Why Pennsylvania's GOP Districts Are Embracing Weed: The Cannabis Revolution You Didn't See Coming

As Pennsylvania’s legislative session heats up, one question stands out: why are Republican-controlled districts turning cannabis-friendly? Polling data reveals strong bipartisan support for cannabis legalization across key competitive districts. What’s driving this change?

A deeper look at economic distress, poverty and the opioid epidemic in these areas could hold the answer and offer a roadmap for other red states grappling with similar issues. With Pennsylvania being a critical swing state in national elections, the outcome of this issue may have broader political implications.

- Get Benzinga’s exclusive analysis and the top news about the cannabis industry and markets daily in your inbox for free. Subscribe to our newsletter here. You can’t afford to miss out if you’re serious about the business.

Voter Support Across Party Lines

According to surveys conducted by Cygnal and Responsible PA, a clear majority in districts like HD 44 (Allegheny County) and HD 18 (Bucks County) support cannabis legalization.

In HD 44, 67% of voters back legal and regulated cannabis, including 56% of Republicans. Similarly, 68% of voters in HD 18 support adult-use cannabis, with 55% of Republicans in favor.

Even in traditionally conservative areas like Beaver County (HD 16), strong support reaches 72%, reflecting widespread public approval.

Interestingly, the support transcends party lines, with voters citing economic growth, public safety, and criminal justice reform as top reasons for legalization. More than half of voters in HD 44 and HD 18 believe that passing cannabis reform this session is “crucial” for stimulating local economies.

But why is this happening in these conservative strongholds?

Economic Struggles And The Opioid Crisis: Key Drivers?

Beyond the polling data, a closer look at these districts’ economic and social conditions paints a clearer picture of why cannabis legalization is gaining traction.

Beaver County, which shows high support for cannabis, faces a poverty rate of 11.3%, while Luzerne County (HD 118) has a poverty rate of 13.4%. The opioid epidemic also looms large.

Pennsylvania has been one of the states hardest hit by the opioid epidemic, with an overdose death rate of 44.3 per 100,000 people, among the highest in the U.S., according to the Philadelphia Federal Reserve Bank. This crisis has deeply affected the labor force, particularly in regions already suffering from economic decline.

Many of these areas have seen significant drops in workforce participation, especially among men, as addiction further limits job opportunities. These intertwined issues of addiction and unemployment highlight why distressed regions might view cannabis legalization as a potential solution for both economic growth and harm reduction

According to the National Bureau of Economic Research (NBER), opioid-related deaths increase by 3.6% for every one-percentage-point rise in unemployment. Pennsylvania ranks among the states most affected by opioid addiction, particularly in rural and economically distressed areas like Beaver County.

In regions where traditional healthcare options are out of reach, residents could be seeing cannabis as a safer, cost-effective alternative for pain management.

Fleeing Sales

Many voters in these districts travel to nearby states like New Jersey and New York to buy cannabis, highlighting an economic drain. Pennsylvania is missing out on both tax revenue and consumer dollars by keeping cannabis illegal while neighboring states benefit.

Presidential And State House Polling Context

The polls also show that cannabis legalization is becoming a pivotal issue in Pennsylvania’s competitive political landscape.

The surveys conducted by Responsible PA, show tight races, with 49% supporting Trump versus 47% for Harris in HD 44, and similarly close margins in other districts. Despite these tight races, bipartisan support for cannabis is rising.

Polling reveals that nearly one-third of voters in HD 44 said they’d be more likely to support a candidate in favor of cannabis legalization. This suggests that cannabis reform could sway voters in key districts, especially in a state like Pennsylvania, where every vote counts in national elections.

Read Also: It’s Your Constitutional Right: How You Can Break The Senate’s Block On Cannabis Legalization

Broader Support Across Competitive Districts

Support for cannabis legalization isn’t limited to just one or two areas. Across five key competitive districts—HD 16 (Beaver County), HD 72 (Cambria County), HD 118 (Luzerne and Lackawanna Counties), HD 144 (Bucks County), and HD 151 (Montgomery County)—more than 60% of voters support regulated cannabis sales.

These areas, which include traditionally conservative regions, are turning to cannabis as a way to stimulate economic growth, create jobs, and reduce reliance on illegal markets.

This growing support is not just about personal freedom or criminal justice reform—it’s deeply tied to economic concerns.

In districts like HD 151, 74% of voters believe cannabis legalization will boost the economy by creating jobs, and similar high numbers are seen across HD 118, HD 144, and HD 16. As these regions grapple with unemployment and poverty, the promise of a cannabis industry offering economic stimulus and new job opportunities is highly appealing.

Read Also: The Election Issue No One Saw Coming: Trump’s Weed Gamble In Swing States

A Model For Other States?

The story unfolding in Pennsylvania could serve as a blueprint for other conservative strongholds. By addressing real-world problems like unemployment and alternative healthcare options, cannabis reform crosses party lines and offers a pragmatic solution to economic and social crises.

With voter support building and a bipartisan bill on the table, it’s clear that cannabis legalization is no longer just a liberal issue. It’s a matter of economic survival in some of the state’s most distressed areas—and potentially a model for other states facing similar struggles.

In the meantime, several cannabis companies stand to benefit from the potential legalization of adult-use cannabis in Pennsylvania. These include Jushi Holdings JUSHF, Cresco Labs CRLBF, Green Thumb Industries GTBIF, Verano Holdings VRNOF, and Trulieve Cannabis TCNNF.

Read Next: What Trump Learned About Marijuana That DeSantis Did Not And Why The GOP Might Become Weed-Friendly

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

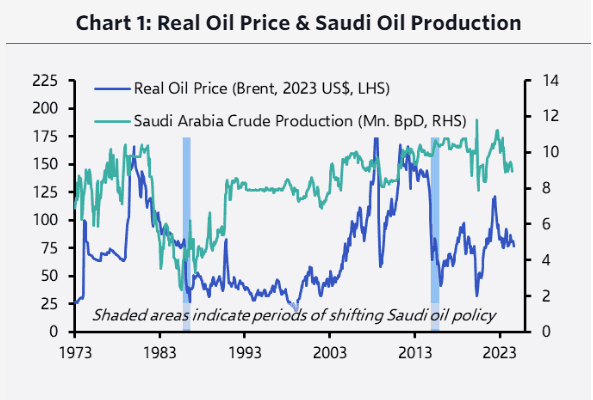

Why Saudi Arabia may ‘open the spigot’ on oil production — and crater crude prices

The possibility that Saudi Arabia will lift the “floodgates” on its oil production has climbed in recent weeks, fueled by “deteriorating cohesion” among the group of major oil producers known as OPEC+, according to a report from Capital Economics released Monday.

A “sense of frustration is clearly building,” Kieran Tompkins, climate and commodities economist at Capital Economics, wrote in Monday’s note. “Although the focus in the oil market has shifted to geopolitical risks and potential short-term supply disruptions, just as importantly, we think the possibility that Saudi Arabia could open the floodgates has increased in recent weeks alongside reports of deteriorating cohesion among OPEC+ members.”

Most Read from MarketWatch

Producers in OPEC+ — comprised of the Organization of the Petroleum Exporting Countries and its allies — who have been implementing voluntary production cuts have overproduced by as much as 800,000 barrels per day, he said.

Earlier this month, the Wall Street Journal reported that Prince Abdulaziz bin Salman, Saudi Arabia’s oil minister, warned fellow producers in a conference call that oil could drop to $50 a barrel if they don’t comply with agreed production cuts. OPEC said on X, however, that the article falsely reported that a conference call took place. “The OPEC Secretariat categorically refutes the claims made within the story as wholly inaccurate and misleading.”

Tompkins also pointed out that a Sept. 26 article from the Financial Times suggested that Saudi Arabia would comfortably weather a period of lower oil prices through alternative funding measures. That “strikes of a not-so-subtle reminder it has the ability to ‘punish’ ‘cheating’ producers,” said Tompkins, who titled his note: “It is when, not if, Saudi Arabia opens the oil taps.”

In the past, marked shifts in Saudi Arabia’s oil policy, in the mid-1980s and mid-2010s, led to declines in oil prices.

In a note last month, Capital Economics’ James Swanston, a Middle East and North Africa economist, had also said that the case for Saudi Arabia to ramp up oil output was strengthening. A ramp-up, he said, would result in some economic pain and require Crown Prince Mohammed bin Salman to reverse course on his approach to oil policy since coming to power, but it would “enable the Kingdom to recapture market share.”

For now, the current oil-market backdrop probably does not suggest that a big shift in oil policy is imminent, said Tompkins. Saudi Arabia’s current situation is “nowhere near as dire as it has been in the past,” he said. For example, the Saudis had cut oil production by 75% in the lead-up to their reversal on oil policy in the mid-1980s, but since September 2022, it has cut output by nearly 20% — suggesting that the Kingdom “isn’t in quite as concerning a position now.”

If Saudi Arabia did ramp up production to its capacity of 12.5 million barrels per day, from around 9 million bpd, it would require a sizeable fall in oil prices below $50 a barrel for its oil export revenues to be “markedly worse than they are today,” said Tompkins.

In Monday dealings, global benchmark Brent crude’s December contract BRN00 BRNZ24 traded at $77.60 a barrel on ICE Futures Europe, down $1.44, or 1.8%.

“All told, the risks to our view that Saudi Arabia open the spigots and ramps up output at some point have increased, perhaps to around a 30% chance by end-2025,” Tompkins said.

The OPEC+ meeting scheduled for Dec. 1 will be key. In September, OPEC+ agreed to extend voluntary production cuts by two months to the end of November and then gradually phase out the cuts on a monthly basis at the start of December.

“One of the lessons from 2014 and 2020 was that a breakdown of negotiations around these meetings led to Saudi shifting tack,” Tompkins said. “The December meeting could be a potential flashpoint.”

Most Read from MarketWatch

Bank First Announces Net Income for the Third Quarter of 2024

- Net income of $16.6 million and $48.0 million for the three and nine months ended September 30, 2024, respectively

- Earnings per common share of $1.65 and $4.75 for the three and nine months ended September 30, 2024, respectively

- Annualized return on average assets of 1.56% and 1.54% for the three and nine months ended September 30, 2024, respectively

- Quarterly cash dividend of $0.45 per share declared, an increase of 12.5% from the prior quarter and 50.0% from the prior-year third quarter

MANITOWOC, Wis., Oct. 15, 2024 /PRNewswire/ — Bank First Corporation BFC (“Bank First” or the “Bank”), the holding company for Bank First, N.A., reported net income of $16.6 million, or $1.65 per share, for the third quarter of 2024, compared with net income of $14.8 million, or $1.43 per share, for the prior-year third quarter. For the nine months ended September 30, 2024, Bank First earned $48.0 million, or $4.75 per share, compared to $39.6 million, or $3.89 per share for the same period in 2023. After removing the impact of one-time expenses related to acquisitions as well as gains and losses on sales of securities and other real estate owned (“OREO”), the Bank reported adjusted net income (non-GAAP) of $15.1 million, or $1.46 per share, for the third quarter of 2023. There were no such expenses during the third quarter of 2024. For the first nine months of 2024, adjusted net income (non-GAAP) totaled $47.4 million, or $4.69 per share, compared to $44.4 million, or $4.36 per share for the same period in 2023.

Operating Results

Net interest income (“NII”) during the third quarter of 2024 was $35.9 million, $2.9 million higher than the previous quarter and up $1.8 million from the third quarter of 2023. The impact of net accretion and amortization of purchase accounting related to interest-bearing assets and liabilities from past acquisitions (“purchase accounting”) increased NII by $1.7 million, or $0.13 per share after tax, during the third quarter of 2024, compared to $1.2 million, or $0.09 per share after tax, during the previous quarter and $1.8 million, or $0.13 per share after tax, during the third quarter of 2023. A previously purchased loan with remaining associated purchase accounting adjustments of $0.6 million was fully repaid before maturity during the third quarter of 2024, leading to the elevated impact of purchase accounting during the quarter.

Net interest margin (“NIM”) was 3.76% for the third quarter of 2024, compared to 3.63% for the previous quarter and 3.71% for the third quarter of 2023. NII from purchase accounting increased NIM by 0.17%, 0.13%, and 0.19% for each period, respectively. While the Bank continued to see average rates paid on interest-bearing deposits rise, the velocity of those increases slowed during the most recent quarter, with month-by-month results showing these rates at 2.66% in July, 2.71% in August, and 2.70% in September. Meanwhile, new loan originations and loan repricing from low rates over the last several years have allowed for continued improvement in the yield of the Bank’s loan portfolio, coming in at 5.73% during the most recent quarter compared to 5.51% during the prior quarter and 5.23% during the prior-year third quarter.

Bank First did not record a provision for credit losses during the third quarter of 2024, matching the previous quarter and third quarter of 2023. Provision expense was $0.2 million for the first nine months of 2024 compared to $4.2 million for the same period during 2023. The acquisition of the loan portfolio of Hometown Bancorp, Ltd. (“Hometown”) during the first quarter of 2023 resulted in a day one provision for credit losses expense of $3.6 million. Recoveries of previously charged-off loans exceeded currently charged-off loans by $0.5 million through the first nine months of 2024, compared to recoveries exceeding charge-offs by $0.1 million through the first nine months of 2023. Other than a $0.3 million charge-off during the third quarter of 2024, related to a single customer relationship, the Bank’s loan portfolio continues to exhibit very little credit stress. The Bank experienced a reduction in unfunded loan commitments during the most recent quarter, allowing it to move $0.4 million from its liability for potential credit losses in unfunded commitments to its allowance for credit losses in its loan portfolio. While this move did not impact on the Bank’s profitability for the quarter, it did increase the allowance for potential loan credit losses to correspond with the increase in overall loan portfolio balances during the quarter.

Noninterest income was $4.9 million for the third quarter of 2024, compared to $5.9 million and $5.3 million for the prior quarter and third quarter of 2023, respectively. Service charge income increased by $0.1 million, or 4.2%, and $0.4 million, or 20.2%, from the prior quarter and prior-year third quarter, respectively, as the Bank continues to benefit from the renegotiation of vendor incentive programs related to the Bank’s credit and debit card payments processing. Income provided by the Bank’s investment in Ansay & Associates, LLC (“Ansay”) increased by $0.3 million from the prior-year third quarter while declining $0.3 million from the prior quarter. Although income from Ansay has historically been less consistent than most areas of the Bank quarter-to-quarter, it has remained strong during 2024, increasing by $0.6 million, or 21.6%, through the first nine months of 2024 compared to the same period in 2023. Finally, the Bank experienced a negative $0.3 million valuation adjustment to its mortgage servicing rights asset during the third quarter of 2024 which compared unfavorably to positive valuation adjustments of $0.3 million and $0.2 million during the prior quarter and prior-year third quarter, respectively. Changes in the valuation of this asset historically correlate to changes in prevailing residential mortgage rates. Residential mortgage rates have ebbed and flowed during 2024, causing the valuation of this asset to be volatile through the first three quarters of the year.

Noninterest expense was $20.1 million for the third quarter of 2024, compared to $19.1 million during the prior quarter and $19.6 million during the third quarter of 2023. Most areas of noninterest expense have remained well-contained over the past five quarters as the Bank has worked efficiencies from recent acquisitions into its operations. The prior quarter included a $0.5 million gain on the sale of OREO which offset total noninterest expense, leading to some of the increase quarter-over-quarter. Beyond that, occupancy, equipment, and office expenses were elevated during the current quarter due to $0.2 million in losses on the disposal of equipment that needed to be upgraded. Finally, data processing contained $0.4 million in project-related expenses during the current quarter as part of the Bank’s continued upgrade of its online customer platform.

Balance Sheet

Total assets were $4.29 billion on September 30, 2024, a $72.7 million increase from December 31, 2023, and a $207.0 million increase from September 30, 2023.

Total loans were $3.47 billion on September 30, 2024, up $127.9 million from December 31, 2023, and up $115.4 million from September 30, 2023. Loans grew 4.9% on an annualized basis during the third quarter of 2024.

Total deposits, nearly all of which remain core deposits, were $3.48 billion on September 30, 2024, up $51.8 million from December 31, 2023, and up $86.4 million from September 30, 2023. Total deposits grew by 10.0% and noninterest-bearing deposits grew by 18.8% on an annualized basis during the third quarter of 2024.

Asset Quality

Nonperforming assets on September 30, 2024, remained negligible, totaling $11.9 million compared to $11.0 million and $5.2 million at the end of the prior quarter and third quarter of 2023, respectively. Nonperforming assets to total assets ended the third quarter of 2024 at 0.28%.

Capital Position

Stockholders’ equity totaled $628.9 million on September 30, 2024, an increase of $9.1 million from the end of 2023 and $51.6 million from September 30, 2023. Earnings of $48.0 million through the first nine months of 2024, offset by dividends totaling $11.1 million and repurchases of BFC common stock totaling $31.2 million during that period, were the primary factors leading to the increase in capital year-to-date. The Bank’s book value per common share totaled $62.82 on September 30, 2024, compared to $59.80 on December 31, 2023, and $55.62 on September 30, 2023. Tangible book value per common share (non-GAAP) totaled $43.07 on September 30, 2024 ,compared to $40.30 on December 31, 2023, and $36.00 on September 30, 2023.

Dividend Declaration

Bank First’s Board of Directors approved a quarterly cash dividend of $0.45 per common share, payable on January 6, 2025, to shareholders of record as of December 23, 2024. This dividend represents a 12.5% increase over the previous quarter’s dividend and a 50.0% increase over the dividend declared one year earlier.

For further information, contact:

Kevin M LeMahieu, Chief Financial Officer

Phone: (920) 652-3200 / klemahieu@bankfirst.com

![]() View original content:https://www.prnewswire.com/news-releases/bank-first-announces-net-income-for-the-third-quarter-of-2024-302276977.html

View original content:https://www.prnewswire.com/news-releases/bank-first-announces-net-income-for-the-third-quarter-of-2024-302276977.html

SOURCE Bank First Corporation

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Cathie Wood's Ark Offloads $1.28M In Jack Dorsey's Block Shares Despite Bitcoin Rally

On Tuesday, Cathie Wood-led Ark Invest made significant trades, most notably selling off shares of Block Inc. SQ.

The SQ Trade

Ark Invest sold 17,816 shares of the Jack Dorsey-headed Block Inc. from its ARKK fund. This move comes despite Block Inc.’s recent positive second-quarter results, which showcased growth in its Cash App and strategic innovations. The value of the trade, based on the closing price of $71.79 per share on Tuesday, is approximately $1.28 million.

Significantly, the sale of Block shares came on a day when Bitcoin BTC/USD moved up. The apex cryptocurrency has been on a tear this week. Dorsey has envisioned a transformative future for Block, moving beyond payments to focus on Bitcoin and the potential for building a new banking model. Recently, Block took a significant step into the crypto realm by securing its first major deal in crypto mining with Core Scientific, which J.P. Morgan estimates could generate between $225 million and $300 million. While Dorsey’s commitment to Bitcoin is evident, analysts remain cautious, emphasizing the need for solid profit margins to validate this ambitious direction

Other Key Trades:

- Ark Invest bought shares of Tempus AI Inc. The firm purchased 17,082 shares from its ARKG fund and 75,991 shares from its ARKK fund.

- Ark Invest bought shares of Blade Air Mobility Inc. (BLDE) from its ARKQ fund. The firm sold shares of Materialise NV (MTLS) from its ARKQ fund. Ark Invest bought 1,000 shares of Advanced Micro Devices Inc. AMD from its ARKX fund.

- Significantly, Ark also sold shares of COVID-19 vaccine maker Moderna Inc MRNA. The firm sold a total of 24,981 shares from ARKK and ARKG funds worth $1.4 million approximately.

Image via Shutterstock

Read Next:

This story was generated using Benzinga Neuro and edited by Shivdeep Dhaliwal

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Wearable Medical Devices Market to Soar to $151.8 Billion by 2029, Driven by a 27.5% CAGR from 2024

Boston, Oct. 15, 2024 (GLOBE NEWSWIRE) — “According to the latest BCC Research study, the demand for “Wearable Medical Devices: Technologies and Global Markets” is estimated to grow from $45.0 billion in 2024 to $151.8 billion by the end of 2029, at a compound annual growth rate (CAGR) of 27.5% from 2024 through 2029.”

The research report on the global market for wearable medical devices provides a comprehensive analysis segmented by product, application, and sales channel. Covering market estimations and trends through 2029, the report divides the market into North America, Europe, Asia-Pacific, and the Rest of the World (RoW), with 2023 as the base year for data and forecasts extending to 2029. It delves into major players, technologies, applications, and market dynamics, exploring geographic opportunities in detail. Analytical frameworks such as PESTEL analysis, ESG (Environmental, Social, and Governance) analysis, regulatory landscape, reimbursement scenarios, and competitive analysis are also featured, offering valuable insights for strategic planning by companies in the sector.

The following factors drive the global market for wearable medical devices:

Increasing Prevalence of Chronic Lifestyle Diseases: The global rise in chronic conditions like diabetes, hypertension, and cardiovascular diseases is a significant concern. Wearable devices have emerged as effective tools to monitor vital signs, track symptoms, and manage these chronic illnesses. The need for continuous health monitoring is driving the demand for wearable medical devices, providing individuals with the means to keep their conditions in check and potentially prevent complications.

Growing Population of Dependents: As the global population ages, there is an increasing demand for healthcare services. Wearable devices are instrumental in enabling remote patient monitoring, which allows caregivers to keep track of patient’s health without the need for frequent hospital visits. This technology is particularly beneficial for dependents, including the elderly and those with disabilities, offering them a better quality of life and more independence.

Rising Healthcare Expenditure: Both governments and individuals are investing more in healthcare, seeking cost-effective solutions for preventive care, early detection, and disease management. Wearable medical devices contribute to this by reducing the need for hospitalization and promoting better health outcomes. The cost savings associated with these devices are significant, making them an attractive option for managing healthcare expenditures.

Technological Advancements: The field of wearable devices has been transformed by innovations in sensor technology, miniaturization, and connectivity. Modern smartwatches, fitness trackers, and medical wearables offer accurate data collection, real-time alerts, and seamless smartphone integration. These technological advancements have driven the adoption of wearable devices, contributing to the market’s growth as more people recognize their benefits.

Corporate Wellness Programs and Incentives: Employers increasingly recognize the importance of employee health and well-being. Corporate wellness programs are designed to encourage healthier lifestyles among employees, and wearable devices play a crucial role in these initiatives. By promoting physical activity, stress management, and better sleep, wearable devices help improve overall employee health. Additionally, incentives such as insurance discounts further boost the adoption of wearable health technology, making these devices a key component of corporate wellness strategies.

Request a sample copy of the global market for wearable medical device reports.

Report Synopsis

| Report Metrics | Details |

| Base year considered | 2023 |

| Forecast Period considered | 2024-2029 |

| Base year market size | $35.6 Billion |

| Market Size Forecast | $151.8 Billion |

| Growth rate | CAGR of 27.5% from 2024 to 2029 |

| Segment Covered | By Product, Application, Sales Channel, and Region |

| Regions covered | North America, Europe, Asia-Pacific, and Rest of the World (RoW) |

| Countries covered | The U.S., Canada, Mexico, Germany, U.K., France, Italy, Spain, Japan, China, and India |

| Key Market Drivers |

|

Key Interesting Facts About the global market for wearable medical devices:

- 1 billion individuals use smart wearables daily.

- Over 7.5 billion people worldwide.

- 1 in 5 individuals uses a smartwatch or fitness tracker.

- 70% of wearable users show greater levels of physical activity.

The global market for wearable medical devices report includes in-depth data and analysis addressing the following important queries:

- What is the projected market size and growth rate?

- The global wearable medical devices market is valued at an estimated $45.0 billion in 2024. It is projected to reach $151.8 billion by 2029, at an estimated CAGR of 27.5% from 2024 to 2029.

- What are the key factors driving the growth of the market?

- Increasing prevalence of chronic lifestyle diseases.

- Growing population of dependents.

- Technological advancements.

- Rising demand for home healthcare and remote monitoring.

- Corporate wellness programs.

- What segments are covered in the market?

- The report will provide information on the wearable medical devices market and their growth projections in the coming years. Recent developments of companies operating in this market space have been covered. Information about technologies, applications, PESTEL analysis, reimbursement scenarios, and business strategies have been provided in the report. The report also identifies promising and emerging countries where the established players can expand their business.

- Which segment will dominate the market by the end of 2029 by application type?

- The health and fitness segment dominates the wearable medical devices market and will continue to do so by 2029.

- Which region has the highest market share?

- North America holds the highest share of the market.

Some of the Key Market Players Are:

- ABBOTT

- ACTIGRAPH LLC.

- DEXCOM INC.

- GE HEALTHCARE

- KONINKLIJKE PHILIPS N.V.

- MEDTRONIC

- MASIMO

- SENSORIA INC.

- TURINGSENSE INC.

- VITALCONNECT

- VIVALNK INC.

- VIVOSENSMEDICAL GMBH

- WAHOO FITNESS

- WHOOP

- YBRAIN INC.

- ZEPHYR (MEDTRONIC)

- ZOLL MEDICAL CORP.

Browse More Related Reports

3D Printing Medical Devices: Global Markets: This report provides an overview of the global 3D printing medical devices market and analyzes market trends. It features an updated review of the market, including a breakdown by product segments, technology, sales channel, and application. Using 2023 as the base year, the report offers estimated market data for the forecast period from 2024 to 2029. Geographical segments covered include North America (U.S., Canada, Mexico), Europe (U.K., Germany, France, Rest of Europe), Asia-Pacific (Mainland China, Japan, Australia, South Korea, Rest of Asia-Pacific), and the Rest of the World (South America, Middle East, Africa). The report also focuses on emerging technologies and the vendor landscape, concluding with profiles of the major players in the market. Notably, within the implants and prosthetics application segment, dental implants are not included, as they are categorized under the dental application segment.

Directly Purchase a copy of the report with BCC Research.

For further information or to make a purchase, please get in touch with info@bccresearch.com.

About BCC Research

BCC Research provides objective, unbiased measurement, and assessment of market opportunities with detailed market research reports. Our experienced industry analysts’ goal is to help you make informed business decisions, free of noise and hype.

Corporate HQ: 50 Milk St. Ste 16, Boston, MA 02109, USA Email: info@bccresearch.com, Phone: +1 781-489-7301 For media inquiries, email press@bccresearch.com or visit our media page for access to our market research library. Data and analysis extracted from this press release must be accompanied by a statement identifying BCC Research LLC as the source and publisher.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Nisun International Reports Financial Results for the First Half of 2024

Company Reports 52% Revenue Growth, Initiates $15 Million Share Buyback Program

SHANGHAI, Oct. 15, 2024 /PRNewswire/ — Nisun International Enterprise Development Group Co., Ltd. (“Nisun International” or the “Company”) NISN, a technology and industry driven integrated supply chain solutions provider, today announced its reviewed but unaudited financial results for the six months ended June 30, 2024.

First Half 2024 Financial Highlights:

- Total revenue increased by 52% to $192.5 million, compared to $126.9 million for the first half of 2023.

- Supply chain trading business revenue increased by 114% to $142.1 million, up from $66.2 million in the prior-year period, driven primarily by growth in the gold trading sector.

- Small and medium-sized enterprises (“SME”) financing services revenue declined by 16% to $48.5 million due to the challenging market conditions, but the Company is optimistic about the future growth as recent government stimulus measures in China begin to take effect.

- Supply chain financing solutions revenue decreased by 30% to $1.9 million, also impacted by market conditions, but is expected to recover alongside broader economic improvements.

- Net income was $10.3 million, compared to $11.4 million for the first half of 2023.

- Earnings per share were $2.61, compared to $2.87 in the prior-year period.

Operational Highlights:

- Cash Position: As of June 30, 2024, The Company’s cash and cash equivalents were $47.8 million, compared to $114.4 million at the end of 2023. This decline was primarily driven by an increase in advances to suppliers, a strategic investment expected to fund future growth in sales and earnings. Additionally, a decrease in accounts payable contributed to the cash reduction.

- Cost Control: Operating expenses decreased by 31% to $5.7 million, reflecting effective cost management and efficiency improvements. Selling expenses fell by 69% as the Company maintained existing sales channels without expanding into new ones, and general and administrative expenses were reduced by 14% due to enhanced cost controls.

- Buyback Program: Nisun International has approved a $15 million share buyback program, which underscores the Company’s confidence in its future growth and commitment to enhancing shareholder value. The program will begin as soon as the trading window opens in the coming days.

Management Commentary:

Mr. Xin Liu, Chief Executive Officer of Nisun International, commented:

“We are very pleased with our strong financial performance in the first half of 2024, marked by a significant 52% increase in total revenue. Our supply chain trading business continues to grow at an impressive rate, particularly in the gold trading sector, which underscores the effectiveness of our business model and technology-driven approach. While the challenging economic conditions impacted our SME financing services, we are beginning to see signs of a turnaround following the government’s recent stimulus measures, and we are optimistic about the future of this segment.

Looking ahead, we remain committed to enhancing operational efficiency and seeking new growth opportunities. We also believe our stock is significantly undervalued, which is why we are excited to announce a $15 million share buyback program. Our largest shareholder has already demonstrated confidence in our future by increasing their stake by approximately $1 million during the first half of the year. We are confident that our growth initiatives and the share repurchase program will create additional value for our shareholders in the near term and beyond.”

2024 Outlook:

Nisun International expects the momentum in its supply chain trading business to continue through the second half of 2024 and into 2025. With the Chinese government’s stimulus measures beginning to take effect, the Company anticipates a more favorable environment for its SME financing and supply chain financing solutions, positioning Nisun International for sustained growth in the coming periods.

Details of the conference call, including dial-in information, will be announced in the coming days.

About Nisun International Enterprise Development Group Co., Ltd

Nisun International Enterprise Development Group Co., Ltd. NISN is a technology-driven, integrated supply chain solutions provider focused on transforming the corporate finance industry. Leveraging its industry experience, Nisun International is dedicated to providing professional supply chain solutions to Chinese and foreign enterprises and financial institutions. Through its subsidiaries, Nisun International provides users with professional solutions for technology supply chain management, technology asset routing, and digital transformation of tech and finance institutions, enabling the industry to strengthen and grow. At the same time, Nisun International continues to deepen the field of industry segmentation through industrial and financial integration. Focusing on industry-finance linkages, Nisun International aims to serve the upstream and downstream of the industrial supply chain while also assisting with supply-side sub-sector reform. For more information, please visit http://ir.nisun-international.com/

Cautionary Note Regarding Forward-Looking Statements

This press release contains information about Nisun International ‘s view of its future expectations, plans and prospects that constitute forward-looking statements. Actual results may differ materially from historical results or those indicated by these forward-looking statements as a result of a variety of factors including, but not limited to, risks and uncertainties associated with its ability to raise additional funding, its ability to maintain and grow its business, variability of operating results, its ability to maintain and enhance its brand, its development and introduction of new products and services, the successful integration of acquired companies, technologies and assets into its portfolio of products and services, marketing and other business development initiatives, competition in the industry, general government regulation, economic conditions, dependence on key personnel, the ability to attract, hire and retain personnel who possess the technical skills and experience necessary to meet the requirements of its clients, and its ability to protect its intellectual property. Nisun encourages you to review other factors that may affect its future results in Nisun’s registration statement and in its other filings with the Securities and Exchange Commission. Nisun assumes no obligation to update or revise its forward-looking statements as a result of new information, future events or otherwise, except as expressly required by applicable law.

Contacts

Nisun International Enterprise Development Group Co., Ltd

Investor Relations

Tel: +86 (21) 2357-0055

Email: ir@cnisun.com

![]() View original content:https://www.prnewswire.com/news-releases/nisun-international-reports-financial-results-for-the-first-half-of-2024-302276120.html

View original content:https://www.prnewswire.com/news-releases/nisun-international-reports-financial-results-for-the-first-half-of-2024-302276120.html

SOURCE Nisun International Enterprise Development Group Co., Ltd

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Nvidia, Apple, And Microsoft In Race For $4 Trillion Market Cap: 'Stage Is Set For Tech Stocks For Another 20% Move Higher In 2025'

The tech industry is witnessing fierce competition among Apple Inc. AAPL, Microsoft Corp MSFT, and NVIDIA Corp NVDA as they vie to reach a $4 trillion market cap. This race is expected to intensify in the next 6-9 months.

What Happened: Wedbush Securities analyst Dan Ives has predicted that the three tech giants will be the frontrunners in the race to a $4 trillion market cap.

This race is expected to be a key factor in the tech industry’s future, with a potential 20% surge in tech stocks by 2025, driven by the AI revolution.

“We believe the stage is set for tech stocks for another 20% move higher in 2025 with this tech bull market led by the AI Revolution,” Ives wrote on social media platform X.

Why It Matters: The race to a $4 trillion market cap has been a topic of interest for some time. In July, Ives predicted that Nvidia, Apple, and Microsoft were on track to reach this milestone, driven by the accelerating AI revolution. This was followed by an analyst’s prediction in August that Apple’s historic upgrade cycle would push its valuation past $4 trillion.

These predictions come amid a turbulent period for the tech industry. On Tuesday, a technical error led to a premature disclosure of ASML Holding NV‘s ASML third-quarter earnings, causing a sharp decline in the company’s stock. This incident also contributed to a broader decline in tech stocks, with the NASDAQ and other large-cap indices experiencing losses.

Read Next:

Tesla Stock Tumbles After Underwhelming Robotaxi Presentation

Image Via Shutterstock

This story was generated using Benzinga Neuro and edited by Kaustubh Bagalkote

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

3 Stocks to Buy on the Real Estate Operations Industry's Recovery

The Zacks Real Estate Operations industry constituents are poised to gain from the increased adoption of outsourced real estate services and emerging trends. The easing of monetary policy in many large markets is expected to result in a decrease in borrowing costs, more availability of credit and drive economic growth, in turn fueling transaction activity. Companies like Newmark Group, Inc. NMRK, Kennedy-Wilson Holdings, Inc. KW and RE/MAX Holdings, Inc. RMAX are set to benefit from these positive trends.

However, the industry faces challenges such as macroeconomic uncertainty and geopolitical tensions. Customers remain focused on cost controls and for certain asset categories are delaying their decision-making with respect to leasing.

About the Industry

The Zacks Real Estate Operations industry comprises companies that provide leasing, property management, investment management, valuation, development services, facility management, project management, transaction and consulting services, among others. However, real estate investment trusts or REITs are excluded from this group. Economic trends and government policies impact the real estate market (global and regional), which determines the industry’s performance. Economic activity, employment growth, office-based employment, interest-rate levels, costs and availability of credit, tax and regulatory policies, and the geopolitical environment are the major factors shaping the real estate market’s fate. Also, pandemic-induced public health challenges and geopolitical issues have affected property sales and the leasing lines of businesses.

What’s Shaping the Real Estate Operations Industry’s Future?

Interest Rate Cut Provides Relief for Transaction-Based Business: The latest cut in the interest rates by the Federal Reserve and anticipations of future reductions are expected to drive transaction-based businesses in the United States. Along with the United States, the easing of monetary policy in many large markets is expected to result in a decrease in borrowing costs, more availability of credit, and drive economic growth. This is expected to help investors in better price discovery and consequently result in reduced transaction completion times. It is also expected to lead to a rise in the average deal size, thereby bolstering the industry’s near-term revenue prospects.

Outsourcing of Real Estate Needs to Remain Strong: Real estate occupiers, including corporations, public sector entities, healthcare providers, and those in finance, industry, life sciences and technology, are increasingly preferring to outsource their real estate needs. They are entrusting third-party real estate experts to enhance execution and efficiency. Organizations are seeking strategic advice to reimagine their workplaces and workstyles to foster culture, attract talent and improve performance. These developments are creating opportunities for participants in the real estate operations industry. Major players in the industry are leveraging this transition, securing new clients and expanding relationships with existing ones. Also, companies in this industry continue to prioritize investments in technology as it consistently improves efficiency, delivers client services and supports market share growth.

Certain Real Estate Categories’ Demand Hurt: The pandemic has significantly reshaped the use of commercial real estate. Also, economic uncertainty continues to affect real estate sales and leasing activities. While companies are promoting the return to office, this transition is gradual, which is hindering tenants’ confidence in long-term commitments. As such, pre-pandemic office occupancy levels are likely to remain elusive in the near or intermediate term. Amid a volatile environment and geopolitical issues, customers remain focused on cost controls and delaying their decision-making with respect to leasing. As such, industrial real estate demand remains subdued and this trend is expected to continue in the near term. Additionally, the pace of business-related travel and in-person interactions has not fully rebounded to pre-pandemic norms.

Zacks Industry Rank Indicates Bright Prospects

The Zacks Real Estate Operations industry is housed within the broader Zacks Finance sector. It carries a Zacks Industry Rank #104, which places it in the top 42% of more than 250 Zacks industries.

The group’s Zacks Industry Rank, which is the average of the Zacks Rank of all the member stocks, indicates robust near-term prospects. Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than two to one.

The industry’s positioning in the top 50% of the Zacks-ranked industries is a result of the upward earnings per share outlook for the constituent companies in aggregate. Looking at the aggregate earnings per share estimate revisions, it appears that of late, analysts are gaining confidence in this group’s growth potential. Over the past year, the industry’s earnings per share estimates for 2024 and 2025 have moved 46.8% and 37.2% north, respectively.

Before we present a few stocks that you may want to consider for your portfolio, let’s take a look at the industry’s recent stock-market performance and valuation picture.

Industry Outperforms the Sector & the S&P 500

The Zacks Real Estate Operations industry has outperformed the broader Zacks Finance sector and the S&P 500 composite over the past year.

The industry has advanced 40.8% during this period compared with the S&P 500’s growth of 32.5% and the broader Finance sector’s rise of 31.2%.

One-Year Price Performance

Industry’s Current Valuation

On the basis of the forward 12-month price-to-earnings, which is a commonly used multiple for valuing Real Estate Operations stocks, we see that the industry is currently trading at 17.06X compared with the S&P 500’s forward 12-month price-to-earnings (P/E) of 22.08X. The industry is trading above the Finance sector’s forward 12-month P/E of 16.66X. This is shown in the chart below.

Forward 12-Month Price-To-Earnings Ratio

Over the last five years, the industry has traded as high as 32.49X and as low as 11.45X, with a median of 17.26X.

3 Real Estate Operation Stocks to Bet On

RE/MAX Holdings: Headquartered in Denver, CO, it is a franchisor in the real estate industry. The company franchises real estate brokerages globally under the RE/MAX brand and mortgage brokerages within the United States under the Motto Mortgage brand. It also sells ancillary products and services, such as loan processing services, mainly to its Motto network.

RE/MAX is poised to benefit from its strategic growth initiatives. With its efforts to expand the mortgage business and its objective to maintain a strong liquidity position, RE/MAX is well-poised to ride the growth curve.

RE/MAX Holdings currently sports a Zacks Rank #1 (Strong Buy). The Zacks Consensus Estimate for the company’s 2024 earnings per share currently stands at $1.24. The stock has increased 20.8% in the past three months.

Newmark Group, Inc.: Headquartered in New York City, Newmark is a leading commercial real estate services company that is rapidly expanding its presence globally. Together with its subsidiaries, Newmark Group advises and provides services to large institutional investors, global corporations and other owners and occupiers of commercial real estate.

With investments in talent and technology, the company is expected to experience decent performance going forward. It is poised to benefit from the opportunities from the large and highly fragmented market, institutional investor demand for commercial real estate and from the favorable trend toward outsourcing of commercial real estate services.

Newmark carries a Zacks Rank of 2 (Buy) at present. The Zacks Consensus Estimate for the company’s 2024 EPS has remained unchanged at $1.15 over the past month. This also suggests 9.5% growth year over year. NMRK shares have gained 22.7% over the past three months.

Kennedy Wilson: Headquartered in Beverly Hills, CA, Kennedy Wilson is a global real estate investment company that invests in high-growth markets across the United States, the U.K. and Ireland. KW is engaged in the ownership, operation and investment in real estate on its own and through its investment management platform.

The company is expected to benefit from the continued growth of its investment management business and healthy demand for its high-quality multifamily and commercial portfolio.

Kennedy Wilson has a Zacks Rank of 2 at present. The Zacks Consensus Estimate for 2024 EPS has moved significantly upward over the past two months to $2.96. This suggests a notable increase year over year. The company’s shares have appreciated 32.1% in the past six months.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.