Shares of Trump's media firm sink to record low

By Chibuike Oguh

NEW YORK (Reuters) -Shares of Trump Media & Technology Group, which is majority-owned by former U.S. President Donald Trump, sank to record lows on Tuesday, following the Republican presidential candidate’s recent return to rival social media platform X.

Trump Media shares dropped to as low as $21.33, down more than 4%. The stock finished down 3.7% at $21.42, marking the eighth consecutive session of losses.

Trump’s dwindling lead in polls and election betting markets in recent weeks has also hit the stock, which has been seen by some retail traders as a bet on whether Trump would win a second term.

“I’ve always looked at Truth Social and DJT as a voting mechanism versus an investment mechanism,” said Lou Basenese, president and chief market strategist at MDB Capital in New York. “The valuation never made sense in relation to the fundamentals.”

The stock had reached an all-time high of $79.38 during their Nasdaq debut on March 26 following a merger with blank-check company Digital World Acquisition Corp.

Earlier this month, Trump Media – whose main asset is the Truth Social app – reported a quarterly loss of $16.4 million and revenue of just $837,000. The company has a market value of about $4.3 billion, down from over $8 billion earlier this year.

Trump is expected to be eligible to begin cashing out his nearly 60% stake – or 114.75 million shares – in his social media company when the insider lockup period expires next month.

“It’s always traded in line with his odds of winning or losing, and that’s what we’re seeing now that the race is tight and the probability of him winning has narrowed. And I think it’s hitting record lows also because you’re coming up against the insider lockup,” Basenese added.

Trump began posting on the X platform last week for the first time in nearly a year, coinciding with an interview with owner Elon Musk.

Trump in recent weeks has lost his sizeable lead in polls against Vice President Kamala Harris, the Democratic candidate.

With 78 days to go before the Nov. 5 vote, contracts for a Harris victory are trading at 56 cents, with a potential $1 payout, on the PredictIt politics betting platform.

Trump contracts are at 46 cents, down from as much as 69 cents in mid-July.

(Reporting by Chibuike Oguh in New York; Editing by Daniel Wallis)

Stock-Split Watch: 3 Artificial Intelligence (AI) Stocks That Look Ready to Split

The past few months have seen a bunch of artificial intelligence (AI)-related technology companies announce stock splits. In fact, of the five potential AI stock splits I wrote about back in May, four have already either executed or announced imminent splits.

Remember, a stock split doesn’t change the intrinsic value of a stock one iota. But it can open up the stock to more retail investors and/or employees who would like to buy shares in lower dollar amounts, and who don’t have access to fractional share buying.

With stock-split fever in the air and the Nasdaq recovering from its late-July slump, even more AI-related stocks are seeing their share prices soar. With a high share price and the likelihood of more AI-fueled growth ahead, these three are the next candidates to split their stock in the near to medium term.

Meta Platforms

One might not think of Meta Platforms (NASDAQ: META) as an AI leader, but don’t underestimate CEO Mark Zuckerberg and his management team: Meta actually has the potential to beat current market leaders such as OpenAI and others at their own game.

Meta obviously has the financial resources to invest in leading AI infrastructure, but its competitive advantage may be in Zuckerberg’s decision to open-source the company’s Llama model code. Open source essentially means giving away the code for free, but that allows outside developers to optimize and make improvements to the underlying model. That decision has the potential to increase Llama’s innovation faster than closed-source competitors like OpenAI or the models coming from other “Magnificent Seven” stocks.

Meta can afford to do this because selling direct access to its AI large language model isn’t its core business. Rather, its core social media platforms all benefit from the increased potency of AI, which has shown the ability to increase user engagement and better target ads, which leads to more revenue per ad.

That was on display in the second quarter. Despite Meta’s already enormous size, the company was able to grow daily active people by 7%, while increasing revenue by 22% and operating income by a whopping 58%.

Of course, one day, Llama should become a revenue generator, as Zuckerberg has identified potential future use cases, such as agents automating a lot of tasks for creators, inserting ads into AI interactions, or potentially directly charging for higher, more advanced levels of AI modeling and compute. But for now, Meta can afford to take its time and develop those services.

Meta is currently the only Magnificent Seven stock to have never split its stock. But with its share price already north of $525 per share and a very reasonable valuation at 26 times earnings, it’s not far-fetched that a stock split may be in the near future. After all, this year has already seen another first for Meta, as the company initiated a dividend for the first time back in February.

KLA Corporation

KLA Corporation (NASDAQ: KLAC) has seen its stock surge in anticipation of an artificial intelligence investment boom. As the dominant player in process control equipment, which helps chipmakers check chip wafers for defects at multiple steps of the chipmaking process, KLA seems set for growth as leading-edge AI chips and memory become more and more complex.

KLA has a dominant market share in the metrology and inspection end market, with its share as high as 55% in some verticals. That market dominance of a crucial semiconductor process enables high margins and free cash flow, with the company’s operating margin coming in at a whopping 41% last quarter.

KLA’s killer combination of growth and profitability is the reason it has raised its dividend at a 15% annualized rate since 2006. And it’s also why the stock price has surged to $820 per share, making it ripe for a stock split.

Semiconductor capital equipment peer Lam Research announced it would be splitting its stock back in May, to take effect in October, and its shares trade around the same price as KLA’s today. Like KLA, Lam dominates a certain part of the chipmaking process, but a different step in etch and deposition. So, these two aren’t really competitors, but they have similar high profit margins due to a lack of competition. Given their similar characteristics and the chip industry seemingly on the brink of an upturn, it’s not unthinkable KLA Corporation may announce a split sometime soon.

Arista Networks

At $350 per share, Arista Networks (NYSE: ANET) may not undergo a 10-for-1 stock split like some of its tech peers have recently done, but it could split 2 or 3 for 1.

Arista was a disruptive company at the advent of the cloud computing age. Its new-age networking switch architecture fashioned data center switches out of best-of-breed merchant third-party hardware, lowering internal costs. Arista’s EOS software is what ties it all together, enabling high performance, system intelligence, and lightning-fast speeds at lower costs than traditional switches.

Arista’s software focus and huge scale affords it very high margins. Last quarter, Arista’s revenue grew 15.9%, and its operating margin reached over 41% over the past 12 months, with an admirable return on equity of 34.5%. Those are top-tier levels of profitability and solid growth.

Artificial intelligence needs efficient switching and routing as traditional data centers do, but on a bigger and more complex scale. So Arista is a natural beneficiary of the theme. But earlier this year, some may have grown concerned that in-house networking solutions from Nvidia, based on Infiniband technology, might become a competitive threat.

But Ethernet-based Arista seems to have put that to bed with recent results. In fact, Arista even unveiled a new holistic AI data center solution in collaboration with Nvidia on its recent earnings release, showing that the leading AI chipmaker still values collaboration with Arista and its leading ethernet-based solutions.

Look for Arista to continue to innovate its EOS software and switching architecture for super-large AI clusters. With a bright future, expect Arista to continue riding the AI wave higher, and for a potential eventual stock split.

Should you invest $1,000 in Meta Platforms right now?

Before you buy stock in Meta Platforms, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Meta Platforms wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $796,586!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Billy Duberstein and/or his clients have positions in KLA, Lam Research, and Meta Platforms. The Motley Fool has positions in and recommends Arista Networks, Lam Research, Meta Platforms, and Nvidia. The Motley Fool has a disclosure policy.

Stock-Split Watch: 3 Artificial Intelligence (AI) Stocks That Look Ready to Split was originally published by The Motley Fool

Here Are All 45 Stocks Warren Buffett Holds for Berkshire Hathaway's $314 Billion Portfolio

Although most investors were laser-focused on the release of the July inflation report last week, they may have missed what could be described as the most insightful data dump of the third quarter.

On Aug. 14, institutional investors with at least $100 million in assets under management were required to file Form 13F with the Securities and Exchange Commission. A 13F is the filing that alerts investors to the stocks, exchange-traded funds, and (occasionally) options that Wall Street’s smartest money managers bought and sold in the latest quarter (in this instance, the June-ended quarter).

No asset manager garners more attention on Wall Street than Berkshire Hathaway‘s (NYSE: BRK.A)(NYSE: BRK.B) billionaire CEO Warren Buffett. That’s because Buffett has overseen an increase in his company’s Class A shares (BRK.A) of more than 5,387,000% since becoming CEO in 1965. When you run circles around Wall Street’s major stock indexes, investors of all walks will want to ride your coattails.

According to Berkshire’s newest 13F, the appropriately named “Oracle of Omaha” and his investment lieutenants, Todd Combs and Ted Weschler, are overseeing a 45-stock portfolio spread across $314 billion of invested assets. Make note that this figure excludes the two index funds Berkshire currently holds small stakes in — the Vanguard S&P 500 ETF and SPDR S&P 500 ETF Trust — because index funds are comprised of baskets of securities and aren’t themselves stocks.

Here’s a thorough breakdown of Warren Buffett’s portfolio at Berkshire Hathaway.

Buffett’s portfolio is highly concentrated in eight core investments

At quick glance, you’d assume Buffett, Combs, and Weschler were well diversified, given that their company has $314 billion spread out across 45 stocks — but you’d be sorely mistaken. In reality, more than 79% of Berkshire’s invested assets can be traced back to eight core holdings.

-

Apple (NASDAQ: AAPL): $90,420,000,000 in market value (as of Aug. 16)

-

American Express: $38,161,929,297

-

Bank of America (NYSE: BAC): $37,075,191,558

-

Coca-Cola: $27,672,000,000

-

Chevron (NYSE: CVX): $17,467,773,342

-

Occidental Petroleum (NYSE: OXY): $14,706,768,598

-

Moody’s: $11,513,878,788

-

Kraft Heinz: $11,273,477,399

Despite Berkshire’s team being big net-sellers of equities over the last seven quarters, these eight investments make crystal clear that Buffett prefers to have an outsized percentage of his company’s capital put to work in his best ideas.

Perhaps the biggest surprise here is energy stocks accounting for a double-digit percentage of invested assets. Buffett has overseen the purchase of more than 255.2 million shares of Occidental Petroleum since the start of 2022 and also holds around 118.6 million shares of Chevron.

Historically, energy stocks haven’t played a key role in Buffett’s portfolio. But in the wake of the COVID-19 pandemic, multiple years of capital underinvestment by global energy majors (including Chevron) has led to tight global oil supply. When the supply of an in-demand commodity is constrained, this often means its spot price receives a boost. Occidental Petroleum, in particular, generates the bulk of its revenue from its drilling segment, and would be a prime beneficiary of a sustainably higher spot price for crude oil.

It is worth noting that Buffett and his crew have sold well over 500 million shares of their top holding, Apple, since Oct. 1, 2023, and they recently dumped north of $3.8 billion worth of Bank of America stock over 12 consecutive trading sessions (July 17 – Aug. 1).

Though it’s highly unlikely Buffett has lost faith in the management teams of either company, Berkshire is sitting on mammoth unrealized gains in Apple and Bank of America. With the stock market at historically pricey levels, and Buffett opining during his company’s annual shareholder meeting in May that he believes corporate tax rates will climb, locking in some gains makes perfect sense.

The Oracle of Omaha has 20 additional billion-dollar wagers

Even though the lion’s share of Berkshire Hathaway’s invested assets can be traced back to the aforementioned eight brand-name companies, it doesn’t mean there aren’t sizable wagers elsewhere. As of the closing bell on Aug. 16, there were 20 holdings that ranged in value between $1.2 billion and $7.4 billion.

-

Chubb (NYSE: CB): $7,391,306,883

-

Mitsubishi (OTC: MSBHF)(OTC: MTSU.Y): $7,357,559,195

-

Itochu (OTC: ITOCY)(OTC: ITOCF): $5,744,464,819

-

DaVita: $5,425,164,171

-

Mitsui (OTC: MITSY)(OTC: MITSF): $5,390,943,959

-

Citigroup: $3,392,030,536

-

Kroger: $2,659,500,000

-

Marubeni (OTC: MARUY): $2,416,778,056

-

Sumitomo (OTC: SSUM.Y)(OTC: SSUM.F): $2,388,438,078

-

VeriSign: $2,305,016,154

-

Visa: $2,218,574,855

-

Mastercard: $1,869,259,514

-

Amazon: $1,770,600,000

-

BYD: $1,550,124,061

-

Liberty Sirius XM Group Series C (NASDAQ: LSXMK): $1,540,063,734

-

Nu Holdings: $1,509,303,667

-

Capital One Financial: $1,370,346,897

-

Aon: $1,361,405,000

-

Charter Communications: $1,352,803,145

-

Ally Financial: $1,218,870,000

One of the interesting quirks about Buffett’s “other” billion-dollar investments is that this section contains five of the eight companies he described as “indefinite” holdings in his most recent annual letter to shareholders.

Aside from longtime holdings Coca-Cola and American Express, as well as Occidental Petroleum, Buffett listed the five Japanese trading houses (Mitsubishi, Itochu, Mitsui, Marubeni, and Sumitomo) as forever-type holdings for his company. The only reason Buffett hasn’t purchased an even larger stake in these businesses is because he has to keep Berkshire Hathaway’s stake in all five companies below 10%.

The “why?” behind Mitsubishi, Itochu, Mitsui, Marubeni, and Sumitomo has everything to do with these companies being cyclical and cheap. The Oracle of Omaha is a big fan of diversified companies able to take advantage of long-winded periods of economic expansion. When those businesses have single-digit price-to-earnings ratios, hearty capital-return programs, and CEOs with reasonably low compensation packages, Buffett tends to be a happy camper.

There’s also a sizable presence of financial stocks among Buffett’s billion-dollar ventures. It’s here we find insurer Chubb, which was the confidential stock Berkshire’s brightest minds began building a position in last summer. Insurers typically possess strong premium pricing power, and they’ve notably benefited from higher net interest income on their float (i.e., premium collected that hasn’t been paid out via claims) over the last two years.

Warren Buffett’s smaller holdings

To round things out, the roughly $314 billion portfolio overseen by Buffett, Combs, and Weschler also has 17 “smaller” holdings, ranging in market value from a little over $9 million to as much as $918 million.

-

T-Mobile: $918,328,320

-

Liberty Sirius XM Group Series A (NASDAQ: LSXMA): $774,712,462

-

Liberty Formula One Series C: $594,705,952

-

Louisiana-Pacific: $561,167,725

-

Liberty Live Series C: $430,810,903

-

Floor & Décor: $418,352,588

-

Sirius XM Holdings (NASDAQ: SIRI): $398,634,639

-

Ulta Beauty (NASDAQ: ULTA): $260,328,686

-

HEICO Class A: $195,471,660

-

Liberty Live Series A: $192,282,833

-

NVR: $96,329,150

-

Diageo: $29,293,205

-

Liberty Latin America Series A: $25,650,222

-

Jefferies Financial Group: $24,946,927

-

Lennar Class B: $24,352,017

-

Liberty Latin America Series C: $12,570,556

-

Atlanta Braves Holdings Series C: $9,370,726

If there’s a prevailing theme to these sub-$1 billion wagers, it’s that these companies were likely purchased, and/or are actively overseen, by Combs and Weschler.

For instance, Wall Street has been crowing about Berkshire’s purchase of more than 690,000 shares of Ulta Beauty following the release of Berkshire’s second-quarter 13F. While Ulta’s chain of cosmetics stores have been a popular launch point for a number of beauty products, cosmetics are well outside the realm of where Buffett focuses his research. This makes it highly likely that Combs and/or Weschler is behind this trade.

You can also see a potential arbitrage opportunity at play among these smaller holdings. In particular, Berkshire’s stake in Sirius XM Holdings has more than tripled over the last three months. By the end of September, Sirius XM is expected to complete its merger with Liberty Media’s Sirius XM tracking stock, Liberty Sirius XM Group, to create a single class of shares. Sirius XM will also conduct a 1-for-10 reverse split upon consummation of the merger.

Differences in price between Sirius XM and Liberty Sirius XM Group may be opening the door for Buffett and his investing lieutenants to take advantage.

Should you invest $1,000 in Berkshire Hathaway right now?

Before you buy stock in Berkshire Hathaway, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Berkshire Hathaway wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $796,586!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Bank of America is an advertising partner of The Ascent, a Motley Fool company. American Express is an advertising partner of The Ascent, a Motley Fool company. Ally is an advertising partner of The Ascent, a Motley Fool company. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Citigroup is an advertising partner of The Ascent, a Motley Fool company. Sean Williams has positions in Amazon, Bank of America, Mastercard, Sirius XM, and Visa. The Motley Fool has positions in and recommends Amazon, Apple, BYD Company, Bank of America, Berkshire Hathaway, Chevron, Jefferies Financial Group, Lennar, Mastercard, Moody’s, NVR, Ulta Beauty, Vanguard S&P 500 ETF, VeriSign, and Visa. The Motley Fool recommends Diageo Plc, Heico, Kraft Heinz, Kroger, Nu Holdings, Occidental Petroleum, and T-Mobile US and recommends the following options: long January 2025 $370 calls on Mastercard and short January 2025 $380 calls on Mastercard. The Motley Fool has a disclosure policy.

Here Are All 45 Stocks Warren Buffett Holds for Berkshire Hathaway’s $314 Billion Portfolio was originally published by The Motley Fool

Subway’s $5 footlong is now the $15 footlong. Customers want the old deal back.

It’s been years since Subway offered a $5 footlong sandwich, a deal celebrated with an ear-catching jingle. Now, the sandwiches can cost up to $15.

And the chain’s regular customers are none too happy about the inflationary state of affairs.

Most Read from MarketWatch

“People too broke for $15 subs,” one Reddit user said.

“I made my own sandwich last night. I calculated it cost me ~$3-$4 worth of ingredients.” another Reddit user noted.

The discussion about Subway’s pricing has been a hot topic of late, especially since news broke that the chain was reportedly having a large-scale meeting with North American franchisees about ways to boost business.

Naturally, customers want to see a return to the good ol’ days of those $5 footlongs and say that’s the best path forward to win their business. “It’s that easy,” another Reddit user said.

The $5 deal ended in 2014, and Subway’s footlongs currently range from around $8 to $15, though prices vary by location. A sandwich combo meal with chips and a drink adds a few dollars to the tab. Extras like more meat and cheese also increase the price.

Admittedly, few fast-food industry watchers predict the $5 deal will ever return. But Subway franchisees told MarketWatch that bargain offerings are still important sales boosters.

“Promotions can only help us increase traffic,” said Monica Laldin, a Subway franchisee in Georgia with seven locations.

Subway does have offers that bring down the cost of a sandwich below the $10 mark, such as a current buy-one-footlong-get-one-free deal. But the chain — which generates around $10 billion in annual sales, and was purchased last year by Roark Capital in a reported $9.6 billion transaction — faces pushback from some franchisees because the offers can cut into profits.

Subway is far from the only fast-food chain dealing with a difficult financial environment, driven in recent years by higher food and labor costs. As chains have increased prices to counter these developments, inflation-weary customers have voiced their displeasure and have often opted not to frequent establishments as much.

McDonald’s MCD has become something of a focal point in this regard, especially when word spread of one location charging nearly $18 for a Big Mac meal. In a recent letter to customers, McDonald’s U.S. President Joe Erlinger indicated that was more the exception than the rule, though he did note that the price for a Big Mac has risen 21% since 2019.

“Inflationary pressures have affected all sectors of the economy, including ours,” Erlinger said.

To woo customers back, fast-food chains have begun offering a wave of deals and discounts, as exemplified by the McDonald’s $5 value meal — which includes a McDouble cheeseburger or McChicken sandwich, a four-piece order of Chicken McNuggets, a small order of french fries and a small soft drink. All items on the McDonald’s $5 meal deal used to be on its dollar menu, which no longer exists.

A Subway spokesperson told MarketWatch that it’s indeed “challenging times for the entire restaurant industry. Our approach to value is thoughtful and strategic, based on data to help balance consumer needs while protecting franchisee profits.”

In some ways, Subway was a victim of its own success with the triumph of the $5 footlong deal and its accompanying jingle, industry experts say. It cemented the idea of the chain as a low-cost leader and arguably left it with less wiggle room to raise prices without facing consumer backlash.

Plus, as Arlene Spiegel, a New York-based hospitality consultant, argues, consumers can find top-of-the-line sandwich options at those higher price levels, so why should they opt for a chain sub that could cost as much as $15?

“Not when you can go to a mom-and-pop Italian deli and get a sandwich with freshly sliced prosciutto,” Spiegel said.

Adding to Subway’s woes: One of its other major marketing campaigns promoted the low-calorie aspect of some of its offerings and spotlighted Jared Fogle, who reportedly lost 245 pounds on a diet of Subway sandwiches. But Fogle later pled guilty in a child sex-abuse case, which damaged the Subway brand, experts say.

“There are still people who won’t go because of the Jared fiasco,” said Mark Kalinowski, a veteran fast-food industry analyst.

Add it all up and Kalinowski said it should come as no surprise that Subway has seen its U.S. store count drop considerably, from 27,129 in 2015 to 20,133 last year. Yet Kalinowski remains relatively bullish about Subway, even with the growing competition it faces from other sandwich chains.

The bottom line: Plenty of people still like their Subway footlongs regardless of how much they cost, he said: “Subway will be around for decades to come.”

Most Read from MarketWatch

Should You Buy Chevron While It's Below $150?

Chevron (NYSE: CVX) has a lot going for it as an energy investment, not least of which is the dividend, which has been increased annually for 37 consecutive years and supports a lofty 4.4% dividend yield at present. With the stock more than 20% below its most recent highs, should you buy Chevron? Here are some important factors to consider before making the final call.

What does Chevron do in the energy industry?

The headline is actually a trick question because Chevron pretty much does everything, which is why it is classified as an integrated energy company. But to be more specific, it has operations in the upstream segment (energy production), the midstream arena (pipelines and other transportation and storage infrastructure), and the downstream niche (chemicals and refining). Each segment of the broader energy sector operates a little differently and has different market dynamics.

Putting upstream, midstream, and downstream businesses all under one roof not only creates a diversified company, which is further enhanced by Chevron’s global reach, but tends to help soften the ups and downs of the energy cycle. Commodity prices are the main driver of Chevron’s top and bottom lines, but the inherent swings won’t be quite as material as they would be if it were solely focused on the upstream.

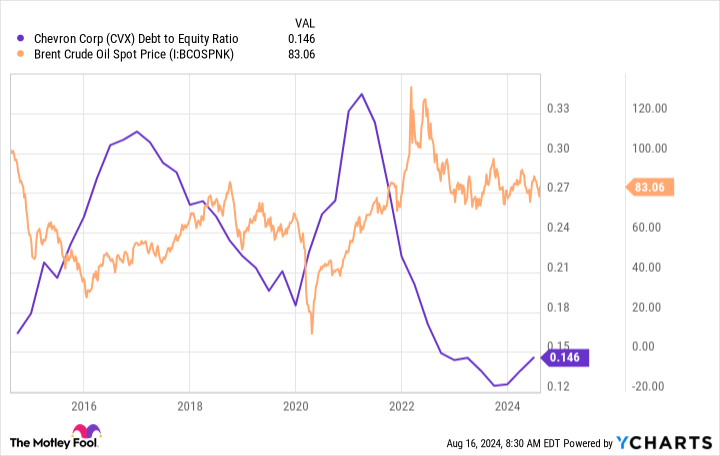

Chevron is also keenly focused on the strength of its balance sheet. To put a number on that, Chevron’s debt-to-equity ratio is a minuscule 0.15 today. That would be a low number for any company, but it also happens to be the lowest figure relative to Chevron’s closest peers. This gives Chevron more leeway to take on leverage to support its business and dividend during the inevitable oil downturns it will face. Simply put, Chevron is a conservative way to invest in the energy sector.

Is Chevron a buy under $150?

Chevron’s stock is under $150 today, which represents a roughly 20% decline from the recent price peak of roughly $188 per share in late 2022. That could be seen as a solid entry point for dividend investors who want to add energy exposure to their portfolios, noting the stock’s attractive 4.4% yield. After all, the S&P 500 index is only yielding around 1.2% or so, and the average energy stock, using Energy Select Sector SPDR ETF as a proxy, is yielding about 3.1%.

Now add in Chevron’s strong financial position, diversified business, and long history of weathering energy downturns while continuing to reward investors with regular dividend increases. You can see where a conservative type would be making a wise choice to buy the stock if they are looking for an energy investment right now.

But there’s one problem: Oil prices are actually fairly high right now. Sure, they’ve been higher, but they’ve also been a lot lower. Given the nature of the oil industry, it is highly likely that Chevron will have to deal with materially lower energy prices at some point in the not-too-distant future.

Chevron is ready, noting its very low debt-to-equity ratio, but that won’t change the fact that revenue and earnings fall when energy prices decline. That, in turn, will lead investors to sell the stock.

In fact, over the past decade, Chevron’s stock has dipped below $80 a share three times. The dividend yield, meanwhile, has risen as high as 9% at one point. That was an extreme peak related to the coronavirus pandemic. But 6% isn’t out of bounds, having been reached three times as well.

It wouldn’t be at all shocking to see a deep oil downturn that leads to a deep drawdown in Chevron’s stock and pushes the yield up to materially more attractive levels. Or to put it another way, if you are looking to buy Chevron at a bargain price, you’ll want to wait until the next big oil sell-off.

Chevron is a good company

Here’s the thing: For long-term investors with an income focus, Chevron is probably a good choice right now. You won’t be getting the best possible price, but you are probably buying it at a fair level if you add the stock below $150.

However, if you are willing to watch and wait, you can probably buy it at a much better price at some point in the future, given the inherent volatility of the energy sector. The one caveat here is that you should get to know the company today and create a concrete plan for when you want to buy it (perhaps when the yield hits 6%).

Indeed, the best time to buy Chevron is likely to be when the fear of owning it seems highest, and if you don’t plan ahead, fear might lead you to miss the opportunity.

Should you invest $1,000 in Chevron right now?

Before you buy stock in Chevron, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Chevron wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $779,735!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chevron. The Motley Fool has a disclosure policy.

Should You Buy Chevron While It’s Below $150? was originally published by The Motley Fool

TD Takes $2.6 Billion Hit on US Probe, Sells Schwab Shares

(Bloomberg) — Toronto-Dominion Bank is setting aside $2.6 billion to cover fines it expects to pay for failures in its money-laundering controls, and the company sold part of its stake in Charles Schwab Corp. to fund it.

Most Read from Bloomberg

Including a $450 million provision announced in April, the lender now estimates it will pay $3 billion related to its US compliance lapses.

“The bank expects that a global resolution will be finalized by calendar year-end,” Toronto-Dominion said in a statement after markets closed Wednesday.

Canada’s second-biggest bank said its ownership interest in Schwab will fall to 10.1% from 12.3% after selling 40.5 million shares of the discount broker. Toronto-Dominion acquired that stake in 2020 as part of a transaction to sell its interest in online brokerage TD Ameritrade Holding Corp. to Schwab.

The shares were being marketed at $61.35 to $62.65 each, according to terms of the deal seen by Bloomberg News. The range represents a potential discount of as much as 5% to Wednesday’s closing price of $64.57 apiece, Bloomberg calculations show.

Analysts and investors had speculated that Toronto-Dominion could sell some or all of its interest in Schwab to help cover the financial penalties it’s facing in the criminal and regulatory money-laundering matters.

“We recognize the seriousness of our US AML program deficiencies,” Chief Executive Officer Bharat Masrani said in the statement, adding, “The work required to meet our obligations and responsibilities is of paramount importance to me, our senior leaders, and our boards.”

Bribe Allegations

Last year, Toronto-Dominion’s landmark $13.4 billion deal to acquire First Horizon Corp. collapsed, with the Canadian lender saying it was unclear regulators would ever approve the deal. Soon after, TD acknowledged that it was receiving inquiries from the US Department of Justice, in addition to financial regulators and the Treasury Department.

The core allegations are that it failed to catch money laundering and other financial crimes at several US branches where customer-facing employees took bribes to help move money. So far, federal prosecutors in New Jersey have filed at least four cases alleging serious misconduct by branch employees in New York, New Jersey and Florida. The bank has said it fired about a dozen front-line workers for code-of-conduct breaches.

TD also replaced about 10 senior leaders in compliance and legal roles in the wake of the money-laundering allegations. But Masrani, who has been CEO for almost a decade, remains in his post despite swirling speculation that the board could look to replace him.

On top of fines, analysts have suggested the bank could also face years of restrictions on either organic growth or acquisitions in the US, where it has built a significant retail business. It has more than 10 million clients in the country and a network of almost 1,200 branches along the US east coast.

“While the market now has certainty surrounding the amount of the charge, this is offset by the fact that it is larger than expectations and the impact this has on capital,” Jefferies Financial Group Inc. analyst John Aiken said in a note to clients. “The valuation impact will hinge on tomorrow’s earnings, but it is already behind the eight-ball.”

Toronto-Dominion said the provision, which will be reflected in its fiscal third-quarter report on Thursday, will reduce its common equity tier 1 ratio to 12.%. That’s still above the 11% minimum ratio of capital to risk-weighted assets required by Canada’s bank regulator.

TD said the provision will further dent its CET1 ratio by 35 basis points in the fiscal fourth quarter, but that the Schwab sale will increase the ratio by 54 basis points in the period.

“The big question remains: What could the non-monetary penalties be? Hard to tell at this point in time,” Desjardins Capital Markets analyst Doug Young said in a report. “And we highly doubt that management will comment on this right now.”

–With assistance from Bre Bradham.

(Updates with compliance costs in second paragraph, analyst’s comment in third-to-last.)

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Why Evoke Pharma (EVOK) Stock Is Volatile

Evoke Pharma Inc EVOK shares ended Tuesday down 16.40% to 42 cents after the company announced a 1-for-12 reverse stock split of its common stock, set to take effect at 12:01 a.m. ET on August 1, 2024. After-hours trading has it up 12.44% at 47 cents.

The reverse stock split means that every 12 shares of the company’s existing common stock will be consolidated into one share. The stock will trade on a split-adjusted basis on NASDAQ under the same symbol, EVOK, starting Aug. 1.

This reverse split, approved by shareholders at the 2024 annual meeting, will not change the par value or the authorized number of shares. Fractional shares will not be issued; instead, shareholders will receive a cash payment for any fractional shares.

Should I Buy, Hold or Sell My EVOK Stock?

When deciding to buy, hold or sell a stock, investors should consider their time horizon, unrealized gains and total return.

Shares of Evoke Pharma have decreased by 75.13% in the past year. An investor who bought shares of Evoke Pharma at the beginning of the year would take a loss of $0.64 per share if they sold it today. The stock has fallen 16.7% over the past month, meaning an investor who bought shares on Jun. 1 would see a capital loss of $0.11.

Investors may also consider market dynamics. The Relative Strength Index can be used to indicate whether a stock is overbought or oversold. Evoke Pharma stock currently has an RSI of 28.29, indicating oversold conditions.

For access to advanced charting and analysis tools and stock data, check out Benzinga PRO. Try it for free.

EVOK has a 52-week high of $1.67 and a 52-week low of 36 cents.

Read Next:

Market News and Data brought to you by Benzinga APIs

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Who is Jonathan Bloomer, Morgan Stanley’s chairman who is presumed dead in the Bayesian yacht disaster?

Morgan Stanley International chairman Jonathan Bloomer is among the missing after a tornado struck a luxury yacht off the coast of Sicily on Monday. Billionaire tech entrepreneur Mike Lynch, dubbed the “British Bill Gates,” as well as his daughter and three others, is also missing and presumed dead.

The disaster came weeks after Lynch was acquitted in the U.S. of fraud charges. Bloomer—who has served as Morgan Stanley’s chair for almost eight years and is also the chair of insurance group Hiscox, according to his LinkedIn profile—played a small role in the trial.

Lynch, 59, founded software company Autonomy in 1996 and sold it to Hewlett-Packard in 2011 for $11 billion. HP paid a 60% premium over Autonomy’s stock price, but just one year after the blockbuster deal, HP reported an $8.8 billion write-down, attributing over $5 billion of that to inflated revenue data from Autonomy. Lynch was charged with 16 counts of conspiracy and fraud, with one fraud charge later dismissed. In June, Lynch was acquitted of fraud and cleared of charges.

Bloomer, 70, served on Autonomy’s audit committee and as a non-executive on the company’s board in 2010. He also testified during Lynch’s trial, telling the court in May that Lynch was “more interested in the strategy, new products, new areas to look at, potential acquisitions,” rather than looking at the financial side of the company.

The trip aboard the Bayesian was a celebration following the decades-long trial, but Bloomer and Lynch were declared missing after high winds and a vortex of water struck and capsized the superyacht. There were 22 passengers aboard the 180-foot sailing yacht, 15 of whom were rescued, and one who was declared dead. Italian emergency services brought Lynch’s wife, Angela Bacares, who owned the yacht, to safety. Bloomer’s wife remains missing.

The Bayesian yacht accident has odd timing: It coincided with the death of Lynch’s co-defendant Stephen Chamberlain, who died after being hit by a car in Cambridgeshire, England, on Saturday.

“We are deeply shocked and saddened by this tragic event,” Hiscox CEO Aki Hussain said in a statement. “Our thoughts are with all those affected, in particular our chair, Jonathan Bloomer, and his wife Judy, who are among the missing, and with their family as they await further news from this terrible situation.”

Hiscox senior independent director Colin Keogh will serve as interim chair, the company told Fortune. Morgan Stanley did not respond to Fortune’s request for comment.

Bloomer’s tumultuous career

Prior to his tenure at Morgan Stanley and Hiscox, Bloomer was the CEO of insurance company Prudential Financial; he was ousted in 2005. The timing of Bloomer’s rising up the ranks was ill-timed, coinciding with the dotcom crash and 9/11, which sent Prudential’s share prices plummeting 40%.

During that time, Bloomer proposed buying U.S. insurer American General, a move that was largely doomed thanks to American International Group’s bid for the company that topped Prudential’s, as well as lack of investor confidence in the acquisition that sent Prudential’s shares tanking. Bloomer had to backtrack on the move, but through the takeover proposal, exposed Prudential’s relatively weak U.S. presence.

To make matters worse, Prudential’s internet banking arm, Egg, fell short of expectations, but Bloomer couldn’t find an adequate buyer. Prudential eventually sold Egg to Citigroup for about $750 million in 2007, but the company estimated a $190 million operating loss from Egg, twice what was originally expected.

Investors’ outcry reached a fever pitch in 2004, when Bloomer surprise-launched a $1.3 billion rights issue in an effort to expand the firm’s U.K. business, despite having to assuage concerns the company needed to raise more capital to do so. The CEO was ousted less than a year later and replaced with HBO’s finance chief Mark Tucker. Bloomer called it “part of the ups and downs of corporate life.”

“We have had to manage the company through difficult times and not everything has made us popular,” he said at the time. “But my job has been to lead a transformation and Prudential is now set fair to deliver further substantial growth and returns.”

This story was originally featured on Fortune.com

Wolfspeed forecasts weak first-quarter revenue on manufacturing issues

(Reuters) – Wolfspeed forecast first-quarter revenue below estimates on Wednesday, anticipating manufacturing issues that could affect its production capacity amid slowing EV sales.

Shares of the chipmaker, however, surged around 6% in extended trading, as CEO Gregg Lowe said the company continues to see strong growth from its Mohawk Valley, New York-based chip fabrication facility.

In June, Wolfspeed had said it faced issues with equipment at its Durham-based 150-mm chip fabrication plant and which could potentially impact its first-quarter revenue by about $20 million.

Meanwhile, Wolfspeed’s Mohawk Valley chip fabrication plant is targeted to reach 25% of its operating capacity in the first quarter, ahead of schedule.

“Our 200mm device fab is currently producing solid results … This improved profitability gives us the confidence to accelerate the shift of our device fabrication to Mohawk Valley,” Lowe said in a statement.

Shares started to recover as the market acknowledged the cost benefits of the new 200-mm Mohawk Valley fabrication unit, compared to the old 150-mm one, said Michael Ashley Schulman, chief investment officer, Running Point Capital.

The company counts General Motors and Mercedes-Benz among its customers and makes chips using silicon carbide, which is more energy-efficient material than standard silicon, for tasks such as transmitting power from an electric car’s batteries to its motors.

Wolfspeed expects first-quarter revenue to be between $185 million and $215 million, the mid-point of which is below analysts’ average estimate of $211.7 million, according to LSEG data.

It expects adjusted loss per share to be between $1.09 and $0.90, compared with estimate of loss of 84 cents per share.

Revenue for the fourth-quarter came in at $200.1 million, compared with average estimate of $201.2 million.

Wolfspeed’s net loss per share was $1.39 per share, compared with loss of $0.73 per share a year earlier.

(Reporting by Jaspreet Singh in Bengaluru; Editing by Mohammed Safi Shamsi)

Ask an Advisor: I Want to Avoid Dumping My RMDs Into My Checking Account – What Are My Choices?

I am approaching the time when I’ll take required minimum distributions (RMDs) from my individual retirement account (IRA). I am in a quandary about what I can do with this anticipated largesse of cash. I do not necessarily need the money dumped into my checking account.

-Tommy

Retirees who don’t need the cash from required minimum distributions (RMDs) aren’t required to dump it directly into a checking account. Fortunately, a range of options exists that allows the RMDs to work more effectively for you.

Keep in mind that how you handle your RMDs may come with tax consequences, so it’s important to keep an eye out for those repercussions. Here’s what to do with RMDs when you don’t need the cash. (If you have additional questions about investing or retirement, this tool can help match you with potential advisors.)

Consider an In-Kind Distribution

An in-kind distribution allows you to transfer or withdraw the assets from your account while maintaining their invested status, rather than cashing them out.

The benefit of distributing assets this way is that your money will stay invested in a stock, exchange-traded fund, mutual fund or other investment. That may be particularly beneficial if you’ve experienced losses recently and would like to wait to see your investments recover before cashing them in.

One downside is that you’ll still need to be able to cover the tax bill that accompanies the distribution. (If you have additional questions about the tax repercussions of investing decisions, this tool can help match you with potential advisors.)

Opt for a QCD

A qualified charitable distribution (QCD) allows taxpayers to transfer assets directly to a charity, bypassing the need to pay taxes on the distribution.

QCDs are an option for folks who truly don’t need RMD money to pay for living expenses and would prefer to use it to fund charitable causes.

Additionally, strategically utilizing QCDs can result in other important retirement benefits. They remove money from the accountholder’s taxable income, which can reduce Medicare premiums. Plus, folks who utilize this strategy before RMD age (they become available for individuals who are 70 1/2 and older) can reduce the value of their overall tax-advantaged retirement account, minimizing RMDs in the future. (If you have additional questions about investing or retirement, this tool can help match you with potential advisors.)

If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

Try Converting to a Roth

As you approach RMD age, consider the benefits of strategically converting dollars from your traditional IRA to a Roth.

Roth accounts are not subject to RMDs, and executing a Roth conversion may allow you to both reduce future taxes and minimize or eliminate mandated distributions, giving you more control of that money in the future. Again, there will be a tax consequence to these conversions, so plan accordingly. (If you have additional questions about the tax repercussions of investing decisions, this tool can help match you with potential advisors.)

Bottom Line

There is a range of ways to approach RMDs that don’t involve dumping them in a checking account. But some of these approaches may have implications for your tax bill, investment strategy and retirement income. Consider working with a knowledgeable financial advisor if you’re unsure of how to proceed.

Tips for Finding a Financial Advisor

-

Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three vetted financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

-

Consider a few advisors before settling on one. It’s important to make sure you find someone you trust to manage your money. As you consider your options, these are the questions you should ask an advisor to ensure you make the right choice.

-

Keep an emergency fund on hand in case you run into unexpected expenses. An emergency fund should be liquid — in an account that isn’t at risk of significant fluctuation like the stock market. The tradeoff is that the value of liquid cash can be eroded by inflation. But a high-interest account allows you to earn compound interest. Compare savings accounts from these banks.

-

Are you a financial advisor looking to grow your business? SmartAsset AMP helps advisors connect with leads and offers marketing automation solutions so you can spend more time making conversions. Learn more about SmartAsset AMP.

Susannah Snider, CFP® is SmartAsset’s financial planning columnist, and answers reader questions on personal finance topics. Got a question you’d like answered? Email AskAnAdvisor@smartasset.com and your question may be answered in a future column.

Please note that Susannah is not a participant in the SmartAsset AMP platform and was an employee of SmartAsset at the time of writing.

Photo credit: ©Jen Barker Worley, ©iStock.com/Halfpoint, ©iStock.com/Tom Merton

The post Ask an Advisor: I Don’t Need Them ‘Dumped Into My Checking Account.’ What Can I Do With RMDs? appeared first on SmartAsset Blog.