rate of 30%.

It almost sounds too fantastical. If nothing else the complicated logistics of the SMR movement is a limiting factor.

There are many factors working in the small modular reactors’ favor, however, that are so much more powerful.

Chief among these factors are carbon-neutral power goals that are evolving into outright mandates. While nuclear power may have a dented reputation due to its fair share of catastrophic (or near-catastrophic) accidents, it does work and can be safe using more modern reactor designs and better-grounded standards.

Another driving force is the way and reasons energy is created and then utilized. Modular reactors are feasible for on-site energy creation at facilities like mines, refineries, and desalination plants, or even for generating the heat needed by smelters, many of which still burn coal.

SMRs are also particularly promising as a means of producing pure hydrogen, used in fuel cells to create clean electricity. The stumbling block is just the amount of raw energy needed to split water into its two atomic elements (hydrogen and oxygen) in the first place. With nuclear power, there’s plenty of clean energy to spare when splitting water molecules.

Two ways to play

So it’s a work in progress. The core opportunities are starting to gel, though. Two stand out among the rest.

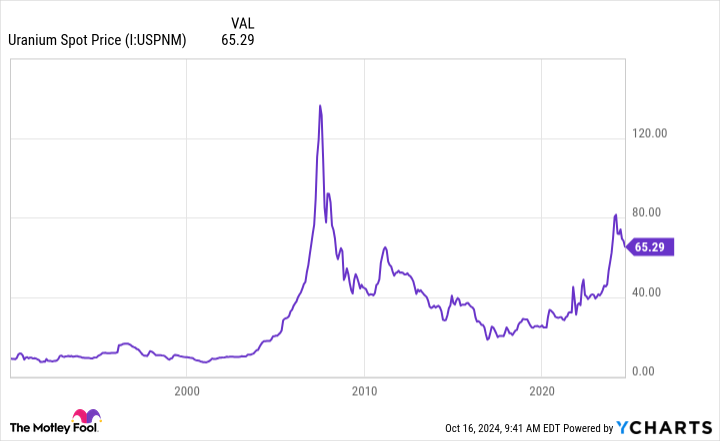

First, with the creation and consumption of nuclear power set to grow for the foreseeable future, the world needs more nuclear fuel — predominantly uranium-238. BMO Capital Markets expects global consumption of uranium to grow by nearly 3% per year through 2035.

That’s not massive growth, but given that the supply-and-demand dynamic favors continued price increases, look for uranium prices to continue growing.

There’s a handful of publicly traded uranium miners like Uranium Energy (NYSEMKT: UEC) and Australia’s diversified mineral miner BHP Group Limited. But perhaps your best bet is a company called Cameco (NYSE: CCJ). It’s one of the world’s biggest suppliers of high-grade uranium, selling $2.6 billion worth of nuclear fuel last year, turning $339 million of it into net income thanks to its low-cost operation. It’s also sitting on nearly 500 million pounds worth of the material just waiting to be dug up.

Small modular reactors are of course the other major opportunity. Nano Nuclear Energy (NASDAQ: NNE) and Oklo (NYSE: OKLO) are a couple of SMR manufacturers perhaps worth putting on your radar. A company called NuScale Power (NYSE: SMR), however, is arguably further along than any other outfit on the monetization front.

This optimism wasn’t felt a year ago when Utah Associated Municipal Power Systems canceled its plans made with NuScale to establish what would have been the nation’s first SMR. It wasn’t quite the indictment of the idea it was being made out to be at the time though. NuScale is still working on nearly a dozen other small modular reactor projects — here and abroad — with undeterred partners.

The reward aligns with the risk

There’s risk here, to be sure.

Again, although nuclear power itself is well-proven, small modular reactors aren’t; would-be partners may be taking a “wait and see” approach, prolonging the adoption process. Moreover, while NuScale is the only company with an SMR design thet’s been approved by U.S. Nuclear Regulatory Commission for use in this country, this particular 50-megawatt reactor design isn’t the 77-megawatt version NuScale Power ultimately hopes to offer. Even if the new model is approved, that approval won’t come through until mid-2025, clouding the bullish argument.

Waiting for absolute certainty before stepping in, however, also leaves money on the table. The time to take your shot on less-than-fully gelled premises is before they become obvious opportunities. Once they’re obvious, much of any prospective gain is in the rearview mirror.

Of course, given the fluidity of the movement, we can’t rule out the possibility of a new name surfacing as an important nuclear power player either. Keep your eyes open to that possibility too.

Should you invest $1,000 in NuScale Power right now?

Before you buy stock in NuScale Power, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and NuScale Power wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $845,679!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 14, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. James Brumley has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Amazon, and Goldman Sachs Group. The Motley Fool recommends Cameco and NuScale Power. The Motley Fool has a disclosure policy.

A $295 Billion Opportunity Is Hiding In Plain Sight. 2 Stocks That Should Help You Plug Into It. was originally published by The Motley Fool